Thrombosis Drugs Market Size 2024-2028

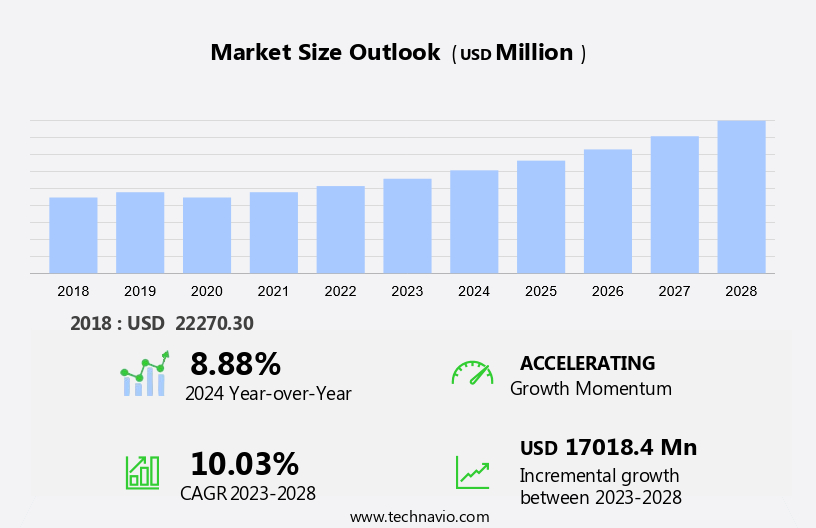

The thrombosis drugs market size is forecast to increase by USD 17.02 billion at a CAGR of 10.03% between 2023 and 2028. The market is experiencing significant growth, driven by the introduction of novel oral anticoagulants (NOACs) that offer improved efficacy and reduced side effects compared to traditional anticoagulants. NOACs have gained popularity due to their convenience and ease of use, leading to a shift from injectable anticoagulants. Another growth factor is the rising prevalence of sedentary lifestyles and obesity, which increase the risk of thrombosis. Thrombotic disorders, including deep vein thrombosis, pulmonary embolism, stroke, myocardial infarction, and others, are major health concerns worldwide. However, the market faces challenges, including the strong side effects of anticoagulants, such as bleeding risks, and the high cost of these pharmaceutical equipment and medications. Regulatory approvals and reimbursement policies also impact market growth. In summary, the market is witnessing growth due to the introduction of NOACs and the increasing prevalence of thrombosis risk factors but faces challenges related to side effects and cost.

What will be the Size of the Market During the Forecast Period?

The market encompasses a range of medications used for the treatment and prevention of thrombotic disorders, which are conditions characterized by the formation of blood clots in the arteries or veins. Thrombotic disorders pose a significant health risk to various populations, particularly the geriatric population and those undergoing surgical procedures. Thrombotic disorders, including deep vein thrombosis (DVT), pulmonary embolism (PE), stroke, myocardial infarction, and others, are prevalent in the US due to sedentary lifestyles, obesity, and the increasing prevalence of chronic conditions such as diabetes and cardiovascular diseases. According to the Centers for Disease Control and Prevention (CDC), approximately 900,000 Americans experience a DVT each year, and about 100,000 die from PE annually. The healthcare expenditure on thrombosis medications is substantial, driven by the increasing prevalence of thrombotic disorders and the growing demand for effective treatment and prevention options. Thrombosis medications include antiplatelet drugs, thrombolytic drugs, and novel oral anticoagulants. Personalized medicine and advanced drug delivery systems are emerging trends in the market.

Moreover, the market is driven by the increasing prevalence of thrombotic disorders, particularly in the geriatric population and those undergoing surgical procedures. Factors such as sedentary lifestyles, obesity, chronic conditions like diabetes, cardiovascular disease, and infectious diseases contribute to the rising incidence of these disorders. Thrombosis medications, including antiplatelet drugs, thrombolytic drugs, and novel oral anticoagulants, play a crucial role in treatment and prevention. The aging population, with its higher susceptibility to thrombotic disorders, is a significant market opportunity. Drug development in this area is ongoing, with a focus on personalized medicine, drug delivery systems, outpatient management, home healthcare, long-acting formulations, transdermal patches, and implantable devices. The regulatory framework for thrombosis drugs is stringent, ensuring safety and efficacy. The pipeline analysis of thrombosis drugs is strong, with several promising candidates in various stages of development. The market is expected to grow significantly due to the increasing healthcare expenditure and the rising obesity rates.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

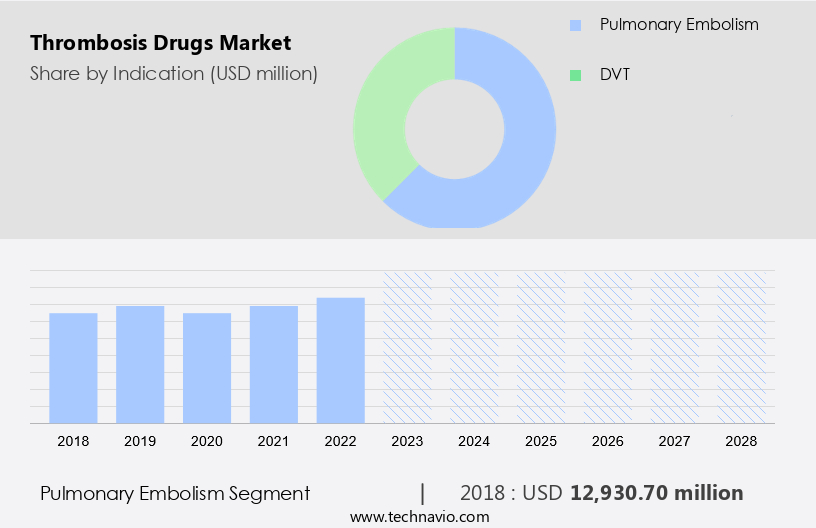

- Indication

- Pulmonary embolism

- DVT

- Geography

- North America

- US

- Europe

- UK

- France

- Norway

- Asia

- Japan

- Rest of World (ROW)

- North America

By Indication Insights

The pulmonary embolism segment is estimated to witness significant growth during the forecast period. Pulmonary embolism is a serious health condition characterized by a blood clot obstructing the pulmonary arteries in the lungs. These clots typically originate in other veins and travel to the lungs via the bloodstream. The condition can be life-threatening if left untreated, with a high mortality rate. Risk factors for pulmonary embolism include immobility, obesity, and advanced age. Other factors, such as fractures, smoking, and heart diseases, can also increase the risk. With an incidence of around 600-700 cases per million people, pulmonary embolism is a common blood disorder. The aging population, with its increased prevalence of cardiovascular diseases and diabetes, is a significant demographic at risk.

The market encompasses the development and distribution of medications used for the treatment and prevention of thrombotic disorders, including deep vein thrombosis, pulmonary embolism, heart attacks, stroke, myocardial infarction, and venous thromboembolism. With an aging population and rising prevalence of sedentary lifestyles, obesity, and chronic conditions such as diabetes and cardiovascular diseases, the demand for thrombosis medications continues to escalate.

Get a glance at the market share of various segments Request Free Sample

The pulmonary embolism segment was valued at USD 12.93 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

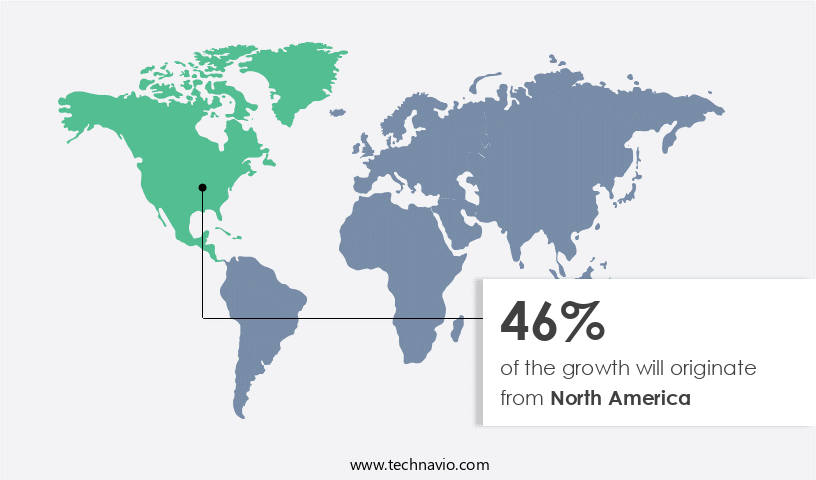

North America is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The North American market has witnessed notable expansion due to the rising incidence of Deep Vein Thrombosis (DVT) and Pulmonary Embolism (PE) in the region. The US, in particular, holds a substantial market share, accounting for approximately 22.98% of the global revenue. According to the Centers for Disease Control and Prevention (CDC), the US experiences around 900,000 new cases of DVT and PE annually. These conditions pose a serious health risk, with PE being particularly life-threatening. As a result, there has been a swell in demand for effective thrombosis treatments. Key players in the market include Bayer and Anthos Therapeutics, among others. This drug holds promise in the treatment of cancer-related thrombosis. Hospital pharmacies play a crucial role in the distribution of thrombosis drugs. Healthcare expenditures on these medications continue to rise as the number of cases increases. The US healthcare spending on prescription drugs is projected to reach USD 650 billion by 2026.

Similarly, thrombosis drugs are expected to contribute significantly to this figure. In conclusion, the North American market is poised for continued growth due to the increasing prevalence of DVT and PE, the life-threatening nature of PE, and the availability of effective treatments. Market participants, including Bayer and Anthos Therapeutics, are investing in research and development to bring innovative solutions to market. Hospital pharmacies will remain key players in the distribution of these essential medications.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The introduction of novel oral anticoagulants is the key driver of the market. The market has experienced significant growth due to the introduction of new oral anticoagulants. Previously, most anticoagulants were administered via the parenteral route, which was not well-received by patients due to its invasive nature and poor adherence. In response, market companies developed oral anticoagulants, which have gained popularity among medical professionals and patients alike. Notable new-generation oral anticoagulants include direct thrombin inhibitors like dabigatran and anti-Xa agents such as ELIQUIS (apixaban), SAVAYSA, LIXIANA (edoxaban), and XARELTO (rivaroxaban). These drugs have revolutionized the treatment of thrombosis, offering improved efficacy and convenience. The patient epidemiology, regulatory framework, and pipeline analysis continue to shape the market.

Diagnostic techniques and clinical trials play a crucial role in the discovery of new thrombosis drugs. Obesity rates and the increasing prevalence of thrombosis are key factors driving market growth. Online, retail, and hospital pharmacies are the primary distribution channels for thrombosis drugs. The regulatory framework ensures the safety and efficacy of these drugs, while ongoing clinical trials and drug discovery efforts continue to expand the market pipeline.

Market Trends

Sedentary lifestyle is the key trend in the market. Thrombosis, a condition characterized by the formation of blood clots in the arteries or veins, is a significant health concern worldwide. Obesity and advanced age are leading risk factors for thrombosis, with obesity being a result of both genetic and environmental factors. A sedentary lifestyle, characterized by little to no physical activity, is a major contributor to obesity and the subsequent risk of thrombosis. Deep Vein Thrombosis (DVT), a type of thrombosis, can occur when the muscles in the legs do not contract, preventing proper blood flow.

Moreover, this can lead to the formation of blood clots in deep veins. The global market is witnessing significant growth due to the increasing prevalence of thrombosis, particularly in the context of cancer-related thrombosis, pulmonary embolism, and atrial fibrillation. Key players in the market include Bayer and Anthos Therapeutics, with the latter developing Abelacimab, an antiplasmin antibody for thrombosis treatment. Thus, such trends will shape the growth of the market during the forecast period.

Market Challenge

Strong side-effects of anticoagulants is a key challenge affecting market growth. Thrombosis drugs, also known as anticoagulants or blood thinners, are essential medications used to prevent and treat cardiovascular crises, such as deep vein thrombosis (DVT) and pulmonary embolism. These drugs work by inhibiting the body's natural blood clotting process, allowing blood to flow freely and preventing new clots from forming. However, their use comes with risks, including increased bleeding, especially in trauma cases. The market is dominated by several leading brands, offering a range of treatments, including antiplatelet therapy with aspirin and other agents. Local competition also exists, providing cost-effective alternatives. Hematology, the branch of medicine dealing with blood disorders, plays a crucial role in the diagnosis and treatment of thrombosis.

Despite the risks, the prevalence of chronic DVT is significant, necessitating the continued use of thrombosis drugs. The market for these medications is expected to grow due to the increasing awareness of thrombosis risks and the availability of new treatments. As a professional assistant, it is important to understand the benefits and risks associated with thrombosis drugs and their role in managing cardiovascular crises. Use header tags effectively to structure content. Ensure proper use of internal and external links. Optimize images with relevant alt tags and descriptions. Regularly update content to maintain its relevance and accuracy.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Aspen Pharmacare Holdings Ltd: The company offers the thrombosis portfolio which is comprised largely of a broad range of specialist injectable anticoagulants.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AuroMedics Pharma LLC

- Baxter International Inc.

- Bayer AG

- Biogen Inc.

- Boehringer Ingelheim International GmbH

- Bristol Myers Squibb Co.

- Daiichi Sankyo Co. Ltd.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- GoodRx Holdings Inc.

- Grifols SA

- Inari Medical Inc.

- Italfarmaco Holding SPA

- Johnson and Johnson Services Inc.

- Pfizer Inc.

- Sanofi SA

- Vasudha Pharma Chem Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Thrombotic disorders, including deep vein thrombosis (DVT), pulmonary embolism (PE), stroke, myocardial infarction, and others, pose a significant health risk to the global population. The aging population and sedentary lifestyles contribute to the rising prevalence of thrombotic disorders, particularly in the geriatric population and those with chronic conditions such as diabetes, obesity, and cardiovascular diseases. Thrombosis medications, including anticoagulants, antiplatelet drugs, and thrombolytic drugs, play a crucial role in the treatment and prevention of these disorders. The market for thrombosis medications is expected to grow due to increasing healthcare expenditure and the development of novel oral anticoagulants, personalized medicine, drug delivery systems, and long-acting formulations.

Moreover, thrombosis medications are administered through various routes, including oral medications, self-administered injectables, transdermal patches, implantable devices, and intravenous infusions. Diagnostic imaging techniques and laboratory assays are essential in the diagnosis and monitoring of thrombotic disorders, particularly venous thromboembolism. Factor Xa inhibitors and direct thrombin inhibitors are among the emerging thrombosis medications with label extensions and innovative route of administration. The regulatory framework for thrombosis drugs is stringent, with trade regulations and clinical trials playing a crucial role in bringing new drugs to market. Thrombosis medications are available through hospital pharmacies, retail pharmacies, and online pharmacies, making them accessible to a wide range of patients. The market is competitive, with several global brands and local competition. The market is also influenced by cardiovascular crises, such as atrial fibrillation and trauma cases, and the ongoing research in hematology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

144 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.03% |

|

Market Growth 2024-2028 |

USD 17.01 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.88 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 46% |

|

Key countries |

US, France, Norway, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Aspen Pharmacare Holdings Ltd., AuroMedics Pharma LLC, Baxter International Inc., Bayer AG, Biogen Inc., Boehringer Ingelheim International GmbH, Bristol Myers Squibb Co., Daiichi Sankyo Co. Ltd., F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, GoodRx Holdings Inc., Grifols SA, Inari Medical Inc., Italfarmaco Holding SPA, Johnson and Johnson Services Inc., Pfizer Inc., Sanofi SA, Vasudha Pharma Chem Ltd., and Viatris Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -