Wind Turbine Generator Market Size 2024-2028

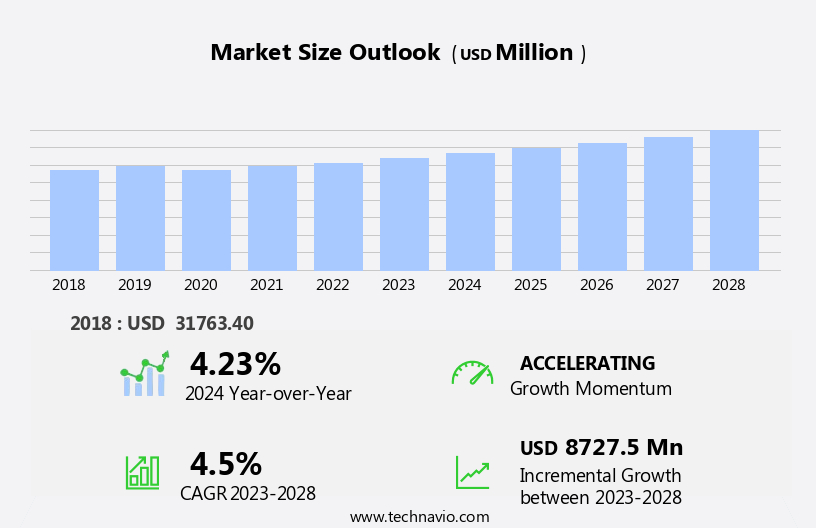

The wind turbine generator market size is forecast to increase by USD 8.73 billion, at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing research and development in direct-drive generators for wind turbines. This technological advancement offers improved efficiency and reliability, making wind energy a more competitive alternative to traditional fossil fuels. However, the market faces challenges as well. The competition from fossil fuels, which continue to dominate the energy sector, poses a significant obstacle. Despite this, opportunities exist for companies to capitalize on the growing demand for renewable energy and the advancements in wind turbine technology.

- To succeed, businesses must focus on enhancing efficiency, reducing costs, and addressing the intermittency challenges associated with wind energy. By staying abreast of market trends and navigating these challenges effectively, companies can position themselves to thrive in the evolving wind energy landscape.

What will be the Size of the Wind Turbine Generator Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and shifting policy landscapes. Offshore wind farms, with their vast potential for energy production, are a significant focus, requiring specialized blade inspection techniques and power conversion systems adhering to IEC standards. Blade materials, including composite materials and carbon fiber, are continually improving to enhance turbine efficiency and reduce operational costs. Wind energy policy and noise reduction measures are shaping market dynamics, with feed-in tariffs and wind resource assessment playing crucial roles in utility-scale wind farm development. Bird strike mitigation and voltage regulation are essential considerations for turbine servicing, ensuring the continued safety and efficiency of wind power generation.

Turbine efficiency is a critical factor, with direct drive generators, pitch control, and variable speed generators all contributing to optimized energy yield. Data acquisition, wind power forecasting, wind turbine simulation, and maintenance schedules are essential components of wind turbine operations. Distributed generation and grid connection are increasingly important, with generator capacity and grid integration key concerns. Foundation design, structural integrity, and safety standards are essential for both onshore and offshore wind farms. Capacity factor, power electronics, blade optimization, environmental impact, wind speed measurement, and grid integration are all ongoing areas of research and development.

How is this Wind Turbine Generator Industry segmented?

The wind turbine generator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Onshore

- Offshore

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- India

- Rest of World (ROW)

- North America

.

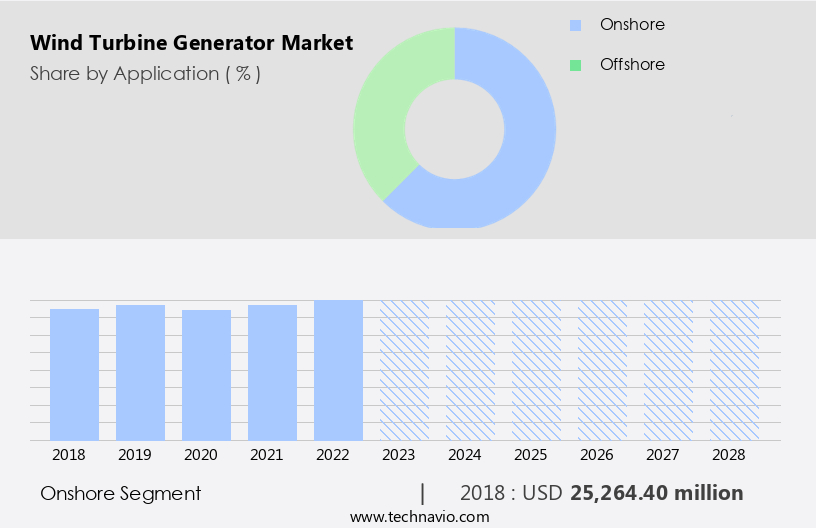

By Application Insights

The onshore segment is estimated to witness significant growth during the forecast period.

The market encompasses various segments, including onshore and offshore wind farms. The onshore segment currently holds a significant market share due to its lower capital requirements compared to offshore wind farms. This segment's growth is fueled by the declining cost of power generation worldwide. For instance, onshore wind auctions in India in February 2020 resulted in winning bids as low as USD0.038/kilowatt-hour (KWh). Technological innovations are a key driver for the onshore wind sector, with advancements in power electronics leading to increased reliability and reduced prices. Efficient wind farm planning and management, along with the adoption of sophisticated power conversion systems, have contributed to these improvements.

Offshore wind farms present unique challenges, necessitating specialized blade inspection, wind resource assessment, foundation design, and safety standards. IEC standards ensure uniformity and safety in the industry, while blade optimization, pitch control, and variable speed generators enhance turbine efficiency. Noise reduction, bird strike mitigation, and voltage regulation are essential considerations for wind turbine operations. Composite materials, including carbon fiber, are increasingly used in turbine blades for their strength and durability. Wind turbine simulations and maintenance schedules help optimize energy yield and minimize operational costs. Utility-scale wind farms and distributed generation are integral to the market's growth, with grid connection and generator capacity key factors.

Synchronous and asynchronous generators, along with reactive power compensation, ensure grid integration. Renewable energy credits further incentivize wind power adoption. Environmental impact assessments, wind speed measurement, and grid integration are crucial for wind power forecasting. Safety standards, capacity factor, and power electronics are essential for optimizing wind turbine performance. The market's future trends include blade design, fatigue analysis, and yaw system improvements.

The Onshore segment was valued at USD 25.26 billion in 2018 and showed a gradual increase during the forecast period.

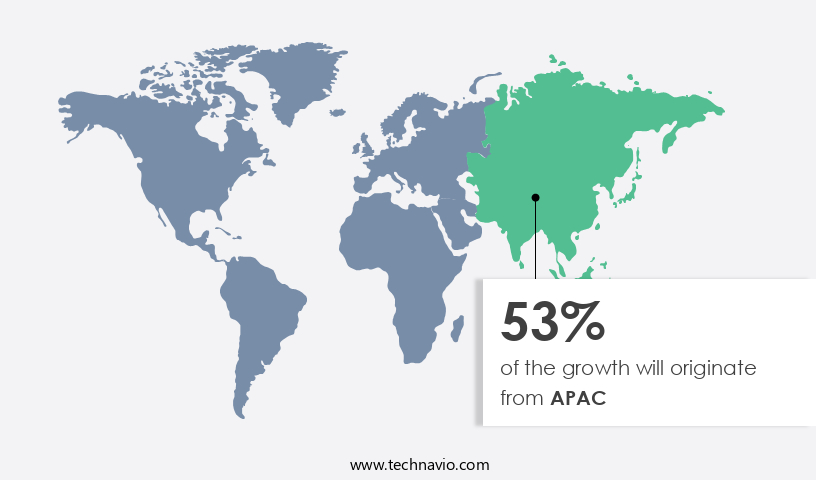

Regional Analysis

APAC is estimated to contribute 53% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the region is experiencing significant growth due to the increasing emphasis on renewable energy sources, particularly wind power. Notably, China and India are leading the way with the majority of installations. In India, the government aims to reach a wind power capacity of 60GW by 2024, focusing primarily on onshore wind farms. However, the country is also exploring the potential of offshore wind farms, which could further boost market growth. IEC standards ensure uniformity in turbine design and operation, while blade inspection and maintenance are crucial for maintaining turbine efficiency. Composite materials, including carbon fiber, are increasingly used for blade production due to their strength and durability.

Power conversion systems convert wind energy into usable electricity, and variable speed generators offer improved efficiency and power output. Wind resource assessment is essential for site selection, and turbine control systems optimize energy yield through pitch control and yaw systems. Operational costs, including turbine servicing and voltage regulation, are significant considerations. Grid connection and generator capacity are essential for utility-scale wind farms, while distributed generation allows for smaller-scale installations. Environmental impact, including bird strike mitigation and noise reduction, is a critical concern. Capacity factor, power electronics, and blade optimization are essential factors in maximizing energy output. Wind speed measurement and grid integration are crucial for ensuring stable power output.

Safety standards and foundation design are essential for structural integrity, and synchronous and asynchronous generators serve different purposes in wind power generation. The market's evolution includes advancements in wind power forecasting, simulation, and reactive power compensation. The focus on renewable energy credits and feed-in tariffs continues to drive market growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Wind Turbine Generator Industry?

- The significant increase in wind energy consumption serves as the primary market driver.

- The market is experiencing significant growth due to the worldwide shift towards renewable energy sources and the depletion of conventional energy resources. Wind power, as one of the most abundant and efficient renewable energy sources, is at the forefront of this transition. According to the Global Wind Energy Council (GWEC), China led the way in installed wind power capacity in 2021, adding 26,798 MW. This trend, along with increasing awareness of wind energy's benefits, is driving demand for wind turbine generators. Key market dynamics include advancements in power electronics, blade optimization, and environmental impact assessments. Wind speed measurement, grid integration, and power output are critical factors influencing market growth.

- Asynchronous generators, reactive power compensation, yaw systems, fatigue analysis, and other technologies are essential for enhancing wind turbine generator performance and efficiency. Power electronics play a crucial role in optimizing wind turbine generator performance by controlling the conversion of electrical power between the rotor and the grid. Blade optimization is another essential aspect, with researchers focusing on improving blade design and materials to increase capacity factor and reduce environmental impact. Wind speed measurement is critical for optimizing power output and ensuring grid stability. Grid integration is a significant challenge for the wind energy sector, necessitating advanced power electronics and control systems to ensure stable power delivery to the grid.

- Reactive power compensation is essential for maintaining grid stability, and yaw systems help optimize wind turbine orientation for maximum energy production. Fatigue analysis is crucial for assessing the structural integrity of wind turbine components, ensuring long-term reliability and reducing maintenance costs. In conclusion, the market is poised for continued growth due to increasing demand for renewable energy sources and technological advancements in power electronics, blade optimization, wind speed measurement, grid integration, and other areas. These developments are crucial for enhancing wind turbine generator performance, efficiency, and reliability.

What are the market trends shaping the Wind Turbine Generator Industry?

- Direct-drive generators for wind turbines are experiencing significant growth in the R&D sector. This trend reflects a shift towards more efficient and streamlined technology in the wind energy industry.

- Wind turbine generators have historically utilized gearboxes to increase the rotational speed from the typical 14 rpm in onshore wind turbines to the required 560-1,500 rpm for efficient power generation. However, the wind energy industry is exploring direct-drive generators, which operate without gearboxes. This technology offers advantages such as a simplified design, as the generator and rotor rotate as an integrated unit, eliminating the need for a gearbox and reducing the number of moving parts.

- Consequently, direct-drive wind turbines experience less wear and tear, leading to enhanced reliability and lower maintenance costs. The shift towards direct-drive generators signifies an evolution in wind turbine technology, promising increased efficiency and cost savings for wind energy producers.

What challenges does the Wind Turbine Generator Industry face during its growth?

- The growth of the industry faces significant challenges due to intense competition from fossil fuels.

- Wind power, a vital component of the renewable energy sector, accounted for approximately 7% of the global power generation mix in 2021, with fossil fuels dominating at around 61%. Despite the consistent growth in wind energy, its share remains relatively low compared to the massive electricity production from fossil fuels. In countries rich in coal reserves, governments often prefer maintaining the status quo due to the high cost of transitioning to wind power. However, many developing nations aspire to expand their wind power generation capacity. Yet, they face challenges due to insufficient investments and unstable energy policies.

- The absence of competition in these markets drives up the cost of wind power. Key aspects driving the market include advancements in blade inspection, power conversion systems, and turbine efficiency. IEC standards play a crucial role in ensuring uniformity and safety in the wind energy industry. Additionally, wind resource assessment, noise reduction, voltage regulation, bird strike mitigation, and turbine servicing are essential considerations. Governments worldwide are implementing policies such as feed-in tariffs to encourage wind power adoption and incentivize investments. These initiatives aim to reduce greenhouse gas emissions and promote energy independence. Despite these efforts, the wind energy sector continues to face challenges, including the intermittency of wind and the high upfront costs.

- In conclusion, the market is poised for growth, driven by technological advancements and supportive government policies. Addressing the challenges of intermittency and high costs will be crucial for the sector's continued expansion.

Exclusive Customer Landscape

The wind turbine generator market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wind turbine generator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, wind turbine generator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB - The company specializes in wind energy solutions, providing a range of wind turbine generators.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB

- Alxion

- AVANTIS Energy Group

- Bergey Wind Power Co.

- Bora Energy

- Doosan Corp.

- Emergya Wind Technologies BV

- ENERCON GmbH

- Equinor ASA

- General Electric Co.

- Hitachi Ltd.

- Nordex SE

- Principle Power Inc.

- ReGen Powertech Pvt. Ltd.

- Sany Group

- Siemens Gamesa Renewable Energy SA

- Sinovel Wind Group Co. Ltd.

- Suzlon Energy Ltd.

- Vestas Wind Systems AS

- Xinjiang Goldwind Science and Technology Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wind Turbine Generator Market

- In March 2024, Vestas Wind Systems, a leading wind turbine manufacturer, introduced the V21-3.0 MW wind turbine, marking a significant leap in generating capacity for a single wind turbine (Vestas press release). This new turbine model is expected to contribute to the increasing demand for larger, more efficient wind energy solutions.

- In August 2024, Siemens Gamesa Renewable Energy and Enel Green Power announced a strategic partnership to collaborate on the development, construction, and operation of wind farms in Europe and Latin America (Enel Green Power press release). This collaboration is expected to strengthen both companies' positions in the global wind energy market.

- In January 2025, Orsted, the world's largest renewable energy company, raised â¬4.5 billion in a bond issuance to fund its renewable energy projects, including offshore wind farms (Orsted press release). This substantial investment underscores the growing financial commitment to renewable energy, particularly wind power.

- In March 2025, the European Union approved the State Aid Guidelines on the Modernization of the EU's Renewable Energy Support Regime (European Commission press release). This policy change aims to simplify and streamline the support schemes for renewable energy, making it more attractive for investors and accelerating the transition to renewable energy sources.

Research Analyst Overview

- The market is experiencing significant advancements, driven by the need for carbon footprint reduction and climate change mitigation. One trend shaping the industry is the acceptance of floating wind turbines, which expand the reach of wind energy into deeper waters. Computational fluid dynamics and finite element analysis are crucial in optimizing blade aerodynamics and tower stability. Permitting processes and grid synchronization remain key challenges, requiring careful planning in wind farm development. Nacelle cooling and generator efficiency improvements enhance operational performance, while torque control ensures smooth power output. Wind energy economics are evolving, with electrical transmission and wind energy storage playing essential roles in grid integration.

- Foundation engineering, environmental monitoring, and battery energy storage are critical aspects of minimizing environmental impact and ensuring grid reliability. Gearbox lubrication and blade recycling contribute to life cycle assessment and cost savings. Wind turbine acoustics and power quality are essential considerations for public acceptance, with financial modeling and land acquisition essential for project viability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wind Turbine Generator Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

144 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 8727.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

China, US, Germany, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Wind Turbine Generator Market Research and Growth Report?

- CAGR of the Wind Turbine Generator industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the wind turbine generator market growth of industry companies

We can help! Our analysts can customize this wind turbine generator market research report to meet your requirements.

RIA -

RIA -