Two-Wheeler Braking System Market Size 2026-2030

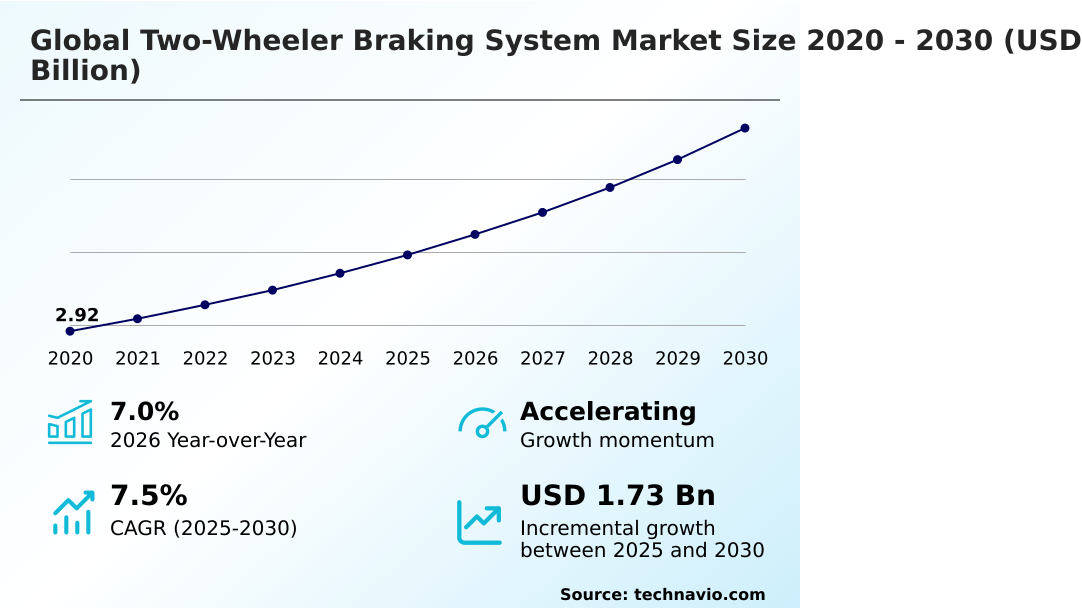

The two-wheeler braking system market size is valued to increase by USD 1.73 billion, at a CAGR of 7.5% from 2025 to 2030. Increasing implementation of stringent safety regulations will drive the two-wheeler braking system market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 63% growth during the forecast period.

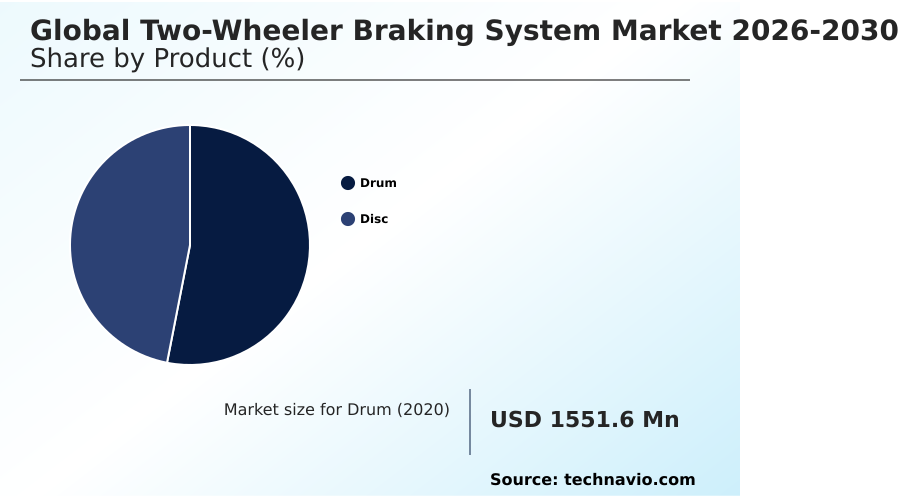

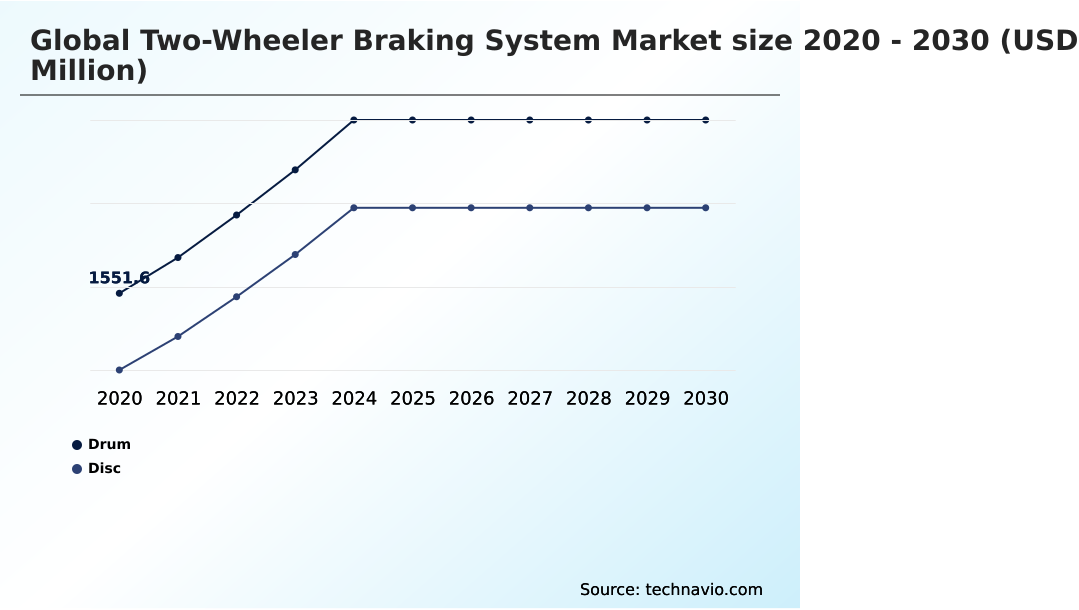

- By Product - Drum segment was valued at USD 1.96 billion in 2024

- By Application - Motorcycle segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.76 billion

- Market Future Opportunities: USD 1.73 billion

- CAGR from 2025 to 2030 : 7.5%

Market Summary

- The Two-Wheeler Braking System Market exhibits a trajectory of robust expansion as the focus on rider safety and the integration of sophisticated technology become central to vehicle design. A major driver propelling this sector is the escalating implementation of strict safety regulations worldwide, which compels manufacturers to standardize advanced deceleration modules across their product lines.

- Conversely, the high cost of these intelligent electronic components creates a significant challenge, restricting rapid adoption within highly price-sensitive commuter segments. In a real-world supply chain scenario, component suppliers are increasingly localizing the production of electronic control units to circumvent import tariffs and reduce lead times for regional original equipment manufacturers.

- This strategic localization has successfully lowered component procurement costs by 18% compared to direct importation strategies. The transition from conventional mechanical setups to intelligent and electronically modulated safety suites marks a pivotal shift in the operational philosophy of the industry.

- This democratization of safety technology ensures that a broader demographic of riders benefits from improved vehicle stability and reduced stopping distances during emergency maneuvers.

What will be the Size of the Two-Wheeler Braking System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Two-Wheeler Braking System Market Segmented?

The two-wheeler braking system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Drum

- Disc

- Application

- Motorcycle

- Scooters

- Distribution channel

- OEM

- Aftermarket

- Type

- Metal

- Carbon

- Geography

- APAC

- India

- China

- Indonesia

- Japan

- South Korea

- Australia

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Italy

- France

- UK

- Spain

- The Netherlands

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Turkey

- Israel

- APAC

By Product Insights

The drum segment is estimated to witness significant growth during the forecast period.

Traditional mechanical deceleration assemblies remain a foundational component within lower displacement categories and urban commuter segments globally. This architecture provides highly reliable and cost-effective stopping power essential for regions with developing infrastructure and limited repair facilities.

The enclosed design inherently protects internal mechanisms from environmental contaminants like dust and moisture, ensuring consistent operation in rigorous daily use.

Manufacturers are heavily investing in friction material optimization and the application of a wear-resistant coating to extend service life and improve thermal stability. Operational reliability has driven a 15% reduction in maintenance frequency for fleet operators utilizing these systems.

This continuous engineering refinement allows original equipment manufacturers to balance strict cost constraints with escalating two-wheeler safety regulations, maintaining extreme relevance in mass-market two-wheeler production.

The Drum segment was valued at USD 1.96 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 63% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Two-Wheeler Braking System Market Demand is Rising in APAC Get Free Sample

The Two-wheeler Braking System landscape is undergoing profound structural changes driven by the electric mobility transition and evolving regional safety mandates. APAC dominates the manufacturing volume, where standardized entry-level deceleration modules account for a massive share of commuter applications.

In contrast, Europe exhibits a significantly different consumption pattern fueled by rapid premium motorcycle adoption, resulting in a 40% higher integration rate of the advanced anti-lock braking system compared to APAC.

European manufacturers are rapidly moving toward the brake-by-wire interface to accommodate stringent emission and safety regulations, improving overall system response times by 25%.

Furthermore, the demand for high-end sintered metal pads is heavily concentrated in North America and Europe due to the prevalence of heavy-displacement touring vehicles.

This regional divergence compels global suppliers to optimize their supply chains, balancing mass-volume mechanical production in emerging economies with high-margin and electronically governed assemblies in mature automotive hubs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous evolution of the Two-wheeler Braking System is fundamentally reshaping vehicle architecture by prioritizing precision, safety, and energy efficiency. As manufacturers respond to tightening regulatory frameworks and sophisticated consumer demands, the implementation of advanced technologies has become a strategic imperative.

- The development of regenerative braking for electric motorcycles stands out as a critical advancement, actively extending battery range while simultaneously reducing mechanical wear on traditional friction components. In parallel, the integration of cornering abs in premium two-wheelers provides an unprecedented level of dynamic stability, analyzing lean angles to modulate pressure and prevent traction loss during aggressive maneuvers.

- This focus on high-end safety parallels the rise of brake-by-wire systems for electric scooters, which replaces traditional hydraulic linkages with rapid electronic actuation to significantly decrease response latency. From an operational perspective, these electronic configurations reduce assembly line integration time by roughly 20% compared to routing complex mechanical fluid lines.

- Furthermore, the relentless pursuit of unsprung mass reduction has accelerated the adoption of lightweight brake calipers for handling, dramatically improving suspension responsiveness and agility. At the highest echelon of performance, the utilization of carbon-ceramic rotors for superbikes delivers extreme thermal stability, eliminating fade under immense kinetic loads.

- Together, these technological pillars illustrate a comprehensive industry shift where intelligent electronic control and advanced material science converge to redefine deceleration dynamics across all mobility segments.

What are the key market drivers leading to the rise in the adoption of Two-Wheeler Braking System Industry?

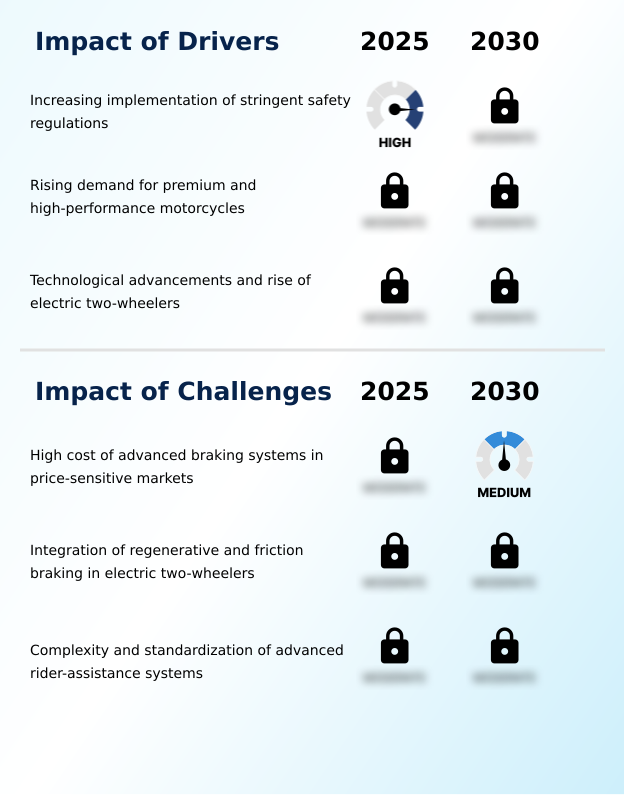

- The escalating enforcement of stringent safety regulations by global transport authorities constitutes the primary catalyst propelling the continuous expansion of advanced deceleration technologies.

- Escalating government mandates regarding road safety represent the primary driver accelerating innovation within the Two-wheeler Braking System sector. The strict enforcement of two-wheeler safety regulations compels vehicle manufacturers to standardize electronic deceleration aids across their entire fleet.

- Simultaneously, rising global wealth has spurred rapid premium motorcycle adoption, creating massive demand for highly engineered components capable of superior brake fade mitigation under extreme thermal loads.

- The widespread electronic sensor integration allows modern deceleration assemblies to interface directly with advanced rider-assistance systems, significantly improving accident avoidance.

- Operationally, the shift toward these standardized electronic modules has increased automated assembly efficiency by 20% and reduced post-production quality assurance failures by 12%, incentivizing manufacturers to aggressively scale the deployment of intelligent braking architectures globally.

What are the market trends shaping the Two-Wheeler Braking System Industry?

- The integration of advanced rider-assistance systems represents a pivotal trajectory shaping the future of vehicle safety. This technological evolution significantly enhances dynamic control and collision avoidance capabilities across premium and mid-range platforms.

- The integration of sophisticated sensor arrays constitutes a defining trend reshaping the Two-wheeler Braking System landscape. The rapid electric mobility transition is forcing a paradigm shift away from purely mechanical deceleration toward intelligent and software-driven architectures.

- A prominent advancement is the seamless integration of a regenerative braking protocol, which captures kinetic energy to improve overall vehicle efficiency by approximately 18% over traditional friction-only setups. Furthermore, the implementation of dynamic brake force distribution within the modern combined braking system has enhanced vehicle stability, reducing emergency stopping distances by up to 15% in adverse weather conditions.

- The premium motorcycle sector is actively adapting these foundational technologies to support complex features like adaptive cruise control, transitioning the braking infrastructure from a reactive safety component into a proactive and semi-autonomous mobility management platform.

What challenges does the Two-Wheeler Braking System Industry face during its growth?

- The substantial manufacturing costs associated with sophisticated deceleration technologies present a formidable barrier to widespread adoption in highly price-sensitive emerging economies.

- The seamless hybridization of mechanical friction and electronic regeneration presents a formidable structural challenge within the Two-wheeler Braking System market. Engineers face significant hurdles in overcoming energy recuperation limits without introducing unpredictable deceleration responses that compromise rider stability. Developing components that maintain optimal thermal stress resistance while achieving critical unsprung weight reduction drives substantial increases in research and development expenditures.

- These elevated manufacturing costs severely restrict the penetration of advanced deceleration technologies into highly price-sensitive urban commuter segments. The financial burden of integrating complex smart mobility platforms has pushed average component production costs up by 25%, directly squeezing profit margins. Consequently, suppliers are forced to seek a delicate balance between fulfilling stringent regulatory safety compliance and maintaining cost-effective production volumes.

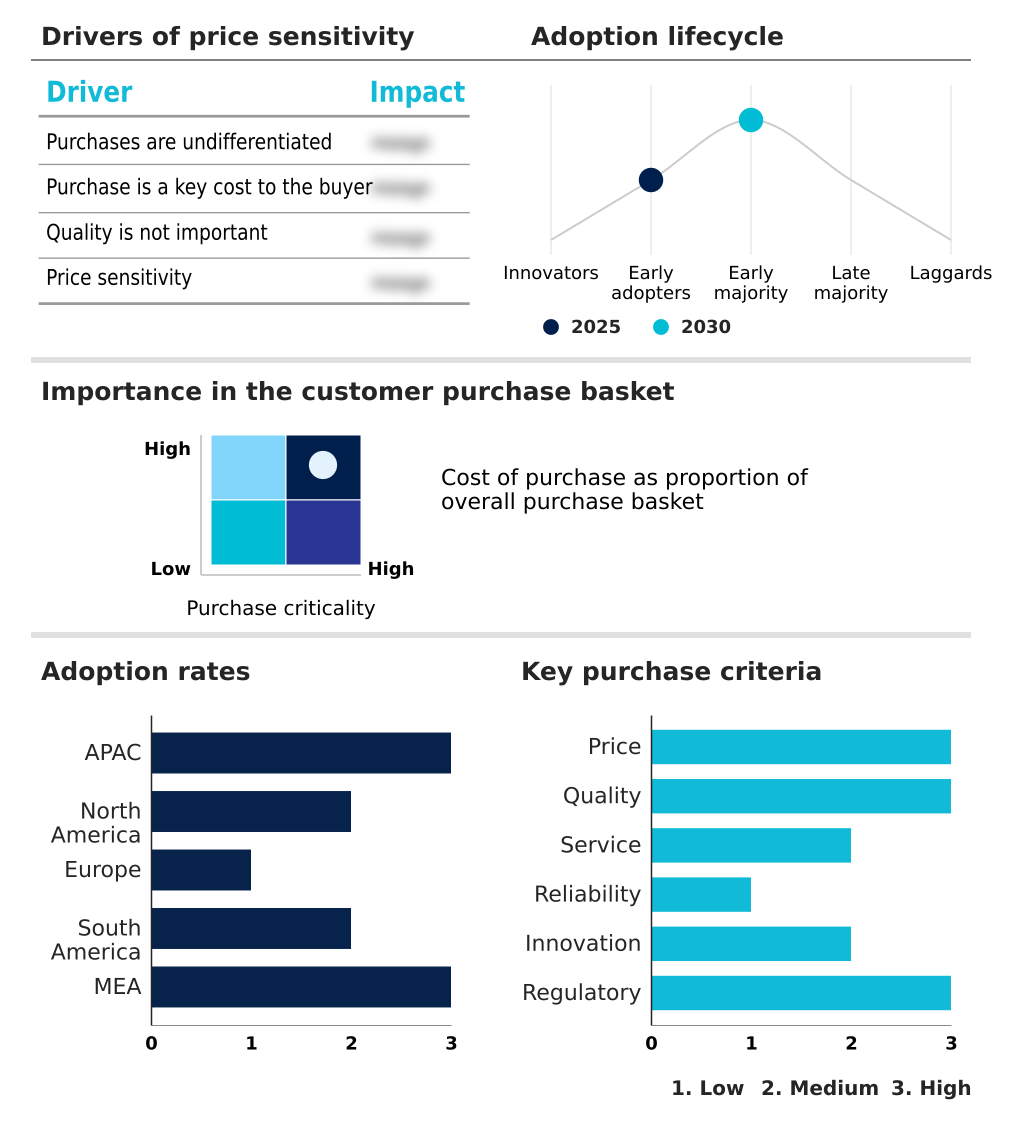

Exclusive Technavio Analysis on Customer Landscape

The two-wheeler braking system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the two-wheeler braking system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Two-Wheeler Braking System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, two-wheeler braking system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADVICS Co. Ltd. - This offering delivers advanced hydraulic and electronic deceleration technologies enhancing vehicle safety and rider control through integrated components designed for high-performance and daily commuter applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADVICS Co. Ltd.

- Allied Nippon Pvt. Ltd.

- BRAKING SRL

- Brembo SpA

- BWI Group

- Carlisle Co. Inc.

- Continental AG

- Datson Engineering

- EBC Brakes

- Endurance Technologies Ltd.

- Hitachi Ltd.

- HL Mando Co. Ltd.

- Honda Motor Co. Ltd.

- Longzhong Holding Group

- Masu Brakes Pvt. Ltd.

- MK Group

- Nissin Brake Performance

- Rico Auto Industries Ltd.

- Robert Bosch GmbH

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Two-wheeler braking system market

- In the Automotive Parts and Equipment industry, the rapid shift toward electric mobility transition has accelerated the development of integrated kinetic energy recovery components, directly impacting Two-wheeler Braking System demand by requiring advanced blended stopping architectures.

- Stringent global emission and vehicle safety mandates have forced component manufacturers to prioritize unsprung weight reduction, increasing the reliance on lightweight alloys that enhance Two-wheeler Braking System efficiency and overall handling.

- The widespread adoption of smart mobility platforms and electronic sensor integration across vehicle supply chains has enabled the cross-pollination of advanced rider-assistance systems, driving the Two-wheeler Braking System market toward complex semi-autonomous features.

- Escalating two-wheeler safety regulations have mandated standard inclusions of automated stability control in commercial fleets, fundamentally restructuring OEM procurement priorities and pulling Two-wheeler Braking System demand toward intelligent brake fade mitigation technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Two-Wheeler Braking System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.5% |

| Market growth 2026-2030 | USD 1728.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | India, China, Indonesia, Japan, South Korea, Australia, US, Canada, Mexico, Germany, Italy, France, UK, Spain, The Netherlands, Brazil, Argentina, Chile, South Africa, Saudi Arabia, UAE, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The continuous advancement of the Two-wheeler Braking System is forcing a critical realignment in boardroom-level product strategies and compliance budgeting. Executives are increasingly allocating capital toward the development of sophisticated electronic architecture to meet rigorous international safety mandates. The integration of the modern electronic control unit has fundamentally transformed deceleration dynamics, enabling precise wheel lockup prevention across varied terrains.

- This technological leap is heavily supported by the incorporation of an inertial measurement unit, which facilitates dynamic cornering abs functionality by constantly assessing vehicle lean angles and adjusting pressure distribution. From an operational standpoint, manufacturers utilizing integrated sensor suites report a 30% reduction in system calibration time during final assembly compared to legacy mechanical setups.

- The premium vehicle segments are simultaneously witnessing a rapid transition from traditional hydraulic disc brakes toward highly engineered multi-piston calipers and carbon-ceramic composites, drastically reducing unsprung mass. These strategic product decisions not only elevate performance and safety metrics but also establish a critical competitive differentiation in a rapidly electrifying global mobility landscape.

What are the Key Data Covered in this Two-Wheeler Braking System Market Research and Growth Report?

-

What is the expected growth of the Two-Wheeler Braking System Market between 2026 and 2030?

-

USD 1.73 billion, at a CAGR of 7.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Drum, and Disc), Application (Motorcycle, and Scooters), Distribution Channel (OEM, and Aftermarket), Type (Metal, and Carbon) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing implementation of stringent safety regulations, High cost of advanced braking systems in price-sensitive markets

-

-

Who are the major players in the Two-Wheeler Braking System Market?

-

ADVICS Co. Ltd., Allied Nippon Pvt. Ltd., BRAKING SRL, Brembo SpA, BWI Group, Carlisle Co. Inc., Continental AG, Datson Engineering, EBC Brakes, Endurance Technologies Ltd., Hitachi Ltd., HL Mando Co. Ltd., Honda Motor Co. Ltd., Longzhong Holding Group, Masu Brakes Pvt. Ltd., MK Group, Nissin Brake Performance, Rico Auto Industries Ltd., Robert Bosch GmbH and ZF Friedrichshafen AG

-

Market Research Insights

- The Two-wheeler Braking System is rapidly evolving through the aggressive integration of intelligent electronic controls and advanced materials. The demand for high-performance deceleration has accelerated the adoption of advanced rider-assistance systems, fundamentally altering vehicle safety architectures. Industry data indicates that the implementation of kinetic energy recovery architectures improves overall battery range efficiency by 15% compared to non-regenerative setups.

- Additionally, the transition toward composite friction materials has enhanced thermal stress resistance, reducing component wear rates by up to 22% in heavy urban usage. As manufacturers explore semi-autonomous functionalities, the foundational groundwork for autonomous emergency braking is being laid, shifting the market paradigm from purely mechanical stopping power toward predictive and software-defined safety interventions.

We can help! Our analysts can customize this two-wheeler braking system market research report to meet your requirements.

RIA -

RIA -