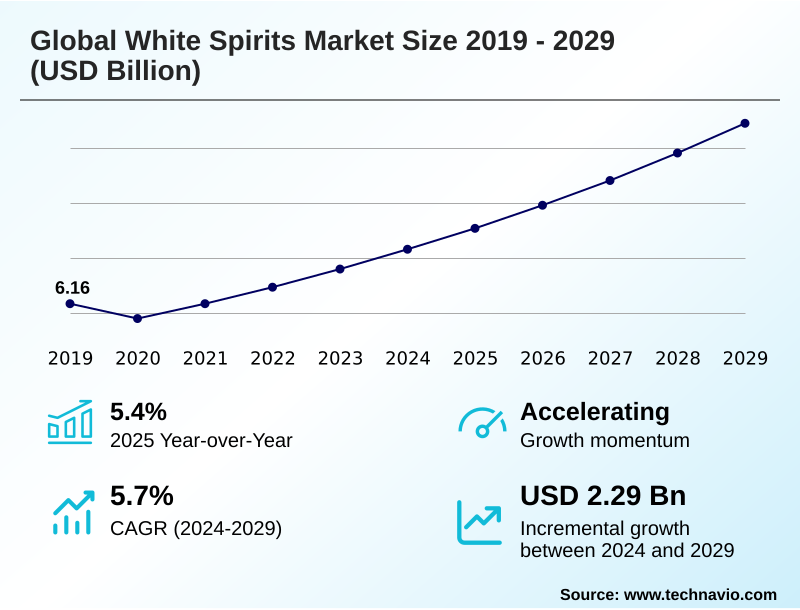

White Spirits Market Size 2025-2029

The white spirits market size is valued to increase by USD 2.29 billion, at a CAGR of 5.7% from 2024 to 2029. Growing usage of white spirits as cleaning and degreasing agent will drive the white spirits market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 35.2% growth during the forecast period.

- By Application - Thinner and solvent segment was valued at USD 2.01 billion in 2023

- By Grade Type - Regular flash segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 3.27 billion

- Market Future Opportunities: USD 2.29 billion

- CAGR from 2024 to 2029 : 5.7%

Market Summary

- The white spirits market is undergoing a significant transformation, balancing its foundational role in industries like paints and coatings with a pressing need for environmental responsibility. Demand is sustained by the performance of these hydrocarbon-based solvent products as a paint thinner formulation and an industrial degreasing agent. However, concerns over volatile organic compounds are reshaping the landscape.

- A key business scenario involves a manufacturer reformulating its product line away from standard petroleum distillate to a low aromatic white spirit. This requires significant R&D investment in processes like hydrodesulfurization and solvent extraction to produce dearomatized solvent options, such as type 3 hydrogenated spirits, which offer lower toxicity.

- This strategic pivot aims to meet stricter regulatory compliance for VOCs while maintaining the high solvency power and controlled evaporation rate that industrial customers depend on. The success of this transition hinges on balancing cost, performance, and sustainability, with a focus on developing eco-friendly solvent alternatives and bio-based solvent technology.

- The market's future direction will be defined by the ability of producers to innovate within these constraints, offering products that are both effective and compliant.

What will be the Size of the White Spirits Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the White Spirits Market Segmented?

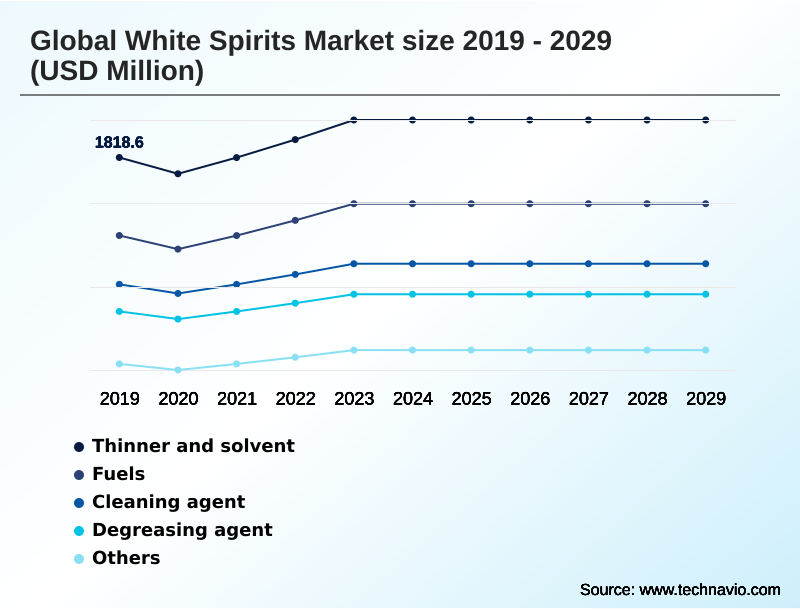

The white spirits industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Thinner and solvent

- Fuels

- Cleaning agent

- Degreasing agent

- Others

- Grade type

- Regular flash

- Low flash

- High flash

- Product type

- Type 1

- Type 2

- Type 3

- Type 0

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Application Insights

The thinner and solvent segment is estimated to witness significant growth during the forecast period.

The thinner and solvent segment is the principal application, driven by its use in adjusting the viscosity of oil-based paints and coatings.

A critical dynamic is the market's evolution from traditional options like stoddard solvent toward low aromatic white spirit alternatives, a move accelerated by stringent regulations.

This is evident in architectural coatings thinner formulations, where manufacturers are compelled to reduce volatile organic compounds. Formulations using type 1 hydrodesulfurized solvents are being refined for compliance while retaining high solvency power.

The effectiveness of a paint thinner formulation is judged by its evaporation rate, with new variants improving coating uniformity by over 15%.

This involves careful selection of a hydrocarbon-based solvent via specialty chemical distribution, ensuring safe solvent handling and adherence to occupational exposure limits for a safer industrial surface cleaning process.

These developments also consider eco-friendly solvent alternatives and the product's flash point determination.

The Thinner and solvent segment was valued at USD 2.01 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 35.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How White Spirits Market Demand is Rising in APAC Get Free Sample

The geographic landscape is diverse. APAC leads with over 35% of incremental growth, driven by construction industry chemicals demand. Here, type 0 straight-run products and those with a low flash point remain common.

In contrast, North America and Europe prioritize low VOC coating formulation and high-purity aliphatic solvent products for uses like precision cleaning solvent applications.

This has spurred demand for spirits with a high flash point for safer industrial use, such as in metalworking fluid and rubber industry solvent applications. European regulations have driven a 50% increase in compliant coatings adoption.

Demand is also shaped by specialized regional industries, including oil and gas exploration chemicals in the Middle East, bitumen extraction in Canada, and use as a pharmaceutical extraction solvent.

This varied demand influences the use of different solvent grades, including those produced via solvent extraction.

Market Dynamics

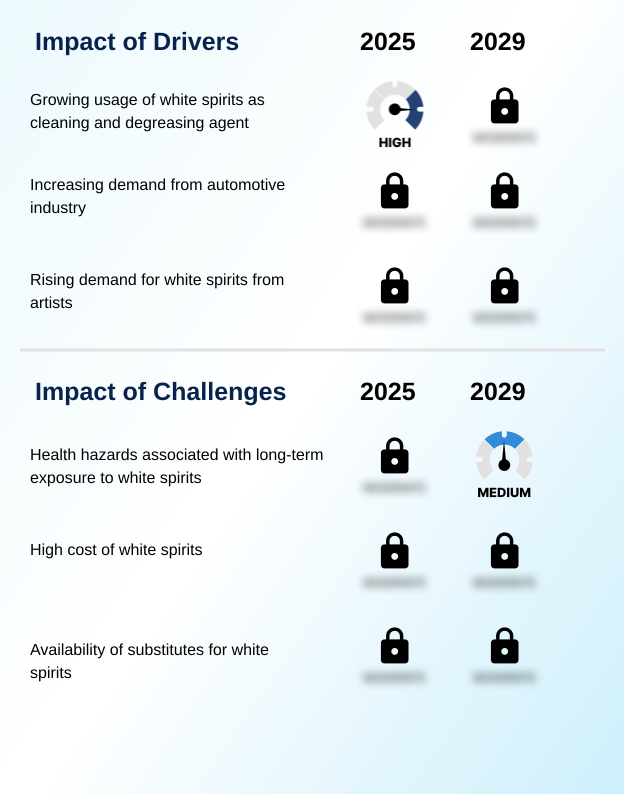

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the white spirits market requires a deep dive into its technical nuances. A common query is about low aromatic content white spirit uses, which are primarily in applications demanding lower toxicity and odor, such as indoor coatings. The hydrodesulfurization process for solvents is a key technology for achieving this, reducing impurities and aromatic compounds.

- This leads to questions about Type 3 hydrogenated solvent properties, which include high purity and minimal environmental impact, making them ideal for sensitive applications. In contrast, the flash point of regular mineral spirits makes it a versatile choice for general workshop use. Navigating VOC limits in industrial coatings is a major compliance challenge, driving the market toward cleaner alternatives.

- This also brings up the classic question of stoddard solvent vs mineral turpentine, where differences in distillation range and composition dictate their best use. For operational safety, protocols for the safe handling of aliphatic hydrocarbons are paramount, as is understanding the evaporation rate of paint thinners for achieving a desired finish.

- The technical side of production involves processes like solvent extraction in petroleum refining, which separates aromatic from aliphatic components. The resulting dearomatized solvents for cleaning offer superior safety profiles. For heavy-duty tasks, a high flash point degreasing agent is preferred. The versatility extends to white spirit in adhesive formulation and as a key component in automotive paint thinner specifications.

- Stakeholders are increasingly exploring alternatives to petroleum distillate solvents and biodegradable substitutes for mineral spirits.

- The market also includes niche applications for Type 0 straight-run naphtha applications, making it crucial to understand the right product for specific tasks, from enhancing solvency power for industrial resins to choosing solvents for wood preservatives and adhering to regulatory standards for dry cleaning fluids, all while considering the environmental impact of hydrocarbon solvents.

- The complexity is evident, as solvent choice impacts performance more than cost-effectiveness in many scenarios. For instance, using the correct solvent can improve process efficiency by over 20% compared to a cheaper, less suitable alternative.

What are the key market drivers leading to the rise in the adoption of White Spirits Industry?

- The market is primarily driven by the expanding use of white spirits as an effective and affordable cleaning and degreasing agent in various industrial and household applications.

- A primary market driver is its widespread use as a cleaning and degreasing agent.

- The solvency power of aliphatic hydrocarbons makes them highly effective for industrial surface cleaning, with studies showing they can reduce cleaning times by up to 25% compared to some water-based degreaser alternatives.

- This efficiency is critical in the automotive industry for automotive refinishing solvent applications and general maintenance.

- The demand is also bolstered by its utility as a wood preservative and in dry cleaning fluid formulations, where a low flash point is often required.

- The versatility of petroleum distillate products, including their role as a chemical synthesis intermediate, supports steady demand.

- Increased adoption of odorless mineral spirits for indoor applications has broadened their appeal, part of a larger push for bio-based solvent technology and creating a non-toxic degreaser.

What are the market trends shaping the White Spirits Industry?

- A key market trend is the rising demand from the global construction industry. This is driven by increased use in paints and coatings for new infrastructure and residential projects.

- A significant trend is the rising demand from the construction industry, fueling consumption for protective coating application and as a paint viscosity modifier. With infrastructure investments growing over 10% in key emerging markets, the need for these solvents is escalating.

- This is complemented by its role as an industrial degreasing agent, where formulations with a regular flash point, like mineral turpentine, are preferred. The demand for a fast-drying solvent is another key factor. Furthermore, there is a rising demand for type 2 solvent-extracted products in specialized uses like adhesive formulation.

- This trend is pushing innovation towards biodegradable hydrocarbon solvent options, with new applications emerging in bitumen-based waterproofing and as an agrochemical solvent carrier, expanding beyond traditional uses as a printing ink solvent. New formulations reduce drying time by 15%.

What challenges does the White Spirits Industry face during its growth?

- A significant challenge restraining market growth is the documented health hazards associated with long-term exposure to white spirits, leading to stricter safety regulations and handling protocols.

- Significant market challenges stem from the health risks associated with the aromatic hydrocarbon content in many formulations, necessitating strict regulatory compliance for VOCs. The availability of substitutes, such as water-based solvent alternatives, presents a persistent challenge, capturing up to 30% of the market share in certain categories like textile cleaning agent products.

- The cost and complexity of implementing solvent recovery systems can also be a barrier. Moreover, the process of solvent extraction and subsequent treatment to produce dearomatized solvent types like type 3 hydrogenated spirits adds to production costs, which can be 15-20% higher than for untreated variants. The industry also faces scrutiny over the environmental impact of petroleum refining byproduct streams.

- These challenges are driving research into bio-based solvent development and advanced hydrodesulfurization techniques to produce cleaner products for uses like pesticide formulation and as an aerosol propellant.

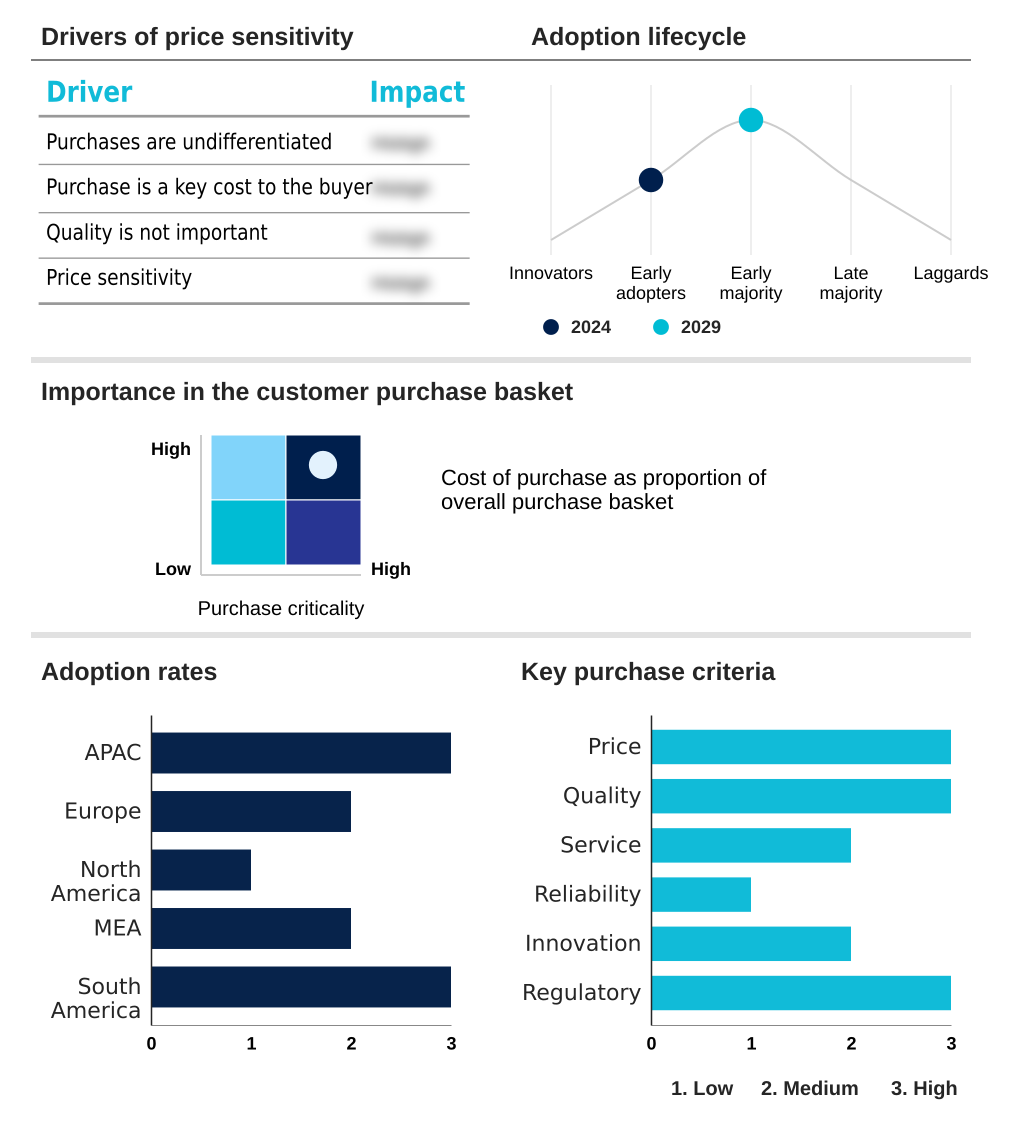

Exclusive Technavio Analysis on Customer Landscape

The white spirits market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the white spirits market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of White Spirits Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, white spirits market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

2M Holdings Ltd. - Vendors focus on providing high-purity hydrocarbon solvents, including refined white spirits, engineered for diverse industrial processes demanding specific performance characteristics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2M Holdings Ltd.

- Al Oga Factory

- Al Sanea Chemical Products

- Bharat Petroleum Corp. Ltd.

- Compania Espanola de Petroleos SA

- DHC Solvent Chemie GmbH

- Exxon Mobil Corp.

- G.S.B Chemical Co. Pty. Ltd.

- Haltermann Carless

- HCS Group GmbH

- Indian Oil Corp. Ltd.

- KH Chemicals BV

- Neste Corp.

- Pure Chemicals Co. Ltd

- Rebain International

- Sel Chemie BV

- Shanghai Chemex Group Ltd.

- Shell plc

- TotalEnergies SE

- Vizag Chemical International

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in White spirits market

- In August 2024, HCS Group GmbH announced its proactive compliance plan in anticipation of new proposed regulations for stricter VOC content limits in industrial maintenance coatings.

- In January 2025, TotalEnergies SE launched a pilot program with industrial partners to test advanced solvent recovery and recycling techniques, aiming to create a circular economy model for hydrocarbon-based solvents.

- In March 2025, Shell plc announced a significant expansion of its eco-friendly solvent portfolio, introducing a new line of biodegradable, low-aromatic white spirits to meet stringent regulatory frameworks.

- In April 2025, in response to China's newly unveiled draft environmental code, Shanghai Chemex Group Ltd. announced a strategic shift to prioritize green and low-carbon production technologies for its solvent offerings.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled White Spirits Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.7% |

| Market growth 2025-2029 | USD 2291.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, US, Canada, Mexico, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The white spirits market is evolving beyond its identity as a simple petroleum distillate. Boardroom decisions now center on a strategic pivot toward sustainable chemistry, driven by the need to manage volatile organic compounds and aromatic hydrocarbon content.

- This has intensified focus on refining processes like hydrodesulfurization and solvent extraction, creating a clear distinction between a basic type 0 straight-run product and a highly refined type 3 hydrogenated or dearomatized solvent. Formulations featuring aliphatic hydrocarbons now achieve up to a 40% VOC reduction while matching the solvency power of traditional stoddard solvent.

- Product specification is critical, defined by characteristics like evaporation rate and whether a regular flash point, low flash point, or high flash point is required.

- This impacts its use across a vast range of applications: from a paint thinner formulation and industrial degreasing agent to more specialized roles as a printing ink solvent, aerosol propellant, wood preservative, dry cleaning fluid, metalworking fluid, rubber industry solvent, pesticide formulation, chemical synthesis intermediate, and in adhesive formulation.

- The nuances between type 1 hydrodesulfurized and type 2 solvent-extracted grades, as well as products like mineral turpentine and naphtha solvent, are crucial for applications ranging from bitumen extraction to household cleaning product lines.

What are the Key Data Covered in this White Spirits Market Research and Growth Report?

-

What is the expected growth of the White Spirits Market between 2025 and 2029?

-

USD 2.29 billion, at a CAGR of 5.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Thinner and solvent, Fuels, Cleaning agent, Degreasing agent, Others), Grade Type (Regular flash, Low flash, High flash), Product Type (Type 1, Type 2, Type 3, Type 0) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing usage of white spirits as cleaning and degreasing agent, Health hazards associated with long-term exposure to white spirits

-

-

Who are the major players in the White Spirits Market?

-

2M Holdings Ltd., Al Oga Factory, Al Sanea Chemical Products, Bharat Petroleum Corp. Ltd., Compania Espanola de Petroleos SA, DHC Solvent Chemie GmbH, Exxon Mobil Corp., G.S.B Chemical Co. Pty. Ltd., Haltermann Carless, HCS Group GmbH, Indian Oil Corp. Ltd., KH Chemicals BV, Neste Corp., Pure Chemicals Co. Ltd, Rebain International, Sel Chemie BV, Shanghai Chemex Group Ltd., Shell plc, TotalEnergies SE and Vizag Chemical International

-

Market Research Insights

- The market is shaped by the dual pressures of industrial performance and environmental sustainability. While demand for effective resin and polymer solvent solutions remains strong, there is a notable shift toward a circular economy for solvents, with adoption of recycling technologies increasing by over 15% in regulated markets.

- The development of products that serve as both a drilling fluid component and a cleaner solvent represents a key innovation area. Compared to five years ago, formulations with lower VOC content now account for a 30% greater share of the specialty chemicals market, reflecting successful alignment with compliance goals without compromising performance.

We can help! Our analysts can customize this white spirits market research report to meet your requirements.

RIA -

RIA -