Data Warehousing Market Size 2026-2030

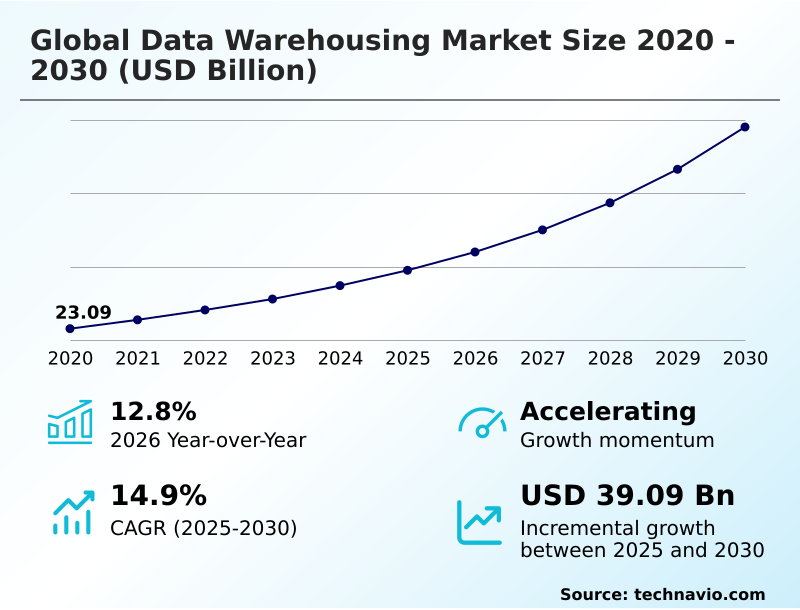

The data warehousing market size is valued to increase by USD 39.09 billion, at a CAGR of 14.9% from 2025 to 2030. Mainstreaming of generative AI and industrialization of agentic data fabric architectures will drive the data warehousing market.

Major Market Trends & Insights

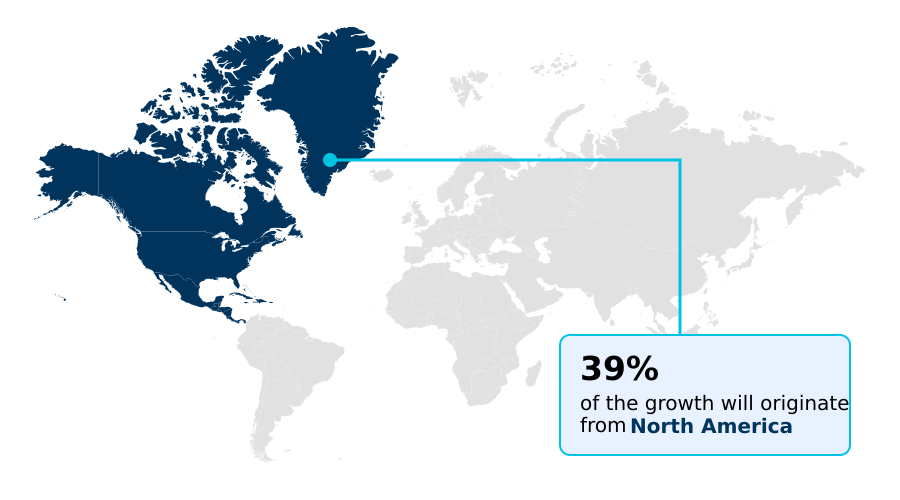

- North America dominated the market and accounted for a 39.4% growth during the forecast period.

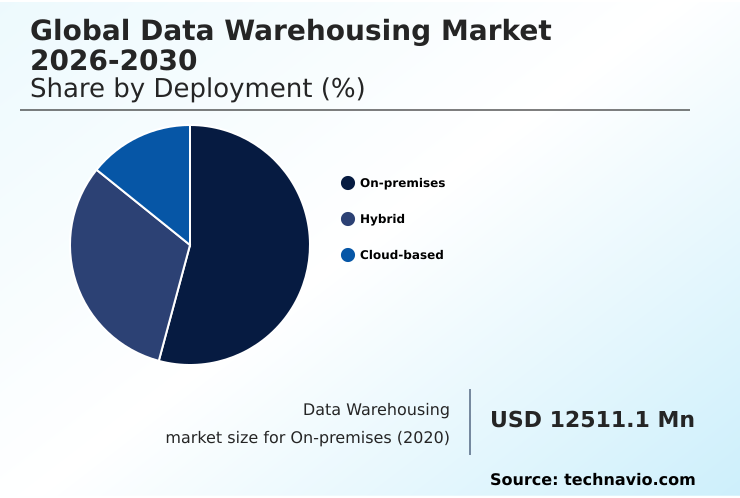

- By Deployment - On-premises segment was valued at USD 19.00 billion in 2024

- By Type - Structured and semi-structured data segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 55.01 billion

- Market Future Opportunities: USD 39.09 billion

- CAGR from 2025 to 2030 : 14.9%

Market Summary

- The data warehousing market is undergoing a significant transformation, evolving from static repositories for historical reporting into dynamic engines for real-time decision intelligence. This shift is propelled by the need to manage and analyze vast volumes of structured and unstructured data from diverse sources.

- A primary trend is the adoption of data lakehouse architecture, which combines the reliability of traditional warehouses with the flexibility of data lakes, supported by open table formats. This unified approach facilitates the mainstreaming of agentic artificial intelligence and large language models directly on operational data, eliminating complex data pipelines.

- For instance, a global retail enterprise can leverage this architecture to integrate real-time sales transaction data with unstructured customer feedback from social media, enabling immediate inventory adjustments and highly personalized marketing campaigns without data movement delays. However, organizations face challenges in managing cloud consumption costs and require robust FinOps practices.

- The market's future is shaped by the move toward autonomous governance, serverless data warehousing, and ensuring data sovereignty across multi-cloud environments, making data democratization a tangible goal for modern enterprises seeking a competitive edge through analytics.

What will be the Size of the Data Warehousing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Data Warehousing Market Segmented?

The data warehousing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

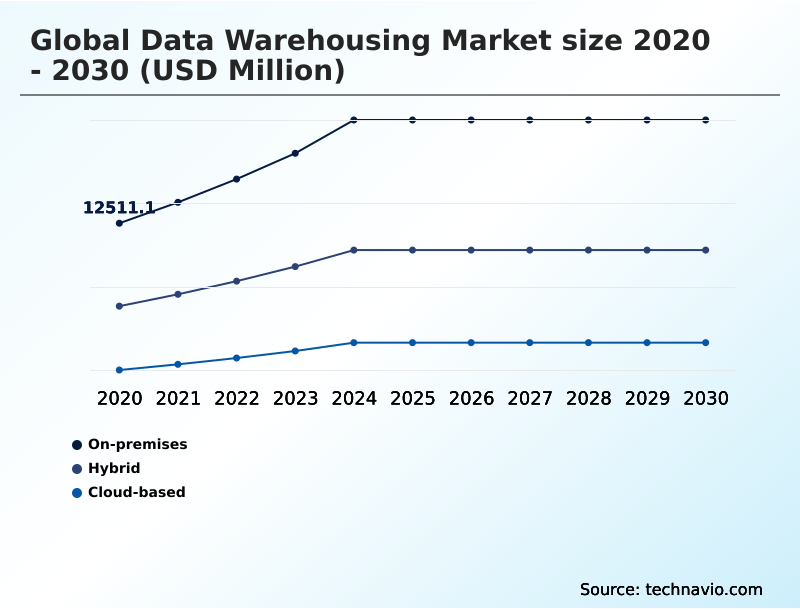

- Deployment

- On-premises

- Hybrid

- Cloud-based

- Type

- Structured and semi-structured data

- Unstructured data

- End-user

- BFSI

- Healthcare

- Retail and e-commerce

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

On-premises deployments remain a foundational pillar, particularly for organizations bound by stringent regulatory mandates that prioritize data sovereignty and data residency.

This model, which involves hosting infrastructure within an organization's own data centers, offers superior control over security and network speeds for analytical processing (OLAP).

While the overall share is contracting, on-premises systems still represent a significant portion of the market, accounting for approximately 37% of the value due to their necessity in sectors like finance and government.

Modern appliances featuring columnar storage and query optimization are narrowing the performance gap with cloud alternatives.

The high capital expenditure is often justified by the elimination of unpredictable monthly costs from unmanaged compute phenomenon and egress fees, making it a calculated choice for risk mitigation and cost predictability.

The On-premises segment was valued at USD 19.00 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Data Warehousing Market Demand is Rising in North America Get Free Sample

The global landscape is led by North America, which is projected to contribute 39.4% of the market's incremental growth, driven by the early adoption of cloud-native warehousing and the presence of major technology vendors.

Enterprises in the region have increased investments in AI-native data modernization strategies by over 20%, prioritizing platforms that decouple storage and compute.

This trend is a direct response to challenges like the unmanaged compute phenomenon, with a focus on implementing serverless data warehouse models and cost-governance tools. Europe is focused on navigating data sovereignty regulations, mandating localized residency compliance.

Meanwhile, APAC is emerging as a high-growth region, with firms rapidly adopting hybrid cloud architecture and open table formats to bypass legacy infrastructure and accelerate their digital transformation initiatives without the burden of technical debt.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Modern enterprises are strategically overhauling their data infrastructure, with a primary focus on converging structured and unstructured data to build a cohesive analytical foundation. The goal is to move toward reducing ETL with zero-ETL futures, a shift made possible by deploying AI-native lakehouse architectures.

- At the core of this transformation is understanding the role of open table formats, which provide the reliability needed for complex analytics while supporting the massive scale of data lakes. This architectural evolution enables advanced capabilities, including on-device model training and inference for edge applications and sophisticated real-time stream processing use cases.

- For example, in supply chain management, this integration has led to forecast accuracy improvements twice as effective as legacy systems. However, this transition is not without its hurdles. Key priorities include avoiding cloud consumption cost escalation and managing unpredictable query latency challenges through better governance.

- Implementing sovereign data governance standards has become non-negotiable due to the complex impact of data sovereignty regulations. Furthermore, organizations must focus on securing data with zero-trust architecture, especially when integrating legacy systems with cloud environments.

- Success hinges on optimizing a multi-cloud data warehouse strategy and overcoming the persistent challenges of data engineering talent scarcity to achieve true data democratization for non-technical users.

What are the key market drivers leading to the rise in the adoption of Data Warehousing Industry?

- The market is primarily driven by the mainstreaming of generative AI and the industrialization of agentic data fabric architectures.

- Market growth is primarily driven by the mainstreaming of generative AI and the industrialization of agentic data fabric architectures.

- The evolution of data warehouses into foundational engines for AI has spurred a 14% increase in the adoption of AI-optimized warehouse clusters, which are essential for high-speed model training and inference.

- The proliferation of real-time stream processing enables critical business functions, such as fraud detection, where its implementation has reduced false positives by up to 25%.

- This shift toward an intelligent data ecosystem is further supported by the strategic rise of multi-cloud data mesh ecosystems, which provide the agility required to manage distributed data sources effectively.

- The demand for sovereign data governance and zero-trust data standards is another key factor, compelling organizations to modernize their infrastructure.

What are the market trends shaping the Data Warehousing Industry?

- A key market trend is the institutionalization of AI-native lakehouse architectures. This involves the convergence of online transactional processing (OLTP) and online analytical processing (OLAP) systems.

- Key market trends are centered on the institutionalization of AI-native lakehouse architectures and autonomous governance, dissolving the lines between operational and analytical systems. This convergence is enabled by a unified data compute fabric, allowing real-time decision intelligence without traditional data movement delays.

- The adoption of AI-driven data observability frameworks has improved the accuracy of predictive models by over 15% by ensuring higher data quality and reliability. Furthermore, the strategic transition toward serverless data warehouse models and regional data immunity addresses both cost and compliance mandates.

- By leveraging these architectures, organizations have been able to reduce data pipeline complexity by over 40% in early use cases, a direct result of eliminating the need for separate transactional and analytical environments. Agent-centric data warehousing is at the forefront of this evolution.

What challenges does the Data Warehousing Industry face during its growth?

- A key challenge affecting industry growth is the escalation of cloud consumption costs, compounded by the economic friction from unpredictable query latency.

- The market faces significant challenges, led by the escalation of cloud consumption costs and the economic friction of unpredictable query latency. Nearly 50% of enterprises have exceeded their cloud data budgets by at least 20%, a direct result of unmanaged compute phenomenon where automated scaling triggers high-cost cycles.

- The technical debt of legacy system integration also remains a major barrier, with the scarcity of real-time data engineering talent extending project timelines by up to 30%. Furthermore, the fragmented regulatory landscape surrounding data sovereignty and the complexity of localized residency compliance add considerable operational overhead, with compliance-related activities increasing costs by 15% in multi-regional deployments.

- These issues necessitate a shift toward capacity-based pricing and algorithmic compression to ensure sustainable adoption.

Exclusive Technavio Analysis on Customer Landscape

The data warehousing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data warehousing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Data Warehousing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, data warehousing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Offerings are centered on cloud data warehousing, AI-native platforms, and real-time analytics, enabling unified governance and advanced data intelligence for enterprise operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Cloudera Inc.

- Databricks Inc.

- Firebolt

- Google LLC

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Informatica Inc.

- Infosys Ltd.

- Microsoft Corp.

- MongoDB Inc.

- Oracle Corp.

- QlikTech International AB

- SAP SE

- SingleStore Inc.

- Snowflake Inc.

- Teradata Corp.

- Yellowbrick Data Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data warehousing market

- In May, 2025, Databricks Inc. announced the general availability of its Lakebase service, a managed, serverless PostgreSQL database designed to operate directly on the Databricks Data Intelligence Platform, enabling operational applications and AI agents on a unified data foundation.

- In April, 2025, Snowflake Inc. launched Cortex Code, an intelligent, fully managed service designed to automate data engineering, application development, and data analysis tasks within the Snowflake AI Data Cloud, leveraging large language models to convert natural language to SQL.

- In February, 2025, Datadog Inc. announced the launch of a new data center in the United Kingdom, designed to help financial services and public sector organizations meet local data residency and sovereignty requirements for their observability and analytical telemetry.

- In November, 2024, Amazon.com Inc. enhanced its Amazon Web Services Redshift platform by updating materialized view auto-refresh functions to a user-query priority model, ensuring that analytical snapshots remain more closely synchronized with real-time base table changes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Warehousing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.9% |

| Market growth 2026-2030 | USD 39085.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data warehousing market is undergoing a fundamental architectural shift from static repositories to intelligent, distributed ecosystems. This evolution is defined by the adoption of data lakehouse architecture and cloud-native warehousing, which merge the reliability of columnar storage with the scalability of the cloud.

- Core technologies such as massively parallel processing (MPP) and advanced ETL/ELT processes are being re-engineered for a serverless data warehousing model. A crucial trend influencing boardroom strategy is the increasing importance of data sovereignty and data residency, forcing global organizations to adopt multi-cloud strategies and hybrid cloud architecture to comply with regional regulations.

- This requires robust unified governance and metadata management to maintain control. The integration of specialized hardware accelerators is demonstrably improving performance, with some organizations reporting up to a 30% reduction in processing times for complex analytical workloads. This allows for real-time applications using vector embeddings and semantic search capabilities, driven by an agentic data fabric.

- The rise of FinOps is also critical for managing consumption-based models and ensuring cost efficiency as data democratization expands across the enterprise.

What are the Key Data Covered in this Data Warehousing Market Research and Growth Report?

-

What is the expected growth of the Data Warehousing Market between 2026 and 2030?

-

USD 39.09 billion, at a CAGR of 14.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, Hybrid, and Cloud-based), Type (Structured and semi-structured data, and Unstructured data), End-user (BFSI, Healthcare, Retail and e-commerce, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Mainstreaming of generative AI and industrialization of agentic data fabric architectures, Escalation of cloud consumption costs and economic friction of unpredictable query latency

-

-

Who are the major players in the Data Warehousing Market?

-

Amazon.com Inc., Cloudera Inc., Databricks Inc., Firebolt, Google LLC, HCL Technologies Ltd., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., IBM Corp., Informatica Inc., Infosys Ltd., Microsoft Corp., MongoDB Inc., Oracle Corp., QlikTech International AB, SAP SE, SingleStore Inc., Snowflake Inc., Teradata Corp. and Yellowbrick Data Inc.

-

Market Research Insights

- The market is defined by a rapid pivot toward intelligent, automated data ecosystems. This transition to agent-centric data warehousing and a unified data compute fabric is driven by the need for real-time decision intelligence. Organizations are actively deploying autonomous self-tuning systems to reduce manual oversight and operational friction.

- This shift addresses significant fiscal pressures; for example, the adoption of advanced query-tuning services helps mitigate budget overruns, where nearly half of enterprises previously exceeded cloud spend by over 20%. Furthermore, the proliferation of AI-optimized warehouse clusters, showing a 14% increase in adoption, directly accelerates predictive analytics and machine learning workloads.

- These advancements, coupled with automated data cataloging, are enabling a new class of context-aware insights while optimizing resource utilization.

We can help! Our analysts can customize this data warehousing market research report to meet your requirements.

RIA -

RIA -