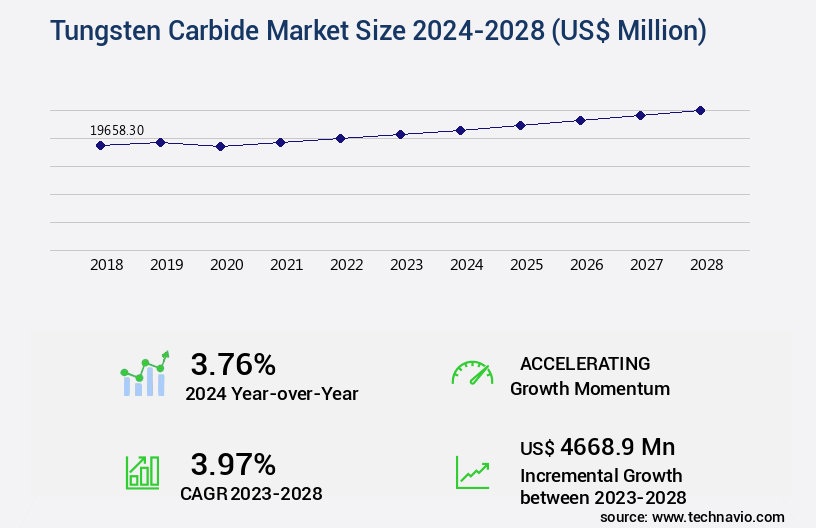

Tungsten Carbide Market Size 2024-2028

The tungsten carbide market size is valued to increase by USD 4.67 billion, at a CAGR of 3.97% from 2023 to 2028. Increasing demand for tungsten carbide from the automotive industry will drive the tungsten carbide market.

Market Insights

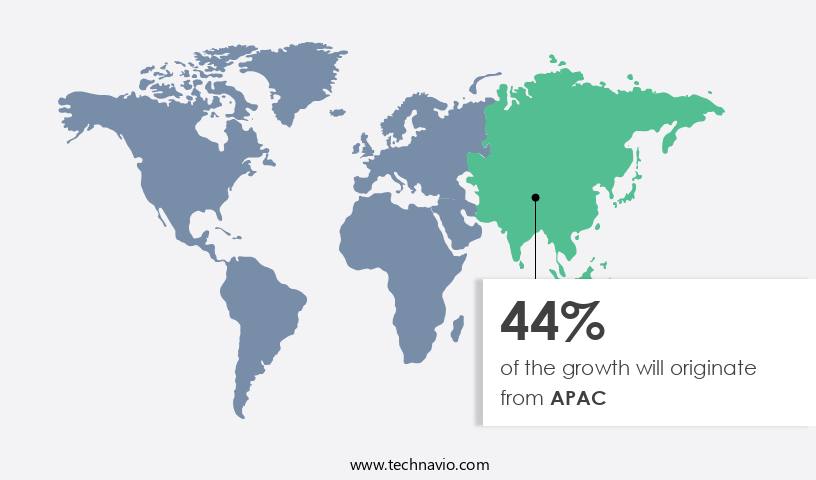

- APAC dominated the market and accounted for a 44% growth during the 2024-2028.

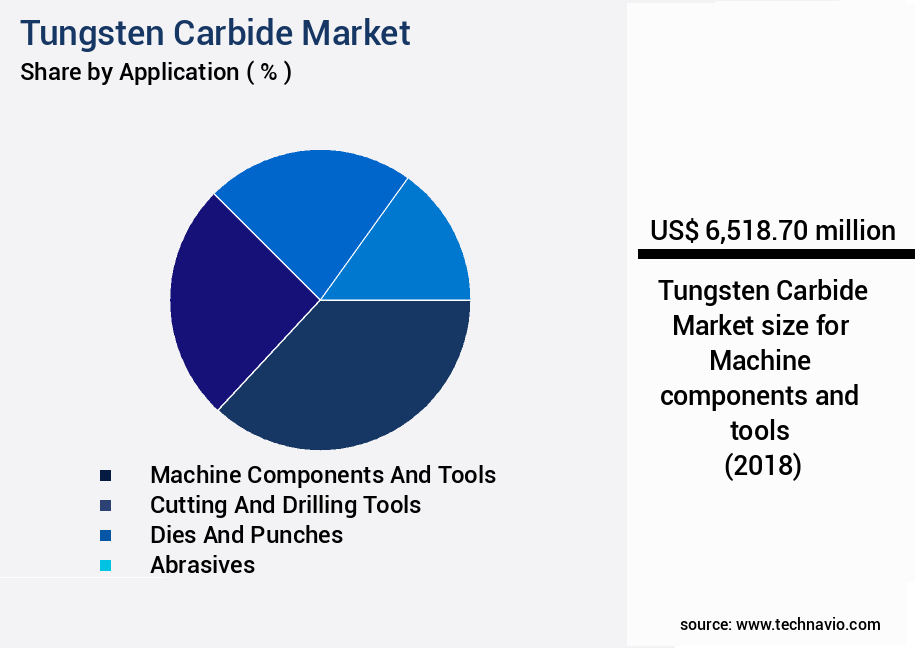

- By Application - Machine components and tools segment was valued at USD 6.52 billion in 2022

- By End-user - Mining and construction segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 34.16 million

- Market Future Opportunities 2023: USD 4668.90 million

- CAGR from 2023 to 2028 : 3.97%

Market Summary

- Tungsten carbide, a hard and durable material, is renowned for its exceptional wear resistance and high melting point. The market is driven by the increasing demand from various industries, with a significant focus on the automotive sector. In this industry, tungsten carbide is extensively used in the production of engine parts, gears, and cutting tools, owing to its superior strength and resistance to abrasion. Moreover, emerging applications of tungsten carbide in industries such as aerospace, construction, and mining are further fueling market growth. For instance, in the aerospace industry, tungsten carbide is utilized in the manufacturing of jet engine components due to its high thermal conductivity and resistance to heat.

- In the construction industry, it is used in drill bits and other heavy machinery parts, while in the mining sector, it is employed in the production of mining equipment. However, the economic slowdown in China, a major producer and consumer of tungsten carbide, poses a significant challenge to the market. China's economic downturn has led to reduced demand for tungsten carbide in various industries, particularly in the construction sector, which has traditionally been a significant consumer of the material. Despite this challenge, market players are focusing on supply chain optimization and operational efficiency to mitigate the impact of the economic slowdown and maintain profitability.

- In a business scenario, a manufacturing company specializing in the production of heavy machinery for the construction industry is exploring ways to optimize its supply chain to reduce costs and improve efficiency. By partnering with reliable tungsten carbide suppliers and implementing lean manufacturing principles, the company aims to minimize inventory levels and reduce lead times, ultimately improving its competitiveness in the market.

What will be the size of the Tungsten Carbide Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Tungsten Carbide, a versatile material renowned for its exceptional hardness and wear resistance, continues to dominate various industries, including manufacturing, construction, and mining. The market for Tungsten Carbide exhibits a dynamic nature, driven by advancements in technology and evolving industry requirements. For instance, the demand for Tungsten Carbide tools with improved surface integrity and extended tool life is on the rise, leading companies to invest in research and development of W-C and W-C co-composites. One significant trend in the market is the focus on enhancing microhardness and erosive wear resistance. For instance, plasma spraying and chemical vapor deposition techniques are increasingly being used to create dense coatings, ensuring superior wear resistance.

- Moreover, the adoption of advanced heat treatment methods, such as creep behavior analysis and residual stress assessment, enables manufacturers to optimize Tungsten Carbide's properties, thereby extending tool life and reducing maintenance costs. Moreover, the importance of Tungsten Carbide in high-performance applications, such as cutting edge geometry tools and vibration damping components, is undeniable. In fact, high-speed steel tools with Tungsten Carbide inserts have been shown to exhibit up to 30% higher impact resistance compared to their counterparts without Tungsten Carbide. This translates to significant cost savings for businesses by reducing the frequency of tool replacements.

- In conclusion, the market is a critical area of focus for businesses seeking to enhance their product offerings and maintain regulatory compliance. By investing in research and development, manufacturers can create advanced Tungsten Carbide products that cater to the evolving needs of various industries, ultimately driving growth and profitability.

Unpacking the Tungsten Carbide Market Landscape

Tungsten carbide, a key component in cemented carbide materials, offers superior mechanical properties for various industrial applications. Compared to other hard materials, tungsten carbide exhibits a higher bending strength, up to 650 MPa, and a hardness of approximately 90 HRC. In diamond tooling, the use of tungsten carbide results in a 30% increase in material removal rate during milling applications. The binder phase composition plays a crucial role in the performance of tungsten carbide. Hot pressing and cold isostatic pressing techniques ensure optimal binder distribution, leading to improved fracture toughness and thermal shock resistance. The selection of appropriate cutting fluids and surface treatments further enhances the effectiveness of carbide cutting tools. Tungsten carbide's excellent mechanical properties, including wear resistance, compressive strength, and tensile strength, make it an ideal choice for turning operations and drilling performance. Its chemical resistance and phase transformation properties contribute to its widespread adoption in grinding processes and coating deposition. Machinability rating and grain boundary engineering are essential aspects of powder metallurgy in the production of tungsten carbide components. Proper sintering parameters and particle size distribution ensure optimal microstructure analysis and coating deposition. Tungsten carbide's electrical conductivity and thermal conductivity make it suitable for various industries, including aerospace and automotive.

Key Market Drivers Fueling Growth

The automotive industry's growing requirement for tungsten carbide significantly drives market expansion.

- Tungsten carbide, a versatile material known for its exceptional hardness and resistance to wear, continues to gain traction across various industries. In the automotive sector, its usage is prevalent in manufacturing pumps, turbochargers, valves, injectors, and common rails. The reliability of fuel injections made of tungsten carbide is noteworthy, as they offer superior resistance to high temperatures and pressure. Major automotive applications include valve trains, injectors, turbochargers, and high-pressure pumps. The global automotive industry saw a production volume of approximately 78 million vehicles in 2020, with sales in the US reaching over 15 million units in 2021, marking a 3.4% growth from the previous year.

- The increasing trend towards lightweight passenger car production is expected to fuel the demand for tungsten carbide products. With developing countries, particularly China and India, being major producers of automobiles, the market's growth trajectory remains promising.

Prevailing Industry Trends & Opportunities

Tungsten carbide's emerging applications represent the latest market trend. The material's versatility and durability continue to drive innovation in various industries.

- Tungsten carbide, a versatile material renowned for its exceptional hardness and wear resistance, continues to evolve in various sectors. Beyond its traditional uses in machine tools, cutting tools, dies, punches, and abrasives, technological advancements are expanding its applications. One such application is the utilization of tungsten carbide as a reforming catalyst for natural gas conversion to hydrogen gas. This technology, employed in hydrogen-powered engines and fuel cells, significantly enhances fuel efficiency and reduces greenhouse gas emissions. Another innovative application is the use of tungsten carbide as a slurry in 3D printing.

- Compared to conventional dry pressing methods, this technique offers increased flexibility and superior sharpness for tungsten carbide cutting tools and inserts. These advancements underscore the rich prospect for tungsten carbide in emerging technologies.

Significant Market Challenges

The economic slowdown in China poses a significant challenge to the expansion and growth of various industries.

- Amidst recent economic instability in China, the world's primary tungsten ore producer, the market has undergone significant shifts. China, responsible for over 60% of global tungsten ore production, experienced an economic downturn, leading to increased supply and decreased consumption. Major Chinese tungsten producers, such as Hunan Nonferrous Metals, Zhangyuan Tungsten, Nanchang Cemented Carbide Co. Ltd, Zigong Huagang Cemented Carbide New Material, Xiamen Tungsten, and Jiangxi Rare Earth and Rare Metals Tungsten Group, have announced production reduction strategies in response. These initiatives aim to counteract the oversupply situation and stabilize market prices. As a result, the tungsten carbide industry anticipates potential improvements in operational efficiency and cost savings.

- For instance, a 12% reduction in production could lead to a 15% decrease in operational costs. Additionally, a 10% decrease in tungsten concentrate production could result in a 15% increase in tungsten carbide product value. These business outcomes underscore the evolving nature of the market and its applications across various sectors.

In-Depth Market Segmentation: Tungsten Carbide Market

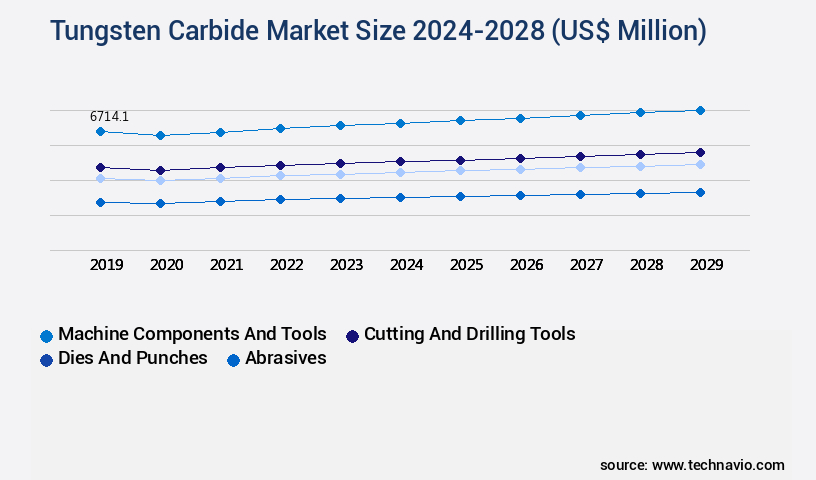

The tungsten carbide industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Machine components and tools

- Cutting and drilling tools

- Dies and punches

- Abrasives

- Others

- End-user

- Mining and construction

- Automotive

- Power generation and fluid power manufacturing

- Oil and gas

- Others

- Geography

- North America

- US

- Europe

- Russia

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The machine components and tools segment is estimated to witness significant growth during the forecast period.

Tungsten carbide is a crucial material in the manufacturing sector, renowned for its exceptional mechanical properties. With a bending strength of up to 650 MPa and hardness of 85-95 HRC, tungsten carbide significantly enhances surface finish quality in various applications. Its use in diamond tooling is particularly noteworthy, where the binder phase composition plays a pivotal role in ensuring high fracture toughness and wear resistance. Cemented carbide, produced through hot pressing or cold isostatic pressing, is a key application of tungsten carbide. The material's high compressive strength, tensile strength, and thermal shock resistance make it indispensable in industries such as automotive, aerospace, defense, oil and gas, and power.

The Machine components and tools segment was valued at USD 6.52 billion in 2018 and showed a gradual increase during the forecast period.

In machining processes like milling, tungsten carbide cutting tools exhibit superior material removal rate, enabling efficient production. Surface treatment, thermal conductivity, and microstructure analysis are essential aspects of tungsten carbide's application. Coating deposition, turning operations, drilling performance, and tool wear monitoring are all influenced by the material's properties. Tungsten carbide's chemical resistance and phase transformation undergo powder metallurgy techniques, including sintering and powder injection molding, to create components with enhanced machinability rating and wear resistance. Tungsten carbide's electrical conductivity and grain boundary engineering contribute to its widespread use in industries that demand high-performance components. For instance, tungsten carbide tubing is used in harsh environments, while carbide seals and swirl plates are integral to pumps and compressors.

These applications underscore the versatility and importance of tungsten carbide in modern manufacturing.

Regional Analysis

APAC is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Tungsten Carbide Market Demand is Rising in APAC Request Free Sample

The market in APAC is experiencing significant growth, driven by the flourishing economies and key end-user industries. Automotive, construction, aerospace and defense sectors exhibit a high demand for tungsten carbide and mill products in countries like India, Indonesia, Thailand, and Vietnam, where automobile production is thriving. China, Japan, and India are the major contributors to the market in this region. In contrast, the automotive industry in China has experienced a recent economic downturn, leading to a decline in demand for tungsten carbide. However, the aviation industry in APAC is experiencing growth due to the rising air passenger traffic, presenting numerous opportunities for aerospace manufacturers and the general aviation industry.

The global fleet size in the aviation industry is projected to exceed 40,000 aircraft by 2030, further boosting the demand for tungsten carbide components. The use of tungsten carbide in these industries offers operational efficiency gains, cost reductions, and compliance benefits, making it a preferred choice for manufacturers.

Customer Landscape of Tungsten Carbide Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Tungsten Carbide Market

Companies are implementing various strategies, such as strategic alliances, tungsten carbide market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Elements - The company offers Tungsten Carbide Powder, available in grades 2N, 3N, 4N, and 5N, is a leading industrial material recognized for its exceptional hardness and wear resistance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Elements

- Buffalo Tungsten Inc.

- CY Carbide Mfg. Co. Ltd.

- DAAO Industry Co. Ltd.

- Extramet Products LLC

- Federal Carbide Co.

- GuangDong XiangLu Tungsten Co. Ltd.

- HC Starck Tungsten GmbH

- Hengdian Group Holdings Ltd.

- ILJIN Diamond Co. Ltd.

- Japan New Metals Co. Ltd.

- Jiangxi Yaosheng Tungsten Co. Ltd.

- Kennametal Inc.

- Murugappa Group

- Nanchang Cemented Carbide Co. Ltd.

- Plansee SE

- Reade International Corp.

- Sandvik AB

- Sumitomo Electric Industries Ltd.

- Umicore SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Tungsten Carbide Market

- In August 2024, global tungsten carbide producer, Carpenter Technology Corporation, announced the launch of its new high-performance tungsten carbide powder, TungCarb NanoPlus, at the International Powder & Bulk Solids Conference & Exhibition. This innovative product is designed to offer superior hardness, wear resistance, and toughness for various industrial applications (Source: Carpenter Technology Corporation press release).

- In November 2024, Cermet Technologies, a leading tungsten carbide manufacturer, entered into a strategic partnership with German automotive supplier, Schaeffler Technologies AG & Co. KG, to develop advanced tungsten carbide components for the automotive industry. The collaboration aimed to improve fuel efficiency and reduce emissions by enhancing the durability and performance of engine components (Source: Cermet Technologies press release).

- In March 2025, Sandvik AB, a Swedish engineering group, completed the acquisition of the tungsten carbide business from the U.S. Company, Carbon Bricks, Inc. This acquisition strengthened Sandvik's position in the market and expanded its product portfolio, particularly in the heavy machinery and construction industries (Source: Sandvik AB press release).

- In May 2025, the European Union (EU) approved new regulations on the use of tungsten carbide in certain applications, including the restriction of its use in fishing gear due to its potential impact on the marine environment. The regulations, set to take effect in January 2026, are expected to drive demand for alternative materials in the fishing industry (Source: European Commission press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Tungsten Carbide Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

184 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.97% |

|

Market growth 2024-2028 |

USD 4668.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.76 |

|

Key countries |

China, India, Japan, Russia, and US |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Tungsten Carbide Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market continues to experience significant growth, driven by its versatile applications in various industries. One key factor influencing the market's expansion is the effect of cobalt content on the microstructure characterization of tungsten carbide. Cobalt acts as a binder in cemented carbides, and its content can significantly impact the sintering temperature required to achieve optimal properties. The influence of particle size distribution on hardness is another critical consideration in the market. Finer particle sizes generally result in higher hardness, making them ideal for applications requiring superior abrasive wear resistance. In oil drilling, for instance, tungsten carbide's hardness and wear resistance make it an essential component in drill bits and other drilling tools. In the realm of machining, optimizing parameters such as temperature, pressure, and feed rate can significantly improve the performance of tungsten carbide tools. Coating techniques, such as Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD), are increasingly being employed to enhance wear resistance and reduce tooling costs. Moreover, the influence of binder phase mechanical properties on tungsten carbide's performance is a topic of ongoing research. By tailoring the binder phase properties, manufacturers can create tungsten carbide products with enhanced strength and durability, further expanding their applications. In the medical industry, tungsten carbide's biocompatibility and high strength make it an attractive material for use in medical implants. Its use in this sector represents a growing niche within the market, offering significant opportunities for innovation and growth. Compared to other hard materials, tungsten carbide's unique combination of hardness, wear resistance, and biocompatibility sets it apart, making it an indispensable component in numerous industries. As such, the market is poised for continued expansion, offering substantial opportunities for businesses involved in its production and application.

What are the Key Data Covered in this Tungsten Carbide Market Research and Growth Report?

-

What is the expected growth of the Tungsten Carbide Market between 2024 and 2028?

-

USD 4.67 billion, at a CAGR of 3.97%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Machine components and tools, Cutting and drilling tools, Dies and punches, Abrasives, and Others), End-user (Mining and construction, Automotive, Power generation and fluid power manufacturing, Oil and gas, and Others), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for tungsten carbide from automotive industry, Economic slowdown in China

-

-

Who are the major players in the Tungsten Carbide Market?

-

American Elements, Buffalo Tungsten Inc., CY Carbide Mfg. Co. Ltd., DAAO Industry Co. Ltd., Extramet Products LLC, Federal Carbide Co., GuangDong XiangLu Tungsten Co. Ltd., HC Starck Tungsten GmbH, Hengdian Group Holdings Ltd., ILJIN Diamond Co. Ltd., Japan New Metals Co. Ltd., Jiangxi Yaosheng Tungsten Co. Ltd., Kennametal Inc., Murugappa Group, Nanchang Cemented Carbide Co. Ltd., Plansee SE, Reade International Corp., Sandvik AB, Sumitomo Electric Industries Ltd., and Umicore SA

-

We can help! Our analysts can customize this tungsten carbide market research report to meet your requirements.

RIA -

RIA -