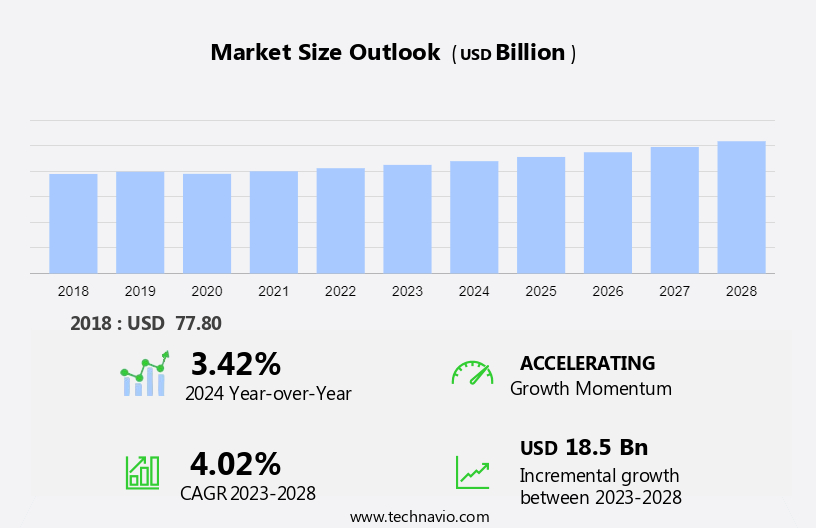

Architectural Coatings Market Size 2024-2028

The architectural coatings market size is forecast to increase by USD 18.5 billion at a CAGR of 4.02% between 2023 and 2028.

- The market is experiencing significant growth due to various trends and factors. One of the key drivers is the increasing adoption of UV-curable architectural coatings, which offer several advantages such as faster curing time and improved durability. Another trend influencing the market is the growing focus on eco-friendly and bio-based coatings and coating raw materials. This shift is being driven by increasing environmental concerns and regulations, as well as consumer demand for sustainable products.

- However, the market is also facing challenges, including the volatility in prices of raw materials used in architectural coatings and protective coatings, which can impact the cost structure of manufacturers and ultimately, the end price for consumers. Overall, these trends and challenges are shaping the future growth of the market.

What will be the Size of the Architectural Coatings Market During the Forecast Period?

To learn more about the market report, Request Free Sample

- The market encompasses a range of products, including paints, primers, sealers, varnishes, inks, and ceramics, used for both decorative and protective purposes in the construction sector. Market dynamics are influenced by consumer preferences, with a growing demand for eco-friendly, low-volatile organic compound (VOC) alternatives, such as water-borne coatings, including acrylic, alkyd, epoxy, polyurethane, polyester, urethane, PTFE, and PVDF. The construction boom, particularly in the residential sector, fuels market growth. However, supply chain disruptions and increasing raw material costs pose challenges. Technological advancements, such as nanocoating and solvent-borne versus water-borne technology, continue to shape the market landscape. Resin type remains a significant factor in product differentiation.

How is this Architectural Coatings Industry segmented and which is the largest segment?

The architectural coatings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

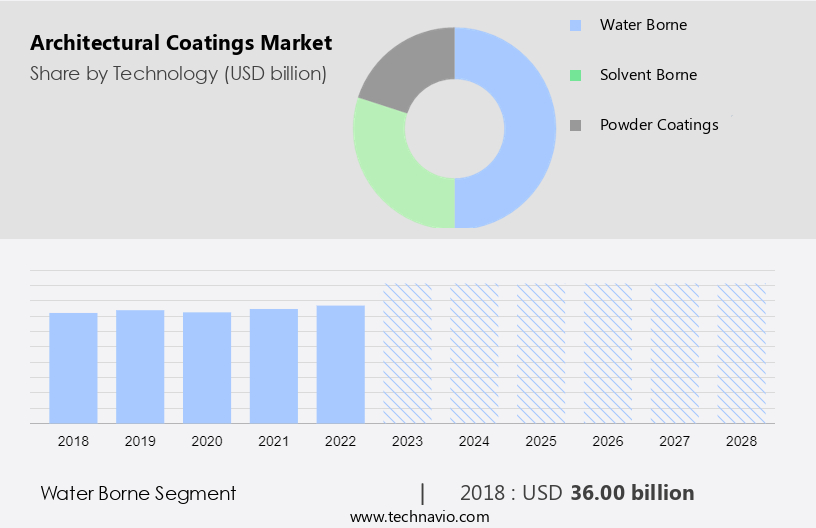

- Technology

- Water borne

- Solvent borne

- Powder coatings

- Type

- Interior

- Exterior

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- France

- Middle East and Africa

- South America

- APAC

By Technology Insights

- The water borne segment is estimated to witness significant growth during the forecast period.

The market has witnessed notable growth in the segment of water borne coatings due to increasing environmental consciousness and stringent regulations limiting the emissions of volatile organic compounds (VOCs) and toxic gases like sulfur dioxide and carbon dioxide. Water borne coatings, which replace harmful chemical solvents with water as a solvent, offer significant benefits, including reduced VOC emissions, improved health and safety, and ease of application. Eco-friendly water borne paint offerings have gained popularity in both residential and commercial sectors for their low odor, easy cleanup, and enhanced durability.

Get a glance at the Architectural Coatings Industry report of share of various segments. Request Free Sample

The water borne segment was valued at USD 36.00 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

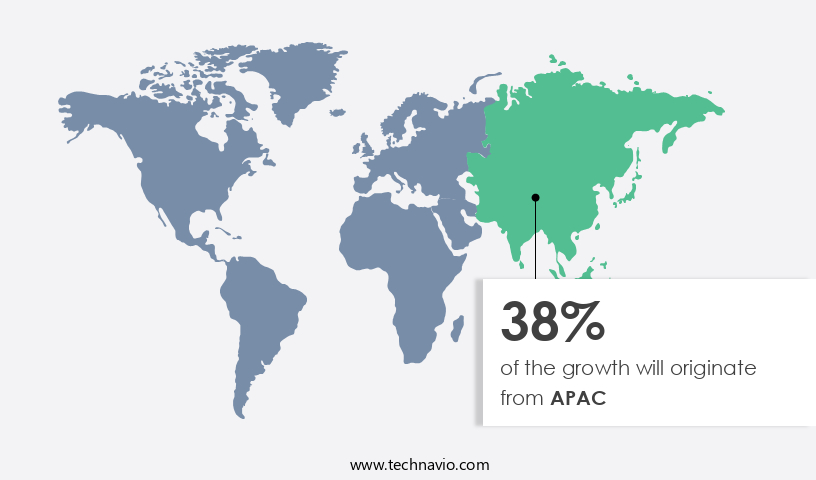

- APAC is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The APAC region is a significant contributor to The market, driven by economic growth, urbanization, and construction activities. Architectural coatings, including decorative paints, decoative coatings, primers, sealers, varnishes, and inks, are essential for enhancing the aesthetics and protecting the surfaces of residential, commercial, and institutional buildings. The market in APAC encompasses a wide range of products to cater to various uses and end-user preferences. One of the market segments experiencing notable growth is water-based architectural coatings, which offer advantages such as low VOC emissions, easy application, and excellent adhesion properties.

Architectural Coatings Market Market Dynamics

Our architectural coatings market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Architectural Coatings Industry?

Rising adoption of UV-curable architectural coatings is the key driver of the market.

- Architectural coatings, including decorative paints, primers, sealers, varnishes, inks, and specialty coatings like lacquers, powders, and stains, play a significant role in the construction sector. The market for these coatings is driven by the consumer preference for aesthetics, durability, and environmental concerns. The construction boom in both residential and non-residential sectors fuels the demand for architectural coatings. Two primary types of architectural coatings are solvent borne and water borne. Solvent borne coatings, such as alkyd, epoxy, and polyurethane, offer excellent performance but have high VOC emissions, leading to air pollution concerns. In contrast, water borne coatings, including acrylic, polyester, PVDF, and PVF, are eco-friendly and have gained popularity due to regulatory changes and consumer preferences for green coatings.

UV-curable coatings, a newer technology, exhibit high performance and offer quick assembly-line benefits. These coatings have gained traction in the architectural industry due to their excellent abrasion property, faster cure time, and chemical and corrosive resistance. companies are investing in research and development to produce UV-curable architectural coatings with enhanced scratch and mar resistance. Despite their high initial cost, the demand for UV-curable architectures coatings is expected to grow due to their long-term benefits. However, supply chain disruptions and raw material price fluctuations can impact the market. The industry is also witnessing technological advancements, such as nanocoating and ceramics, which offer superior durability and performance.

Overall, the market is dynamic, with various factors influencing its growth and trends.

What are the market trends shaping the Architectural Coatings Industry?

Increasing focus on bio-based and eco-friendly architectural coatings is the upcoming trend in the market.

- The market is witnessing a significant shift towards decorative eco-friendly alternatives, such as water borne coatings, nanocoatings, and green coatings. This trend is driven by growing consumer preferences for sustainable building materials and increasing regulatory changes aimed at reducing VOC emissions from solvent borne coatings. The construction boom in both residential and non-residential sectors is fueling the demand for architectural coatings, with various functions including primers, sealers, varnishes, paints, inks, ceramics, and lacquers. Manufacturers are responding to these market dynamics by developing coatings made from resin types like acrylic, alkyd, epoxy, polyurethane, polyester, and PVDF. These coatings offer comparable performance to traditional solvent borne coatings while reducing environmental impact.

The use of water borne coatings, in particular, is gaining popularity due to their lower VOC emissions and ease of application. However, supply chain disruptions caused by raw material shortages and logistical challenges can impact the market. Despite these challenges, the market is expected to continue growing as the construction sector adapts to the changing regulatory landscape and consumer preferences. The adoption of advanced technologies like powder coatings and PTFE coatings is also expected to drive market growth. Overall, the market is evolving to meet the demands of a more sustainable and eco-conscious construction industry.

What challenges does Architectural Coatings Industry face during the growth?

Volatility in prices of raw materials used in architectural coatings is a key challenge affecting the industry growth.

- Architectural coatings, including decorative paints, primers, sealers, varnishes, inks, and lacquers, are essential components of the construction sector. The market for these coatings is subject to various dynamics, with raw material prices being a significant factor. The reliance on petrochemical inputs, particularly feedstock, contributes to price volatility. Global oil prices, geopolitical events, and supply chain disruptions can impact the cost of raw materials, such as petroleum solvents, which are widely used in solvent-borne coatings. Titanium dioxide (TiO2), a primary ingredient in architectural coatings, accounts for a substantial portion of raw material costs, ranging from 20% to 30%. Its limited supply and lack of substitutes make it a critical factor in price fluctuations.

Moreover, consumer preferences are shifting towards eco-friendly alternatives, such as water-borne coatings and green coatings, due to increasing concerns over VOC emissions and air pollution. The construction boom in both residential and non-residential sectors is driving demand for architectural coatings. However, regulatory changes, such as restrictions on solvent borne coatings, are compelling manufacturers to invest in alternative technologies, including nanocoating and powder coatings. Acrylic, alkyd, epoxy, polyurethane, polyester, urethane, PTFE, and PVDF are popular resin types used in architectural coatings, with each offering unique advantages in terms of performance and sustainability. In summary, the market is influenced by various factors, including raw material prices, consumer preferences, and regulatory changes.

The reliance on petrochemical inputs, particularly TiO2, contributes to price volatility. The shift towards eco-friendly alternatives, such as water-borne and green coatings, is a response to environmental concerns. The construction boom and regulatory changes are driving demand and technological innovation in the market.

Customer Landscape

The architectural coatings market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market growth analysis report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akzo Nobel NV - The company, a leading provider in the architectural coatings industry, offers high-quality solutions under its distinguished brands: Dulux, International, Sikkens, and Interpon. These brands cater to various market segments, providing architectural coatings that ensure durability, aesthetics, and sustainability for commercial and residential buildings in the US market.

The architectural coatings industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Asian Paints Ltd.

- Axalta Coating Systems Ltd.

- BASF SE

- Benjamin Moore and Co.

- Berger Paints India Ltd

- Diamond Vogel

- Dow Inc.

- Dunn Edwards Corp.

- Hempel AS

- Jotun AS

- Kansai Paint Co. Ltd.

- Munzing Chemie GmbH

- Nippon Paint India Pvt. Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- Sto SE and Co. KGaA

- The Chemours Co.

- The Sherwin Williams Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Latest Market Developments and News

-

In December 2024, Sherwin-Williams launched a new line of eco-friendly architectural coatings designed to improve indoor air quality. These coatings use low-VOC and non-toxic ingredients, targeting the increasing demand for sustainable and health-conscious building materials in residential and commercial projects.

-

In November 2024, PPG Industries expanded its architectural coatings portfolio with the introduction of a durable, weather-resistant paint product. The new coatings are formulated to withstand extreme weather conditions, providing long-lasting protection for exterior surfaces in both urban and coastal environments.

-

In October 2024, AkzoNobel announced a partnership with a leading technology firm to develop smart architectural coatings that can change color based on temperature or light exposure. This innovation aims to offer more dynamic and energy-efficient solutions for building exteriors and interiors.

-

In September 2024, Benjamin Moore introduced a new line of premium architectural coatings that incorporate antimicrobial properties, aimed at enhancing cleanliness and hygiene in high-traffic spaces such as hospitals, schools, and commercial offices.

Research Analyst Overview

Architectural coatings refer to a broad category of protective and decorative products applied to various surfaces to enhance their appearance and durability. These coatings include, but are not limited to, paints, primers, sealers, varnishes, inks, and lacquers. The market for architectural coatings is driven by several factors, including the construction boom, consumer preferences, and technological advancements. The construction sector's growth is a significant factor driving the demand for architectural coatings. With the increasing number of residential and non-residential construction projects, the need for coatings to protect and enhance the appearance of buildings is on the rise. Consumer preferences also play a crucial role in the market's dynamics.

With growing awareness of environmental concerns, there is a rising demand for eco-friendly coatings, such as water-borne and green coatings. The market is segmented based on resin type, including acrylic, alkyd, epoxy, polyurethane, polyester, urethane, PTFE, and PVDF. Solvent-borne and water-borne coatings are the two primary technologies used in the production of architectural coatings. Solvent-borne coatings offer excellent coverage and fast drying times but have higher VOC emissions, making them less environmentally friendly. In contrast, water-borne coatings have lower VOC emissions and are more eco-friendly, but they may require longer drying times. The supply chain for architectural coatings is subject to disruptions due to various factors, including raw material availability, transportation issues, and regulatory changes.

For instance, air pollution regulations have led to the phasing out of certain solvents used in coatings production, necessitating the development of alternative technologies. The market for architectural coatings is diverse and dynamic, with various players offering a range of products catering to different applications and customer needs. Nanocoating technology is a recent development in the market, offering superior durability and resistance to wear and tear. Powder coatings and stains are also popular choices for their ease of application and low VOC emissions. In conclusion, the market is driven by several factors, including the construction boom, consumer preferences, and technological advancements. The market is segmented based on resin type and technology, with solvent-borne and water-borne coatings being the primary choices. The market is subject to supply chain disruptions due to various factors, and regulatory changes are a significant challenge. Despite these challenges, the market offers significant growth opportunities for players offering eco-friendly and technologically advanced coatings solutions.

|

Architectural Coatings Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.02% |

|

Market growth 2024-2028 |

USD 18.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.42 |

|

Key countries |

China, US, Germany, India, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the Architectural Coatings industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -