Wooden Floor Market Size 2024-2028

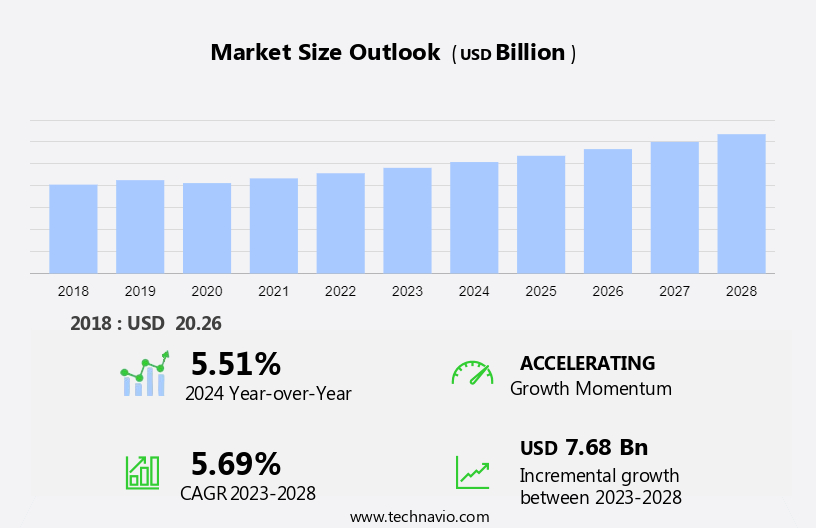

The wooden floor market size is forecast to increase by USD 7.68 billion at a CAGR of 5.69% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing number of construction and real estate projects globally. This trend is driven by the rising demand for aesthetically pleasing and durable flooring solutions. Furthermore, the adoption of advanced technologies such as augmented reality (AR) and virtual reality (VR) is revolutionizing the way consumers purchase wooden flooring products online. However, the market faces challenges due to the volatility in prices of raw materials, particularly wood and other essential components. This can impact the profitability of manufacturers and retailers, requiring them to carefully manage their supply chains and pricing strategies. To stay competitive, market participants must focus on innovation, sustainability, and cost efficiency. Overall, the market is poised for steady growth, driven by consumer preferences and technological advancements.

What will be the Size of the Wooden Floor Market During the Forecast Period?

- The market encompasses a range of hard flooring options, including solid wood, engineered wood, laminate, vinyl flooring, and ceramic tile flooring. These timber products, which include floorboards, flooring, and timber products, continue to hold a significant appeal in interior design due to their timeless and visual appeal. Solid wood and engineered wood flooring, in particular, are favored for their natural beauty and durability.

- Furthermore, wide plank flooring and hardwood flooring are popular choices for those seeking a luxurious and authentic look. However, the production of wooden floors can raise concerns regarding deforestation and associated greenhouse gas emissions. The market is experiencing trends towards the use of sustainable raw materials and manufacturing processes to mitigate these issues. Overall, the market remains a dynamic and evolving sector In the building industry.

How is this Wooden Floor Industry segmented and which is the largest segment?

The wooden floor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Engineered wood flooring

- Solid wood flooring

- End-user

- Residential

- Non-residential

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- Middle East and Africa

- South America

- North America

By Type Insights

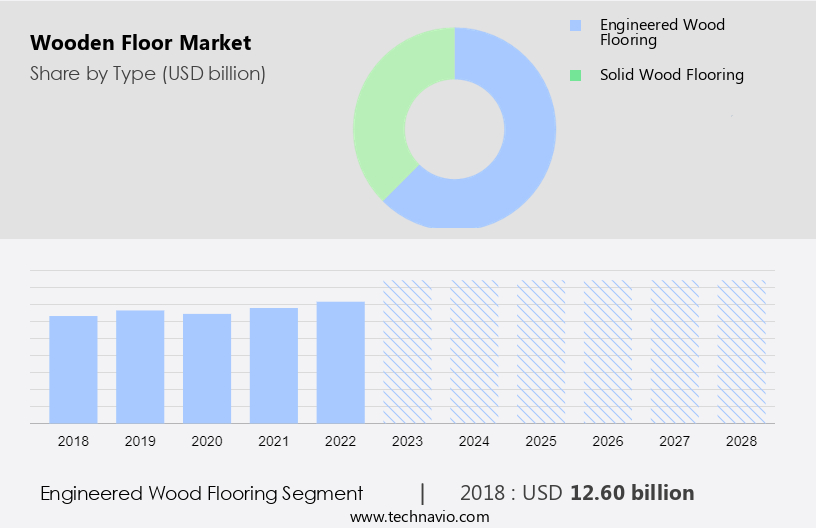

- The engineered wood flooring segment is estimated to witness significant growth during the forecast period.

Solid wood flooring constitutes floorboards crafted from a single, unadulterated piece of natural timber. Renowned for its enduring quality, visual appeal, and longevity, solid wood floors are a popular choice for both residential and commercial applications. The increasing preference for authentic and eco-friendly materials in interior design and construction sectors fuels the demand for solid wood flooring. Consumers are increasingly attracted to the timeless beauty and sustainability of solid wood floors, as they are derived from renewable timber resources and generate minimal environmental impact compared to synthetic flooring alternatives, such as laminate, vinyl, or ceramic tile flooring.

Furthermore, engineered wood flooring, another wood flooring option, is also gaining traction due to its cost-effectiveness and structural stability. Solid wood, engineered wood, and other timber products continue to be integral components of flooring materials in buildings, offering natural textures and a sense of luxury. Sustainable sourcing practices are essential In the production of solid wood flooring, ensuring a responsible approach to resource management and a reduced carbon footprint.

Get a glance at the Wooden Floor Industry report of share of various segments Request Free Sample

The engineered wood flooring segment was valued at USD 12.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

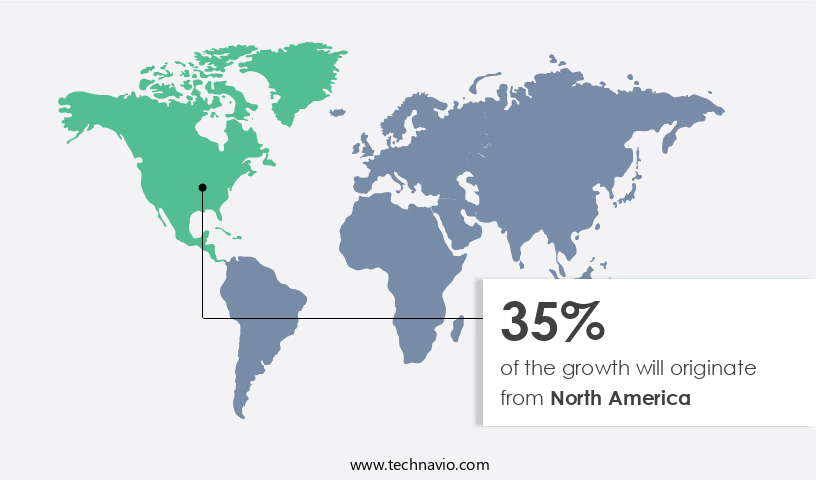

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market experiences significant growth due to the thriving construction industry. With over 919,000 ongoing projects In the US as of Q1 2023, the industry contributes substantially to the economy, employing approximately 8.0 million people and generating nearly USD2.1 trillion in infrastructure projects annually. This sector's revival post-recession drives the demand for various hard flooring options, including solid wood, engineered wood, laminate, vinyl, and ceramic tile flooring.

Furthermore, these timeless and visually appealing flooring materials offer natural textures from raw materials like oak, maple, and cherry. Sustainable sourcing practices are increasingly important In the market, with a focus on reducing deforestation and greenhouse gas emissions. Flooring materials such as hardwood, engineered wood, laminated wood, luxury vinyl tiles, pre-finished hardwood floors, and unfinished hardwood floors cater to diverse interior needs in buildings. Regular cleaning and wear and tear are natural aspects of these flooring types, making them suitable for high foot traffic areas.

Market Dynamics

Our wooden floor market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Wooden Floor Industry?

The rising number of construction and real estate projects worldwide is the key driver of the market.

- The market In the US and Canada is experiencing significant growth due to increasing investments in commercial real estate developments, such as offices and retail spaces, which are primary consumers of wooden floors. The construction sector In the US is expanding rapidly, with numerous projects underway, including the I-4 Ultimate project in Florida, Central 70 in Colorado, SH 99 Grand Parkway in Houston, and DFW Connector in Texas. These projects, among others, are expected to drive the demand for various wooden flooring options, including solid wood, engineered wood, laminate, vinyl, ceramic tile, and wide plank flooring, during the forecast period.

- Furthermore, sustainable sourcing practices are increasingly being adopted by manufacturers to mitigate deforestation and reduce the carbon footprint of wooden flooring. Homeowners and businesses value the timeless appeal and visual appeal of wooden floors, making them a preferred choice for interiors. Flooring materials, such as hardwood, engineered wood, laminated wood, and luxury vinyl tiles, offer natural textures, including oak, maple, and cherry, that add to the appeal. Regular cleaning and maintenance are essential to ensure the longevity of wooden floors, especially in high foot traffic areas, where wear and tear can occur. The market for wooden floors is expected to continue growing due to the increasing demand for hard flooring options that offer durability and aesthetic value.

What are the market trends shaping the Wooden Floor Industry?

The growing adoption of AR and VR technology to enhance online purchasing of flooring products is the upcoming market trend.

- The market encompasses various hard flooring options, including solid wood flooring, engineered wood flooring, laminate flooring, vinyl flooring, ceramic tile flooring, and more. These timeless and visually appealing flooring solutions are derived from raw materials, such as Oak, Maple, Cherry, and other natural textures. Sustainable sourcing practices are increasingly prioritized to minimize deforestation and reduce the carbon footprint of these timber products. Hardwood and engineered wood flooring are popular choices due to their durability and resistance to wear and tear, making them suitable for high foot traffic areas. Pre-finished hardwood floors and unfinished hardwood flooring offer flexibility in terms of customization and installation.

- Furthermore, laminated wood and luxury vinyl tiles are alternative options that mimic the look and feel of wood flooring without the same environmental impact. These flooring materials contribute to reducing greenhouse gas emissions and maintaining the aesthetic appeal of interiors. Cleaning and maintenance are essential aspects of maintaining the longevity and beauty of wooden flooring. Proper care and upkeep ensure these flooring solutions continue to add value to buildings and enhance their overall appeal. AR and VR technology play a significant role In the selection process, allowing potential buyers to visualize and experience different wooden flooring options In their spaces before making a purchase decision. These innovative tools provide a more accurate representation of the flooring's scale, color schemes, and aesthetic compatibility within the intended space.

What challenges does the Wooden Floor Industry face during its growth?

Volatility in prices of raw materials for wooden flooring products is a key challenge affecting the industry growth.

- The market relies heavily on raw materials such as timber for manufacturing various types of wooden flooring products, including solid wood, engineered wood, laminate, vinyl, and ceramic tile flooring. However, the price of these raw materials can be volatile due to various factors, including changes in supply and demand, regulatory policies, weather conditions, and geopolitical tensions. Fluctuations in raw material prices can significantly impact the production costs for manufacturers of wooden flooring products. When timber prices rise unexpectedly, manufacturers may face higher production expenses, leading to reduced profit margins or increased prices for consumers. On the other hand, during periods of declining raw material prices, manufacturers may struggle to maintain profitability, especially if they are unable to adjust product pricing accordingly.

- Moreover, the use of sustainable sourcing practices is becoming increasingly important In the market as consumers become more environmentally conscious. Natural textures such as oak, maple, and cherry continue to be popular choices for hardwood and engineered wood flooring, adding to the timeless appeal and visual appeal of these products. Hard flooring options, including wooden flooring, are preferred for their durability and ability to withstand high foot traffic and wear and tear. Proper cleaning and maintenance are essential to ensure the longevity of these flooring types. With the wide range of flooring materials available, from pre-finished hardwood floors to unfinished hardwood floors, and laminated wood to luxury vinyl tiles, there is a flooring solution for every interior design need and budget. The market is a significant contributor to the building industry, providing flooring solutions for both residential and commercial buildings. Properly managing the price volatility of raw materials is crucial for manufacturers to maintain profitability and competitiveness In the market.

Exclusive Customer Landscape

The wooden floor market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wooden floor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, wooden floor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Armstrong World Industries Inc.

- Barlinek SA

- Bauwerk Group Schweiz AG

- Beaulieu International Group

- Berkshire Hathaway Inc.

- Boral Ltd.

- Broadsword Timber t as British Hardwoods.

- Daikin Industries Ltd.

- GREENBUILD WOOD INDUSTRY CO. LTD

- IM wooden floor

- Junckers Industrier AS

- Kahrs

- kelaiwood

- Lauzon

- Mannington Mills Inc.

- Mirage

- Mohawk Industries Inc.

- Tarkett

- The Solid Wood Flooring Co

- Three Trees Flooring

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of hard flooring options, including solid wood, engineered wood, laminate, vinyl, and ceramic tile flooring. These timber products, often sourced from raw materials, offer a timeless appeal and visual appeal that is unmatched by other flooring alternatives. Solid wood flooring, crafted from a single piece of wood, is prized for its natural textures and authenticity. Engineered wood flooring, on the other hand, is composed of multiple layers, making it more resilient to wear and tear. Both solid wood and engineered wood flooring are available in wide plank options, adding to their aesthetic value. The demand for sustainable sourcing practices is increasingly influencing the market. Manufacturers are implementing responsible forestry management techniques to minimize deforestation and reduce greenhouse gas emissions. This shift towards eco-friendly production methods aligns with the growing trend of environmentally conscious consumers. Hard flooring, including wood flooring, is a popular choice for commercial and residential buildings due to its durability and low maintenance requirements. Wood flooring materials, such as oak, maple, and cherry, are favored for their natural beauty and ability to withstand high foot traffic.

Furthermore, floorboards, available in both pre-finished and unfinished varieties, offer flexibility in design and installation. Pre-finished hardwood floors provide an instant finished look, while unfinished floors allow for customization during the installation process. Laminated wood and luxury vinyl tiles are alternative flooring options that mimic the look and feel of wood flooring. These products offer affordability and ease of installation, making them suitable for various applications. Cleaning and maintenance are essential aspects of maintaining the longevity and appearance of wooden floors. Regular sweeping, dusting, and mopping are recommended to keep the floors in good condition. Proper care and attention can help mitigate wear and tear, ensuring the floors retaIn their visual appeal.

Thus, the market is driven by the desire for authentic, durable, and visually appealing flooring options. The trend towards sustainable sourcing practices and eco-friendly production methods is shaping the industry, as consumers increasingly prioritize environmentally conscious choices. Wood flooring continues to be a popular choice for both residential and commercial applications, offering a timeless and versatile solution for interiors.

|

Wooden Floor Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.69% |

|

Market growth 2024-2028 |

USD 7.68 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.51 |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Wooden Floor Market Research and Growth Report?

- CAGR of the Wooden Floor industry during the forecast period

- Detailed information on factors that will drive the Wooden Floor market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution to the industry in focus on the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the wooden floor market growth of industry companies

We can help! Our analysts can customize this wooden floor market research report to meet your requirements.

RIA -

RIA -