3D Automated Optical Inspection (AOI) Equipment Market Size 2026-2030

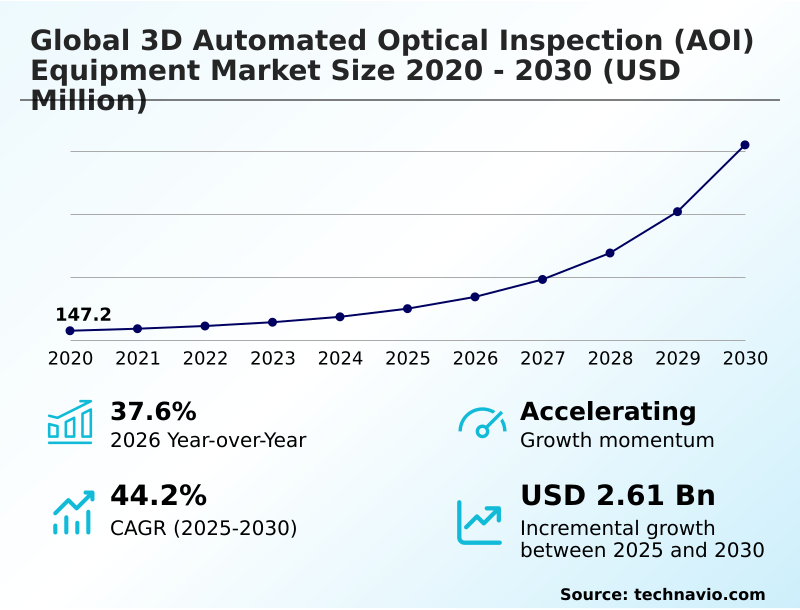

The 3d automated optical inspection (aoi) equipment market size is valued to increase by USD 2.61 billion, at a CAGR of 44.2% from 2025 to 2030. Accelerating complexity in electronic component miniaturization will drive the 3d automated optical inspection (aoi) equipment market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 64.2% growth during the forecast period.

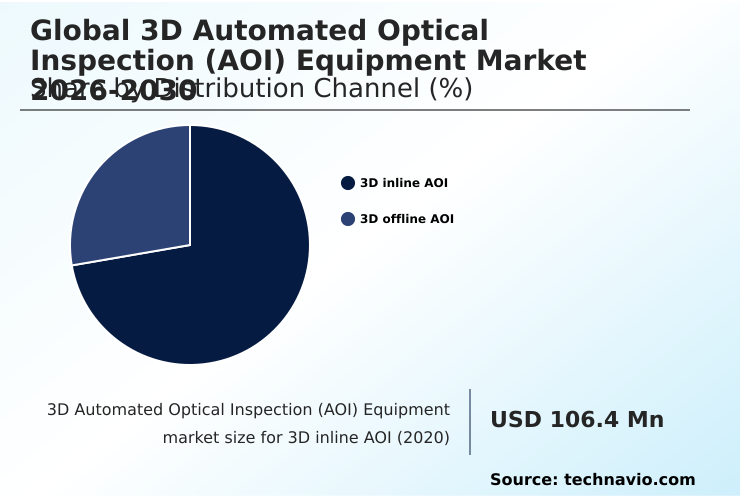

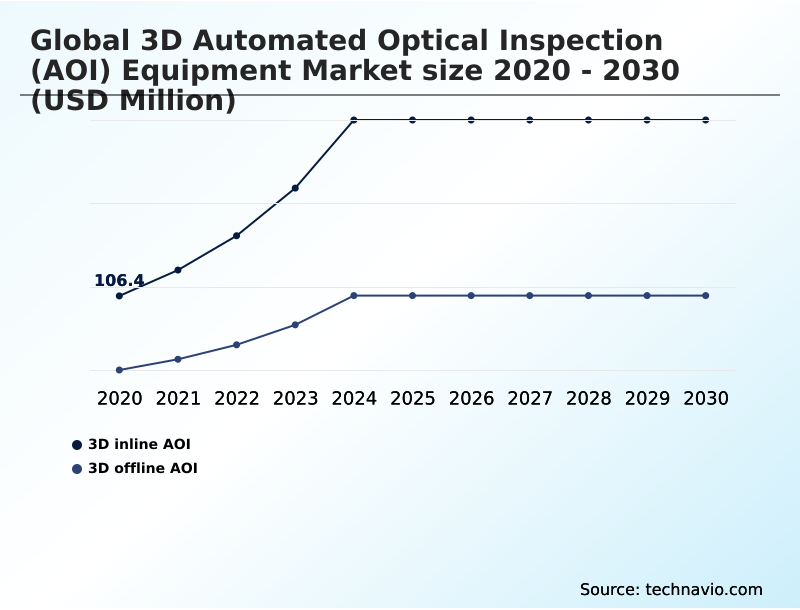

- By Distribution Channel - 3D inline AOI segment was valued at USD 262.2 million in 2024

- By Technology - Confocal inspection segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.96 billion

- Market Future Opportunities: USD 2.61 billion

- CAGR from 2025 to 2030 : 44.2%

Market Summary

- The 3D automated optical inspection (AOI) equipment market is undergoing a significant transformation, driven by the relentless pace of electronic component miniaturization and the widespread adoption of Industry 4.0 principles. Traditional 2D inspection methods are no longer sufficient for verifying the integrity of high density interconnect designs found in advanced electronics.

- This has created a critical need for systems capable of precise volumetric measurement to detect defects like lifted leads and ensure the reliability of micro solder joints. For instance, an automotive electronics manufacturer producing advanced driver assistance systems (ADAS) relies on 3D AOI to achieve zero-defect quality mandates, thereby preventing costly recalls and ensuring passenger safety.

- While the integration of AI-driven autonomous programming promises to enhance defect classification and reduce the reliance on skilled operators, the industry grapples with the high initial capital investment for these systems and the complexities of managing the massive datasets they generate.

- The convergence of 3D AOI with solder paste inspection (SPI) and automated x-ray inspection (AXI) into unified platforms marks a key trend toward achieving a holistic view of the manufacturing process, transforming inspection from a quality gate into a predictive optimization tool.

What will be the Size of the 3D Automated Optical Inspection (AOI) Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the 3D Automated Optical Inspection (AOI) Equipment Market Segmented?

The 3d automated optical inspection (aoi) equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- 3D inline AOI

- 3D offline AOI

- Technology

- Confocal inspection

- Structured light inspection

- Laser inspection

- Multi-directional inspection

- End-user

- Original equipment manufacturers

- Contract manufacturers

- Research and development institutions

- Quality control laboratories

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Distribution Channel Insights

The 3d inline aoi segment is estimated to witness significant growth during the forecast period.

The 3D inline AOI segment is central to modern manufacturing, enabling real-time, high-speed volumetric measurement without interrupting production flow.

These systems are crucial for achieving high first pass yields, particularly in high-volume sectors where firms using this technology report a defect detection improvement of over 98% compared to manual methods.

Integrating directly into the SMT line, they facilitate immediate closed loop process control by providing data for real-time process optimization.

The technology's capability for coplanarity verification and inspection of micro solder joints is indispensable for the assembly of advanced driver assistance systems and wearable medical sensors.

This approach to quality assurance drives significant gains in overall equipment effectiveness by minimizing rework and scrap, ensuring total process transparency within the smart factory ecosystem.

The 3D inline AOI segment was valued at USD 262.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 64.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Automated Optical Inspection (AOI) Equipment Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for over 64% of the market's incremental growth, driven by its massive electronics manufacturing hubs.

In this region, the push toward lights out manufacturing leverages 3D inline AOI and AI-driven autonomous programming to manage high-volume production.

North America and Europe focus on high-value sectors, where IATF 16949 certification is crucial for automotive suppliers using these systems for the inspection of electric vehicle electronics and autonomous driving sensors.

In these markets, advanced systems for non destructive testing and first article inspection are standard.

Firms in these regions achieve a significant reduction in inspection-related labor costs, sometimes by as much as 50%, by adopting automated platforms for high mix low volume production. The expansion into specialized semiconductor wafer inspection further defines regional priorities.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of 3D automated optical inspection (AOI) equipment is reshaping quality assurance across advanced manufacturing. For specialized applications like 3D automated optical inspection for EV power modules, the technology's ability to perform volumetric measurement of solder fillets for automotive electronics is critical for ensuring long-term reliability.

- The integration of AI-driven defect classification in SMT lines is a core component of the role of 3D AOI in Industry 4.0 environments, where systems learn to distinguish true defects from minor process variations. This capability is pivotal for reducing false call rates in 3D AOI systems, which has been a persistent challenge.

- The use of structured light inspection for BGA solder joints and confocal inspection for advanced semiconductor packaging addresses the impact of component miniaturization on 3d aoi adoption. Furthermore, innovations like high speed multi projection moire for reflective surfaces solve inspection challenges with mirror finish dies using 3d aoi.

- The integration of disparate systems is another key area of development, with a focus on integrating 3D AOI with solder paste inspection systems and using IPC CFX for smart factory connectivity with AOI. This creates a closed loop feedback from 3D AOI to pick and place machines, enabling real-time adjustments.

- The adoption of 3d aoi for 01005 and 008004 chip components and 3D metrology for micro bumps and through silicon vias is now standard for firms assembling high performance computing module assembly. Multi-directional inspection to eliminate shadow effects is essential for complex assemblies, as is the inspection of wide bandgap semiconductors like SiC and GaN.

- Even in flexible manufacturing, 3D offline AOI for high mix low volume manufacturing provides a pathway to zero defect manufacturing using 3d optical inspection, with some users reporting double the throughput of older methods. Finally, AI autonomous programming for 3d aoi systems simplifies setup and operation, making advanced inspection more accessible.

What are the key market drivers leading to the rise in the adoption of 3D Automated Optical Inspection (AOI) Equipment Industry?

- The accelerating complexity in electronic component miniaturization is a key driver for the 3D automated optical inspection (AOI) equipment market.

- Market growth is fundamentally driven by the accelerating complexity of electronic assemblies and the stringent quality demands of high-reliability sectors.

- The relentless trend of electronic component miniaturization makes 3D metrology indispensable for verifying the structural integrity of high density interconnects and micro solder joints.

- In the automotive sector, the transition to electric vehicle electronics and advanced driver assistance systems mandates rigorous inspection to IATF 16949 certification standards, with some manufacturers reporting a 99.9% defect capture rate for critical components.

- Furthermore, the proliferation of Industry 4.0 and the smart factory ecosystem requires the closed loop process control that 3D AOI systems provide, feeding real-time data to pick and place machines and solder paste printers to dynamically optimize production and improve overall equipment effectiveness by up to 20%.

What are the market trends shaping the 3D Automated Optical Inspection (AOI) Equipment Industry?

- The integration of AI-driven autonomous programming and defect classification is a transformative market trend. This development automates complex inspection parameter settings and enhances defect classification accuracy.

- Key market trends are centered on intelligent automation and system convergence. The adoption of deep learning algorithms for AI-based defect classification allows systems to reduce false call rates by over 30%, a significant improvement that minimizes manual intervention. This trend toward AI autonomous programming is critical for addressing the complexities of high-mix production environments.

- Concurrently, the market is seeing a convergence of inspection technologies, with multi modal data fusion integrating data from solder paste inspection and automated x ray inspection. This provides a holistic view of the manufacturing process, enabling predictive process optimization.

- The use of the IPC CFX protocol facilitates seamless machine to machine communication, transforming disparate inspection points into a cohesive, data-rich network that enhances process capability index metrics and supports zero defect manufacturing goals.

What challenges does the 3D Automated Optical Inspection (AOI) Equipment Industry face during its growth?

- The high initial capital expenditure and total cost of ownership present a key challenge affecting the growth of the 3D automated optical inspection (AOI) equipment industry.

- Significant challenges constrain market adoption, primarily the high initial capital investment and the complexity of data management. The cost of acquiring systems with high resolution CMOS sensors and advanced digital light projectors is a barrier for smaller enterprises.

- Moreover, managing the high volume of data and the prevalence of false calls creates operational bottlenecks, with some lines experiencing a 10% reduction in throughput due to unnecessary re-inspection. The technical skills gap presents another hurdle, as programming and optimizing these systems for tasks like silicon carbide inspection or gallium nitride inspection require specialized expertise.

- Integrating data across platforms for shadow effect elimination and lifted leads detection remains a complex software challenge, hindering the achievement of a truly unified, multi-vendor inspection ecosystem.

Exclusive Technavio Analysis on Customer Landscape

The 3d automated optical inspection (aoi) equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the 3d automated optical inspection (aoi) equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of 3D Automated Optical Inspection (AOI) Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, 3d automated optical inspection (aoi) equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Shenzhen Zhenhuaxing Intelligent - Delivers true 3D measurement-based inspection technology, focusing on the development and manufacturing of advanced 3D metrology solutions for complete process optimization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Shenzhen Zhenhuaxing Intelligent

- Camtek Ltd.

- GOPEL electronic GmbH

- KLA Corp.

- Koh Young Technology Inc.

- MEK Europe BV

- Mirtec Co. Ltd.

- Mycronic AB

- NANOTRONICS IMAGING INC.

- Nordson Corp.

- OMRON Corp.

- PARMI Co. Ltd.

- Saki Corp.

- Stratus Vision GmbH

- Viscom AG

- Machine Vision Products Inc.

- Visionx Inc.

- ViTrox Corp. Berhad

- Yamaha Motor Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3d automated optical inspection (aoi) equipment market

- In March 2025, Koh Young Technology Inc. launched its advanced AI-powered software suite, designed to reduce 3D AOI programming time and automate defect classification, significantly enhancing efficiency in high-mix manufacturing environments.

- In February 2025, Saki Corp. announced a strategic partnership with a leading industrial robotics firm to integrate its 3D-AOI systems into fully autonomous SMT lines, improving M2M communication for real-time process adjustments and predictive maintenance.

- In November 2024, Viscom AG expanded its North American presence by opening a new technology and training center in California, dedicated to providing enhanced local support for semiconductor and electric vehicle manufacturing clients.

- In September 2024, Nordson Corp. completed the acquisition of a specialized optics technology firm, strengthening its portfolio of high-resolution sensors and advanced digital light projectors for its 3D inspection division.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Automated Optical Inspection (AOI) Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 44.2% |

| Market growth 2026-2030 | USD 2605.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 37.6% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The 3D automated optical inspection (AOI) equipment market is defined by a shift toward data-driven, autonomous quality control. The proliferation of electric vehicle electronics and components for high performance computing necessitates advanced 3D metrology for tasks like solder fillets inspection and coplanarity verification. Key technologies such as structured light inspection, confocal inspection, and multi-directional inspection are fundamental to this evolution.

- The integration of these systems into a smart factory ecosystem enables closed loop process control, where data from 3D inline AOI units feeds back to solder paste printers and pick and place machines, optimizing overall equipment effectiveness. This machine to machine communication is crucial for managing high density interconnect designs and advanced semiconductor packaging.

- A primary trend influencing boardroom budgeting is the adoption of AI driven autonomous programming and deep learning algorithms, which address the skills gap and push toward lights out manufacturing. Firms adopting these AI-enhanced systems have reported a reduction in program creation time by up to 60%.

- The market also encompasses 3D offline AOI for flexible production, solder paste inspection, and automated x ray inspection for comprehensive multi modal data fusion. Challenges remain in managing false call rates and the high cost of high resolution CMOS sensors and digital light projectors.

- The ultimate goal is achieving high first pass yields and ensuring the integrity of heterogenous integration, 2.5d/3d chip stacking, micro solder joints, and through silicon vias.

What are the Key Data Covered in this 3D Automated Optical Inspection (AOI) Equipment Market Research and Growth Report?

-

What is the expected growth of the 3D Automated Optical Inspection (AOI) Equipment Market between 2026 and 2030?

-

USD 2.61 billion, at a CAGR of 44.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (3D inline AOI, and 3D offline AOI), Technology (Confocal inspection, Structured light inspection, Laser inspection, and Multi-directional inspection), End-user (Original equipment manufacturers, Contract manufacturers, Research and development institutions, and Quality control laboratories) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerating complexity in electronic component miniaturization , High initial capital expenditure and total cost of ownership

-

-

Who are the major players in the 3D Automated Optical Inspection (AOI) Equipment Market?

-

Shenzhen Zhenhuaxing Intelligent, Camtek Ltd., GOPEL electronic GmbH, KLA Corp., Koh Young Technology Inc., MEK Europe BV, Mirtec Co. Ltd., Mycronic AB, NANOTRONICS IMAGING INC., Nordson Corp., OMRON Corp., PARMI Co. Ltd., Saki Corp., Stratus Vision GmbH, Viscom AG, Machine Vision Products Inc., Visionx Inc., ViTrox Corp. Berhad and Yamaha Motor Co. Ltd.

-

Market Research Insights

- The market dynamics are increasingly shaped by the need for superior defect detection, where advanced systems demonstrate a 40% reduction in false call rates compared to legacy platforms. The adoption of AI-based defect classification and predictive process optimization enables manufacturers to achieve higher yields, with some reporting a 15% improvement in overall equipment effectiveness.

- The integration of cloud based analytics allows for real time process optimization across global facilities. Technologies enabling sub micron accuracy are critical for advanced packaging metrology and the inspection of wearable medical sensors.

- These sophisticated capabilities are essential for achieving the zero defect manufacturing standards required by sectors utilizing advanced driver assistance systems, pushing the industry toward greater automation and data-driven quality control.

We can help! Our analysts can customize this 3d automated optical inspection (aoi) equipment market research report to meet your requirements.

RIA -

RIA -