Aerospace Insurance Market Size 2025-2029

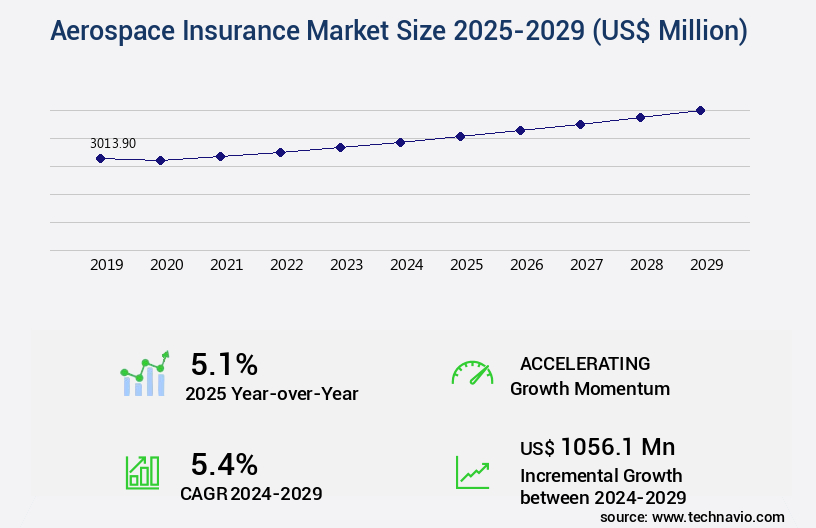

The aerospace insurance market size is valued to increase USD 1.06 billion, at a CAGR of 5.4% from 2024 to 2029. Expansion and construction of new airports will drive the aerospace insurance market.

Major Market Trends & Insights

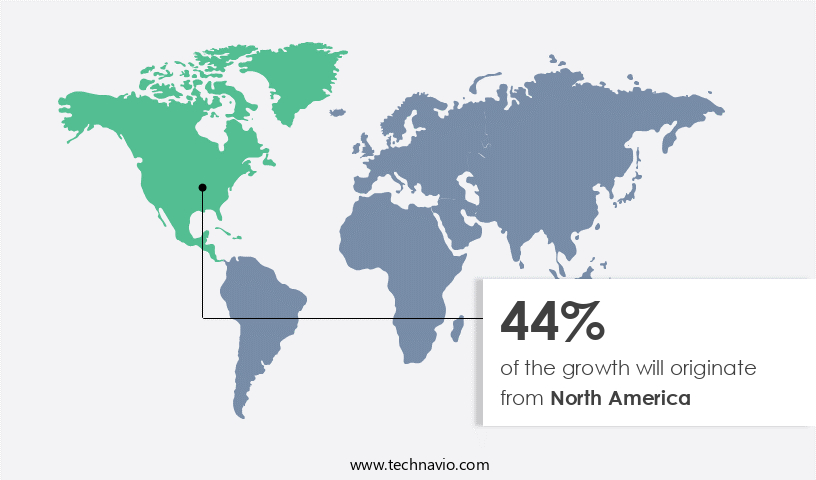

- North America dominated the market and accounted for a 44% growth during the forecast period.

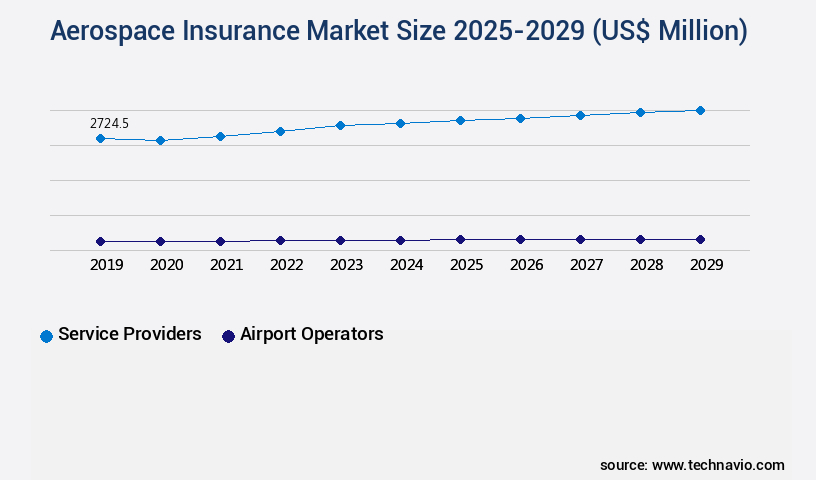

- By End-user - Service providers segment was valued at USD 2.72 billion in 2023

- By Type - In-flight insurance segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 52.44 million

- Market Future Opportunities: USD 1056.10 million

- CAGR from 2024 to 2029 : 5.4%

Market Summary

- The market encompasses a significant and dynamic sector, with global revenues exceeding USD15 billion in 2021. This market's expansion is fueled by the increasing demand for air travel and the proliferation of new technologies in the aviation industry. New aircraft orders, fleet expansion, and maintenance contracts drive the market's growth, while the integration of advanced technologies, such as drones and spacecraft, broadens its scope. Despite these opportunities, the aerospace insurance sector faces challenges, including the growing risk of accidents and the increasing complexity of claims. As the aviation industry evolves, insurers must adapt to new risks and technologies, ensuring their clients are protected while maintaining profitability.

- The market's future direction lies in innovation, with insurers leveraging data analytics, artificial intelligence, and machine learning to assess risks more accurately and efficiently. By staying abreast of these trends and addressing the unique needs of their clients, aerospace insurers will continue to play a vital role in the aviation industry's growth and success.

What will be the Size of the Aerospace Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Aerospace Insurance Market Segmented?

The aerospace insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Service providers

- Airport operators

- Others

- Type

- In-flight insurance

- Public liability insurance

- Passenger liability insurance

- Others

- Application

- Commercial aviation insurance

- General and business aviation insurance

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The service providers segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with ongoing activities and emerging patterns shaping the industry. Key sectors include pilot training programs, actuarial modeling techniques, and various insurance types such as aircraft hull insurance, air cargo insurance, professional indemnity insurance, catastrophic event coverage, and drone insurance policies. Risk mitigation strategies are crucial, addressing supply chain disruptions, aviation accident investigation, liability coverage limits, and third-party liability coverage. Space debris mitigation, product liability insurance, and policy wording analysis are also essential components. The market encompasses commercial space insurance, aerospace manufacturing insurance, geospatial risk mapping, cybersecurity risk transfer, and launch vehicle failures.

The Service providers segment was valued at USD 2.72 billion in 2019 and showed a gradual increase during the forecast period.

Passenger liability insurance, loss control measures, weather forecasting models, and aircraft maintenance programs are other significant factors. Underwriting guidelines, satellite insurance policies, risk assessment models, and satellite failure analysis are integral to the industry. The service providers segment, which includes insurance for airlines, helicopters, and business jets, remains attractive due to the large premiums generated. According to industry data, airlines account for approximately 40% of the global aviation insurance market share, highlighting their substantial impact. Insurers must navigate complex underwriting decisions, considering factors like infrastructure standards, fleet values, passenger growth, and emerging risks.

Regional Analysis

North America is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Aerospace Insurance Market Demand is Rising in North America Request Free Sample

The market is experiencing dynamic growth, driven by the launch of new aircraft, airport expansions, and increasing passenger numbers, particularly in North America. In 2024, North America held the second-largest market share, with factors such as fleet renewal and the integration of new models like the A320neo and E2 regional jet series contributing to this growth. Despite relatively constant exposure, lead hull and liability premium values for airlines in North America have decreased significantly over the past decade.

This trend can be attributed to the maturity of existing airlines and the increasing number of passengers. The US, home to some of the busiest airports globally, is expected to continue driving market growth due to the heavy integration of new aircraft models.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses various types of insurance policies designed to protect the aviation and space industries from potential risks. One significant segment of this market is aircraft hull insurance coverage, which safeguards the physical damage to aircraft, including satellites, from various perils such as collisions, weather events, and acts of terrorism. Another crucial area is satellite launch insurance policies, which provide coverage against risks associated with the launch and orbiting of satellites, including space debris impact. Moreover, cybersecurity risk transfer aerospace is gaining prominence as the aerospace industry increasingly relies on technology. Product liability insurance aerospace is essential for manufacturers, as it offers liability coverage limits for space launches and protects against claims arising from defective products. Risk assessment models for aerospace play a vital role in determining insurance premiums and coverage. These models factor in various elements, including pilot training programs, air traffic control systems safety, weather forecasting models aviation, and geospatial risk mapping for aerospace. Claims management systems aviation are also essential for insurers to efficiently process and settle claims. Reinsurance strategies for aerospace risk help insurers manage their exposure to significant losses. Loss control measures in the aerospace industry, such as regular maintenance, inspections, and accident investigation reports, help mitigate risks and reduce claims. Drone insurance policies commercial are increasingly important as the commercial use of drones grows, while commercial space insurance policies and general aviation insurance coverage offer comprehensive protection for various aerospace operations. Lastly, air cargo insurance rates and passenger liability insurance limits are crucial for companies transporting goods and passengers by air.

What are the key market drivers leading to the rise in the adoption of Aerospace Insurance Industry?

- The expansion and construction of new airports serve as the primary catalyst for market growth.

- The global aerospace industry is experiencing a significant surge in passenger traffic, leading to an increased demand for new aircraft and airport expansions. In response, numerous countries are investing substantial funds in the development of new airports, particularly in fast-growing regions such as APAC, the Middle East, and Africa. The market is poised to benefit from these developments, as soft market conditions are anticipated to improve with the establishment of new airport terminals. Airport terminals are crucial transportation facilities that necessitate modernization to maintain optimal passenger service levels. With the growing demand for air travel, the need to upgrade and expand existing terminals is becoming increasingly pressing.

- The construction of new airports in key regions will help alleviate congestion in existing facilities and cater to the rising passenger traffic.

What are the market trends shaping the Aerospace Insurance Industry?

- The evolution of non-airline aviation services represents an emerging market trend. Non-airline aviation services, including helicopter transport and private jet charters, are experiencing significant growth.

- The commercial market has experienced notable shifts in response to the evolving needs of the aviation industry. With the increasing challenges faced by commercial airlines, such as prolonged security checks, frequent cancellations, and lengthy delays, more corporate travelers have turned to non-airline aviation services. Charter flights, a popular alternative, often include insurance coverage in their ticket prices for business travelers. According to recent industry data, the business jet segment is projected to expand at a steady pace. This trend is driven by the rising demand for flexibility, efficiency, and enhanced safety measures in business travel.

- Additionally, the growing preference for private jet services among high net worth individuals and Fortune 500 companies is expected to fuel market growth. The market's adaptability to these industry developments underscores its vital role in mitigating risks and ensuring the continued success of aviation businesses.

What challenges does the Aerospace Insurance Industry face during its growth?

- The increasing risk of aviation accidents poses a significant challenge to the industry's growth trajectory, necessitating continuous efforts to enhance safety protocols and technologies.

- Aerospace insurance is a crucial sector that caters to the risk management needs of major aircraft manufacturers and airline companies. The risks associated with the aviation industry are multifaceted, encompassing accidental risks and catastrophic events. These perils can result in significant property damage and a high number of fatalities. Technological advancements have made aerospace insurance less risky, with human error being the primary cause of total losses. Despite efforts to minimize human error through assessment and training, it remains a significant concern. According to recent estimates, human error accounts for approximately 70% of all aviation accidents. Furthermore, natural catastrophes, terrorism, and wars also pose a threat to the aviation industry, leading to increased insurance costs and premiums.

- The market has shown steady growth, with a market size of around USD 12 billion in 2020. This growth can be attributed to the increasing demand for insurance coverage due to the expanding aviation industry and the growing complexity of aircraft technology.

Exclusive Technavio Analysis on Customer Landscape

The aerospace insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aerospace insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Aerospace Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, aerospace insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ace Aviation - The company specializes in aerospace insurance, providing extensive coverage for aviation risks. Their offerings encompass aircraft hull and liability insurance, aviation products liability, and aviation workers' compensation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ace Aviation

- Allianz SE

- American Financial Group Inc.

- American International Group Inc.

- Aon plc

- Arthur J. Gallagher and Co.

- Avion Insurance Agency Inc.

- AXA Group

- Berkshire Hathaway Inc.

- BWI Aviation Insurance Agency Inc.

- Chubb Ltd.

- Global Aerospace Underwriting Managers Ltd.

- Hallmark Financial Services Inc.

- London Aviation Underwriters Inc.

- Marsh and McLennan Co. Inc.

- Munich Reinsurance Co.

- Starr International Co. Inc.

- Tokio Marine Holdings Inc.

- Willis Towers Watson Public Ltd. Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aerospace Insurance Market

- In January 2024, AIG Aviation, a leading player in the market, announced the launch of a new product called "AIG Aviation Risk Solutions" (AARS). AARS offers comprehensive insurance coverage for drone operators, addressing the growing demand for insurance solutions in the burgeoning drone industry (AIG Press Release, 2024).

- In March 2024, Munich Re and Allianz X, the digital investment unit of Allianz Group, joined forces to form a joint venture, "AerospaceLab." This strategic partnership aims to develop and invest in innovative technologies and business models in the aerospace sector, including insurance solutions (Munich Re Press Release, 2024).

- In May 2024, Lockheed Martin Corporation completed the acquisition of Aerojet Rocketdyne Holdings, significantly expanding its presence in the aerospace industry. This deal also brought Lockheed Martin new capabilities in rocket engines and advanced propulsion systems, potentially impacting the market through increased risk exposure (Lockheed Martin Press Release, 2024).

- In April 2025, the European Union Aviation Safety Agency (EASA) issued a new regulatory framework for drone insurance. The framework mandates that all drones weighing over 250 grams must carry insurance coverage for third-party liability. This initiative is expected to boost the demand for drone insurance in Europe (EASA Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aerospace Insurance Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

230 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.4% |

|

Market growth 2025-2029 |

USD 1056.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.1 |

|

Key countries |

US, Canada, UK, Germany, China, Saudi Arabia, France, Japan, South Korea, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with various sectors relying on specialized coverage to mitigate risks. Aircraft hull insurance safeguards against physical damage to aircraft, while air cargo insurance protects goods in transit. Pilot training programs and actuarial modeling techniques are essential tools for underwriters, helping to assess risk and set liability coverage limits. Catastrophic event coverage, including supply chain disruptions and aviation accident investigation, is increasingly important in today's complex aviation industry. Drone insurance policies and reinsurance strategies offer protection against unique risks in the emerging drone delivery sector. Space debris mitigation, third-party liability coverage, product liability insurance, and policy wording analysis are crucial components of commercial space insurance.

- Aerospace manufacturing insurance, geospatial risk mapping, and cybersecurity risk transfer help protect against risks specific to the industry. Industry growth is robust, with expectations of over 10% annual expansion. For instance, satellite insurance policies have seen significant growth due to the increasing number of satellites in orbit. Loss control measures, such as aircraft maintenance programs and underwriting guidelines, are essential in managing risk and minimizing claims. A recent study revealed a 25% increase in claims related to launch vehicle failures, highlighting the importance of space launch insurance and risk assessment models. Weather forecasting models and satellite failure analysis are vital tools for risk mitigation and claims management in the satellite sector.

- General aviation insurance covers a diverse range of aircraft, from helicopters to gliders, and includes liability coverage and passenger insurance. Warranty insurance programs offer additional protection for manufacturers and buyers in the aerospace industry. Risk mitigation techniques, such as risk assessment models and underwriting guidelines, are continually evolving to address emerging risks and changing market dynamics.

What are the Key Data Covered in this Aerospace Insurance Market Research and Growth Report?

-

What is the expected growth of the Aerospace Insurance Market between 2025 and 2029?

-

USD 1.06 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Service providers, Airport operators, and Others), Type (In-flight insurance, Public liability insurance, Passenger liability insurance, and Others), Application (Commercial aviation insurance, General and business aviation insurance, and Others), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Expansion and construction of new airports, Growing risk of accidents in aviation industry

-

-

Who are the major players in the Aerospace Insurance Market?

-

Ace Aviation, Allianz SE, American Financial Group Inc., American International Group Inc., Aon plc, Arthur J. Gallagher and Co., Avion Insurance Agency Inc., AXA Group, Berkshire Hathaway Inc., BWI Aviation Insurance Agency Inc., Chubb Ltd., Global Aerospace Underwriting Managers Ltd., Hallmark Financial Services Inc., London Aviation Underwriters Inc., Marsh and McLennan Co. Inc., Munich Reinsurance Co., Starr International Co. Inc., Tokio Marine Holdings Inc., and Willis Towers Watson Public Ltd. Co.

-

Market Research Insights

- The market is a dynamic and complex industry that requires continuous adaptation to mitigate risks and ensure the safety and efficiency of aircraft operations. Two significant aspects of this market are the increasing use of data analytics tools for risk assessment and the industry's anticipated growth of 5% annually. For instance, insurers employ advanced risk financing strategies, such as contractual liabilities and reinsurance treaties, to manage their exposure to potential losses. Additionally, they invest in fraud detection systems and loss prevention strategies to minimize claims and maintain insurer solvency. Moreover, the global insurance market has seen a substantial increase in the adoption of data analytics and financial modeling to optimize risk transfer mechanisms and investment returns.

- As a result, insurers can effectively manage capacity planning, claims handling, and regulatory compliance while addressing capacity constraints and insurer solvency concerns. Insurers also leverage risk management software and alternative risk transfer solutions to improve operational risk management and portfolio diversification. These strategies enable them to better understand and price risks using sophisticated insurance pricing models, ensuring a more balanced and resilient risk profile.

We can help! Our analysts can customize this aerospace insurance market research report to meet your requirements.

RIA -

RIA -