Thermoformed Packaging Market Size 2026-2030

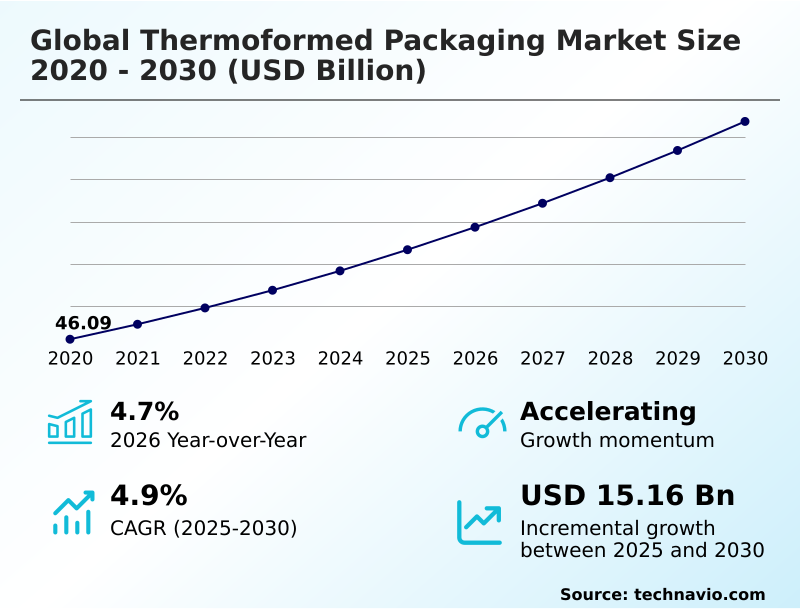

The thermoformed packaging market size is valued to increase by USD 15.16 billion, at a CAGR of 4.9% from 2025 to 2030. Increasing demand for convenient and sustainable food packaging will drive the thermoformed packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 45.6% growth during the forecast period.

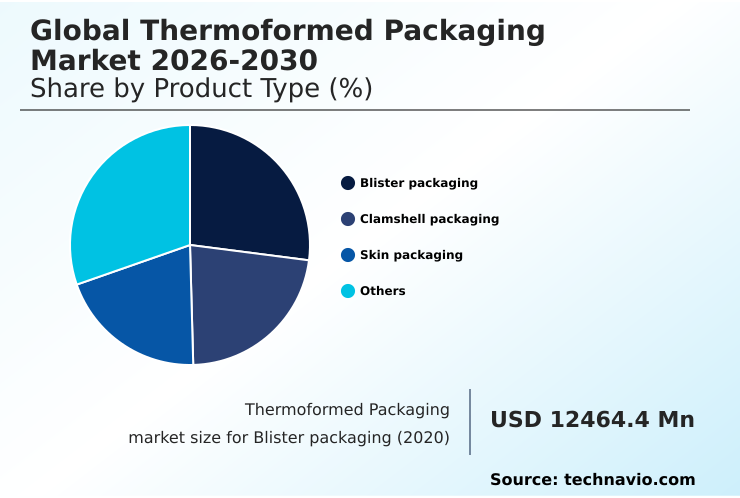

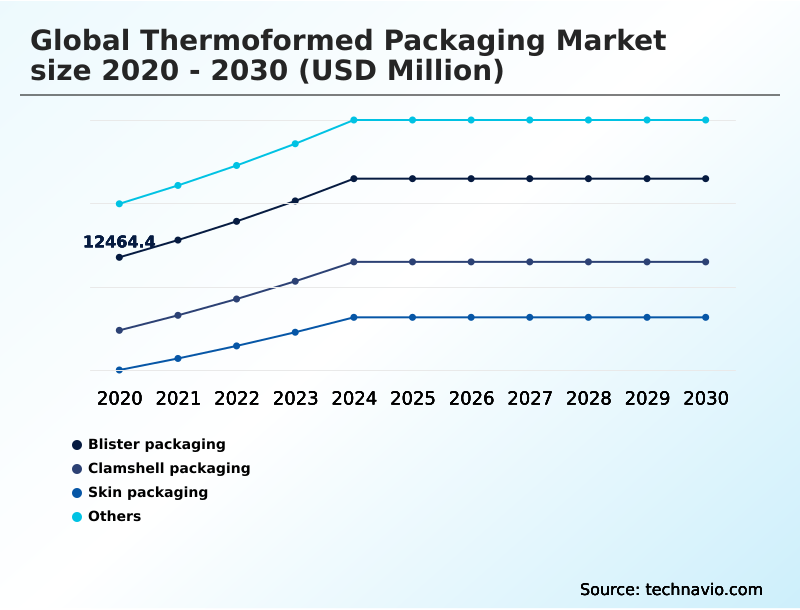

- By Product Type - Blister packaging segment was valued at USD 14.70 billion in 2024

- By End-user - Food and beverages segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 25.74 billion

- Market Future Opportunities: USD 15.16 billion

- CAGR from 2025 to 2030 : 4.9%

Market Summary

- The thermoformed packaging market is characterized by a dynamic interplay between technological innovation and sustainability imperatives. Growth is underpinned by persistent demand from the food, beverage, and pharmaceutical sectors for lightweight, protective, and cost-effective solutions. Key trends include the widespread adoption of mono-material designs and recycled content to meet circular economy goals.

- However, the industry navigates significant challenges, including volatile raw material pricing and intense competition from alternative formats like molded fiber. For instance, a food processing company aiming to improve supply chain efficiency might adopt thermoformed trays designed for automated filling and sealing lines, which can increase throughput by over 20%.

- This scenario highlights the balance between operational gains and the strategic necessity of aligning with evolving environmental regulations, such as extended producer responsibility schemes. Success hinges on manufacturers' ability to innovate materials and processes that deliver both performance and sustainability.

What will be the Size of the Thermoformed Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Thermoformed Packaging Market Segmented?

The thermoformed packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Blister packaging

- Clamshell packaging

- Skin packaging

- Others

- End-user

- Food and beverages

- Pharmaceuticals

- Personal care and cosmetics

- Others

- Material

- Plastic

- Paper

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- APAC

By Product Type Insights

The blister packaging segment is estimated to witness significant growth during the forecast period.

Blister packaging, a dominant segment, is evolving due to stringent pharmaceutical blister packaging regulations and demand for superior consumer goods packaging aesthetics.

Innovations are moving beyond traditional materials toward polyethylene terephthalate glycol (PETG) and high-density polyethylene (HDPE) as cold form foil (CFF) alternatives.

Achieving precise regulatory compliance validation is critical, driving advancements in heat-seal coating and tamper-evident design features for medical device sterile packaging. Ensuring food contact material safety through robust material traceability solutions is also a focus.

Enhanced die-cutting precision now allows for more complex designs, with some automated processes improving throughput by over 15%, meeting both functional and branding requirements for unit-dose blister packs.

The Blister packaging segment was valued at USD 14.70 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Thermoformed Packaging Market Demand is Rising in APAC Get Free Sample

The global landscape is led by APAC, which accounts for over 45% of the incremental growth, driven by rapid urbanization and rising disposable incomes.

In this region, deploying automated quality control systems has been shown to reduce defect rates by up to 25%. North America and Europe are mature markets focused on sustainability innovations like vacuum skin packaging (VSP) for shelf-life extension.

Investment in pressure forming technology enables the production of sterile medical trays with higher precision. As companies adopt plug-assist forming and in-mold labeling (IML), they achieve better material distribution and branding.

In sectors requiring electrostatic discharge (ESD) protection for electronics, specialized food-grade recycled polymers are gaining traction, supported by digital watermark integration for sorting.

These regional dynamics highlight a universal push toward advanced manufacturing and custom thermoformed inserts to meet specific end-user demands.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the thermoformed packaging market increasingly involve a cost-benefit analysis of rPET in packaging, weighing material costs against sustainability gains. For companies producing convenience foods, thermoformed packaging for ready-to-eat meals is a critical focus, with a strong push toward thermoformable paperboard for food containers as a plastic-alternative.

- The industry is actively comparing thermoforming vs injection molding for high-volume applications, where thermoforming process optimization for speed can offer a distinct advantage, in some cases improving cycle times by over 10%. In pharmaceuticals, developing sustainable alternatives to PVC blister packs is paramount, alongside clarifying regulations for medical device thermoformed trays.

- For consumer goods, key initiatives include improving the recyclability of thermoformed clamshells and designing thermoformed packaging for cosmetic gift sets that enhance brand value. Across sectors, advanced materials for thin-wall thermoforming are being explored to reduce plastic in thermoformed food trays. The impact of PPWR on thermoformed packaging is forcing a transition to the benefits of mono-material thermoformed packs.

- Meanwhile, challenges in recycling multi-layer thermoforms persist, pushing innovation in active packaging features in thermoforming and smart packaging integration with RFID. For industrial uses, thermoformed packaging for electronic components must meet specific protective standards, while recycled content verification for food packaging remains a critical compliance checkpoint.

What are the key market drivers leading to the rise in the adoption of Thermoformed Packaging Industry?

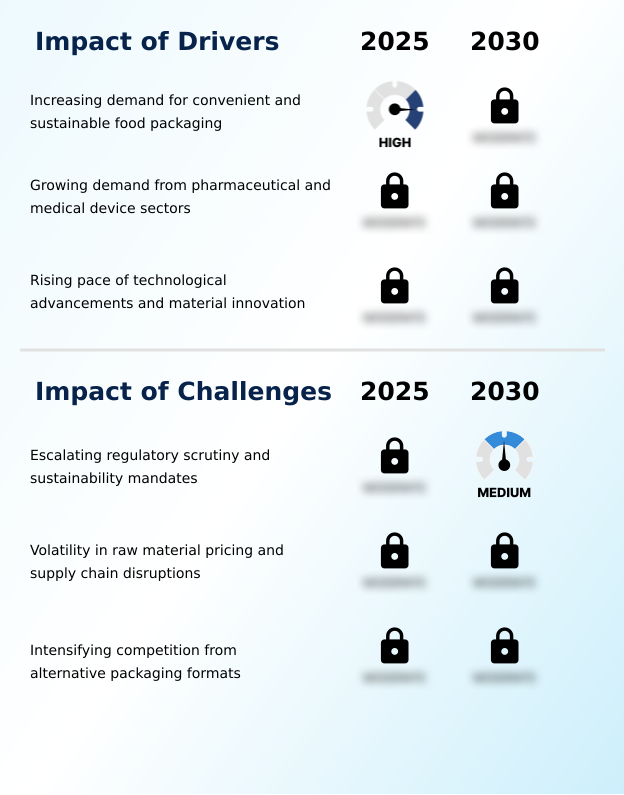

- Increasing global demand for convenient, portable, and sustainable packaging, especially within the food and beverage sector, serves as a primary driver for the market.

- The demand for extended shelf life and enhanced food safety is a primary market driver, fueling innovation in high-barrier thermoforming films and modified atmosphere packaging (MAP).

- The integration of oxygen scavenger integration within packaging substrates can extend the freshness of perishable goods by up to 50%, a critical factor for cold chain packaging integrity.

- Concurrently, the push for sustainable sourcing of polymers is accelerating the adoption of thermoformable paperboard, especially for food service disposable containers. Aseptic packaging integration is enabling new applications in shelf-stable products.

- The performance of these advanced materials is closely monitored through metrics like polymer melt flow index and packaging performance testing, ensuring they meet the rigorous demands of e-commerce ready packaging while using features like anti-fog additives for better retail presentation.

What are the market trends shaping the Thermoformed Packaging Industry?

- The proliferation of mono-material structures and solutions with high recycled content defines a key market trend. This industry-wide shift is driven by regulatory mandates and brand owner demand for a circular economy.

- The market is decisively shifting toward circularity, driven by the adoption of mono-material PET structures and high-percentage post-consumer recycled PET (rPET). This trend is a direct response to regulatory pressures, promoting a mechanical recycling process that is over 30% more efficient for single-polymer streams.

- Innovations in thin-wall thermoforming contribute to lightweighting for cost reduction, while advanced form-fill-seal (FFS) systems improve production speeds. The development of retortable thermoformed trays and biaxially oriented polypropylene (BOPP) lids that align with closed-loop recycling systems is critical.

- These advancements enable a more sustainable ecosystem, where advanced sorting technology can effectively process materials, and compostable bioplastic packaging offers an alternative end-of-life pathway, supporting a true circular economy packaging design.

What challenges does the Thermoformed Packaging Industry face during its growth?

- Escalating regulatory scrutiny combined with stringent sustainability mandates that vary by region presents a key challenge affecting industry-wide growth and material innovation.

- Navigating raw material volatility and stringent packaging waste reduction mandates presents a significant challenge. The reliance on materials like crystal clear polystyrene (PS) and polypropylene (PP) containers exposes manufacturers to price fluctuations, complicating supply chain packaging optimization.

- The technical difficulty of separating multi-layer coextrusion formats hinders end-of-life recyclability, as barrier layer materials often contaminate recycling streams, leading to polymer chain degradation. Compliance with extended producer responsibility (EPR) schemes requires significant investment in tooling design and optimization for mono-material solutions.

- Furthermore, ensuring consistent chemical resistance properties and accurate barrier property measurement across batches adds complexity, demanding robust quality control throughout the sheet extrusion process to meet performance standards.

Exclusive Technavio Analysis on Customer Landscape

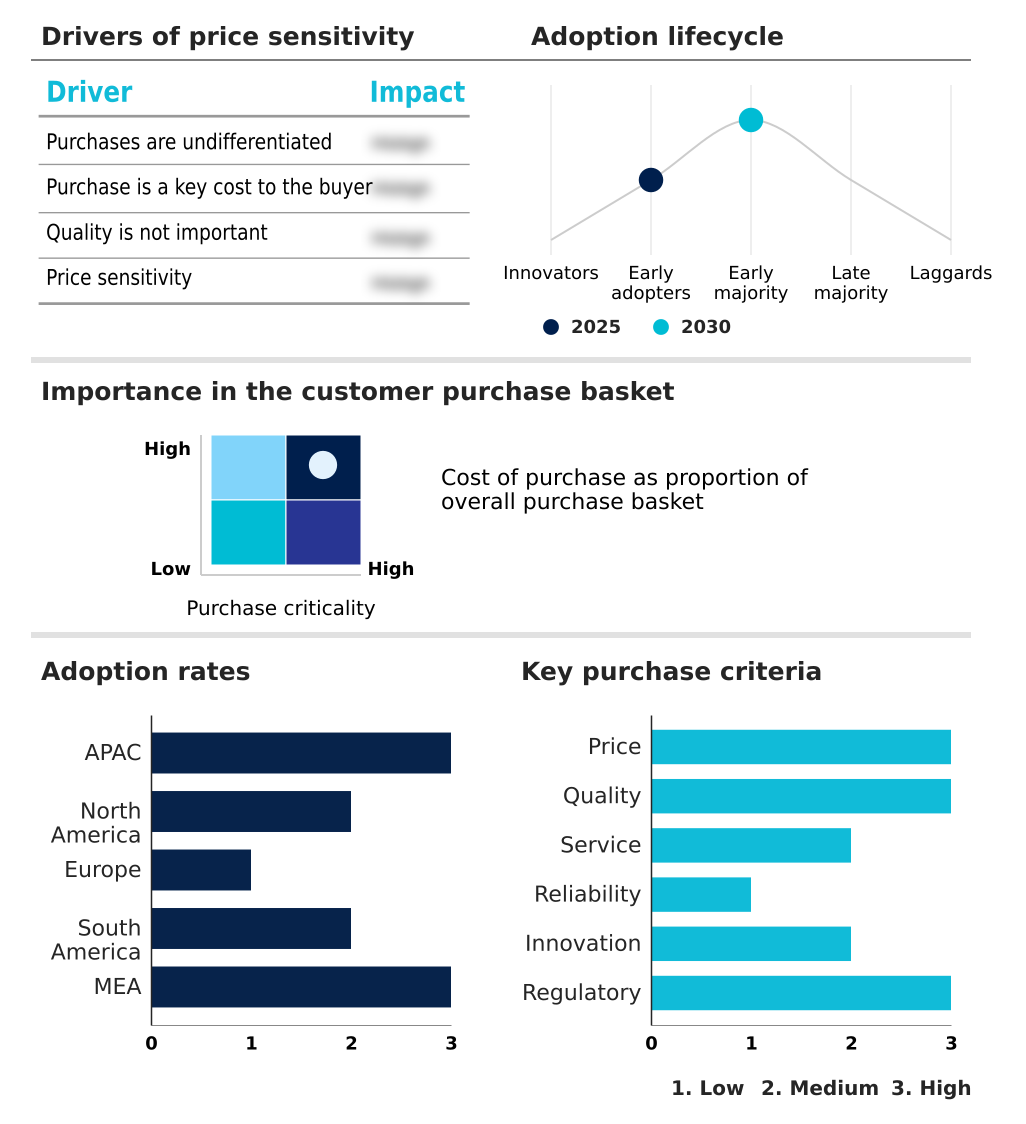

The thermoformed packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thermoformed packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Thermoformed Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, thermoformed packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Analyst research highlights a key offering in thermoformed packaging, focusing on recyclable trays engineered for food and beverage applications to meet performance and sustainability demands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- BBC Packaging SL

- Berry Global Inc.

- CTCI Production

- Dart Container Corp.

- DM THERMOFORMER

- Dordan Manufacturing Co.

- EasyPak LLC

- ENVAPLASTER SA

- Huhtamaki Oyj

- ITC Packaging

- Lacerta Group LLC

- NEFAB GROUP

- Placon Corp.

- Prent Corp.

- Sealed Air Corp.

- Silgan Holdings Inc.

- Sinclair and Rush Inc.

- Sonoco Products Co.

- USK Balaji Plast Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Thermoformed packaging market

- In September 2024, Placon Corp. launched its EcoStar 50S packaging material, made from post-consumer recycled plastic and engineered to meet evolving recycled-content regulations across the United States.

- In January 2025, the EU published its comprehensive Packaging and Packaging Waste Regulation (PPWR), establishing harmonized rules for circularity, including mandatory minimum recycled content targets for plastic packaging.

- In February 2025, ULMA Packaging launched its Width Flex technology, an automated system for thermoforming machines that adjusts film width in real-time to reduce plastic film waste by a significant margin.

- In September 2024, Toppan was involved in a collaborative project in Japan focused on commercializing a tray-to-tray recycling system to create a closed loop for thermoformed PET food trays.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Thermoformed Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.9% |

| Market growth 2026-2030 | USD 15157.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, South Africa, UAE, Saudi Arabia, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The thermoformed packaging market is undergoing a significant transformation driven by material science and process innovation. Demand is robust for solutions that balance performance with circularity, such as high-barrier thermoforming films designed for shelf-life extension and retortable thermoformed trays for convenience foods.

- A key boardroom consideration is the strategic shift toward post-consumer recycled PET (rPET) and other food-grade recycled polymers to comply with evolving regulations. The adoption of mono-material PET structures is critical for recyclability, moving away from complex multi-layer coextrusion.

- Technologies like form-fill-seal (FFS) systems and thin-wall thermoforming are being optimized for efficiency, with some manufacturers achieving a 15% reduction in material usage through lightweighting. Concurrently, the mechanical recycling process is being refined to handle a wider range of inputs, including polypropylene (PP) containers and materials with anti-fog additives.

- This convergence of technology and sustainability is redefining the competitive landscape for manufacturers.

What are the Key Data Covered in this Thermoformed Packaging Market Research and Growth Report?

-

What is the expected growth of the Thermoformed Packaging Market between 2026 and 2030?

-

USD 15.16 billion, at a CAGR of 4.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Blister packaging, Clamshell packaging, Skin packaging, and Others), End-user (Food and beverages, Pharmaceuticals, Personal care and cosmetics, and Others), Material (Plastic, and Paper) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for convenient and sustainable food packaging, Escalating regulatory scrutiny and sustainability mandates

-

-

Who are the major players in the Thermoformed Packaging Market?

-

Amcor Plc, BBC Packaging SL, Berry Global Inc., CTCI Production, Dart Container Corp., DM THERMOFORMER, Dordan Manufacturing Co., EasyPak LLC, ENVAPLASTER SA, Huhtamaki Oyj, ITC Packaging, Lacerta Group LLC, NEFAB GROUP, Placon Corp., Prent Corp., Sealed Air Corp., Silgan Holdings Inc., Sinclair and Rush Inc., Sonoco Products Co. and USK Balaji Plast Pvt. Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by sustainability and operational efficiency. The adoption of circular economy packaging design is not just a trend but a competitive necessity, with some solutions reducing plastic content by up to 80% compared to legacy formats. This shift is driven by packaging waste reduction mandates and a focus on end-of-life recyclability.

- Companies are leveraging automated quality control systems and robotic stacking and packing to enhance productivity, with some achieving a 15% reduction in line-changeover times. Furthermore, supply chain packaging optimization is critical, as e-commerce ready packaging formats must balance protection with lightweighting for cost reduction.

- These factors create a landscape where technological investment is directly tied to achieving both environmental compliance and measurable financial returns.

We can help! Our analysts can customize this thermoformed packaging market research report to meet your requirements.

RIA -

RIA -