AI And Robotics In Aerospace And Defense Market Size 2025-2029

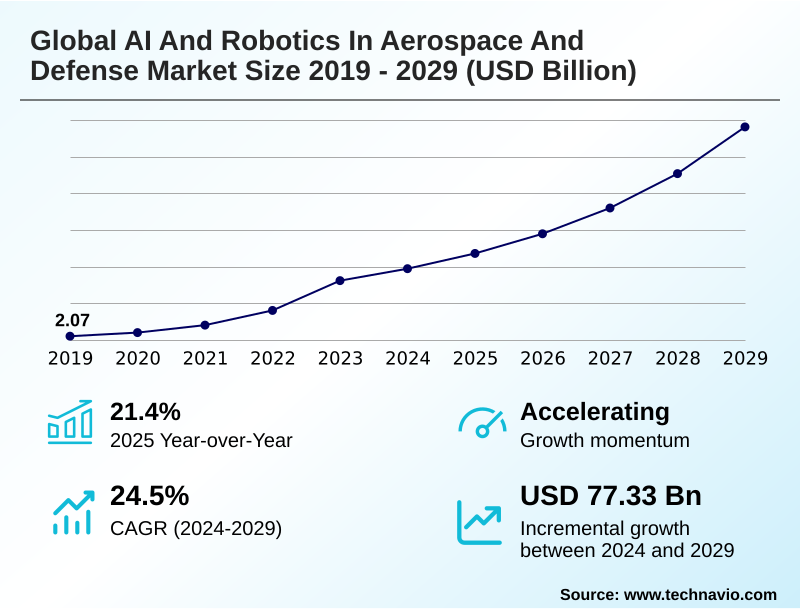

The ai and robotics in aerospace and defense market size is valued to increase by USD 77.33 billion, at a CAGR of 24.5% from 2024 to 2029. Enhanced autonomous capabilities for mission critical operations will drive the ai and robotics in aerospace and defense market.

Major Market Trends & Insights

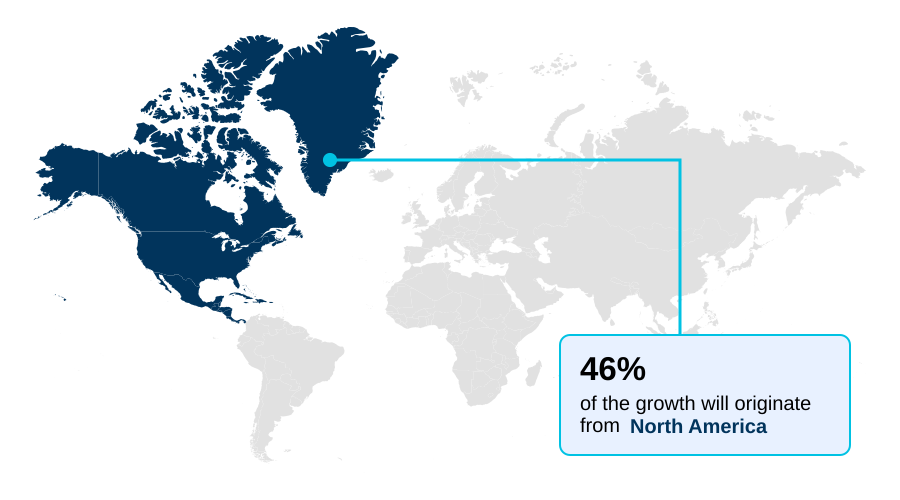

- North America dominated the market and accounted for a 45.7% growth during the forecast period.

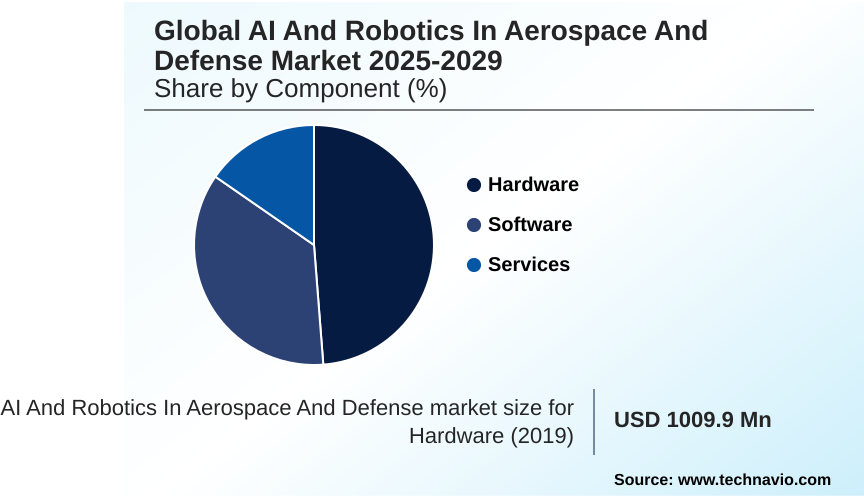

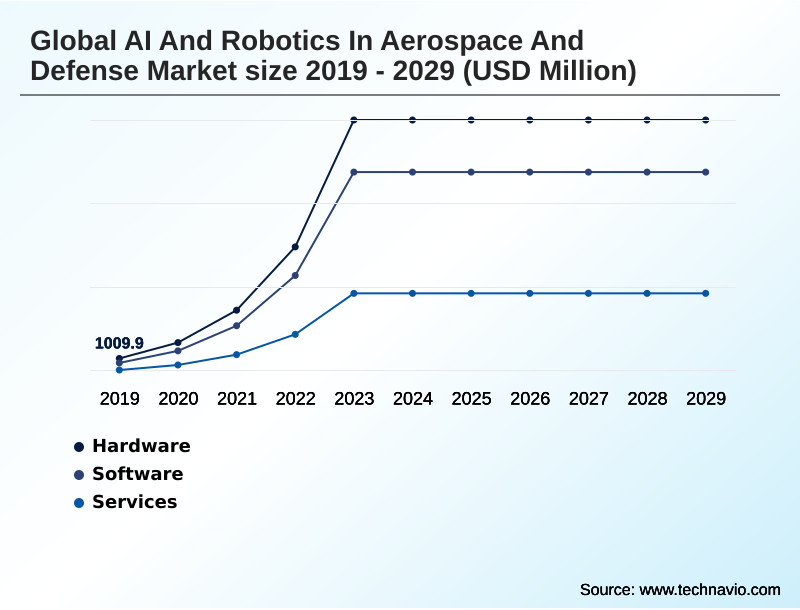

- By Component - Hardware segment was valued at USD 15.30 billion in 2023

- By Deployment - On premises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 114.16 billion

- Market Future Opportunities: USD 77.33 billion

- CAGR from 2024 to 2029 : 24.5%

Market Summary

- The AI And Robotics In Aerospace And Defense Market is undergoing a significant transformation, driven by the strategic imperative to achieve decision superiority and operational efficiency. Enhanced autonomous capabilities are propelling the adoption of intelligent systems for mission-critical operations, ranging from unmanned aerial vehicles executing complex reconnaissance to robotic platforms providing logistical support in hazardous environments.

- This evolution is underscored by rapid advancements in AI and robotic technologies, enabling new levels of performance and precision. A key application involves the use of AI-driven predictive maintenance platforms, which analyze real-time asset data to forecast component failures, thereby increasing fleet readiness and significantly reducing operational costs.

- However, the market's trajectory is tempered by considerable challenges, including the high development and integration costs associated with sophisticated systems, persistent cybersecurity vulnerabilities, and the complex ethical questions surrounding the deployment of autonomous weaponry. These factors create a dynamic landscape where innovation must be balanced with rigorous security and regulatory oversight.

What will be the Size of the AI And Robotics In Aerospace And Defense Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI And Robotics In Aerospace And Defense Market Segmented?

The ai and robotics in aerospace and defense industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Deployment

- On premises

- Cloud based

- Platform

- Airborne platforms

- Ground platforms

- Naval platforms

- Space platforms

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- UK

- Germany

- France

- Middle East and Africa

- Israel

- UAE

- Saudi Arabia

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment is foundational to the AI and robotics in aerospace and defense market, encompassing the physical components that enable advanced autonomous systems and AI for battlespace awareness.

This includes specialized processors for machine learning, sophisticated sensors for real-time threat detection, and robust robotic platforms like unmanned ground vehicles (UGVs) and collaborative combat aircraft (CCAs).

Innovations in edge AI are driving the development of hardware capable of on-device processing, which is critical for autonomous navigation systems in contested environments.

The integration of AI-driven quality control and digital twins into manufacturing hardware is also enhancing production efficiency and reliability.

The development of high assurance AI necessitates hardware that supports secure and resilient cognitive algorithm deployment, with some platforms improving data processing speeds by over 40% for mission-critical tasks.

The Hardware segment was valued at USD 15.30 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI And Robotics In Aerospace And Defense Market Demand is Rising in North America Request Free Sample

The geographic landscape of the AI and robotics market is led by North America, which accounts for over 45% of the market's incremental growth, primarily due to substantial defense investments in the United States in areas like AI-powered target recognition and autonomous flight technologies.

Meanwhile, the APAC region is projected to witness the fastest growth, with a CAGR of 25%, significantly outpacing Europe's 23.5% growth rate.

This expansion is driven by military modernization programs in countries like China and India, which are heavily investing in AI-enabled command and control and autonomous intelligence surveillance reconnaissance (ISR).

The Middle East and Africa is also an emerging hotspot, demonstrating the highest regional CAGR of 26.2%, as nations focus on adopting AI for national security and AI in combat support to bolster their capabilities.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic integration of AI and robotics in aerospace and defense is increasingly focused on complex, long-term objectives that extend beyond simple automation. A primary focus is on integrating AI into legacy defense platforms, a task that presents significant technical hurdles but promises to unlock new capabilities from existing assets.

- The success of this hinges on addressing the cybersecurity challenges for autonomous defense systems, as supply chain vulnerabilities for AI hardware and the risk of data poisoning remain critical concerns. The impact of AI on modern air combat is another key area, with extensive research dedicated to training AI pilots for collaborative combat.

- This involves advancing human-machine teaming in combat scenarios, where AI assists human operators rather than replacing them. Furthermore, the industry is grappling with the ethical considerations for developing military AI, particularly in regulating autonomous weapons in international law to prevent uncontrolled escalation.

- The benefits of robotics in defense manufacturing are more immediate, with some automated processes being twice as efficient as manual methods. In the field, AI's role in space situational awareness and for predictive maintenance in aircraft fleets is revolutionizing operational readiness.

- Efforts to validate AI systems for mission-critical use are ongoing, addressing issues like challenges of AI data fusion from sensors and the extensive data labeling requirements for defense AI. As the technology matures, generative AI applications in military planning and optimizing logistics with autonomous robots are set to redefine strategic operations.

What are the key market drivers leading to the rise in the adoption of AI And Robotics In Aerospace And Defense Industry?

- The expansion of enhanced autonomous capabilities for mission-critical operations serves as a key driver for market growth.

- Market growth is primarily driven by escalating defense modernization initiatives and rapid advancements in core technologies like natural language processing.

- The strategic need for enhanced autonomous capabilities for mission-critical operations is compelling nations to invest heavily in AI and robotics, with some government defense budgets for AI seeing increases of over 30% year-over-year.

- The development of sophisticated data fusion algorithms and predictive analytics is enabling superior battlespace awareness and AI in electronic warfare.

- The push for human-in-the-loop control systems ensures that even as platforms like loitering munitions and robotic combat vehicles become more autonomous, critical decision-making remains under human oversight.

- These advancements in human-machine teaming and AI in military logistics are fundamentally reshaping operational paradigms and enhancing force effectiveness.

What are the market trends shaping the AI And Robotics In Aerospace And Defense Industry?

- A primary trend shaping the market is the escalating adoption of artificial intelligence. This integration is pivotal for enhancing situational awareness and accelerating decision-making processes.

- Key trends shaping the market include the increased use of AI for situational awareness and the proliferation of robotics in maintenance. This is evident in the development of AI-driven data analysis tools that process vast sensor inputs to provide a clearer operational picture, improving threat detection accuracy by over 20%.

- The adoption of swarm technology and autonomous mission planning is transforming strategic capabilities, allowing for more complex and coordinated operations with reduced human oversight. Concurrently, the use of robotics in aircraft manufacturing is optimizing production lines and improving precision.

- The integration of autonomy software development for attritable autonomous systems is also gaining momentum, with some unmanned platforms now able to conduct missions for over 50 consecutive days, showcasing a significant leap in endurance and operational efficiency for multi-domain operations.

What challenges does the AI And Robotics In Aerospace And Defense Industry face during its growth?

- The presence of significant regulatory and ethical hurdles presents a key challenge affecting industry growth.

- Significant challenges constrain the market, led by stringent regulatory frameworks and profound ethical considerations surrounding LAWS. The high development and integration costs, coupled with the complexity of AI integration into legacy systems, present formidable barriers. For example, development cycles for secure autonomous systems can be two to three times longer than for commercial software.

- Furthermore, persistent cybersecurity vulnerabilities and the need to build trust in AI systems are critical concerns. The threat of adversarial AI attacks and AI model data poisoning necessitates robust, resilient architectures.

- The reliance on specialized talent and the extensive testing required for systems like AI-defined ground stations and UUVs add to the overall complexity and expense of responsible AI deployment, making it a capital-intensive endeavor.

Exclusive Technavio Analysis on Customer Landscape

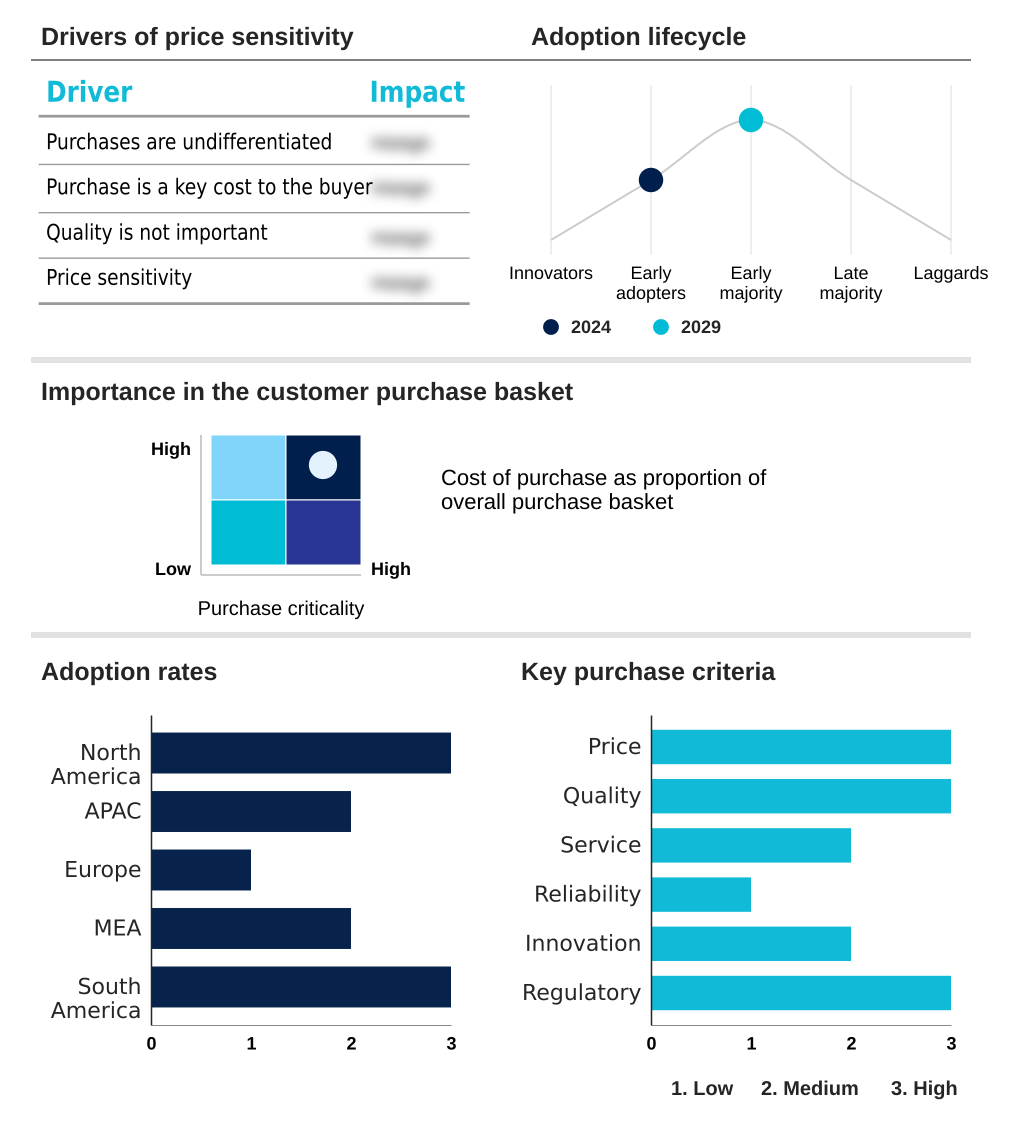

The ai and robotics in aerospace and defense market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai and robotics in aerospace and defense market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI And Robotics In Aerospace And Defense Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai and robotics in aerospace and defense market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Pioneers autonomous flight technologies and robotic assistants, driving innovation in future combat air systems and space exploration platforms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Anduril Industries Inc.

- General Electric Co.

- Honeywell International Inc.

- Indra Sistemas SA

- Intel Corp.

- IBM Corp.

- Lockheed Martin Corp.

- Microsoft Corp.

- Northrop Grumman Corp.

- NVIDIA Corp.

- Palantir Technologies Inc.

- RTX Corp.

- Shield AI

- SITA

- Thales Group

- The Boeing Co.

- T-Systems International GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai and robotics in aerospace and defense market

- In December, 2024, Lockheed Martin Corp. announced the integration of IBM advanced Granite large language models into its AI Factory tools, aiming to enhance innovation across its defense and aerospace offerings.

- In October, 2024, Northrop Grumman Corp. introduced an artificial intelligence feature to its Forward Area Air Defense Advanced Battle Manager system to improve real-time decision-making for counter-unmanned aerial systems missions.

- In October, 2024, Lockheed Martin Corp. demonstrated advanced AI-driven autonomous systems for crewed-uncrewed teaming at U.S. Army events, showcasing capabilities in complex air and ground scenarios even with degraded communications.

- In February, 2025, RTX Corp.'s Raytheon business successfully completed flight testing of its Cognitive Algorithm Deployment System, which integrates AI models into legacy radar warning receiver systems for real-time threat prioritization.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI And Robotics In Aerospace And Defense Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.5% |

| Market growth 2025-2029 | USD 77331.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 21.4% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, UK, Germany, France, Italy, The Netherlands, Spain, Israel, UAE, Saudi Arabia, Turkey, South Africa, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI and robotics in aerospace and defense market is defined by a rapid cycle of innovation, where the development of autonomous systems is a core focus. The proliferation of machine learning and computer vision is enabling sophisticated applications, from unmanned aerial vehicles (UAVs) and unmanned ground vehicles (UGVs) to advanced predictive maintenance platforms.

- A key area is the development of collaborative combat aircraft (CCAs) and the underlying AI pilots that facilitate crew-uncrewed teaming. The integration of AI-driven decision support systems is transforming command and control, while robotics in manufacturing and maintenance are streamlining production.

- For instance, AI-driven quality control has been shown to improve defect detection accuracy by up to 30% over manual inspection. However, the advancement of lethal autonomous weapon systems (LAWS) introduces significant ethical and regulatory discussions at the boardroom level, compelling leadership to balance technological advantage with responsible deployment strategies.

- The push towards multi-domain operations is further driving the need for technologies like drone swarms and AI for threat detection, creating a complex but opportunity-rich landscape.

What are the Key Data Covered in this AI And Robotics In Aerospace And Defense Market Research and Growth Report?

-

What is the expected growth of the AI And Robotics In Aerospace And Defense Market between 2025 and 2029?

-

USD 77.33 billion, at a CAGR of 24.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, Services), Deployment (On premises, Cloud based), Platform (Airborne platforms, Ground platforms, Naval platforms, Space platforms) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Enhanced autonomous capabilities for mission critical operations, Regulatory and ethical hurdles

-

-

Who are the major players in the AI And Robotics In Aerospace And Defense Market?

-

Airbus SE, Anduril Industries Inc., General Electric Co., Honeywell International Inc., Indra Sistemas SA, Intel Corp., IBM Corp., Lockheed Martin Corp., Microsoft Corp., Northrop Grumman Corp., NVIDIA Corp., Palantir Technologies Inc., RTX Corp., Shield AI, SITA, Thales Group, The Boeing Co. and T-Systems International GmbH

-

Market Research Insights

- The dynamics of the AI and robotics in aerospace and defense market are shaped by a strategic push for technological superiority. The adoption of AI for operational efficiency and AI for mission readiness is paramount, with some platforms improving threat identification accuracy by over 30% compared to legacy systems.

- This drive for AI-enabled predictive logistics and decision superiority through AI is balanced by significant implementation hurdles. Development cycles for secure autonomous resupply missions and other advanced systems can be 2-3 times longer than for typical commercial software due to stringent testing and validation requirements.

- The focus on AI for resource allocation aims to optimize expenditures, but the initial investment in capabilities like generative AI use cases remains a considerable factor for budget-conscious defense organizations.

We can help! Our analysts can customize this ai and robotics in aerospace and defense market research report to meet your requirements.

RIA -

RIA -