US Concierge Medicine Market Size 2026-2030

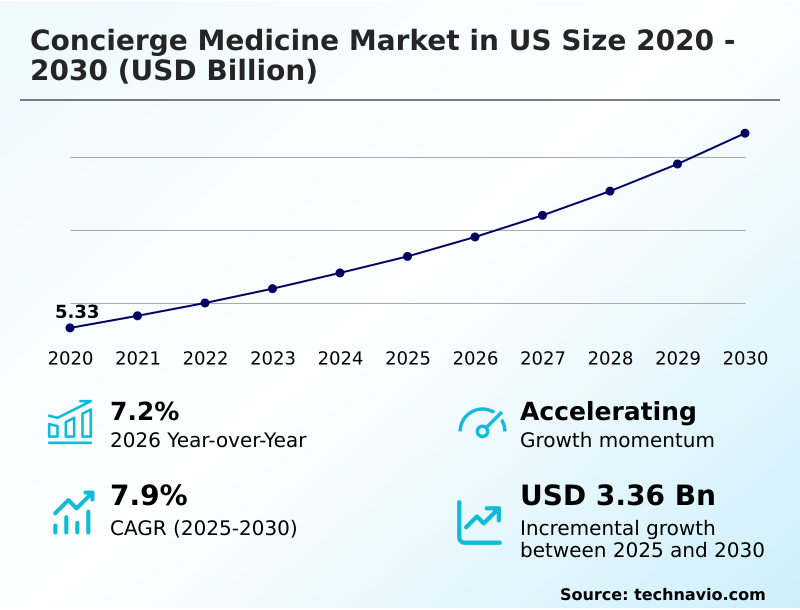

The us concierge medicine market size is valued to increase by USD 3.36 billion, at a CAGR of 7.9% from 2025 to 2030. Mitigating physician burnout and enhancing professional longevity will drive the us concierge medicine market.

Major Market Trends & Insights

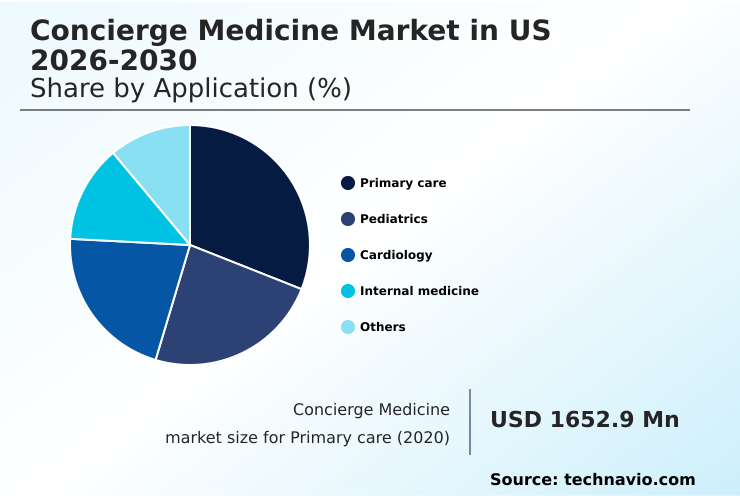

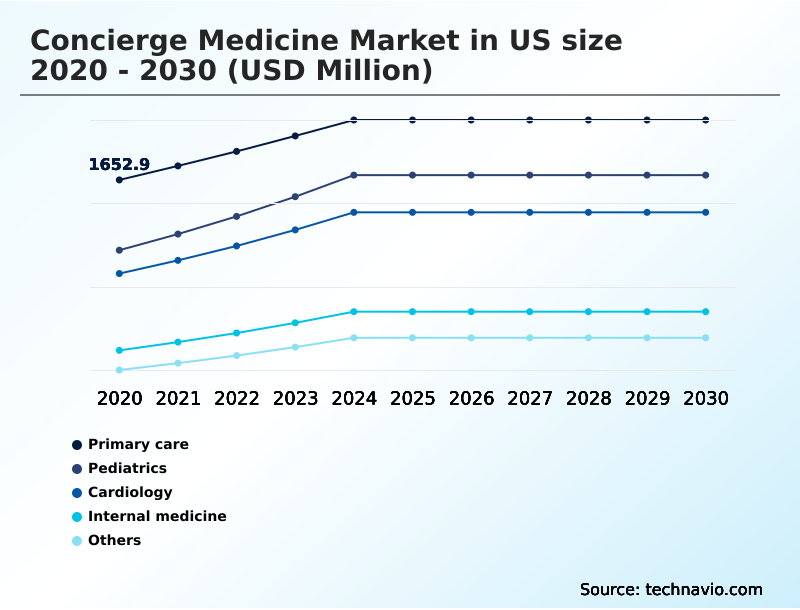

- By Application - Primary care segment was valued at USD 1.99 billion in 2024

- By Ownership - Group segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.31 billion

- Market Future Opportunities: USD 3.36 billion

- CAGR from 2025 to 2030 : 7.9%

Market Summary

- The concierge medicine market in US is defined by a healthcare delivery model based on a direct financial relationship between patients and physicians, moving beyond traditional insurance-based systems. This patient-centric approach operates within a value-based care framework, where a recurring membership fee ensures enhanced access and highly personalized attention.

- Key applications include comprehensive wellness planning and proactive management of chronic conditions, facilitated by a focus on preventive health screenings and advanced diagnostic integration. The model's relevance is growing as both patients and practitioners seek alternatives to high-volume, impersonal medical environments.

- A core driver is the significant administrative burden reduction for physicians, allowing them to bypass complex insurance billing and focus on clinical outcomes. For example, a mid-sized corporation implementing direct primary care (dpc) models for its executive team can reduce healthcare-related absenteeism by ensuring prompt medical attention and continuous health monitoring, directly improving operational efficiency and employee well-being.

- This paradigm shift toward quality over quantity highlights a broader movement in the US medical system.

What will be the Size of the US Concierge Medicine Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Concierge Medicine Market Segmented?

The us concierge medicine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Primary care

- Pediatrics

- Cardiology

- Internal medicine

- Others

- Ownership

- Group

- Standalone

- Service type

- Entry level

- Mid level

- Premium

- Geography

- North America

- US

- North America

By Application Insights

The primary care segment is estimated to witness significant growth during the forecast period.

The primary care segment is central to the concierge medicine market in US, shifting away from the inherent fee-for-service model limitations.

This model emphasizes personalized healthcare programs and proactive health management, driven by rising consumer healthcare expectations for more attentive care. It operates on a membership-based primary care structure, which facilitates a stronger physician-patient relationship and direct physician access.

For a transparent fee, patients receive comprehensive wellness planning, a stark contrast to navigating high-deductible health plans for routine care. This focus on patient-centric healthcare delivery significantly boosts patient satisfaction metrics.

This trend is amplified as a recent survey showed 62% of physicians have made career changes, seeking sustainable models that allow for 24/7 clinician access and deeper patient engagement.

The Primary care segment was valued at USD 1.99 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The concierge medicine market in US is evolving beyond a one-size-fits-all approach, with distinct models emerging to meet specific patient needs. The debate over direct primary care versus concierge medicine often centers on service scope and cost, with both models offering an alternative to traditional care.

- For patients with ongoing health issues, concierge medicine for chronic disease management provides unparalleled continuity and proactive oversight. The costs and benefits of concierge healthcare are a key consideration for consumers, who weigh membership fees against enhanced access and preventive care.

- Many practices are now implementing a hybrid concierge care model, leveraging telehealth integration in membership-based care to offer both virtual and in-person consultations. This flexibility is particularly valuable for pediatric and family concierge medical services.

- On the corporate side, corporate concierge programs for employee wellness are becoming a strategic tool for talent retention, with firms increasingly interested in measuring ROI of executive health programs. However, legal challenges in concierge medicine practice, especially navigating medicare rules in concierge practice, remain a significant hurdle.

- Specialty practices are also growing, with concierge cardiology and specialty care models providing focused expertise. This growth is tempered by ethical considerations in patient panel limitations. The model's success hinges on improving physician work-life balance with concierge models and enhancing the patient experience in high-touch healthcare services. The concierge medicine role in preventive health is perhaps its most significant contribution.

- For instance, practices that reduce physician administrative tasks by over 40% compared to traditional settings can reallocate that time to patient-facing preventive care, directly impacting long-term health outcomes.

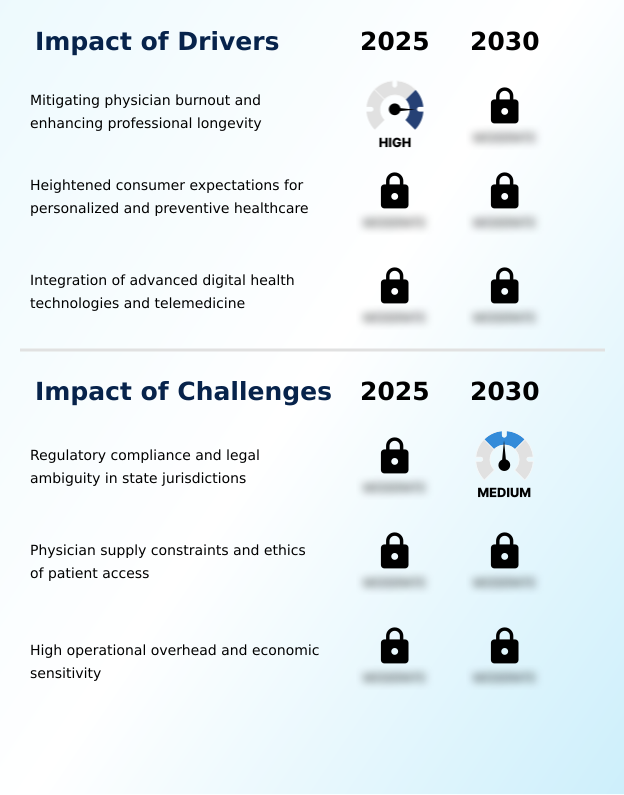

What are the key market drivers leading to the rise in the adoption of US Concierge Medicine Industry?

- Mitigating physician burnout and enhancing professional longevity are key drivers for the adoption of concierge medicine models.

- A key driver is the urgent need for physician burnout mitigation and professional longevity enhancement. The traditional model, which often assigns over 2,500 patients per physician, is unsustainable, leading to significant administrative burden.

- The membership-based financial model allows practices to reduce panel sizes to under 600 patients, facilitating longer appointments and improving clinical outcome optimization. This focus on quality is crucial for medical talent retention amid growing physician supply constraints.

- Furthermore, integrated health services are being leveraged for patient attrition prevention.

- The model’s ability to generate predictable revenue streams is attracting private equity investment in healthcare, enabling practices to achieve economies of scale in healthcare and invest in technologies that support superior care delivery.

What are the market trends shaping the US Concierge Medicine Industry?

- A primary trend is the evolution of hybrid care models that blend in-person visits with digital health integration. This shift prioritizes continuous physician-patient connectivity through advanced telehealth platforms and remote monitoring tools.

- A dominant trend is the rapid evolution of hybrid care delivery models, driven by digital health technology integration. This shift combines the convenience of on-demand medical services with traditional high-touch service delivery. Providers are employing service differentiation strategies, offering specialized diagnostic screenings and real-time vital statistics tracking to stand out.

- This data-driven healthcare approach enables a move from 15-minute appointments to consultations lasting an hour or more. Overcoming brand establishment barriers is crucial as new entrants adopt these technologies.

- While the ethics of patient access remain a topic of discussion, automated decision-making technology (admt) is helping to streamline workflows, allowing physicians to manage smaller patient panels of 400-600 individuals effectively, thereby personalizing care.

What challenges does the US Concierge Medicine Industry face during its growth?

- Navigating regulatory compliance issues and the legal ambiguity across different state jurisdictions presents a significant challenge to market growth.

- A primary challenge lies within the complex regulatory and legal frameworks, where state jurisdiction legal ambiguity creates significant operational hurdles. Practices face uncertainty over membership fee classification and strict federal program reimbursement rules, particularly concerning Medicare. The absence of unified federal standards for direct primary care (dpc) models forces providers to conduct constant and costly legal reviews.

- This environment, coupled with high operational overhead and the need for specialized medical staffing, demands a thorough economic sensitivity analysis. Furthermore, as physician practice transformation accelerates, ensuring robust cybersecurity audit compliance becomes paramount to protect patient data, adding another layer of complexity for providers navigating this evolving market.

Exclusive Technavio Analysis on Customer Landscape

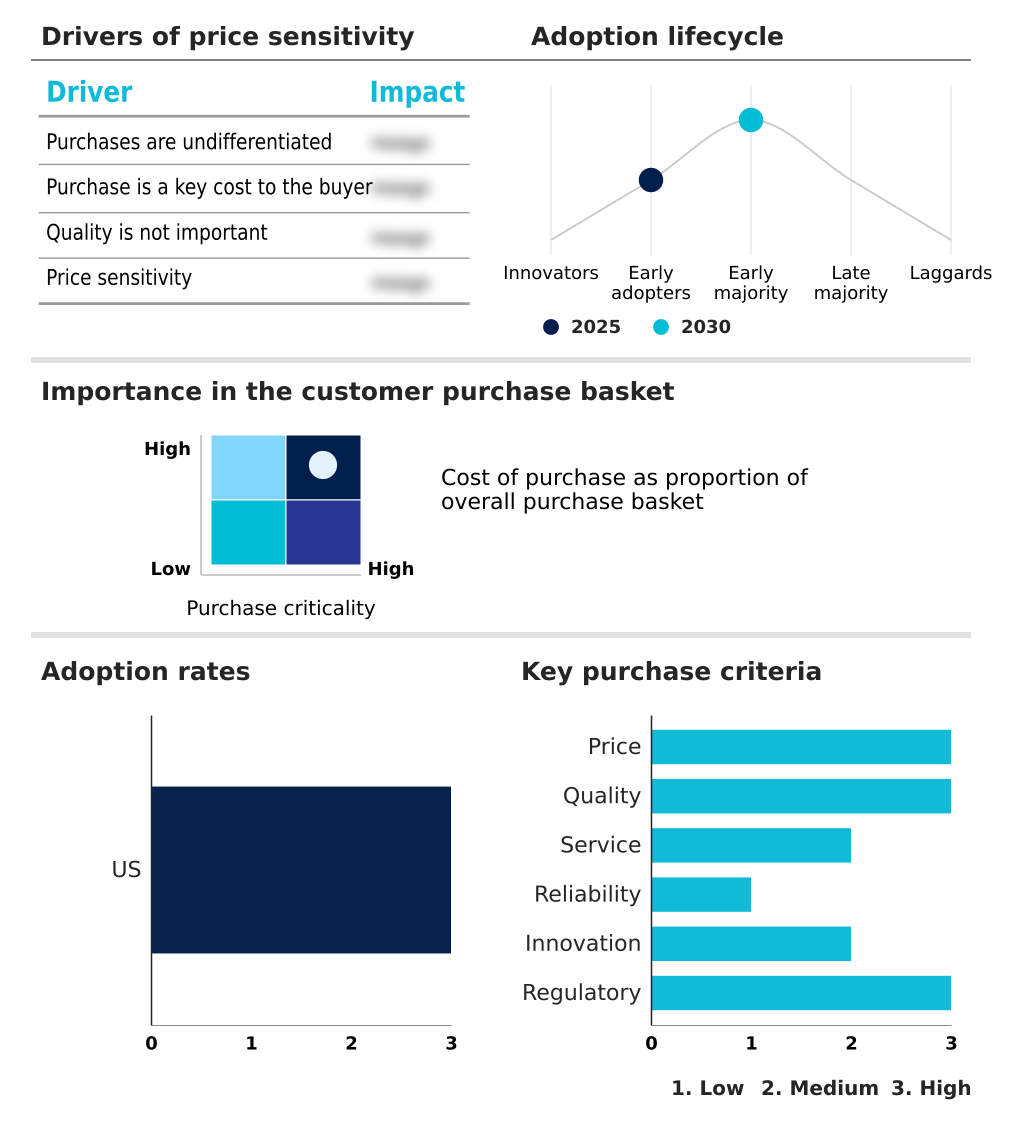

The us concierge medicine market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us concierge medicine market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Concierge Medicine Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us concierge medicine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

1Life Healthcare Inc. - Provides personalized, membership-based primary care integrating digital health tools and preventive wellness programs for enhanced patient access and proactive health management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 1Life Healthcare Inc.

- Castle Connolly Health Partners

- Cedars Sinai Health System

- Crossover Health

- Diamond Physicians

- Hoag Memorial Hospital

- Mass General Brigham Inc.

- Mayo Clinic

- MDVIP Inc.

- Mount Sinai Health System

- Northwestern Medicine

- PartnerMD LLC

- Penn Medicine

- SignatureMD Inc.

- Sollis Health

- Stanford Health Care

- Sutter Health

- The Cleveland Clinic Foundation

- UC San Diego Health

- WorldClinic

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us concierge medicine market

- In August 2024, Mayo Clinic launched a groundbreaking population omics strategy, integrating large-scale biological data with environmental factors to advance personalized diagnostics and treatments for complex diseases.

- In September 2024, Tempus AI, Inc. introduced the beta version of its AI-powered personal health concierge app, olivia, designed to empower patients by consolidating and managing their health information from multiple sources.

- In June 2024, a survey from CHG Healthcare revealed that 62% of US physicians have recently changed their job situations, with many transitioning away from traditional patient care due to burnout.

- In June 2025, the California Privacy Protection Agency published stakeholder feedback on proposed regulations for automated decision-making technology (ADMT), impacting the compliance landscape for digital health and concierge medicine providers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Concierge Medicine Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 177 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.9% |

| Market growth 2026-2030 | USD 3356.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.2% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The concierge medicine market in US is defined by the proliferation of personalized healthcare programs and membership-based primary care models. These systems are built on strengthening the physician-patient relationship through direct physician access and limiting patient panel size. A core component is proactive health management, achieved via preventive health screenings, continuous health monitoring, and comprehensive wellness planning.

- The integration of advanced diagnostic integration and telehealth consultation platforms supports this high-touch service delivery. Many providers also offer specialized executive health programs and corporate wellness solutions. This move toward a value-based care framework is further advanced by the adoption of genomic screening services and population omics strategy for longevity and precision medicine.

- This shift allows for administrative burden reduction, enabling physicians to focus on clinical outcome optimization. Boardroom decisions are increasingly influenced by data showing that over 62% of physicians have recently changed careers, making physician practice transformation essential for talent retention.

- Practices are using integrated health services to offer a holistic health approach, supported by automated decision-making technology (admt) and real-time vital statistics tracking to prevent patient attrition. This data-driven healthcare approach also necessitates robust cybersecurity audit compliance within the membership-based financial model.

What are the Key Data Covered in this US Concierge Medicine Market Research and Growth Report?

-

What is the expected growth of the US Concierge Medicine Market between 2026 and 2030?

-

USD 3.36 billion, at a CAGR of 7.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Primary care, Pediatrics, Cardiology, Internal medicine, and Others), Ownership (Group, and Standalone), Service Type (Entry level, Mid level, and Premium) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Mitigating physician burnout and enhancing professional longevity, Regulatory compliance and legal ambiguity in state jurisdictions

-

-

Who are the major players in the US Concierge Medicine Market?

-

1Life Healthcare Inc., Castle Connolly Health Partners, Cedars Sinai Health System, Crossover Health, Diamond Physicians, Hoag Memorial Hospital, Mass General Brigham Inc., Mayo Clinic, MDVIP Inc., Mount Sinai Health System, Northwestern Medicine, PartnerMD LLC, Penn Medicine, SignatureMD Inc., Sollis Health, Stanford Health Care, Sutter Health, The Cleveland Clinic Foundation, UC San Diego Health and WorldClinic

-

Market Research Insights

- Market dynamics are shaped by pronounced fee-for-service model limitations and heightened consumer healthcare expectations for personalized attention. The threat of rivalry drives providers to adopt robust service differentiation strategies, including specialized diagnostic screenings and transparent pricing structures. This is critical for physician burnout mitigation, as practitioners transition from unmanageable patient panels of over 2,000 to focused groups of 400-600.

- This change enables a dramatic shift in care quality, extending appointments from less than 15 minutes to over an hour. While the bargaining power of buyers is moderate, demanding high-value returns for membership fees, the bargaining power of suppliers, particularly physicians, is increasing due to talent shortages. This environment forces practices to balance premium service delivery with operational efficiency.

We can help! Our analysts can customize this us concierge medicine market research report to meet your requirements.

RIA -

RIA -