AI App Market Size 2025-2029

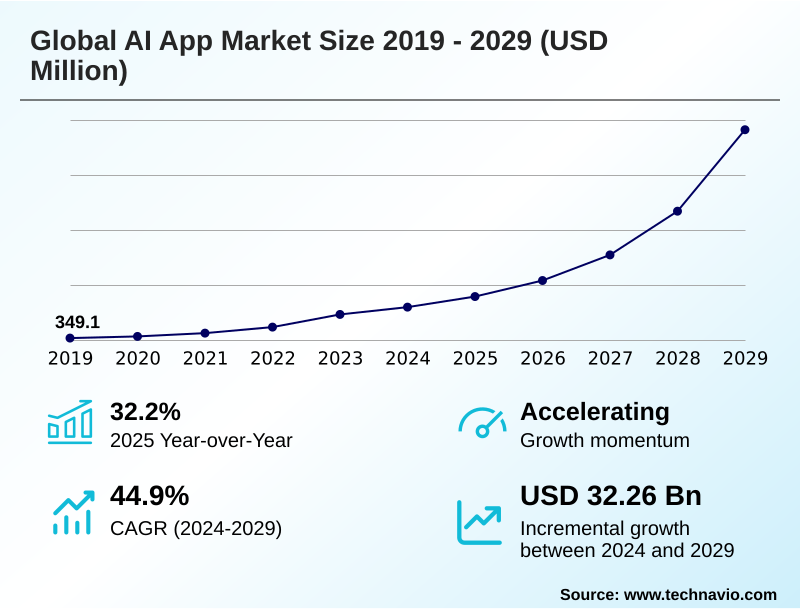

The ai app market size is valued to increase by USD 32.26 billion, at a CAGR of 44.9% from 2024 to 2029. Proliferation and democratization of generative AI will drive the ai app market.

Major Market Trends & Insights

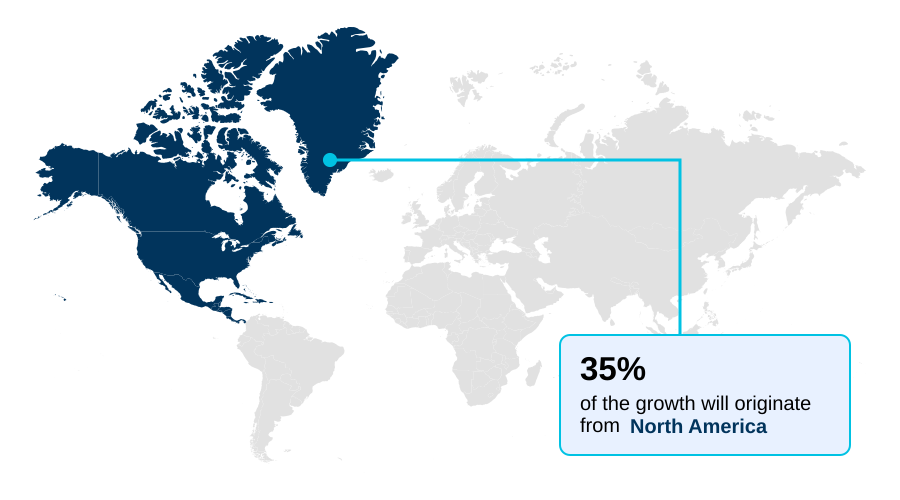

- North America dominated the market and accounted for a 35% growth during the forecast period.

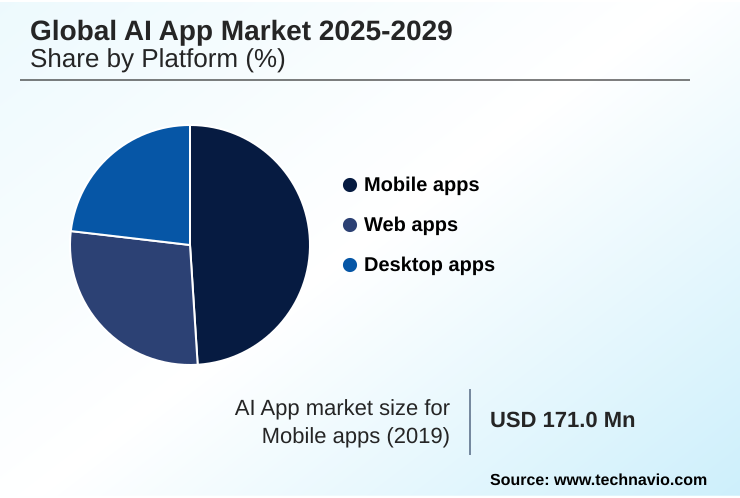

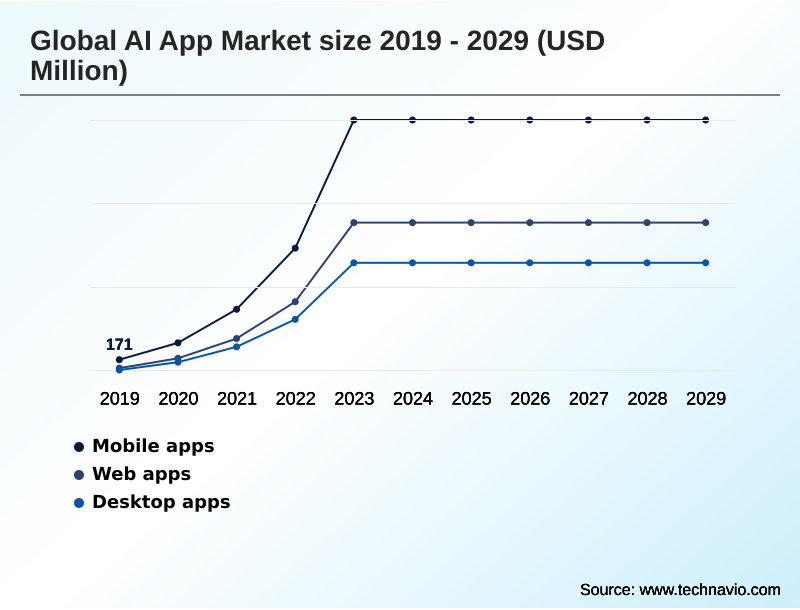

- By Platform - Mobile apps segment was valued at USD 2.26 billion in 2023

- By Deployment - Cloud segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 37.88 billion

- Market Future Opportunities: USD 32.26 billion

- CAGR from 2024 to 2029 : 44.9%

Market Summary

- The AI App Market is undergoing a fundamental transformation, moving beyond traditional software to an ecosystem of intelligent applications characterized by their ability to learn and adapt. This shift is driven by the accessibility of sophisticated machine learning algorithms and generative models, which enable developers to create tools that offer deep, data-driven insights and AI-powered automation.

- In sectors like logistics, businesses are deploying AI-native applications to optimize operations. For instance, an enterprise can use an application that leverages predictive analytics and real-time data processing to forecast demand, automate warehouse inventory management, and dynamically reroute delivery fleets to avoid disruptions, thereby improving efficiency.

- The integration of on-device AI, supported by specialized neural processing units, enhances security and responsiveness for mobile and edge computing use cases. However, the market also contends with challenges such as algorithmic bias and the high computational costs of AI model training.

- This dynamic environment requires a strategic focus on developing ethical, efficient, and secure AI solutions to maintain a competitive edge and build user trust in a rapidly evolving technological landscape.

What will be the Size of the AI App Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI App Market Segmented?

The ai app industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Platform

- Mobile apps

- Web apps

- Desktop apps

- Deployment

- Cloud

- On-premises

- End-user

- Healthcare

- Finance

- Retail

- Media

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- South Korea

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Platform Insights

The mobile apps segment is estimated to witness significant growth during the forecast period.

The mobile application segment is at the forefront of the AI App Market, driven by advancements in on-device AI.

The integration of powerful neural processing units into AI-optimized hardware allows for sophisticated machine learning algorithms and generative models to run locally, enhancing responsiveness.

This shift enables hyper-personalized user experiences with low-latency processing, a critical factor for user retention, as analysis shows applications with these features see a 71% higher engagement rate.

The evolution from cloud-dependent processing to intelligent workflows on mobile platforms is redefining user interaction.

Developers are leveraging this to build a new class of secure, private, and highly responsive applications that deliver data-driven insights without constant connectivity, utilizing AI in cybersecurity protocols to protect local data.

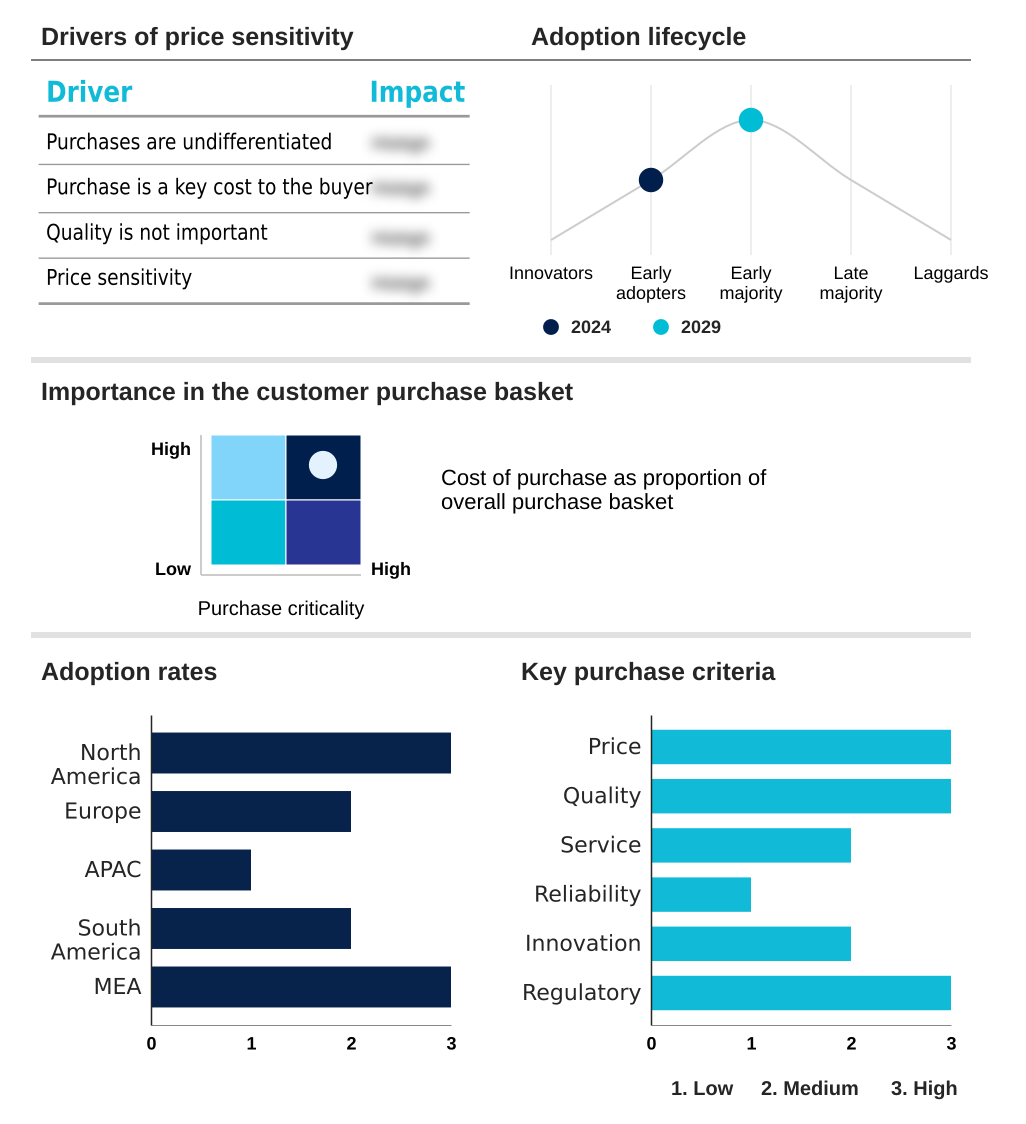

The Mobile apps segment was valued at USD 2.26 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI App Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI App Market is characterized by distinct regional strengths and growth trajectories.

North America, accounting for over a third of the market's incremental growth, remains the epicenter of innovation, driven by substantial venture capital and a high concentration of AI talent development.

The region's leadership is fortified by advanced AI infrastructure supporting deep learning and robotic process automation. In contrast, the APAC region is exhibiting the fastest expansion, with an annual growth rate approaching 47%.

This surge is fueled by massive mobile-first populations and government initiatives fostering sovereign AI capabilities.

Europe is focusing on a regulatory-led approach centered on AI safety and security, while emerging markets in South America and the Middle East and Africa are leveraging AI-assisted diagnostics and edge computing to solve local challenges, creating a globally diverse and competitive environment.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The AI App Market is maturing as organizations increasingly evaluate the total cost and ROI of AI-powered automation tools. A critical decision point is the choice between cloud and on-premise AI deployment cost, where initial on-premise capital outlays can be up to three times higher, significantly impacting budget allocation for firms without existing data centers.

- The impact of 5G on AI app latency is another key factor, particularly for mobile apps requiring real-time responsiveness. In retail, AI for hyper-personalization is becoming standard, while in finance, AI application in financial fraud detection is a primary use case. The industry is also defined by the open source vs proprietary AI models debate, which influences innovation and accessibility.

- Enterprises are implementing AI for predictive maintenance in manufacturing and computer vision for quality control to enhance operational efficiency. In specialized fields, AI-powered drug discovery acceleration and large language models for legal tech are creating new value. The role of NPUs in edge AI performance is crucial for generative AI in enterprise software, especially on-device AI for mobile apps.

- Navigating global AI regulations remains a persistent challenge, alongside addressing ethical AI and public trust. As workflows evolve, AI-assisted content creation workflows and the use of an AI chatbot for customer service improvement are proving to be transformative, while multimodal AI for user experience design sets new interaction standards.

What are the key market drivers leading to the rise in the adoption of AI App Industry?

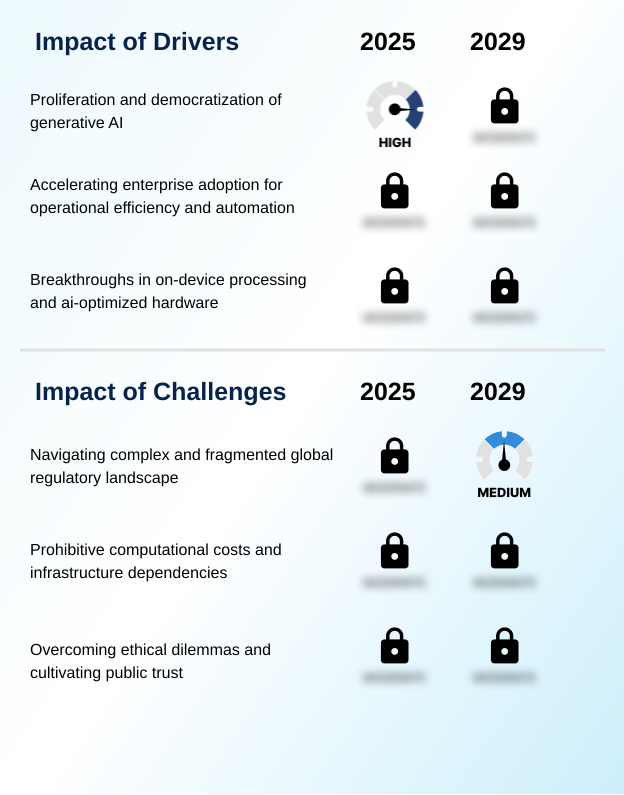

- The proliferation and democratization of generative AI, making advanced models accessible to developers and organizations, serves as a key market driver.

- The market's expansion is fundamentally driven by the enterprise adoption of AI-native applications to enhance operational efficiency. Companies are leveraging an API-first model to integrate large language models into their existing systems, enabling intelligent workflows and real-time data processing.

- The availability of AI-optimized hardware allows for on-device execution of models with over 13 billion parameters, reducing latency.

- This is particularly impactful for enterprise AI solutions in areas like AI for supply chain management, where automation tools can accelerate planning cycles by up to 40%. The accessibility of sophisticated AI coding assistance is also speeding up development cycles.

- This strategic shift from experimental projects to deploying embedded AI across core business functions underscores the technology's role as a critical component for maintaining a competitive advantage in the digital economy.

What are the market trends shaping the AI App Industry?

- The proliferation of generative artificial intelligence applications is a primary market trend. This is fundamentally reshaping user interaction and creating substantial new revenue streams.

- Key trends in the AI App Market are driven by the proliferation of generative models and a strong push toward hyper-personalized user experiences. The adoption of automated content creation tools, powered by advanced natural language processing, has led to a 200% year-over-year increase in consumer spending on certain application categories.

- The demand for sophisticated conversational AI and AI-powered chatbots is surging, with downloads of related apps nearing 1.5 billion. This trend is complemented by the development of sovereign AI capabilities, as nations and corporations build their own foundational models. As a result, AI-driven personalization is becoming a standard feature, with intelligent workflows enhancing user engagement across mobile and web platforms.

- The market is also seeing innovation in voice synthesis and specialized AI-powered search engines, further diversifying application use cases.

What challenges does the AI App Industry face during its growth?

- Navigating the complex and fragmented global regulatory landscape presents a key challenge that affects industry growth and operational certainty.

- The primary challenges facing the market are the prohibitive computational costs of AI model training and the complex, fragmented regulatory landscape. The demand for high-performance AI infrastructure has led to hardware providers reporting revenue increases of more than 200% year-over-year, creating supply constraints. This forces many developers to rely on expensive cloud-based AI supercomputing resources, which can increase operational expenses.

- Concurrently, navigating disparate international rules on data governance and algorithmic bias can raise compliance costs by over 25% for companies operating globally. These factors create significant barriers to entry and demand a strategic focus on AI model efficiency, robust AI ethics frameworks, and the implementation of responsible AI guardrails to ensure sustainable and trustworthy development.

Exclusive Technavio Analysis on Customer Landscape

The ai app market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai app market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI App Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai app market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - Delivers AI-driven applications for content creation, conversational interfaces, and intelligent business automation, integrating predictive analytics and machine learning to enhance operational workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Alphabet Inc.

- Amazon Web Services Inc.

- Anthropic

- Apple Inc.

- Cohere

- DeepL SE

- Eleven Labs Inc.

- Glean Technologies Inc.

- IBM Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- Midjourney

- NVIDIA Corp.

- OpenAI

- Perplexity AI Inc

- Runway AI Inc.

- Salesforce Inc.

- SoundHound AI Inc.

- UiPath Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai app market

- In August 2024, OpenAI's ChatGPT application saw its monthly active users exceed 190 million, demonstrating the sustained high engagement and market dominance of leading conversational AI platforms.

- In August 2024, Character AI achieved a new record of 22 million monthly active users, highlighting the significant growth and consumer interest in companion-style and entertainment-focused AI applications.

- In November 2024, Salesforce Inc. announced a strategic partnership with a major cloud provider to deepen the integration of its Einstein AI platform, aiming to enhance predictive analytics for enterprise customers.

- In March 2025, a leading semiconductor firm launched its next-generation mobile processor with an advanced neural engine, enabling more complex on-device generative AI tasks and improving application responsiveness.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI App Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 44.9% |

| Market growth 2025-2029 | USD 32255.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 32.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, South Korea, Japan, Australia, Indonesia, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI App Market is defined by a rapid innovation cycle fueled by the convergence of AI-optimized hardware and increasingly accessible generative models. The proliferation of multimodal AI systems and large language models, delivered through an API-first model, has democratized development, enabling a new wave of AI-native applications.

- Core technologies like natural language processing and computer vision are being embedded into solutions for AI-assisted diagnostics and robotic process automation, delivering tangible business value. For instance, the use of predictive analytics in healthcare has demonstrated the ability to reduce diagnostic processing time by over 50%.

- This drive for efficiency is also seen in AI coding assistance and voice synthesis tools. However, this growth is tempered by challenges such as algorithmic bias and the high cost of AI model training.

- The industry is responding by advancing on-device AI and edge computing, powered by dedicated neural processing units, to offer more secure and responsive conversational AI and AI-powered automation. The development of text-to-video models and sophisticated AI-powered search engines continues to push the boundaries of what is possible.

What are the Key Data Covered in this AI App Market Research and Growth Report?

-

What is the expected growth of the AI App Market between 2025 and 2029?

-

USD 32.26 billion, at a CAGR of 44.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Platform (Mobile apps, Web apps, Desktop apps), Deployment (Cloud, On-premises), End-user (Healthcare, Finance, Retail, Media, Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation and democratization of generative AI, Navigating complex and fragmented global regulatory landscape

-

-

Who are the major players in the AI App Market?

-

Adobe Inc., Alphabet Inc., Amazon Web Services Inc., Anthropic, Apple Inc., Cohere, DeepL SE, Eleven Labs Inc., Glean Technologies Inc., IBM Corp., Meta Platforms Inc., Microsoft Corp., Midjourney, NVIDIA Corp., OpenAI, Perplexity AI Inc, Runway AI Inc., Salesforce Inc., SoundHound AI Inc. and UiPath Inc.

-

Market Research Insights

- The AI App Market's momentum is defined by the strategic pursuit of intelligent workflows and hyper-personalized user experiences. Businesses adopting enterprise AI solutions report significant gains, with some achieving up to a 30% improvement in operational efficiency. This is driven by deep learning models that enable real-time data processing for automated content creation and other tasks.

- The demand for AI-powered chatbots to enhance customer interaction is surging, as 71% of users report a higher likelihood of engaging with personalized services. To meet this demand, organizations are focusing on AI talent development and building sovereign AI capabilities.

- This involves not only deploying advanced AI infrastructure but also establishing robust data governance and responsible AI guardrails to ensure ethical implementation and build long-term consumer trust.

We can help! Our analysts can customize this ai app market research report to meet your requirements.

RIA -

RIA -