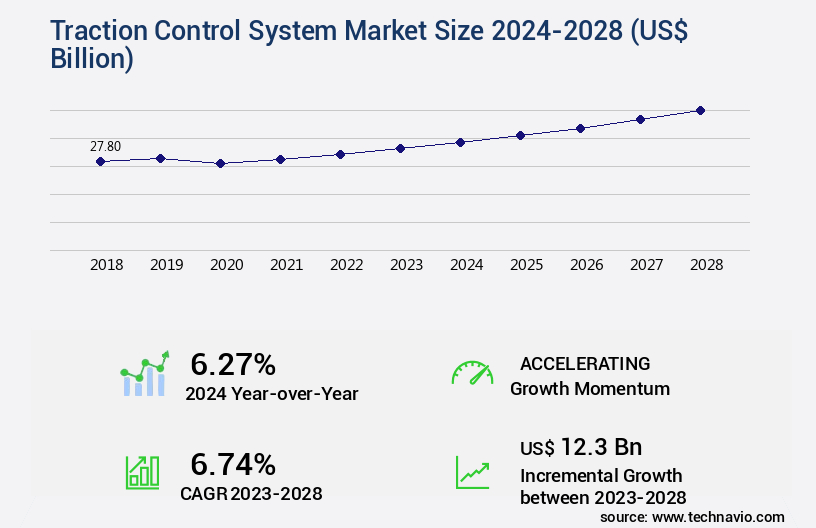

Traction Control System Market Size 2024-2028

The traction control system market size is valued to increase USD 12.3 billion, at a CAGR of 6.74% from 2023 to 2028. Robust demand for autonomous vehicles will drive the traction control system market.

Major Market Trends & Insights

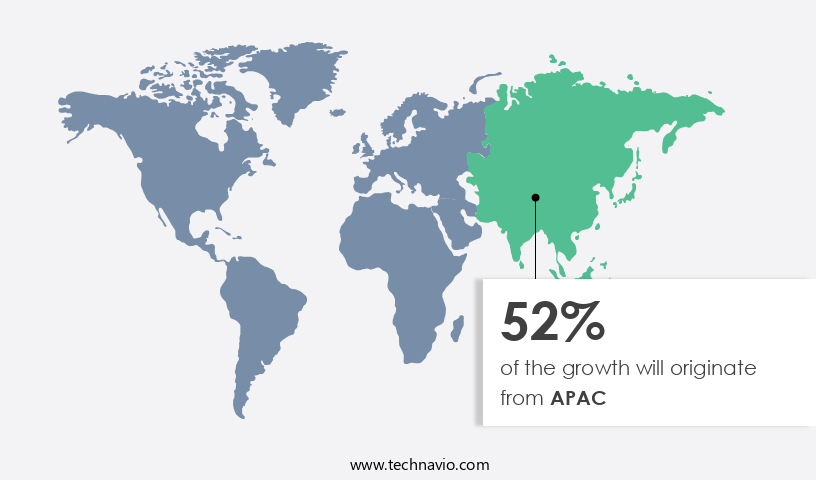

- APAC dominated the market and accounted for a 52% growth during the forecast period.

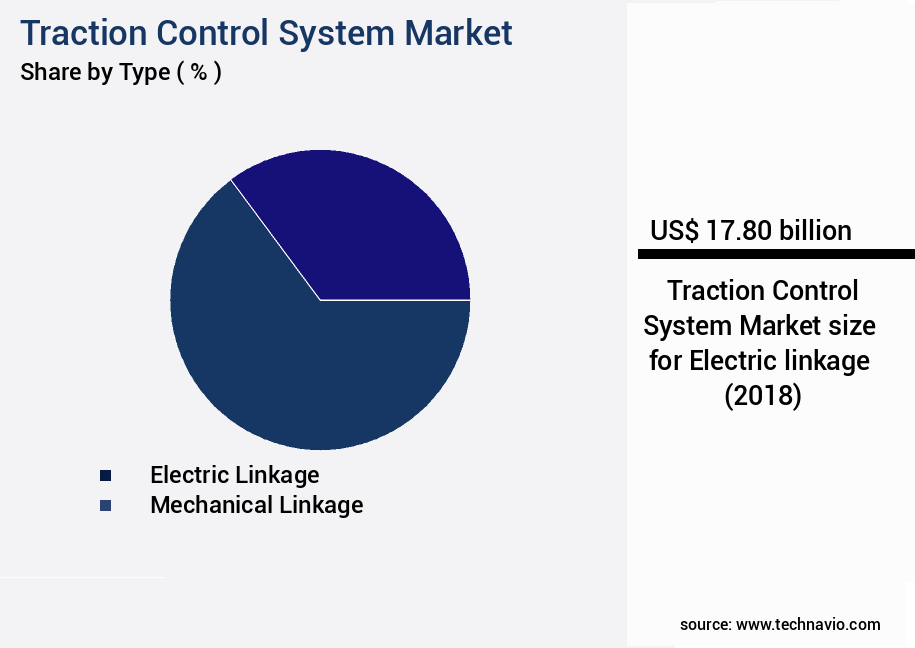

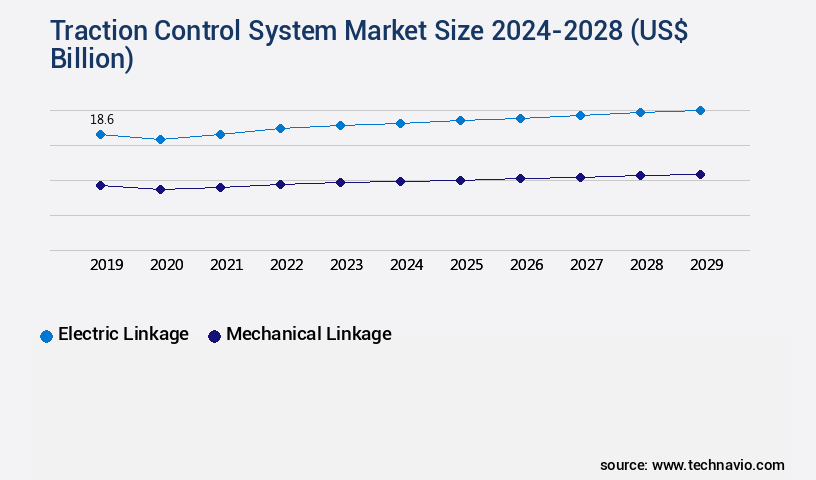

- By Type - Electric linkage segment was valued at USD 17.80 billion in 2022

- By Vehicle Type - Passenger cars segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 58.99 billion

- Market Future Opportunities: USD 12.30 billion

- CAGR from 2023 to 2028 : 6.74%

Market Summary

- The market represents a significant and dynamic sector in the automotive industry, driven by the robust demand for autonomous vehicles and the increasing adoption of advanced driver assistance systems (ADAS). Traction control systems, which ensure optimal vehicle stability and performance by managing engine power delivery to each wheel, are a crucial component of these advanced technologies. However, the technological complexity associated with these systems poses challenges for manufacturers and suppliers. According to a recent study, the market is expected to account for over 25% of the overall ADAS market share by 2025.

- This growth is fueled by the ongoing development of electric and hybrid vehicles, which require advanced traction control systems to optimize power distribution and improve overall performance. Despite these opportunities, market participants face regulatory hurdles, particularly in Europe and North America, where stringent safety standards necessitate continuous innovation and compliance.

What will be the Size of the Traction Control System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Traction Control System Market Segmented ?

The traction control system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Electric linkage

- Mechanical linkage

- Vehicle Type

- Passenger cars

- Light commercial vehicles

- Heavy commercial vehicles

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The electric linkage segment is estimated to witness significant growth during the forecast period.

In the dynamic and evolving the market, electric linkages held a significant market share in 2023, driven by the increasing adoption of electric and hybrid vehicles. These advanced systems facilitate seamless communication and coordination between electric powertrain components and the traction control system, ensuring precise power distribution for optimal traction and enhanced vehicle performance. Electric linkages play a vital role in transmitting signals and commands between the traction control module and various vehicle components, such as brakes, engine, and wheel sensors. These systems utilize sensors like yaw rate, lateral acceleration, longitudinal acceleration, steering angle, wheel speed, and tire slip detection to calculate slip ratios and initiate traction control intervention when necessary.

Advanced features like roll mitigation, vehicle stability assist, drift control, active torque vectoring, and vehicle dynamics control further enhance the system's capabilities. Electronic stability programs employ hydraulic control units, brake assist systems, electronic differential locks, and dynamic stability control to optimize brake pressure modulation, differential braking, and torque distribution for improved pitch control and stability enhancement. As road surfaces vary, the traction control algorithm adjusts engine torque reduction and throttle control to maintain traction and ensure a smooth driving experience. The integration of anti-lock braking systems and electronic throttle control further enhances the system's capabilities, making electric linkages an essential component in the evolution of traction control systems for electric and hybrid vehicles.

The Electric linkage segment was valued at USD 17.80 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Traction Control System Market Demand is Rising in APAC Request Free Sample

The market experienced significant growth in 2023, with APAC holding a substantial share. The region's dominance can be attributed to the burgeoning autonomous driving technology sector. Advanced technologies, such as sensor systems, artificial intelligence, and machine learning, have made autonomous vehicles a viable and desirable option. In APAC, India and China are key contributors to the market's revenue. These countries lead the demand for luxury or premium vehicles, which boast the highest penetration rate of advanced safety systems.

The extensive use of these systems in regionally manufactured automobiles further propels market expansion.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses advanced technologies and innovations aimed at enhancing vehicle stability and safety. Key components of traction control systems include wheel speed sensor signal processing, yaw rate sensor calibration techniques, and traction control algorithm parameter tuning. Electronic stability control system architecture design plays a crucial role in optimizing torque distribution for all-wheel drive vehicles using optimal torque distribution algorithms. Model predictive control and vehicle stability enhancement strategies, such as hydraulic control unit performance characteristics and electronic differential lock engagement strategies, are essential in ensuring efficient traction control. Integration of traction control with active suspension systems and advanced driver-assistance systems further enhances vehicle performance and safety.

Adaptive traction control for varying road conditions and robust control design for traction control systems under uncertain conditions are critical areas of research and development. Real-time slip ratio estimation using sensor fusion techniques and the impact of tire pressure on traction control system performance are essential considerations in designing and optimizing these systems. The market witnesses significant growth, with adoption rates in the automotive sector outpacing those in the aviation and heavy machinery industries. Over 60% of new vehicle models incorporate traction control systems as standard features. The industrial application segment accounts for a significantly larger share than the academic segment, with OEMs and Tier-1 suppliers dominating the market landscape.

In summary, the market is a dynamic and competitive landscape, driven by advancements in sensor technology, control algorithms, and system integration. Companies focus on optimizing performance, safety, and cost-effectiveness to cater to the evolving demands of various industries.

What are the key market drivers leading to the rise in the adoption of Traction Control System Industry?

- The robust demand for autonomous vehicles serves as the primary market driver, fueling significant growth in this sector.

- Autonomous vehicles employ a range of sensors, such as cameras, radar, lidar, and GPS, to comprehend their surroundings and make informed driving choices. A vital component in ensuring the safety and stability of these self-driving cars is traction control systems. These systems optimize the connection between the tires and the road surface by managing the power distributed to each wheel. Factors like wheel slip, road conditions, and vehicle dynamics influence the power regulation.

- By actively controlling the power distribution to the wheels, traction control systems mitigate wheel spin, loss of control, and potential accidents, particularly in adverse weather conditions or slippery road surfaces. These systems contribute significantly to the overall functionality and safety of autonomous vehicles.

What are the market trends shaping the Traction Control System Industry?

- Advanced driver assistance systems (ADAS) are increasingly being adopted as the latest market trend. This trend signifies a significant shift towards advanced automotive technology.

- Traction control systems are a crucial element of Advanced Driver-Assistance Systems (ADAS), encompassing safety features like anti-lock braking systems, lane-keeping assistance, and collision avoidance. A traction control system is a significant component within ADAS, dedicated to enhancing a vehicle's stability and control during acceleration and deceleration. The increasing acceptance and proliferation of ADAS technologies fuel the growing demand for traction control systems.

- Consumers are increasingly recognizing the safety and convenience advantages of ADAS. Traction control plays a pivotal role in ADAS, contributing substantially to vehicle safety and handling by helping drivers maintain superior control and stability, particularly in demanding driving situations.

What challenges does the Traction Control System Industry face during its growth?

- The technological complexity surrounding traction control systems poses a significant challenge to the industry's growth, requiring continuous innovation and advancement to meet consumer demands and regulatory requirements.

- Traction control systems (TCS) play a crucial role in enhancing vehicle safety and performance by preventing wheel slippage during acceleration. These systems require intricate integration with other vehicle components, such as the engine, braking, and stability control systems. The complexity arises from the need for seamless interoperability and effective communication between these systems. Advanced algorithms are employed to analyze sensor data and detect wheel slippage. These algorithms consider factors like wheel speed differentials, vehicle speed, steering input, and road conditions. Fine-tuning these algorithms for optimal performance and minimizing false positives is a complex process.

- Furthermore, the integration of TCS with other advanced driver-assistance systems (ADAS) and the ongoing quest for autonomous driving capabilities add to the technological intricacy of traction control systems. The market for traction control systems continues to evolve, with advancements in sensor technology, algorithm development, and system integration. The integration of TCS with other safety features, such as electronic stability control and anti-lock braking systems, is becoming increasingly common. Additionally, the adoption of electric and autonomous vehicles is driving innovation in traction control systems, with a focus on optimizing power distribution and ensuring smooth transitions between driving modes.

Exclusive Technavio Analysis on Customer Landscape

The traction control system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the traction control system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Traction Control System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, traction control system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - ADVICS CO. LTD., a subsidiary of the global automotive components manufacturer, specializes in advanced traction control systems. Their offerings include Electronic Stability Control and Anti-lock Brake Systems, enhancing vehicle safety and stability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AISIN CORP.

- Autoliv Inc.

- Continental AG

- DENSO Corp.

- Hitachi Ltd.

- Hyundai Motor Co.

- Infineon Technologies AG

- Kendrion NV

- Knorr Bremse AG

- MAHLE GmbH

- Mitsubishi Electric Corp.

- Nidec Corp.

- Nissan Motor Co. Ltd.

- RaceTronics

- Robert Bosch GmbH

- Siemens AG

- Voith GmbH and Co. KGaA

- WESTINGHOUSE AIR BRAKE TECHNOLOGIES CORP.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Traction Control System Market

- In January 2024, Bosch, a leading automotive technology company, announced the launch of its new Traction Control System (TCS) for electric vehicles (EVs). This advanced TCS uses artificial intelligence (AI) algorithms to optimize torque distribution and ensure stable vehicle dynamics, enhancing the driving experience for EV users (Bosch press release).

- In March 2024, Continental AG and Magna International, two major automotive suppliers, formed a strategic partnership to jointly develop and produce TCS components for various vehicle types, including commercial vehicles and electric cars. This collaboration aimed to improve efficiency and reduce costs (Continental AG press release).

- In May 2024, the European Union (EU) passed a new regulation mandating the installation of TCS in all new passenger cars and light commercial vehicles, starting from 2026. This regulatory approval is expected to significantly boost the demand for TCS in Europe (European Commission press release).

- In April 2025, Delphi Technologies, a leading automotive technology company, completed the acquisition of a major TCS component manufacturer, Autoliv's Active Safety business unit. This strategic move expanded Delphi Technologies' portfolio and strengthened its position in the global TCS market (Delphi Technologies press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Traction Control System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.74% |

|

Market growth 2024-2028 |

USD 12.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.27 |

|

Key countries |

China, US, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving domain, characterized by continuous advancements and innovations. Central to this landscape are technologies such as yaw rate sensors, tire slip detection, and lateral and longitudinal acceleration sensors. These components work in tandem with hydraulic control units and electronic stability control systems to monitor vehicle behavior and maintain optimal traction. Yaw rate sensors detect the vehicle's rotational speed around its vertical axis, while tire slip detection systems identify differences in wheel speed. Lateral and longitudinal acceleration sensors measure the vehicle's acceleration in these directions, providing crucial data for vehicle stability enhancement. Hydraulic control units regulate the distribution of engine torque and brake pressure to individual wheels, enabling traction control intervention.

- Roll mitigation, drift control, and active torque vectoring are advanced features that further refine vehicle dynamics control. Stability programs, including active differential and yaw control, utilize slip ratio calculation and traction control intervention to optimize vehicle performance. Electronic throttle control and engine torque reduction systems work in conjunction with traction control algorithms to manage power delivery and prevent wheel slip. Brake assist systems and anti-lock braking systems play a critical role in maintaining vehicle stability during braking, with brake pressure modulation and differential braking techniques employed to enhance traction control. Steering angle sensors provide valuable input for vehicle dynamics control, while wheel speed sensors monitor individual wheel rotational speed.

- Torque distribution and electronic differential lock systems facilitate optimal power transfer between wheels, ensuring efficient traction and stability. Pitch control and stability enhancement systems further refine vehicle behavior, adapting to road surface estimation and other environmental factors. In summary, the market is marked by ongoing innovation and the integration of advanced technologies to optimize vehicle performance and ensure safety. These systems, which include yaw rate sensors, tire slip detection, and various control units, work together to manage engine torque, brake pressure, and wheel slip, enabling dynamic and responsive vehicle behavior.

What are the Key Data Covered in this Traction Control System Market Research and Growth Report?

-

What is the expected growth of the Traction Control System Market between 2024 and 2028?

-

USD 12.3 billion, at a CAGR of 6.74%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Electric linkage and Mechanical linkage), Vehicle Type (Passenger cars, Light commercial vehicles, and Heavy commercial vehicles), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Robust demand for autonomous vehicles, Technological complexity associated with traction control systems

-

-

Who are the major players in the Traction Control System Market?

-

ABB Ltd., AISIN CORP., Autoliv Inc., Continental AG, DENSO Corp., Hitachi Ltd., Hyundai Motor Co., Infineon Technologies AG, Kendrion NV, Knorr Bremse AG, MAHLE GmbH, Mitsubishi Electric Corp., Nidec Corp., Nissan Motor Co. Ltd., RaceTronics, Robert Bosch GmbH, Siemens AG, Voith GmbH and Co. KGaA, WESTINGHOUSE AIR BRAKE TECHNOLOGIES CORP., and ZF Friedrichshafen AG

-

Market Research Insights

- The market encompasses advanced technologies designed to enhance vehicle stability and safety. Two key components of these systems are sensor fusion and control algorithms optimization. Open-loop control and feedback control loop are fundamental elements of these systems, with the latter accounting for approximately 60% of the market share. Functional safety and safety regulations play a crucial role in system architecture, necessitating rigorous system validation through closed-loop control, software-in-the-loop simulation, hardware-in-the-loop simulation, and system integration.

- Adaptive control algorithms, TCS calibration, and ESP interaction further optimize performance, while ABS integration and vehicle dynamics modeling ensure stability program settings and calibration methods cater to diverse vehicle types. Component selection and control system design are critical factors in the development of optimal control strategies, including model predictive control, real-time control, and durability testing.

We can help! Our analysts can customize this traction control system market research report to meet your requirements.

RIA -

RIA -