Thermal Spray Coatings Market Size 2024-2028

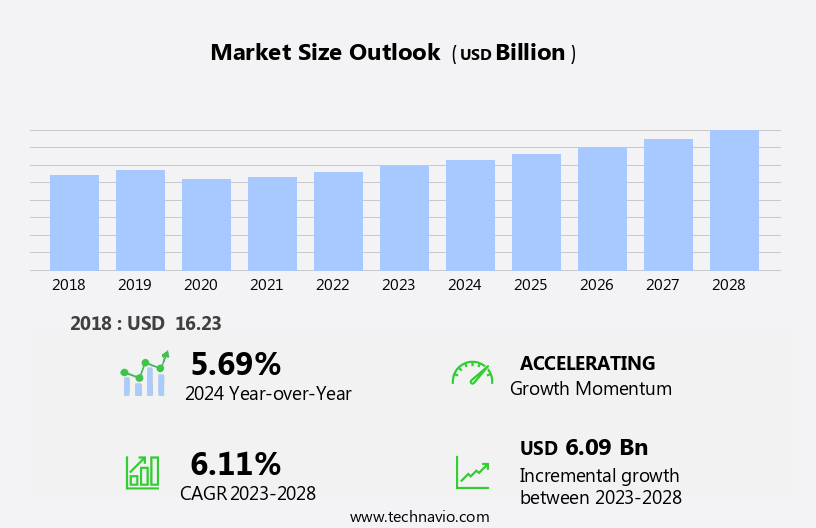

The thermal spray coatings market size is forecast to increase by USD 6.09 billion at a CAGR of 6.11% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for these coatings in various industries, particularly in healthcare. The healthcare sector's focus on improving medical equipment's surface properties to enhance their durability and resistance to corrosion is driving market growth. Additionally, the demand for advanced materials with superior surface characteristics is increasing, leading to a surge In the adoption of thermal spray coatings. However, the high cost of equipment required for thermal spray coating applications may hinder market growth. Despite this challenge, the market is expected to continue expanding as the benefits of thermal spray coatings become more widely recognized.

What will be the Size of the Thermal Spray Coatings Market During the Forecast Period?

- The market In the United States is experiencing significant growth due to the increasing demand for corrosion resistance and wear resistance solutions in various industries. Gas turbines, particularly those used in power generation and aerospace, are major consumers of thermal spray coatings due to their exposure to harsh environments, including high temperatures, moisture-laden conditions, and erosive forces. Thermal spray coatings provide effective protection against fire, cavitation, and chemical attacks. Beyond gas turbines, the market also caters to industries such as pains, medical, and electrical, where tailoring properties such as coating consistency, electrical insulation, and biocompatibility are essential. The demand for thermal spray coatings with anti-corrosion, antimicrobial properties, and occupational safety features is also on the rise.

- As industries strive for greater efficiency and sustainability, there is a growing focus on materials with heat impact resistance and low fossil fuel consumption, as well as those with minimal carbon dioxide emissions. Renewable energy plants, particularly those utilizing hydroelectric and wind power, are increasingly adopting thermal spray coatings to protect their infrastructure from the elements.

How is this Thermal Spray Coatings Industry segmented and which is the largest segment?

The thermal spray coatings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Combustion flame

- Electrical flame

- Material

- Metals and alloys

- Ceramics

- Polymers

- Others

- Geography

- North America

- Canada

- US

- APAC

- China

- Japan

- Europe

- Germany

- South America

- Middle East and Africa

- North America

By Type Insights

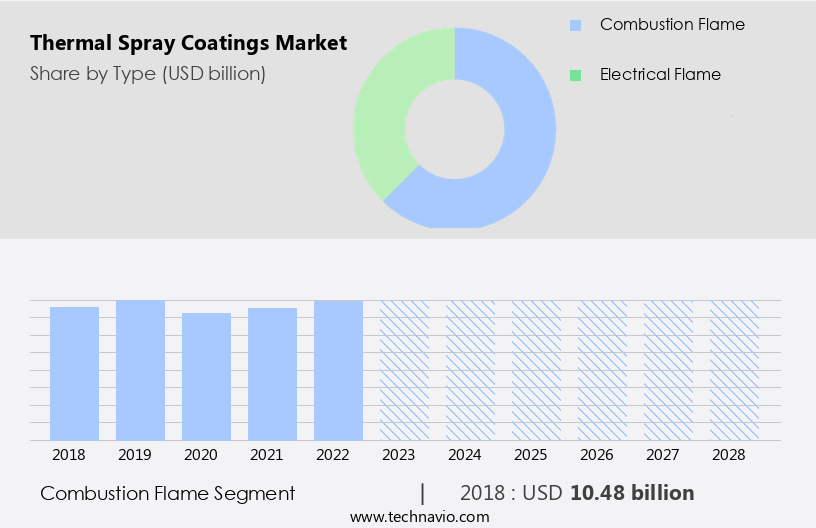

- The combustion flame segment is estimated to witness significant growth during the forecast period.

Thermal spray coatings are essential for enhancing the properties of various surfaces through techniques such as corrosion protection, wear resistance, thermal insulation, and mechanical improvement. One of these methods, combustion flame spraying, utilizes a high-temperature flame produced by the combustion of a gas and oxygen mixture. The molten coating material, usually in powder form, is then propelled onto the substrate, forming a coating upon solidification. This versatile process can apply a range of coating materials, including metals, ceramics, and specific polymers, to industries such as aerospace, paper, gas turbines, and orthopedic implants. Combustion flame spraying is widely used In the production of carbide coatings for gas turbine engines and aviation gas turbines in power generation.

The resulting coatings provide benefits like increased thermal barrier, dielectric strength, sliding wear resistance, and abradable materials.

Get a glance at the Thermal Spray Coatings Industry report of share of various segments Request Free Sample

The Combustion flame segment was valued at USD 10.48 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

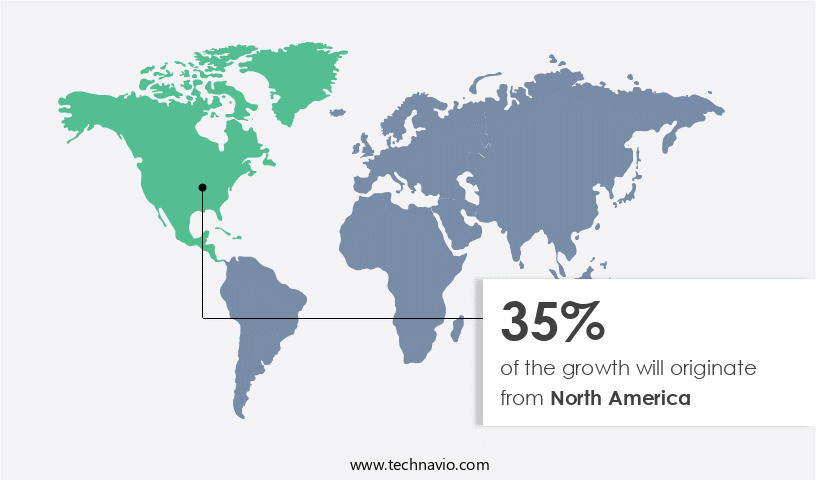

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market for thermal spray coatings is poised for significant expansion due to increasing demand from various industries, particularly automotive, power generation, and aerospace sectors. Thermal spray coatings are crucial for enhancing engine durability and efficiency In the aerospace industry, as demonstrated by major companies like General Electric and Pratt & Whitney's investments in advanced coatings. In power generation, thermal spray coatings play a vital role in extending the lifespan and efficiency of gas turbines, which are integral to energy production processes. Market leaders are expanding their businesses to cater to this growing demand. Thermal spray technologies, which involve the application of fine particles, offer invaluable benefits such as improved wear resistance, corrosion protection, and enhanced performance.

However, potential inhalation hazards associated with thermal spraying have led to government regulations, necessitating innovation in technology and material science to ensure safety.

Market Dynamics

Our thermal spray coatings market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Thermal Spray Coatings Industry?

Growing demand for thermal spray coatings in healthcare industry is the key driver of the market.

- Thermal spray coatings play a crucial role in enhancing the durability and functionality of various industries' components, particularly in sectors like healthcare, aerospace, and power generation. In the healthcare industry, these coatings are applied to medical devices and implants to increase their lifespan and improve performance. Biocompatible coatings, such as hydroxyapatite, are essential for medical implants and devices that come into contact with the human body, promoting osseointegration and reducing the risk of infections. The aerospace sector relies on thermal spray coatings for their corrosion resistance, heat impact resistance, and sliding wear resistance in high-performance applications. Ceramic coatings, like zirconia, alumina, and yttria, are widely used in aviation gas turbines for their excellent thermal barrier and high-temperature resistance properties.

- In the power generation sector, thermal spray coatings are applied to gas turbine engines, pumps, pipelines, and offshore structures to protect against wear, corrosion, and erosion caused by cavitation, abrasion, and erosive forces. These coatings also provide electrical insulation and resistance against decarbonization and fretting. In the pulp and paper industry, thermal spray coatings are used on paper manufacturing equipment, such as rolls and cylinders, to improve their wear resistance and reduce maintenance costs. In the oil and gas industry, thermal spray coatings are used to protect oil production equipment from corrosion and wear caused by harsh operating conditions.

- Cold spray technology is an emerging thermal spray technology used in various industries, including electronics, for its ability to deposit thick coatings with high bond strength and excellent adhesion to the substrate. This technology is also used In the production of high-voltage insulators, circuit boards, and electrical components. Thermal spray coatings offer numerous benefits, including resistance against wear, cavitation resistance, abrasion erosion resistance, and tailoring properties to meet specific application requirements. The market is expected to grow due to the increasing demand for high-performance coatings in various industries, including aerospace, power generation, and healthcare. The market's growth is also driven by the need for lightweight coatings, increasing industrial production, and refurbishment policies In the power generation sector.

- However, certain challenges, such as fine particles and inhalation hazards, need to be addressed to ensure occupational safety and comply with government regulations. Innovation in technology and material science continues to drive the development of new thermal spray technologies, such as plasma spray, electric arc spray, and flame spray, to meet the evolving needs of various industries. In conclusion, thermal spray coatings offer significant benefits in various industries, including improved wear resistance, corrosion protection, and electrical insulation. The market for thermal spray coatings is expected to grow due to the increasing demand for high-performance coatings in various industries, including aerospace, power generation, and healthcare.

- However, challenges such as fine particles and inhalation hazards need to be addressed to ensure occupational safety and regulatory compliance. Innovation in technology and material science continues to drive the development of new thermal spray technologies to meet the evolving needs of various industries.

What are the market trends shaping the Thermal Spray Coatings Industry?

Increase in demand for advanced materials with improved surface properties is the upcoming market trend.

- Thermal spray coatings play a crucial role in various industries by providing effective corrosion and wear resistance for components exposed to harsh conditions. These coatings are particularly valuable in sectors like oil and gas, marine, and infrastructure, where the risk of corrosion is high. The versatility of thermal spray technologies enables customization to meet the unique demands of different applications. For instance, In the aerospace industry, thermal spray coatings offer superior protection against high temperatures, erosion, and cavitation. In healthcare, biocompatible coatings enhance the performance and durability of medical devices, such as orthopedic implants and surgical instruments. Thermal spray coatings can be categorized based on the materials used, including ceramics, carbides, and polymers.

- Ceramic coatings, such as those made from zirconia, alumina, and yttria, provide excellent thermal barrier, abrasion resistance, and high-temperature performance. In contrast, carbide coatings offer superior wear resistance and scuff protection. Powder-based coatings, including those made from flammable solvents, are used in industries with high-performance requirements, such as gas turbines and aviation. The thermal spray coating process involves the application of fine particles onto a substrate using various techniques, including flame spray, plasma spray, and cold spray. These coatings offer numerous benefits, including improved surface properties, such as increased adhesion, electrical insulation, and resistance against wear, cavitation, and erosion.

- In addition, thermal spray coatings can be tailored to meet specific application requirements, such as heat impact resistance, sliding wear resistance, and abradable materials. Industries that rely on thermal spray coatings include power generation, pulp and paper, electronics, aerospace, and oil and gas. In power generation, thermal spray coatings are used to protect components in coal-fired power plants and gas turbine engines from corrosion and erosion. In the pulp and paper industry, thermal spray coatings are used to protect paper manufacturing equipment, such as rolls and cylinders, from wear and abrasion. In aerospace, thermal spray coatings are used to enhance the performance and durability of modern helicopters, locomotives, and aviation gas turbines.

- The market is driven by the increasing demand for high-performance coatings in various industries. The market is expected to grow significantly due to the increasing industrial production, refurbishment policies, and the need for fuel efficiency and reduced carbon dioxide emissions. Emerging economies are also expected to contribute significantly to the growth of the market due to the increasing demand for infrastructure development and the adoption of advanced technologies. In conclusion, thermal spray coatings offer a cost-effective and efficient solution to enhance the surface properties of materials and protect them from various forms of wear, corrosion, and thermal damage.

- The versatility of thermal spray technologies enables customization to meet the unique demands of different applications, making them an essential component in various industries, including power generation, aerospace, automotive, and healthcare. The market for thermal spray coatings is expected to grow significantly due to the increasing demand for high-performance coatings and the need for improved surface properties in various industries.

What challenges does Thermal Spray Coatings Industry face during the growth?

Cost of equipment for thermal spray coatings is a key challenge affecting the industry growth.

- Thermal spray coatings play a crucial role in enhancing the performance and durability of various industries' components, including gas turbines, by providing corrosion resistance, wear resistance, and electrical insulation. However, the significant cost associated with thermal spray equipment can hinder small- and medium-sized businesses from entering the market. The high initial investment and ongoing operating and maintenance expenses make it challenging for these businesses to compete. Gas turbines, such as those used in aviation and power generation, benefit from thermal spray coatings' ability to withstand extreme temperatures, moisture-laden conditions, and erosive forces like cavitation and particle erosion. In the aerospace industry, ceramic coatings offer sliding wear resistance and protection against high-temperature corrosion and hot gas impingement.

- The ceramics material segment, including zirconia, alumina, and yttria, is a significant contributor to the market. The healthcare services sector also relies on thermal spray coatings for corrosion protection and biocompatibility in medical devices, such as orthopedic implants and medical device coatings. In the pulp & paper industry, thermal spray coatings are used for paper manufacturing equipment, providing abrasion resistance, scuff protection, and erosion protection. Despite the benefits, the cost of thermal spray equipment remains a challenge. Thermal spray technologies, including flame spray, plasma spray, cold spray, and electric arc spray, require substantial capital investments. Operating and maintenance costs, including regular calibration and skilled personnel, add to the overall expenses.

- These costs impact the pricing structure of thermal spray coatings and can limit adoption rates, particularly for small- and medium-sized businesses. Innovation in technology and material science continues to drive advancements In thermal spray coatings, offering improved resistance against wear, cavitation resistance, and abrasion erosion resistance. The market's production capacity and footprint are expanding, with emerging economies contributing to the industrial production growth. The market's focus on fuel efficiency, lightweight coatings, and high-performance coatings is expected to drive further demand. The thermal spray coating process's ability to apply fine particles, providing a consistent coating, makes it a valuable solution for various industries.

- However, the potential inhalation hazards from fine particles and the carcinogenic nature of some coatings require adherence to government rules and regulations. The use of flammable solvents and the carcinogenic nature of some coatings also pose occupational safety concerns. The market's growth is influenced by various factors, including the increasing demand for fuel efficiency, refurbishment policies, and the need for high-performance coatings in industries like oil & gas, power generation, and aerospace. The market's expansion is also driven by the growing geriatric population, increasing healthcare services, and the need for biocompatible coatings in medical applications. In conclusion, the market's growth is influenced by various factors, including the need for corrosion protection, wear resistance, and electrical insulation in various industries.

- The cost considerations associated with thermal spray equipment and the potential health and safety concerns impact the market's competitiveness and adoption rates. Innovation in technology and material science continues to drive advancements In thermal spray coatings, offering improved performance and cost-effectiveness.

Exclusive Customer Landscape

The thermal spray coatings market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thermal spray coatings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, thermal spray coatings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

APS Materials Inc. - Our company specializes in applying thermal spray coatings, enhancing the durability and corrosion resistance of applicable equipment. These advanced coatings shield against environmental hazards, ensuring the longevity and optimal performance of industrial assets. By utilizing thermal spray technology, we deliver cost-effective and efficient solutions to mitigate the detrimental effects of corrosion.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- APS Materials Inc.

- Bodycote Plc

- Carpenter Technology Corp.

- CASTOLIN EUTECTIC

- CenterLine Windsor Ltd.

- Compagnie de Saint Gobain

- Curtiss Wright Corp.

- DURUM Wear Protection GmbH

- Fisher Barton

- GTV Wear Protection GmbH

- Hannecard Group

- Hoganas AB

- Kennametal Inc.

- Lincotek Group S.p.A.

- Linde Plc

- MORIMURA BROS. INC.

- OC Oerlikon Corp. AG

- Thermion Inc.

- TOCALO Co. Ltd.

- Treibacher Industrie AG

- Wall Colmonoy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Thermal spray coatings have gained significant attention in various industries due to their ability to enhance the performance and durability of components under harsh operating conditions. These coatings provide resistance against wear, corrosion, erosion, cavitation, and other damaging forces, making them an essential solution for numerous applications. The thermal spray coating market is driven by the increasing demand for improved component efficiency and extended service life in sectors such as power generation, aerospace, and manufacturing. The gas turbine industry is a major consumer of thermal spray coatings, with gas turbine engines requiring robust coatings to withstand the extreme temperatures and pressures they operate under.

Corrosion resistance is a critical factor driving the adoption of thermal spray coatings. In moisture-laden conditions and high-temperature environments, these coatings offer effective protection against the destructive effects of corrosion. In addition, they provide electrical insulation, ensuring the safe operation of components in high-voltage applications. Wear resistance is another essential attribute of thermal spray coatings. In industries such as oil and gas, pulp and paper, and mining, components are subjected to intense wear and abrasion. Thermal spray coatings, such as carbide coatings, offer superior resistance to these forces, increasing the lifespan of components and reducing maintenance costs. Ceramic coatings are a popular choice for thermal spray applications due to their high dielectric strength and sliding wear resistance.

These coatings are used extensively In the aerospace industry for applications such as engine components, aviation gas turbines, and modern helicopters. They also find use In the medical industry for medical device coatings and biomedical implants. Cold spray technology is an emerging thermal spray technique that uses fine particles to deposit coatings at low temperatures. This technology offers advantages such as reduced energy consumption and lower processing temperatures, making it an attractive alternative to traditional thermal spray methods. The thermal spray coating market is characterized by continuous innovation in technology and material science. New coatings are being developed to address specific application requirements, such as particle erosion, hot corrosion, metal-to-metal wear, fretting, decarbonization, and cavitation resistance.

These advancements are expected to expand the market's scope and increase its global footprint. Emerging economies are expected to play a significant role In the growth of the market. Industrial production In these regions is increasing, and there is a growing demand for high-performance coatings to improve component efficiency and reduce maintenance costs. Despite the numerous benefits of thermal spray coatings, there are challenges associated with their use. These include concerns regarding inhalation hazards from fine particles and the potential for environmental impact due to the use of flammable solvents and energy consumption. Regulatory bodies are addressing these issues through innovation in technology and the implementation of government rules.

In conclusion, the market is driven by the increasing demand for improved component performance and extended service life in various industries. The market is characterized by continuous innovation in technology and material science, with a focus on addressing specific application requirements. Despite challenges, the market is expected to grow, driven by the expanding industrial production in emerging economies and the need for fuel efficiency and reduced carbon dioxide emissions.

|

Thermal Spray Coatings Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

159 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.11% |

|

Market growth 2024-2028 |

USD 6.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.69 |

|

Key countries |

US, Canada, China, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Thermal Spray Coatings Market Research and Growth Report?

- CAGR of the Thermal Spray Coatings industry during the forecast period

- Detailed information on factors that will drive the Thermal Spray Coatings growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the thermal spray coatings market growth of industry companies

We can help! Our analysts can customize this thermal spray coatings market research report to meet your requirements.

RIA -

RIA -