US Clinical Trials Market Size 2026-2030

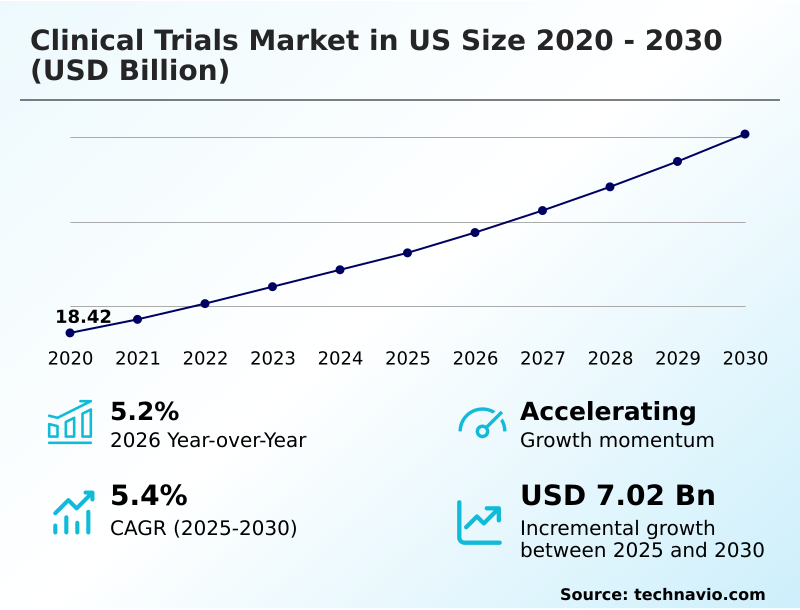

The us clinical trials market size is valued to increase by USD 7.02 billion, at a CAGR of 5.4% from 2025 to 2030. Robust growth in research and development expenditures will drive the us clinical trials market.

Major Market Trends & Insights

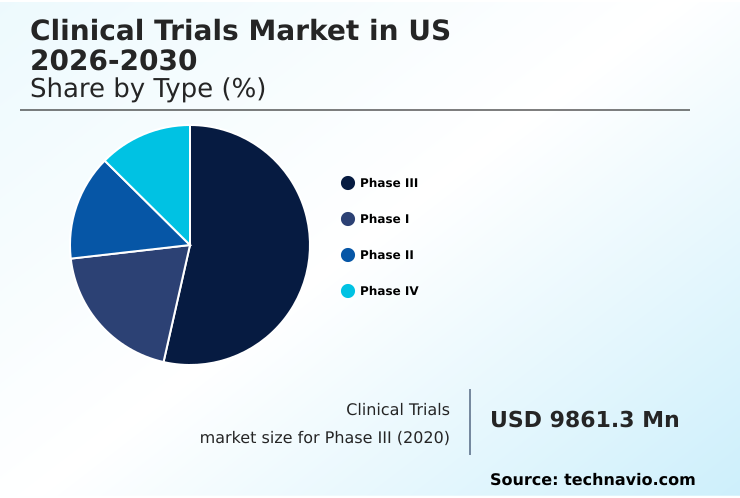

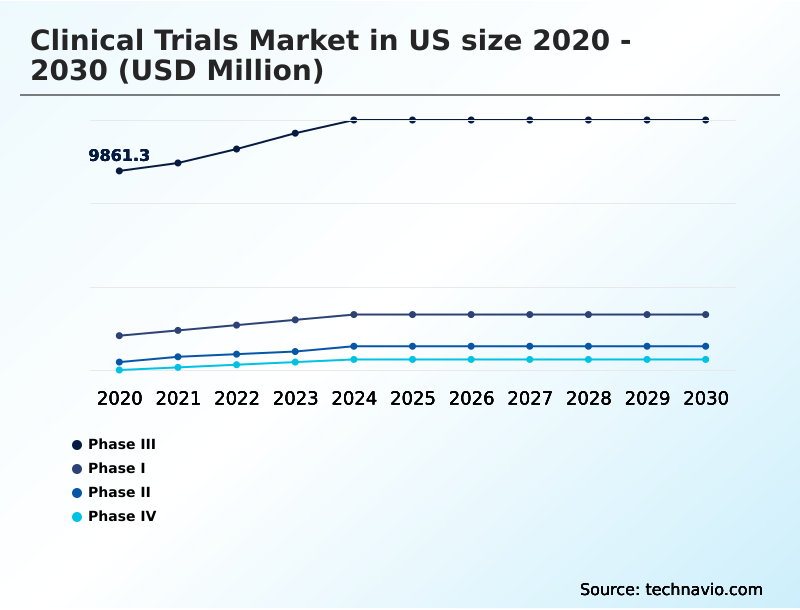

- By Type - Phase III segment was valued at USD 11.79 billion in 2024

- By Service Type - Interventional studies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.75 billion

- Market Future Opportunities: USD 7.02 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The clinical trials market in US is a critical ecosystem for medical innovation, defined by the systematic evaluation of new therapeutic interventions in human participants. This process is indispensable for securing regulatory approval and is structured in sequential phases to assess safety and efficacy.

- Market expansion is driven by substantial research and development investments, particularly in complex areas like oncology and rare diseases, which demand more sophisticated trial designs. A key trend transforming the landscape is the shift toward patient-centricity, accelerated by the adoption of decentralized and hybrid trial models. These models use digital technologies to reduce participant burden and broaden access.

- For instance, a contract research organization managing a multi-site study can deploy a unified clinical trial management system with integrated electronic data capture, streamlining data collection and improving operational efficiency across geographically dispersed locations. However, the industry grapples with persistent challenges, including intense competition for eligible patients and the operational complexities of navigating a stringent regulatory environment.

- Success hinges on balancing innovative trial execution with rigorous adherence to established clinical practice standards.

What will be the Size of the US Clinical Trials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Clinical Trials Market Segmented?

The us clinical trials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Phase III

- Phase I

- Phase II

- Phase IV

- Service type

- Interventional studies

- Observational studies

- Expanded access studies

- Indication

- Oncology

- CNS

- Autoimmune or inflammation

- Others

- Geography

- North America

- US

- North America

By Type Insights

The phase iii segment is estimated to witness significant growth during the forecast period.

The Phase III segment represents the most resource-intensive component of pre-approval research, designed to provide definitive evidence of an intervention's efficacy and safety.

These large-scale studies require meticulous protocol design and robust clinical data management to support a potential new drug application. The logistics of investigational product supply and the management of extensive documentation for trial master file management are critical operational pillars.

Utilizing adaptive trial design can optimize outcomes, while stringent gcp compliance and independent clinical endpoint adjudication are non-negotiable for regulatory success.

Leading cro services manage these complexities, with Phase III trials accounting for over 50% of the total expenditure across all phase i-iv clinical trials, underscoring their pivotal role in the development pathway.

The Phase III segment was valued at USD 11.79 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The clinical trials market in US is undergoing a significant operational evolution, driven by the need for greater efficiency and patient-centricity. The management of phase iii oncology trial logistics, for example, is being transformed by digital platforms that streamline complex processes.

- A decentralized trial technology platform comparison often reveals that integrated systems offer superior performance in managing the clinical supply chain complexity. Furthermore, real world data integration in clinical studies is becoming standard practice to supplement traditional evidence and provide a more holistic view of treatment effects.

- This is particularly valuable in adaptive trial design for neurological disorders, where longitudinal data is critical. Capturing patient reported outcomes in rare disease trials is also being improved through mobile health applications, enhancing data quality and participant engagement. Consequently, biostatistical analysis of complex trial data now incorporates more diverse and continuous information streams.

- Firms that successfully navigate the regulatory pathways for cell and gene therapies while demonstrating the cost-effectiveness of hybrid trial models are setting new industry benchmarks. Those that prioritize improving patient diversity in clinical research and implement robust electronic data capture system validation report significantly faster data-lock timelines than competitors relying on legacy systems, showcasing a clear operational advantage.

What are the key market drivers leading to the rise in the adoption of US Clinical Trials Industry?

- The robust and sustained growth in research and development expenditures by pharmaceutical, biotechnology, and medical device corporations is a primary driver for the market.

- Escalating R&D investments, particularly in complex therapeutic areas, are a primary market driver. The pipeline for cell and gene therapy trials and rare disease trials is expanding, demanding specialized clinical trial logistics and regulatory submission support.

- This complexity increases the need for meticulous source data verification and robust pharmacovigilance solutions to ensure patient safety and data integrity.

- For example, the development of companion diagnostics development programs alongside new therapies has increased, with such integrated projects showing a 20% higher likelihood of regulatory success.

- The formalization of medical writing services is critical for articulating complex scientific findings for a biologics license application.

- Consequently, sponsors are increasingly adopting advanced risk-based monitoring techniques, which can prioritize oversight activities and improve efficiency by over 25% compared to traditional 100% verification methods.

What are the market trends shaping the US Clinical Trials Industry?

- The clinical trials market is experiencing a significant operational shift, marked by the ascendancy of decentralized and hybrid frameworks that leverage digital health technologies.

- The market is rapidly adopting innovative frameworks, with the trend toward decentralized clinical trials and hybrid clinical trials reshaping study conduct. This shift is underpinned by a suite of eclinical solutions designed to enhance participant engagement and data collection. The use of electronic consent has streamlined onboarding, with some platforms reducing consent-related administrative tasks by up to 40%.

- The integration of wearable sensor data provides a continuous stream of objective information, while dedicated patient engagement platforms improve retention by offering unified access to study materials. Capturing patient reported outcomes through these digital tools ensures data is collected in real-time.

- Moreover, real-world data integration is becoming crucial for supplementing trial evidence, offering deeper insights into treatment effectiveness in everyday settings, and interactive response technology ensures seamless randomization and drug supply management in these complex virtual clinical trials.

What challenges does the US Clinical Trials Industry face during its growth?

- Systemic hurdles in patient recruitment and retention represent a key challenge, significantly impacting trial timelines, data integrity, and overall development program viability.

- A significant market challenge stems from escalating operational complexity and the persistent difficulty in patient recruitment. The increasing specificity of protocols makes clinical trial feasibility assessment a critical yet difficult step, as identifying eligible participants becomes more resource-intensive. Advanced clinical trial technology is essential, yet its implementation introduces hurdles related to system validation and data integration.

- For example, while an electronic data capture platform is standard, its inability to seamlessly connect with a separate clinical trial management system can create data silos, with firms reporting that reconciliation efforts consume up to 15% of data management time. Furthermore, leveraging clinical trial data analytics for predictive enrollment modeling is complicated by data privacy regulations.

- Ensuring robust biostatistics services are engaged early in trial design is crucial to mitigate the risk of statistically underpowered studies, a common consequence of failing to meet recruitment targets.

Exclusive Technavio Analysis on Customer Landscape

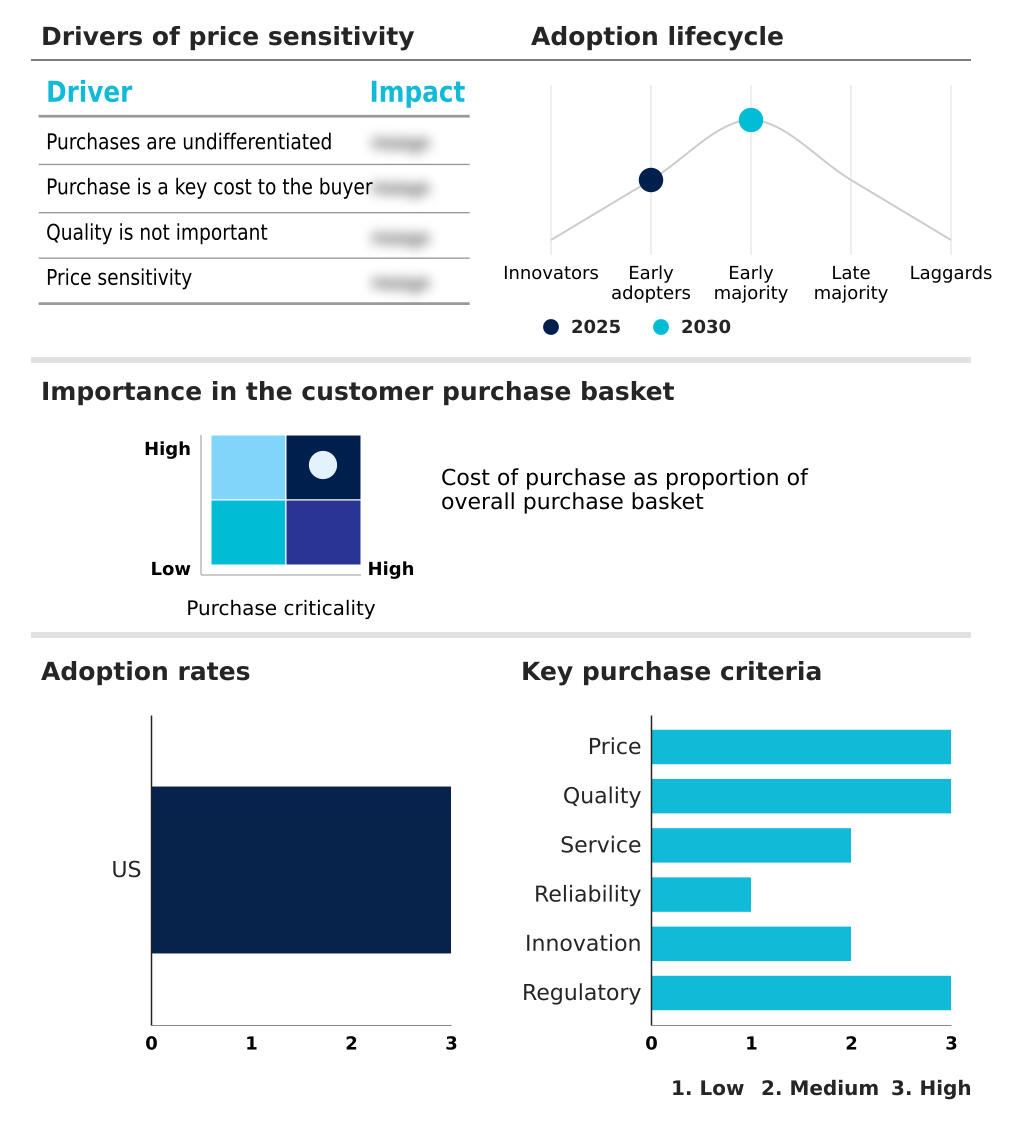

The us clinical trials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us clinical trials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Clinical Trials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us clinical trials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Caidya - Core offerings include comprehensive, full-service contract research organization solutions, managing complex clinical trials from initial study design through to regulatory submission and post-market surveillance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Caidya

- Celerion

- CenExel Clinical Research

- Charles River Laboratories International Inc.

- Clario

- EPS International Holdings Co

- Fortrea Holdings Inc

- ICON plc

- IQVIA Holdings Inc.

- Laboratory Holdings Inc.

- Medelis Inc.

- Medpace Holdings Inc.

- Parexel International Corp.

- PROMETRIKA LLC

- Rho Inc.

- Suvoda LLC

- Syneos Health Inc.

- Thermo Fisher Scientific Inc.

- Veristat LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us clinical trials market

- In August 2024, Thermo Fisher Scientific was recognized for its leadership in digital transformation services, enhancing its PPD clinical research business capabilities to accelerate trial execution.

- In November 2024, Parexel International Corp. deepened its strategic partnership with Palantir Technologies, further integrating artificial intelligence to expedite the delivery of complex clinical trial data.

- In January 2025, Laboratory Corp. of America Holdings initiated a strategic collaboration with Hawthorne Effect, a specialist in decentralized trial technology, to enhance patient diversity and access in clinical studies.

- In April 2025, Suvoda LLC launched its integrated ePatient solution for early adopters, providing a unified mobile interface for participants to manage trial-related payments, appointments, and outcomes reporting.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Clinical Trials Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 193 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 7021.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The clinical trials market in US is characterized by dynamic evolution, driven by technological integration and the increasing complexity of therapeutic development. The sustained investment in biomarker discovery is compelling a strategic pivot toward precision medicine, fundamentally altering protocol design. This shift directly influences boardroom decisions, particularly around capital allocation for advanced analytical capabilities and specialized therapeutic area expertise.

- The ascent of cell and gene therapy trials necessitates novel approaches to clinical trial logistics and gcp compliance. Organizations are adopting sophisticated clinical data management and clinical trial management system platforms to handle the intricacies of these studies. Key differentiators include proficiency in adaptive trial design, effective patient recruitment, and the capacity for robust real-world data integration.

- For instance, contract research organizations that have mastered risk-based monitoring and source data verification through technology have demonstrated a 25% reduction in query resolution times, enhancing operational efficiency. Success increasingly depends on a firm's ability to manage the entire lifecycle, from clinical monitoring and site selection and management to regulatory submission support.

What are the Key Data Covered in this US Clinical Trials Market Research and Growth Report?

-

What is the expected growth of the US Clinical Trials Market between 2026 and 2030?

-

USD 7.02 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Phase III, Phase I, Phase II, and Phase IV), Service Type (Interventional studies, Observational studies, and Expanded access studies), Indication (Oncology, CNS, Autoimmune or inflammation, and Others) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Robust growth in research and development expenditures, Systemic hurdles in patient recruitment and retention

-

-

Who are the major players in the US Clinical Trials Market?

-

Caidya, Celerion, CenExel Clinical Research, Charles River Laboratories International Inc., Clario, EPS International Holdings Co, Fortrea Holdings Inc, ICON plc, IQVIA Holdings Inc., Laboratory Holdings Inc., Medelis Inc., Medpace Holdings Inc., Parexel International Corp., PROMETRIKA LLC, Rho Inc., Suvoda LLC, Syneos Health Inc., Thermo Fisher Scientific Inc. and Veristat LLC

-

Market Research Insights

- The market is shaped by intense competition, compelling providers of cro services to innovate continuously. The adoption of patient-centric trial design and hybrid clinical trials is accelerating, with firms reporting up to a 20% improvement in patient retention rates by reducing site visit burdens.

- This shift is enabled by robust clinical trial technology and integrated eclinical solutions that enhance data quality and operational efficiency. For instance, leveraging clinical trial data analytics and risk-based monitoring allows for a more targeted allocation of resources, reducing monitoring costs by as much as 30% without compromising data integrity.

- The strategic implementation of a sophisticated patient engagement platform is now a key differentiator, directly impacting recruitment success and overall study timelines within the competitive clinical research organization landscape.

We can help! Our analysts can customize this us clinical trials market research report to meet your requirements.

RIA -

RIA -