AI For Scientific Discovery Market Size 2025-2029

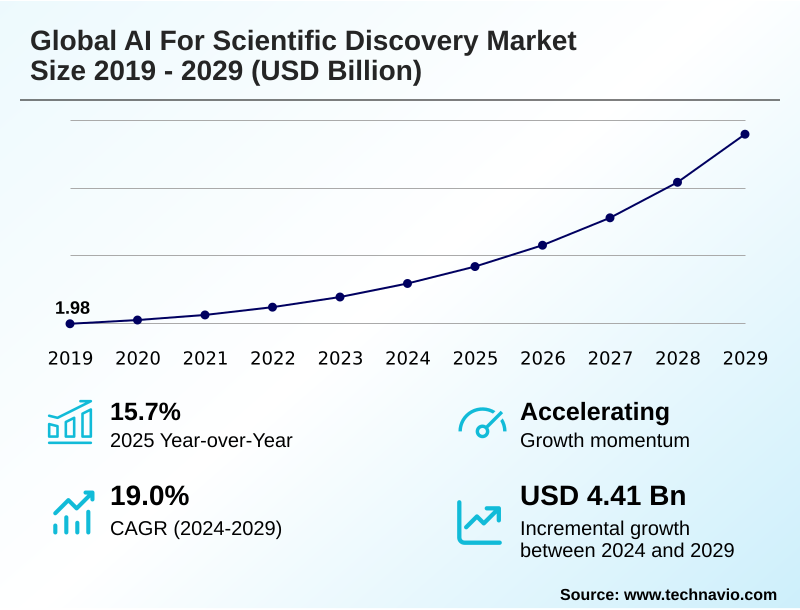

The ai for scientific discovery market size is valued to increase by USD 4.41 billion, at a CAGR of 19% from 2024 to 2029. Proliferation of high-volume scientific data and advanced computational infrastructure will drive the ai for scientific discovery market.

Major Market Trends & Insights

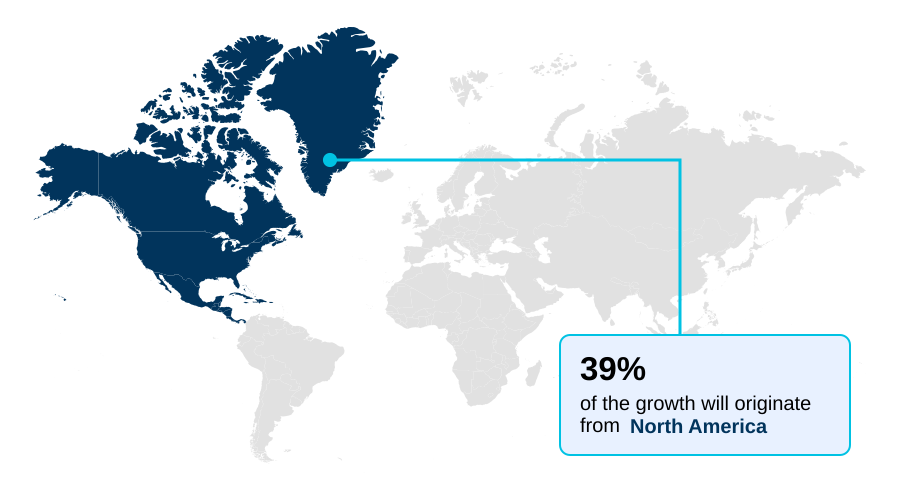

- North America dominated the market and accounted for a 39.2% growth during the forecast period.

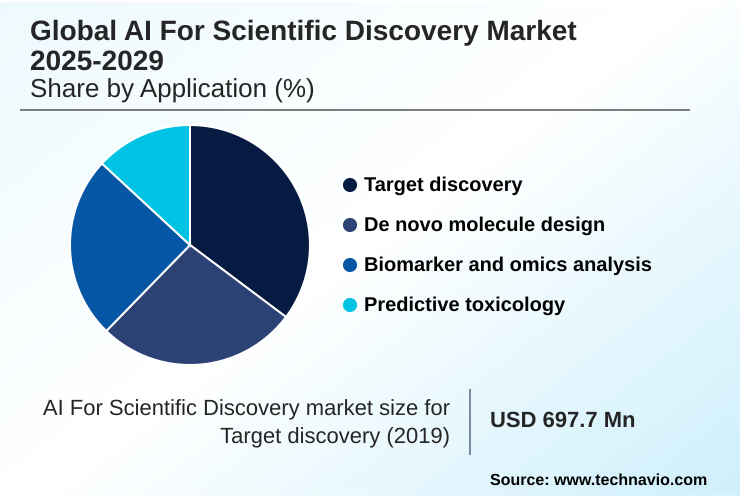

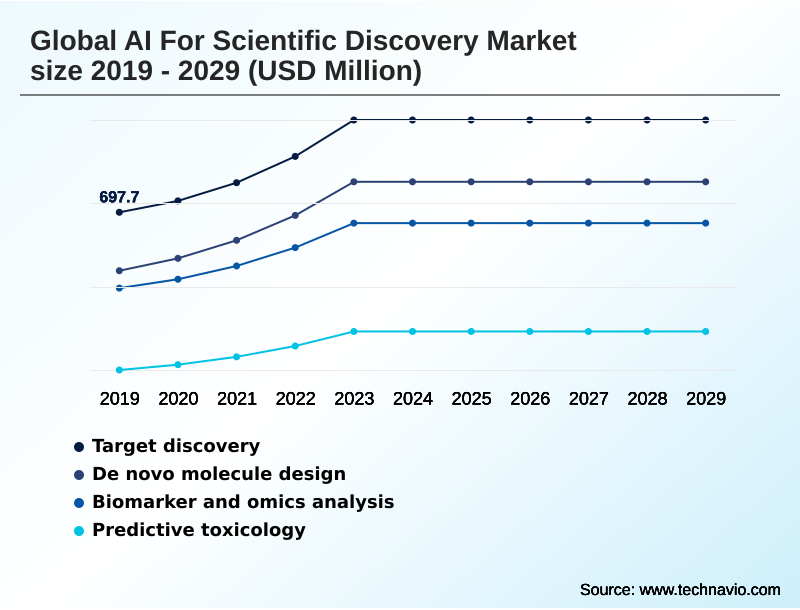

- By Application - Target discovery segment was valued at USD 954.1 million in 2023

- By Technology - Generative models segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 5.60 billion

- Market Future Opportunities: USD 4.41 billion

- CAGR from 2024 to 2029 : 19%

Market Summary

- The AI for scientific discovery market is undergoing a fundamental transformation, shifting research from traditional empirical methods to a data-centric paradigm. This evolution is driven by the capacity of sophisticated algorithms to analyze vast and complex information, enabling breakthroughs at an unprecedented pace. The application of AI now spans from initial R&D stages to late-phase clinical studies.

- For instance, pharmaceutical firms leverage predictive toxicology and pharmacokinetic modeling to de-risk their drug development pipelines, improving candidate success rates and optimizing resource allocation before committing to expensive trials. This computational approach allows for in silico modeling that can simulate biological responses, drastically reducing the need for costly and time-consuming experimentation.

- The market is characterized by rapid innovation in generative models and graph neural networks, which are used for de novo molecule design and understanding complex biological systems. However, challenges surrounding model interpretability and the need for explainable AI (XAI) persist, as scientific validation requires a clear understanding of the model's reasoning.

- The increasing accessibility of high-performance computing further fuels this expansion, democratizing access to powerful tools for researchers globally and fostering automated hypothesis generation.

What will be the Size of the AI For Scientific Discovery Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI For Scientific Discovery Market Segmented?

The ai for scientific discovery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Target discovery

- De novo molecule design

- Biomarker and omics analysis

- Predictive toxicology

- Technology

- Generative models

- Graph and molecular ML

- Physics-informed ML

- Simulation and digital twins

- End-user

- Pharmaceutical research and development

- Biotechnology companies

- Academic and national labs

- Chemical and materials science firms

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The target discovery segment is estimated to witness significant growth during the forecast period.

The application of AI is redefining scientific exploration, moving beyond data analysis to active creation. The use of physics-informed ml integrates established scientific laws into machine learning, improving model accuracy in data-poor environments by over 30%.

This enables the development of digital twins in research, creating high-fidelity virtual replicas of complex systems for exhaustive testing. In materials informatics, AI platforms systematically screen vast compound libraries, accelerating the discovery of novel materials.

Similarly, quantum chemistry simulation is becoming more accessible, allowing for precise molecular modeling.

This paradigm shift supports automated hypothesis generation, where AI systems propose novel research questions, and moves toward a closed-loop discovery process where AI designs, executes, and analyzes experiments autonomously with tools like large language models for science and open source ai tools for researchers.

These ai applications in synthetic biology and with ai-assisted experimental design are accelerating progress in ai in quantum physics and for ai for sustainable materials, enabled by molecular dynamics simulation.

The Target discovery segment was valued at USD 954.1 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI For Scientific Discovery Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is led by North America, which is set to contribute nearly 40% of incremental growth, driven by substantial private and public investment in ai-driven r&d.

This region excels in developing platforms for clinical trial optimization and applying advanced algorithms to real-world evidence analysis. Europe stands as a mature market, emphasizing collaborative research and leveraging AI for detailed proteomic analysis and metabolomic data interpretation.

The APAC region is the fastest-growing, with its 19.8% CAGR fueled by national strategies in countries like China to build leadership in technology. This includes significant investments in genomic data integration and transcriptomic analysis to support public health initiatives.

The adoption of AI in South America and the Middle East and Africa is accelerating, with a focus on applying ai in personalized medicine and supporting ai for rare disease research through robotic process automation in labs and other accelerated discovery cycles.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The practical application of AI is fundamentally reshaping scientific R&D across multiple domains. Beyond life sciences, using generative ai for novel catalysts and advancements in ai for battery material discovery demonstrate how ai accelerates materials science.

- In pharmaceuticals, the impact of ai on preclinical research is profound, with graph neural networks for drug interaction and robust ai-based target validation methods becoming standard.

- These technologies address the significant cost of ai in drug development by improving efficiency; indeed, the ai role in reducing r&d timelines is a primary value proposition, with firms using automated scientific hypothesis generation platforms reporting more than double the rate of novel target identification. A key technical debate involves generative models versus virtual screening, with hybrid approaches gaining traction.

- However, challenges in ai model validation and the difficulty of interpreting ai models in biology remain critical hurdles. The availability of open source ai tools for researchers and dedicated ai platforms for genomic sequencing is helping to democratize access.

- This ecosystem is enabling sophisticated applications, including building a digital twin for biological systems, advancing ai for predicting adverse drug reactions, and powering new ai applications in synthetic biology. Progress in physics-informed ml for fluid dynamics and ai for analyzing omics data sets further showcases the technology's expanding reach.

What are the key market drivers leading to the rise in the adoption of AI For Scientific Discovery Industry?

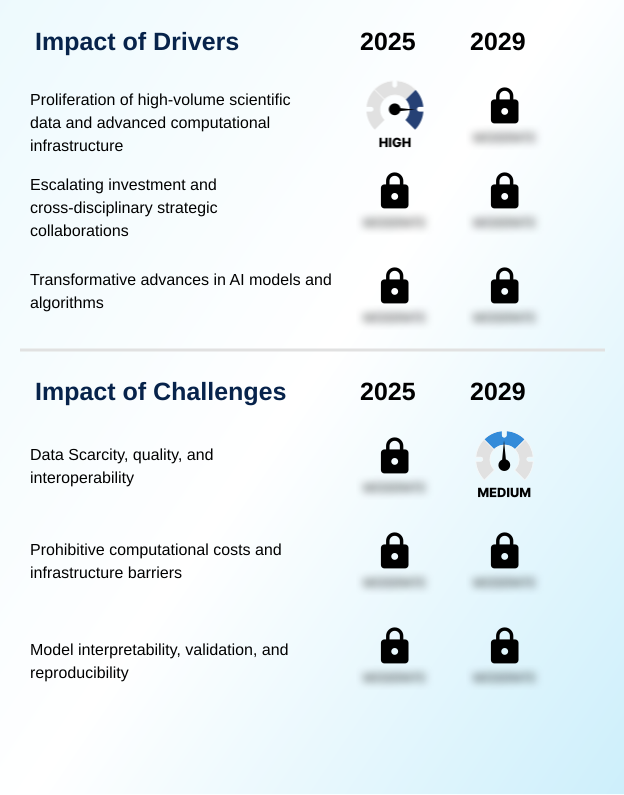

- The proliferation of high-volume scientific data, coupled with advanced computational infrastructure, serves as a key driver for market growth.

- Market growth is significantly driven by the expanding accessibility of high-performance computing (hpc) for ai and sophisticated computational infrastructure for ai. This enables complex computational drug design and large-scale virtual screening, which were once restricted to elite institutions.

- The result is an acceleration in target discovery and biomarker analysis, with automated lab experimentation platforms reducing manual workloads by over 50%.

- The ability to perform detailed structure-activity relationship analysis and utilize ai for scientific literature analysis helps researchers identify promising leads faster. Moreover, ai-powered biomarker discovery is becoming more precise.

- The development of neural networks for chemical synthesis and the use of digital twin for climate modeling showcase the technology's broad impact. Bioinformatics platforms now offer powerful tools that dramatically shorten research cycles.

What are the market trends shaping the AI For Scientific Discovery Industry?

- The exponential growth in multi-modal and high-dimensional scientific data is an emerging market trend. This requires advanced analytical platforms to derive meaningful insights.

- Key market trends are centered on the sophistication of AI architectures. The adoption of generative models and graph neural networks is enabling breakthroughs in protein structure prediction and de novo molecule design. These technologies are crucial for ai platforms for drug discovery and advancements in machine learning in materials science.

- By leveraging generative ai for protein design, organizations are creating novel therapeutics that were previously unfeasible. The application of deep learning for genomics and graph ml in molecular biology allows for a systems biology approach, integrating high-dimensional data from multiple sources.

- This multi-modal data analysis capability is yielding deeper insights, with leading research teams reporting a 25% improvement in identifying viable candidates. Furthermore, predictive models for toxicology are becoming more accurate, de-risking development pipelines earlier in the process.

What challenges does the AI For Scientific Discovery Industry face during its growth?

- Challenges related to data scarcity, quality, and interoperability are significantly affecting industry growth.

- Significant market challenges persist, particularly concerning the 'black box' problem, which elevates the need for explainable ai (xai) and robust methods for model interpretability. Addressing challenges in ai model validation is critical, as over 70% of researchers cite issues with data quality and interoperability as primary obstacles to implementing a data-driven scientific method.

- Data scarcity in niche domains further complicates training reliable models, although techniques like federated learning are emerging as a solution. The high computational cost associated with training state-of-the-art models remains a barrier for many organizations.

- Ensuring reproducible ai in science is fundamental for institutional trust, especially when interpreting ai models in biology or analyzing complex machine learning for clinical data and ai in astrophysics data. These factors are shaping development priorities toward more transparent and efficient AI systems, especially in high-stakes areas like ai for pandemic preparedness.

Exclusive Technavio Analysis on Customer Landscape

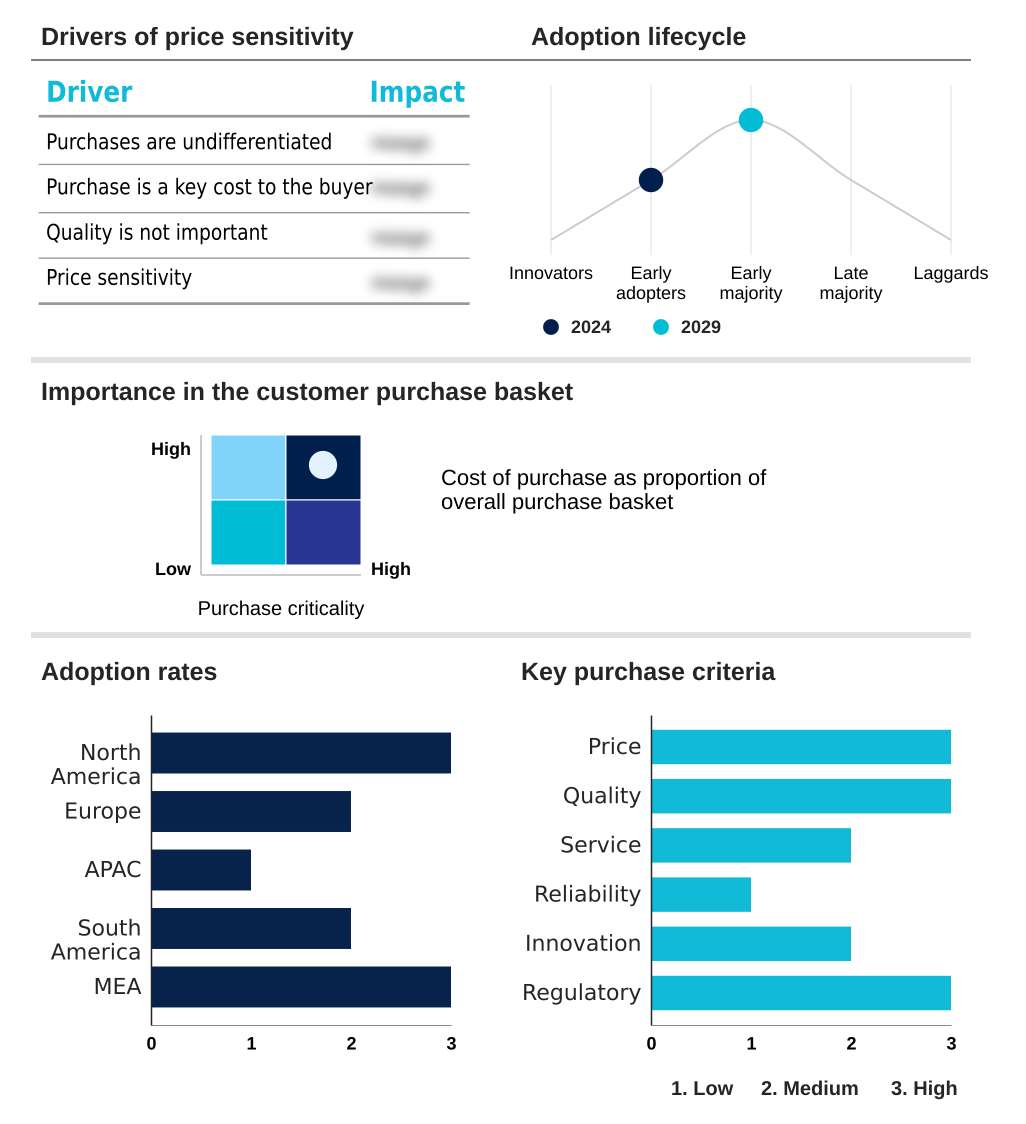

The ai for scientific discovery market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai for scientific discovery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI For Scientific Discovery Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai for scientific discovery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbCellera Biologics Inc. - Accelerates therapeutic antibody discovery through an AI-powered engine, significantly shortening development timelines for complex biologics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbCellera Biologics Inc.

- Amazon Web Services Inc.

- Atomwise Inc.

- Benchling Inc.

- BenchSci Analytics Inc.

- BenevolentAI

- Evaxion AS

- Generate Biomedicines

- Google LLC

- Healx Ltd.

- IBM Corp.

- Insilico Medicine

- Microsoft Corp.

- Nimbus Therapeutics

- Novartis AG

- NVIDIA Corp.

- Recursion Pharmaceuticals Inc.

- Schrodinger Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai for scientific discovery market

- In September 2024, Takeda Pharmaceutical Company announced the expansion of its collaboration with an AI drug discovery firm to identify novel therapeutic targets for complex neurological disorders.

- In November 2024, Recursion Pharmaceuticals Inc. initiated a multi-year collaboration with a leading academic medical center to create one of the largest multi-modal cancer datasets, aiming to identify novel biomarkers.

- In January 2025, Schrodinger Inc. launched an advanced update to its physics-based computational platform, integrating a new generative AI module for de novo protein design.

- In March 2025, Microsoft Corp. announced a strategic initiative to provide significant Azure cloud computing credits to researchers focused on using AI for climate change and sustainability science.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI For Scientific Discovery Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19% |

| Market growth 2025-2029 | USD 4407.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 15.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by the rapid maturation of AI from a niche tool to a core component of the scientific R&D process. Foundational technologies such as generative models and graph neural networks are now central to industrial applications, including de novo molecule design and materials informatics.

- This technological shift is compelling a strategic pivot in corporate budgeting toward bioinformatics platforms and computational drug design to maintain a competitive edge. The entire discovery pipeline, from initial target discovery and biomarker analysis to clinical trial optimization, is being re-engineered with AI. For example, platforms integrating physics-informed ml have demonstrated a 30% improvement in simulation accuracy with sparse data.

- The ability to perform high-fidelity molecular dynamics simulation and quantum chemistry simulation is accelerating research. The focus is now on integrating multi-modal data analysis from genomic data integration and proteomic analysis to create a holistic view within systems biology.

- The demand for explainable ai (xai) is rising to ensure model interpretability and support regulatory validation for applications like predictive toxicology, which is critical for de-risking development.

What are the Key Data Covered in this AI For Scientific Discovery Market Research and Growth Report?

-

What is the expected growth of the AI For Scientific Discovery Market between 2025 and 2029?

-

USD 4.41 billion, at a CAGR of 19%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Target discovery, De novo molecule design, Biomarker and omics analysis, Predictive toxicology), Technology (Generative models, Graph and molecular ML, Physics-informed ML, Simulation and digital twins), End-user (Pharmaceutical research and development, Biotechnology companies, Academic and national labs, Chemical and materials science firms) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of high-volume scientific data and advanced computational infrastructure, Data Scarcity, quality, and interoperability

-

-

Who are the major players in the AI For Scientific Discovery Market?

-

AbCellera Biologics Inc., Amazon Web Services Inc., Atomwise Inc., Benchling Inc., BenchSci Analytics Inc., BenevolentAI, Evaxion AS, Generate Biomedicines, Google LLC, Healx Ltd., IBM Corp., Insilico Medicine, Microsoft Corp., Nimbus Therapeutics, Novartis AG, NVIDIA Corp., Recursion Pharmaceuticals Inc. and Schrodinger Inc.

-

Market Research Insights

- Market dynamics are increasingly shaped by the adoption of specialized AI platforms for drug discovery and advances in machine learning in materials science. These technologies facilitate accelerated discovery cycles and enable new frontiers in ai in personalized medicine.

- The integration of generative AI for protein design has led to a 30% increase in the identification of novel therapeutic candidates compared to traditional screening methods. Similarly, the use of deep learning for genomics is enhancing in silico drug repurposing efforts and aiding ai for rare disease research.

- This progress is underpinned by a robust computational infrastructure for ai, which is essential for processing large datasets. The effectiveness of these systems is evident in performance metrics, with some platforms achieving a 40% reduction in preclinical analysis timelines, thereby improving research ROI.

We can help! Our analysts can customize this ai for scientific discovery market research report to meet your requirements.

RIA -

RIA -