Thin-Film Batteries Market Size 2024-2028

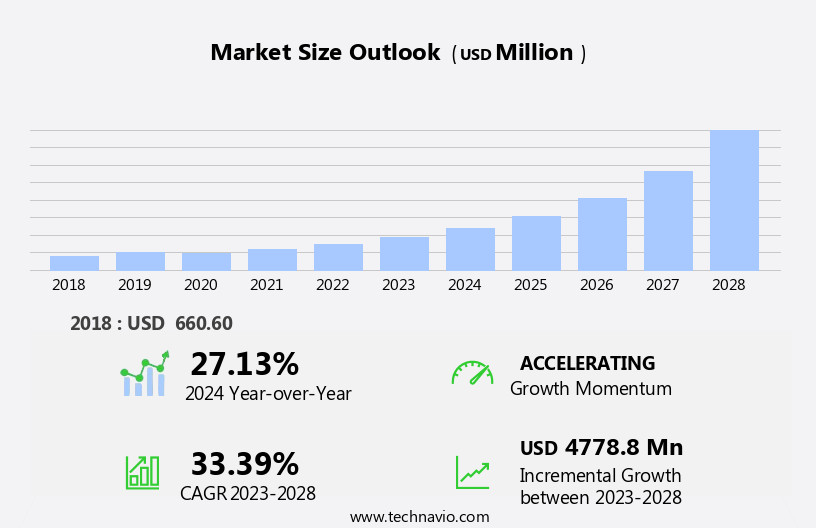

The thin-film batteries market size is forecast to increase by USD 4.78 billion, at a CAGR of 33.39% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing occurrences of hearing loss, leading to a surging demand for miniature and long-lasting batteries. Thin-film batteries, with their thin and flexible nature, cater perfectly to this need. Furthermore, the global shift towards environmentally friendly technologies is fueling the adoption of thin-film batteries, as they offer eco-friendly alternatives to traditional batteries. Additionally, the demand for flexible batteries with intelligent packaging, such as temperature patches, is increasing due to the need for miniaturization and customization in various industries. However, high manufacturing costs pose a substantial challenge to market growth.

- Companies must navigate this obstacle by implementing cost-effective production methods or exploring partnerships to share resources and reduce expenses. By addressing these challenges and capitalizing on the growing demand, market participants can seize opportunities in this dynamic and promising market.

What will be the Size of the Thin-Film Batteries Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The thin-film battery market continues to evolve, driven by advancements in technology and expanding applications across various sectors. Wireless charging technology is gaining traction, enabling convenient and contactless charging of devices. Lithium-ion polymer batteries, with their high energy density and long cycle life, are increasingly being adopted in electric vehicles (EVs) and portable electronics. Cell balancing techniques ensure optimal performance of battery modules by maintaining equal charge levels among individual cells. Battery testing plays a crucial role in assessing battery health and ensuring safety standards. Thermal management systems are essential for maintaining optimal operating temperatures and enhancing battery efficiency.

Aerospace and military applications demand high-performance batteries with long cycle life, energy density, and safety features. Machine learning (ML) and artificial intelligence (AI) are being integrated into battery systems for predictive maintenance and optimization. Power electronics and inverter technology are essential components of battery systems, enabling efficient energy conversion and management. Battery monitoring systems provide real-time data on battery health and performance, enabling proactive maintenance and improving overall system efficiency. Capacity fade, self-discharge rate, and internal resistance are critical factors impacting battery performance and lifespan. Battery packaging, current collectors, and electrode coating technologies are continually evolving to improve battery efficiency and reduce manufacturing costs.

Renewable energy integration and grid-scale energy storage are emerging applications for thin-film batteries, requiring high power density, fast-charging capabilities, and long cycle life. Safety standards and quality control measures are essential for ensuring reliable and safe battery systems. Big data analytics and cyclic voltammetry (CV) techniques are being used to optimize battery design and improve battery performance. Low-temperature and high-temperature batteries are being developed to address specific application requirements. Galvanostatic charge-discharge and DC-DC converters are essential components of battery systems, enabling efficient energy conversion and management. Discharge rate and regulatory compliance are critical factors impacting battery market growth and competitiveness.

How is this Thin-Film Batteries Industry segmented?

The thin-film batteries industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Smart wearables

- Smart cards

- Medical devices

- Others

- Battery Type

- Rechargeable

- Disposable

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

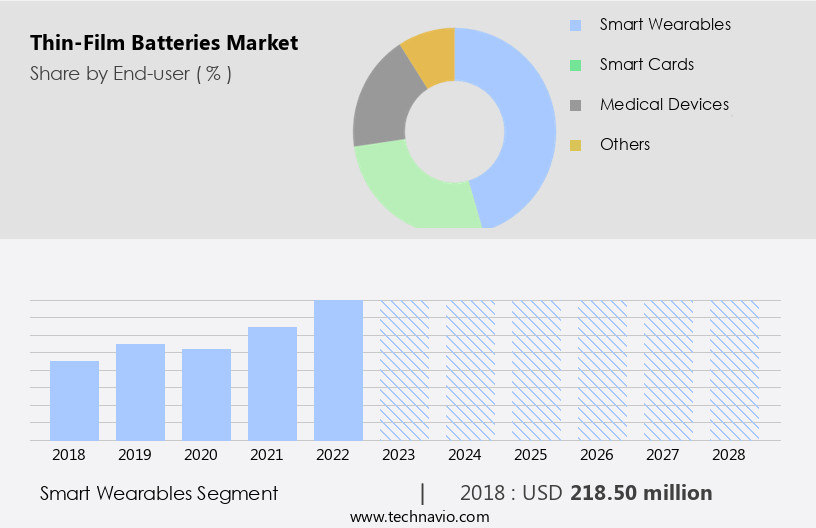

The smart wearables segment is estimated to witness significant growth during the forecast period.

The market is experiencing notable growth, driven by the increasing demand for wearable electronics in various industries, including sports and fitness, military and protection, transportation, fashion, architecture, entertainment, and medicine. This demand is fueled by the rapid advancements in nanotechnology and the miniaturization of electronic components, leading to the development of more sophisticated and efficient thin-film batteries for smart wearable devices. In the realm of grid-scale energy storage, thin-film batteries are gaining traction due to their high energy density and power density, making them suitable for renewable energy integration. The automotive sector, particularly electric vehicles (EVs), is another significant market for thin-film batteries, as they offer advantages such as fast-charging capabilities, long cycle life, and low self-discharge rates.

Medical devices and aerospace applications are also adopting thin-film batteries due to their lightweight and compact design, which is essential in these industries. In addition, the integration of machine learning (ML), artificial intelligence (AI), power electronics, and inverter technology is driving the development of advanced battery monitoring systems, cell balancing, and thermal management solutions. Safety standards and quality control are crucial factors in the market, as these batteries are used in various applications that require high reliability and performance. Regulatory compliance is another essential aspect, as governments and regulatory bodies are implementing stringent safety regulations for battery manufacturing and usage.

The market is also witnessing the emergence of solid-state batteries, which offer advantages such as longer cycle life, higher energy density, and improved safety compared to traditional lithium-ion batteries. However, challenges such as high production costs and limited commercial availability are hindering their widespread adoption. Battery testing, battery packaging, current collectors, and electrode coating are essential components of the market, with ongoing research focusing on improving their performance and reducing their production costs. The market is expected to continue evolving, with advancements in battery technology and increasing demand from various industries driving growth.

The Smart wearables segment was valued at USD 218.50 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

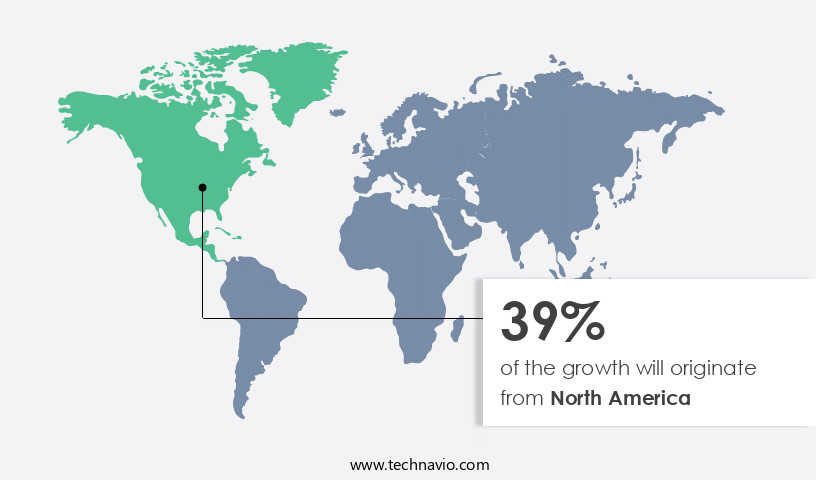

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth due to the increasing adoption of these batteries in various sectors. In the realm of grid-scale energy storage, thin-film batteries offer advantages such as high energy density and long cycle life, making them a preferred choice for renewable energy integration. In the medical devices industry, thin-film batteries' small size and lightweight design are ideal for powering wearable devices and implantable medical devices. The electric vehicle (EV) sector is also witnessing a surge in the use of thin-film batteries, particularly lithium-ion polymer batteries, due to their fast-charging capabilities and long cycle life.

In the realm of cell assembly, advancements in solid-state batteries and electrode coating technologies are driving innovation in the market. Thin-film batteries are also finding applications in battery monitoring systems, portable electronics, and machine learning applications, where low self-discharge rates and high power density are essential. Thermal management and safety standards are critical factors in the market, with regulatory compliance and battery testing playing significant roles in ensuring product quality and safety. In the aerospace and military sectors, thin-film batteries' high power density, long cycle life, and ability to operate in extreme temperatures make them an attractive option for powering various applications.

The integration of power electronics, inverter technology, and artificial intelligence (AI) is also driving the market, enabling advancements in battery monitoring, cell balancing, and battery pack design. As the market evolves, there is a growing focus on improving energy density, cycle life, and fast-charging capabilities, as well as developing low-temperature and high-temperature batteries for various applications. Overall, the market is experiencing significant growth and innovation, driven by the increasing demand for high-performance batteries in various sectors, including grid-scale energy storage, medical devices, electric vehicles, and portable electronics. The market is expected to continue growing as advancements in battery technology and integration with other technologies such as power electronics, inverter technology, and AI drive new applications and use cases.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Thin-Film Batteries Industry?

- The prevalence of hearing loss serves as the primary market driver, as its increasing occurrences continue to fuel market growth.

- Thin-film batteries have gained significant attention in the energy storage market due to their potential advantages over traditional batteries. These batteries use techniques such as x-ray diffraction (XRD) during cell assembly to ensure optimal material alignment and improve battery performance. Thin-film batteries also offer advantages in grid-scale energy storage, including longer cycle life, faster charging times, and higher energy density. Solid-state batteries, a type of thin-film battery, are particularly promising for medical devices and electric vehicles (EVs) due to their improved safety and capacity retention. However, challenges such as capacity fade, battery packaging, current collectors, and electrode coating must be addressed to achieve commercial viability.

- Self-discharge rate is another critical factor affecting the performance and cost-effectiveness of thin-film batteries. Thin-film batteries are expected to play a significant role in the future of energy storage, offering improved efficiency, longer cycle life, and faster charging times compared to conventional batteries. The market for thin-film batteries is expected to grow as the demand for renewable energy sources increases and the need for more efficient and cost-effective energy storage solutions becomes more pressing.

What are the market trends shaping the Thin-Film Batteries Industry?

- The increasing preference for eco-friendly batteries is a notable trend in the current market. This demand stems from growing environmental concerns and the need for sustainable energy solutions.

- The market is experiencing significant growth due to the increasing demand for environmentally friendly energy storage solutions. Thin-film batteries, which are made from non-toxic materials, offer a lower carbon footprint compared to conventional batteries. This environmental advantage is driving the market, as concerns over the impact of batteries on the environment grow, and governments implement regulations and policies to reduce carbon emissions and promote clean energy sources. Thin-film batteries are particularly suitable for applications requiring wireless charging, such as electric vehicles and portable devices. In addition, they are used in various industries, including aerospace and military, where lightweight, high-performance batteries are essential.

- Thin-film batteries offer several advantages, including cell balancing, thermal management, and long cycle life. Advancements in power electronics, inverter technology, and machine learning (ML) are also contributing to the growth of the market. ML algorithms are used to optimize battery performance and improve battery management systems, while power electronics and inverter technology enable efficient energy conversion and management. Battery testing and quality assurance are crucial in the market. Thorough testing ensures the reliability and safety of these batteries, which is essential in applications where safety is paramount, such as in aerospace and military applications. Effective thermal management is also essential to ensure the batteries perform optimally and safely, particularly in high-temperature environments.

What challenges does the Thin-Film Batteries Industry face during its growth?

- The escalating manufacturing costs represent a significant barrier to growth within the industry.

- Thin-film batteries, manufactured using intricate processes and specialized equipment, carry a higher cost due to the use of expensive materials such as lithium, cobalt, and other rare-earth elements. These essential components increase the final product's cost. The complex manufacturing process, which includes deposition, patterning, and packaging, further contributes to the high production cost. Despite these challenges, advancements in technology are driving the adoption of thin-film batteries in various applications. Artificial intelligence (AI) and battery monitoring systems enable better quality control and adherence to safety standards. Big data analytics plays a crucial role in optimizing energy density, cycle life, fast-charging capabilities, and low-temperature performance.

- Thin-film batteries' high energy density and long cycle life make them suitable for portable electronics, particularly those requiring high power density and extended usage. Fast-charging capabilities and low-temperature performance are essential features for applications in extreme environments. Ensuring safety standards is critical, especially in industries where battery failures can lead to catastrophic consequences. By focusing on improving manufacturing processes and optimizing the use of raw materials, the market for thin-film batteries is expected to grow.

Exclusive Customer Landscape

The thin-film batteries market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the thin-film batteries market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, thin-film batteries market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Angstrom Engineering Inc. - This company specializes in the design and production of high-performance sports equipment, leveraging advanced materials and innovative technologies to enhance athlete experience and optimize performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Angstrom Engineering Inc.

- Avery Dennison Corp.

- Coreshell Technologies

- Cymbet Corp.

- EIT InnoEnergy SE

- Enfucell

- Fujitsu Ltd.

- Imprint Energy

- Jenax Inc.

- Koch Industries Inc.

- Kurt J Lesker Co.

- LG Corp.

- RRC power solutions GmbH

- Samsung Electronics Co. Ltd.

- Shenzhen Grepow Battery Co. Ltd.

- Soleras Advanced Coatings BV

- STMicroelectronics International N.V.

- The Swatch Group Ltd.

- Ultralife Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Thin-Film Batteries Market

- In January 2024, Panasonic Corporation and Toyota Motor Corporation announced a strategic collaboration to develop and commercialize solid-state thin-film lithium-ion batteries for electric vehicles (EVs) by 2027 (Panasonic Press Release, 2024). This partnership marks a significant stride in the automotive industry's pursuit of more efficient and sustainable energy storage solutions.

- In March 2024, 24M Technologies, a leading thin-film lithium-ion battery manufacturer, secured a USD 100 million Series D funding round, led by Breakthrough Energy Ventures and ARPA-E (U.S. Department of Energy), to scale up production and accelerate the commercialization of their flexible, lightweight batteries (24M Technologies Press Release, 2024). This investment underscores the growing investor interest in thin-film batteries for various applications, including portable electronics and renewable energy storage.

- In May 2024, the European Union's Horizon Europe research and innovation program granted a â¬10 million grant to a consortium led by the Helmholtz-Zentrum Berlin for a research project focused on developing high-performance, flexible, and scalable thin-film lithium-ion batteries (European Commission Press Release, 2024). This initiative represents a key regulatory approval and government initiative to support the advancement of thin-film battery technology in Europe.

- In April 2025, Solvay, a global chemical company, and Sion Power, a developer of lithium-sulfur rechargeable batteries based on thin-film technology, announced a strategic partnership to commercialize the latter's batteries for stationary energy storage applications (Solvay Press Release, 2025). This collaboration is expected to bring the high-energy-density, long-life batteries to the market, addressing the growing demand for reliable and efficient energy storage solutions for renewable energy integration.

Research Analyst Overview

- The market encompasses various technologies, including magnesium-ion, sodium-ion, lithium-sulfur, and zinc-ion batteries, among others. One significant challenge in this sector is the risk of short circuits, which can lead to thermal runaway and hinder the market's growth. Solid-state electrolytes are gaining traction as they offer improved safety and longer storage life compared to traditional liquid electrolytes. Consumer electronics, IoT devices, power tools, and smart homes are major applications driving the demand for thin-film batteries. Operating at ambient temperatures, these batteries cater to high-energy and high-power applications in fuel cells, hydrogen fuel cells, electric scooters, electric bicycles, smart grids, and spacecraft applications.

- Thin-film deposition techniques, such as laser scribing and roll-to-roll processing, enable mass production and cost reduction. All-solid-state batteries, including lithium-ion, lithium-sulfur, and lithium-air batteries, are being explored for their potential in various sectors. Calendar life and electrochemical degradation are critical factors influencing the market's growth and development. Flow batteries and redox flow batteries are also part of the thin-film batteries landscape, offering advantages in terms of energy density, power density, and scalability. As the market evolves, 3D printing and other advanced manufacturing techniques may further enhance the production process and expand the applications of thin-film batteries.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Thin-Film Batteries Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 33.39% |

|

Market growth 2024-2028 |

USD 4778.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

27.13 |

|

Key countries |

US, China, Germany, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Thin-Film Batteries Market Research and Growth Report?

- CAGR of the Thin-Film Batteries industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the thin-film batteries market growth of industry companies

We can help! Our analysts can customize this thin-film batteries market research report to meet your requirements.

RIA -

RIA -