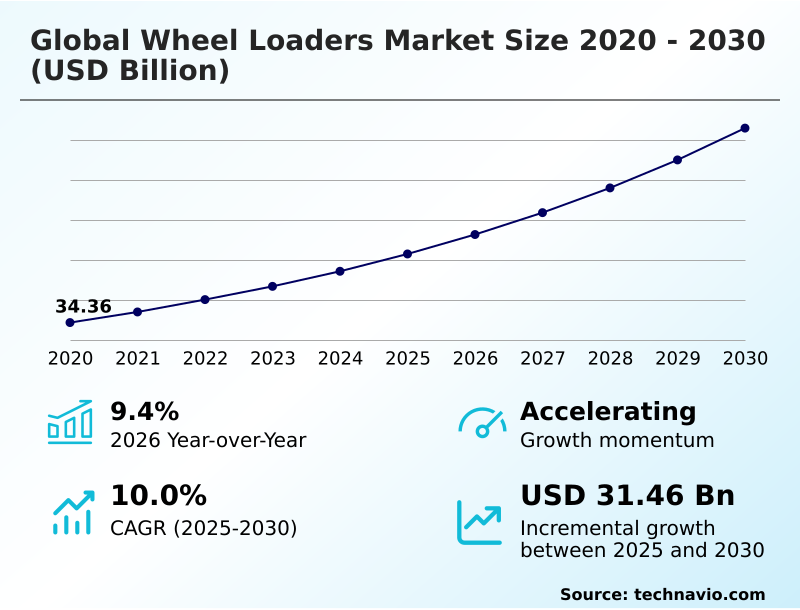

Wheel Loaders Market Size 2026-2030

The wheel loaders market size is valued to increase by USD 31.46 billion, at a CAGR of 10% from 2025 to 2030. Expansion of global infrastructure and urbanization initiatives will drive the wheel loaders market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 34.9% growth during the forecast period.

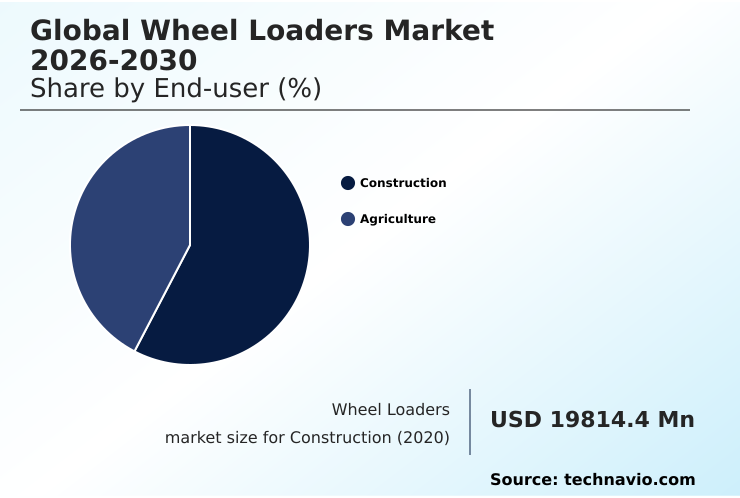

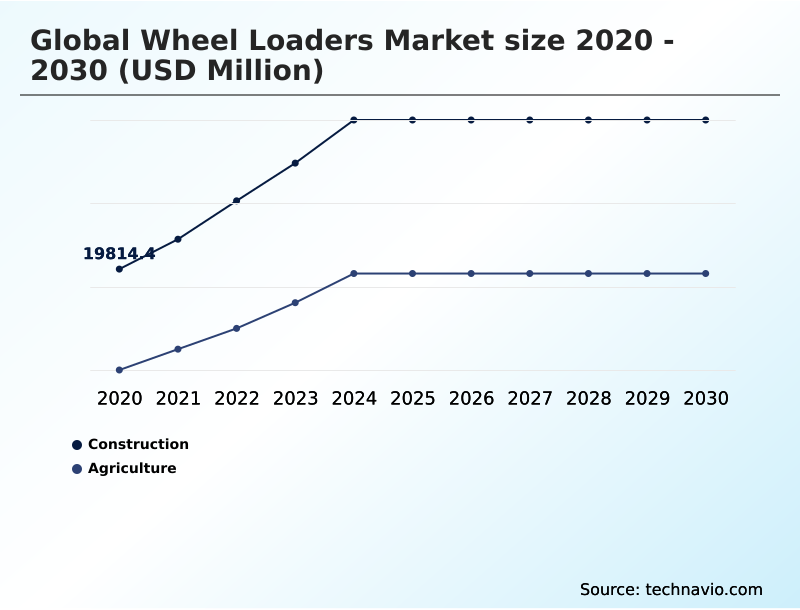

- By End-user - Construction segment was valued at USD 27.59 billion in 2024

- By Power Output - More than 80 HP segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 48.61 billion

- Market Future Opportunities: USD 31.46 billion

- CAGR from 2025 to 2030 : 10%

Market Summary

- The wheel loaders market is undergoing a significant transformation, driven by technological advancement and evolving end-user requirements. A primary driver is the global expansion of infrastructure projects, which necessitates efficient and powerful earthmoving equipment. Concurrently, a major trend is the shift toward sustainability, with manufacturers increasingly developing hybrid powertrain architectures and fully electric models to comply with stricter emissions standards.

- This transition to green technology is particularly evident in urban construction, where reduced noise and zero tailpipe emissions are critical.

- For instance, a logistics firm managing a large urban distribution center might deploy a fleet of electric compact wheel loaders for indoor and outdoor material handling, leveraging their quiet operation for 24/7 schedules while using advanced telematics systems to monitor battery status and optimize charging cycles, thereby reducing operational costs and environmental impact.

- However, the industry faces challenges from supply chain disruptions affecting the availability of critical components like semiconductors and high-grade steel, alongside a persistent shortage of skilled operators capable of managing technologically advanced machinery. The integration of industrial AI, remote-control operation, and predictive maintenance capabilities represents the industry's response, aiming to boost productivity and safety while mitigating labor gaps.

What will be the Size of the Wheel Loaders Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Wheel Loaders Market Segmented?

The wheel loaders industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Construction

- Agriculture

- Power output

- More than 80 HP

- 40 to 80 HP

- Less than 40 HP

- Product type

- Medium

- Large

- Compact

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period.

The construction segment remains the primary end-user, with a significant shift toward specialized machinery for urban redevelopment. Demand is centered on high-efficiency equipment that integrates digital solutions to optimize site productivity and reduce idle times.

This includes the adoption of compact wheel loaders for confined urban spaces and larger earthmoving equipment for major infrastructure projects. Modern intelligent machine control systems are a key focus, improving grading accuracy by over 25% and contributing to operational sustainability.

The adoption of semi-autonomous features and zero-emission construction machinery is accelerating, driven by the need for precision engineering in data-driven construction environments.

This evolution addresses both the total cost of ownership and the increasing complexity of large-scale civil engineering projects, demanding high-performance heavy loaders and advanced site preparation machinery.

The Construction segment was valued at USD 27.59 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

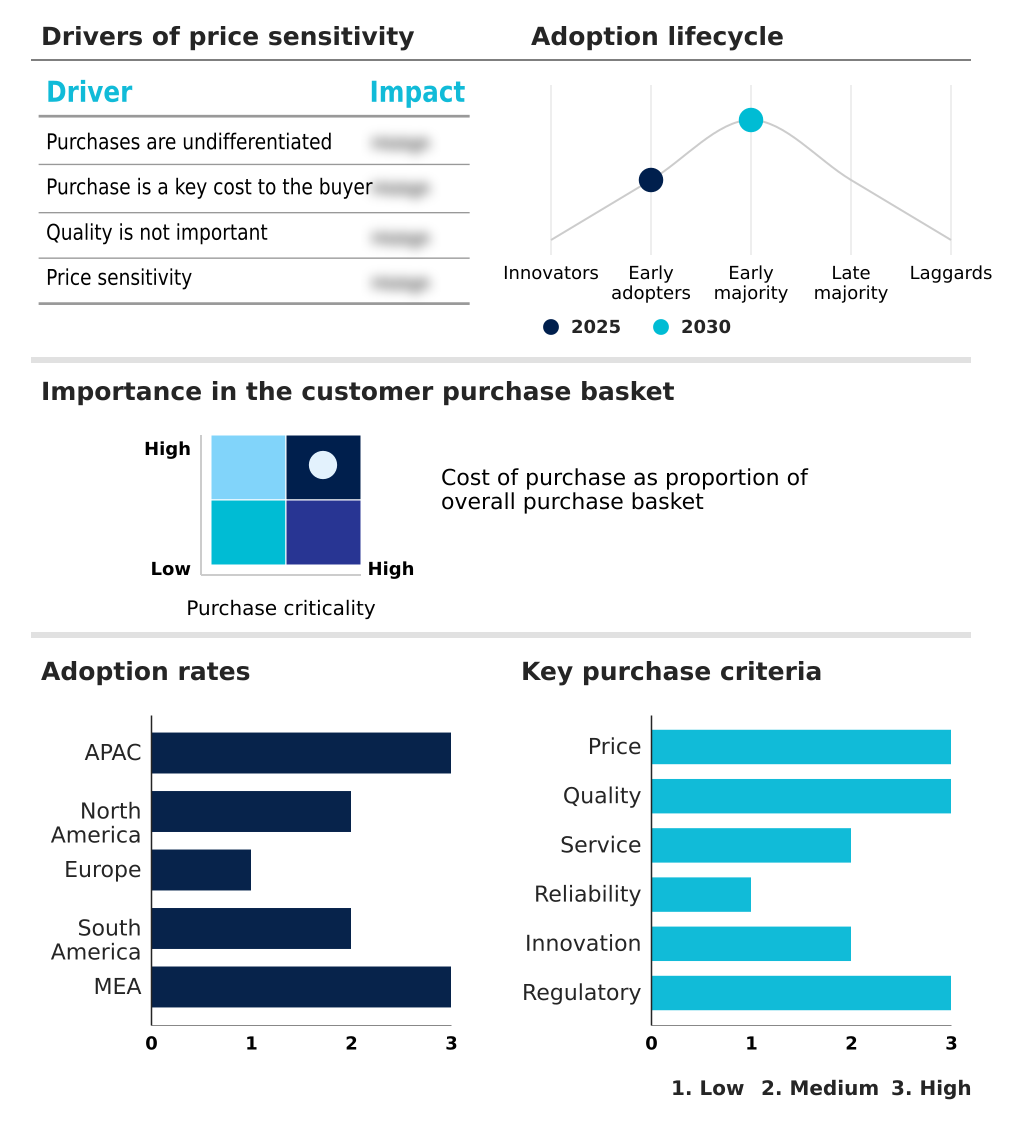

APAC is estimated to contribute 34.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wheel Loaders Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by diverse regional demands and technological adoption rates. APAC leads market expansion, contributing nearly 35% of the incremental growth, driven by massive infrastructure projects in China and India where robust, cost-effective machinery is essential.

In contrast, North America and Europe focus on advanced technology, adopting large wheel loaders and sophisticated joystick steering for quarrying and upgrading public works with sustainable energy infrastructure.

European markets, in particular, pioneer the use of bio-hydraulic oils and circular economy practices.

In South America, a pilot program for hybrid-electric wheel loaders demonstrated a 20% extension in battery life, highlighting the region's focus on operational efficiency in high-altitude mining operations.

This global variance requires manufacturers to offer a diverse portfolio, from heritage-sensitive compact units for urban projects to high-performance heavy loaders for resource extraction.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making for fleet acquisition requires a thorough analysis of both immediate and long-term factors. A fleet manager must evaluate the benefits of telematics in wheel loaders, which can improve asset utilization and enable predictive maintenance for wheel loader fleets.

- The choice between traditional diesel and emerging technologies involves weighing the initial cost of ownership for electric wheel loaders against their lower operational expenses and ability to meet tightening emission standards. For urban projects, electric wheel loaders for urban construction are becoming essential. In parallel, heavy industries are exploring autonomous wheel loaders in mining to enhance safety and productivity.

- Key performance considerations include improving wheel loader cycle times and reducing wheel loader fuel consumption, which is directly tied to wheel loader hydraulic system efficiency. Incorporating advanced operator comfort and ergonomic design, alongside robust wheel loader operator safety features, is crucial for retention and performance.

- Fleets using telematics for wheel loader fleet management have reported fuel savings of up to 15% compared to unmonitored operations, showcasing how technology directly impacts profitability. This detailed assessment ensures that investments in machinery for applications in waste management or infrastructure are both effective and sustainable.

What are the key market drivers leading to the rise in the adoption of Wheel Loaders Industry?

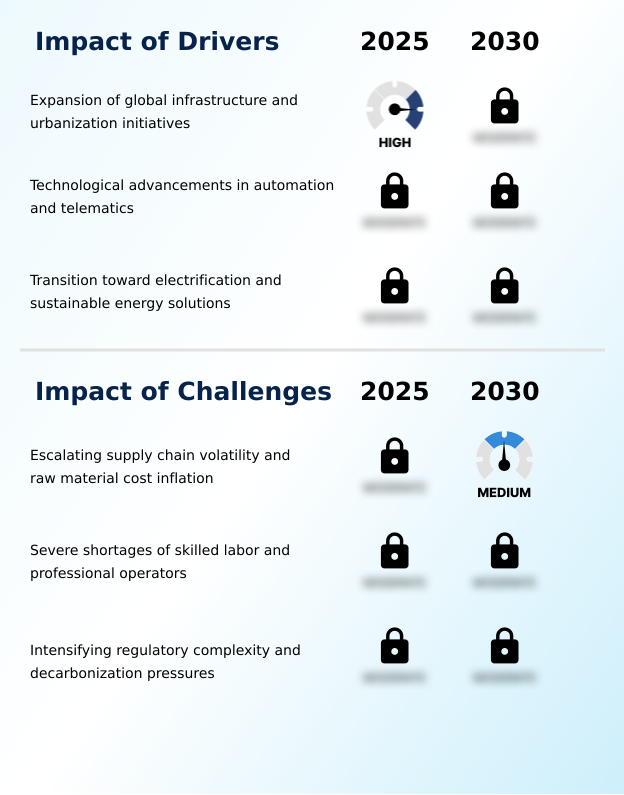

- The expansion of global infrastructure and urbanization initiatives serves as the key driver for market growth.

- Market growth is fundamentally driven by large-scale infrastructure development and the industry-wide adoption of digital technologies. The integration of advanced telematics systems and smart hydraulics allows for real-time monitoring of fuel consumption and mechanical health, directly supporting predictive maintenance.

- This shift toward intelligent machinery, featuring automated bucket leveling, is especially prevalent where contractors seek to improve output. New engine technologies are delivering tangible benefits, with some models achieving a 5% improvement in fuel efficiency.

- This push for efficiency is coupled with a focus on enhancing operator safety through features like intelligent speed control.

- The demand for such advancements ensures that wheel loaders remain essential components of modern construction, especially as the industry grapples with significant skilled labor shortages.

What are the market trends shaping the Wheel Loaders Industry?

- The integration of artificial intelligence and autonomous operating systems is a significant upcoming trend. This is reshaping the market by enhancing operational efficiency and precision.

- The market is rapidly evolving with the integration of intelligent technologies and sustainable power sources. A dominant trend is the proliferation of hybrid powertrain architectures and remote-control operation, which are becoming critical for enhancing site safety and efficiency. Advanced sensors and industrial AI are enabling automated payload measurement and augmented reality overlays in operator cabins, transforming data-driven construction practices.

- In high-altitude mining operations, regenerative braking systems have been shown to extend battery life by nearly 20%, significantly improving the viability of electric models. Concurrently, the adoption of on-board weighing systems and advanced diagnostic tools is streamlining material handling and maintenance, solidifying the shift towards a more connected and autonomous job site.

What challenges does the Wheel Loaders Industry face during its growth?

- Escalating supply chain volatility and raw material cost inflation present a key challenge affecting the industry's growth.

- The market faces significant headwinds from supply chain instability and evolving regulatory pressures. Structural issues have led to logistical bottlenecks, with shipping disruptions contributing to a 30% surge in freight costs for critical components, complicating regionalized sourcing strategies. This volatility directly impacts production cycles for machinery reliant on high-grade steel and hydraulic components.

- Furthermore, the industry is navigating intensifying decarbonization pressures, which demand substantial investment in new technologies while managing the complexities of a multi-tiered regulatory landscape. The transition toward electrification also introduces challenges in scaling production of zero-emission portfolios, particularly concerning the volatile pricing of essential raw materials. These factors collectively test manufacturers' ability to maintain profitability while advancing technological innovation.

Exclusive Technavio Analysis on Customer Landscape

The wheel loaders market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wheel loaders market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wheel Loaders Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wheel loaders market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CASE Construction - A focused portfolio of wheel loaders serves key applications in construction, mining, and energy, with models engineered for diverse operational demands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CASE Construction

- Caterpillar Inc.

- CNH Industrial N.V.

- Deere and Co.

- Doosan Corp.

- HD Hyundai Construction

- Hitachi Construction Machinery

- J C Bamford Excavators Ltd.

- Komatsu Ltd.

- Kubota Corp.

- Liebherr International AG

- Liugong Machinery Co. Ltd.

- Manitou BF SA

- Sany Heavy Industry Co. Ltd.

- SDLG Construction Machinery

- Terex Corp.

- Volvo Construction Equipment

- Wacker Neuson SE

- Weichei Lovol Heavy Industry

- Xuzhou Construction Machinery

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wheel loaders market

- In October, 2024, Volvo Construction Equipment announced the launch of its L120 Electric wheel loader in the Middle East, confirming its operational reliability in extreme heat conditions following rigorous field testing in the UAE.

- In January, 2025, Caterpillar Inc. showcased its Cat 972 Wheel Loader at CES 2025, featuring an Extended Range Electrified Machine hybrid retrofit demonstrator, highlighting a new approach to electrification without requiring DC fast-charging infrastructure.

- In February, 2025, Liebherr-Werk Bischofshofen GmbH announced it would unveil its Autonomous Operations system for driverless wheel loader operation and an L 566 H hydrogen-engine large wheel loader prototype at Bauma 2025.

- In April, 2025, Volvo Construction Equipment announced the introduction of its new generation of wheel loaders, launching five models from the L150 to the L260, engineered to enhance productivity, operator comfort, and safety.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wheel Loaders Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10% |

| Market growth 2026-2030 | USD 31457.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.4% |

| Key countries | China, India, Japan, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The wheel loaders market is pivoting toward a new operational paradigm defined by technological sophistication and sustainability mandates. Boardroom-level strategy is now centered on balancing investments in next-generation platforms, such as those utilizing lithium-ion battery technology or hydrogen fuel cells, against the optimization of existing diesel fleets through advanced exhaust after-treatment systems.

- The integration of autonomous operating systems, predictive maintenance protocols, and digital fleet management is no longer a niche but a core competitive differentiator. From heavy-duty quarrying operations and mining operations to agricultural logistics and site preparation machinery, the demand is for intelligent, connected equipment. High-capacity charging stations, 360-degree camera systems, and rear object identification are becoming standard safety requirements.

- The latest generation of load-sensing hydraulics has demonstrated the ability to reduce cycle times by over 10% in material handling applications. This evolution impacts every category, including compact wheel loaders, medium wheel loaders, and large wheel loaders, all while being governed by the core principles of high breakout force and robust articulated steering mechanisms.

- Innovations in joystick steering, high-flow hydraulic systems, and specialized cooling systems are further refining performance for heavy-duty filtration and cold-weather performance scenarios.

What are the Key Data Covered in this Wheel Loaders Market Research and Growth Report?

-

What is the expected growth of the Wheel Loaders Market between 2026 and 2030?

-

USD 31.46 billion, at a CAGR of 10%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Construction, and Agriculture), Power Output (More than 80 HP, 40 to 80 HP, and Less than 40 HP), Product Type (Medium, Large, and Compact) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Expansion of global infrastructure and urbanization initiatives, Escalating supply chain volatility and raw material cost inflation

-

-

Who are the major players in the Wheel Loaders Market?

-

CASE Construction, Caterpillar Inc., CNH Industrial N.V., Deere and Co., Doosan Corp., HD Hyundai Construction, Hitachi Construction Machinery, J C Bamford Excavators Ltd., Komatsu Ltd., Kubota Corp., Liebherr International AG, Liugong Machinery Co. Ltd., Manitou BF SA, Sany Heavy Industry Co. Ltd., SDLG Construction Machinery, Terex Corp., Volvo Construction Equipment, Wacker Neuson SE, Weichei Lovol Heavy Industry and Xuzhou Construction Machinery

-

Market Research Insights

- Market dynamics are shaped by a strategic push toward operational sustainability and data-driven construction. The adoption of operator assist technologies is accelerating, with regenerative braking systems in some hybrid models extending battery life by nearly 20% in high-altitude mining operations. This enhances the value proposition beyond initial procurement, directly impacting the total cost of ownership.

- However, significant challenges persist; shipping disruptions have contributed to a 30% surge in freight costs for some components, complicating regionalized sourcing strategies.

- Furthermore, a critical shortage of skilled labor, with an estimated need for 349,000 new workers in the US construction sector alone, underscores the urgency for firms to invest in technologies that improve productivity and align with corporate social responsibility goals.

We can help! Our analysts can customize this wheel loaders market research report to meet your requirements.

RIA -

RIA -