AI For Security Compliance Market Size 2025-2029

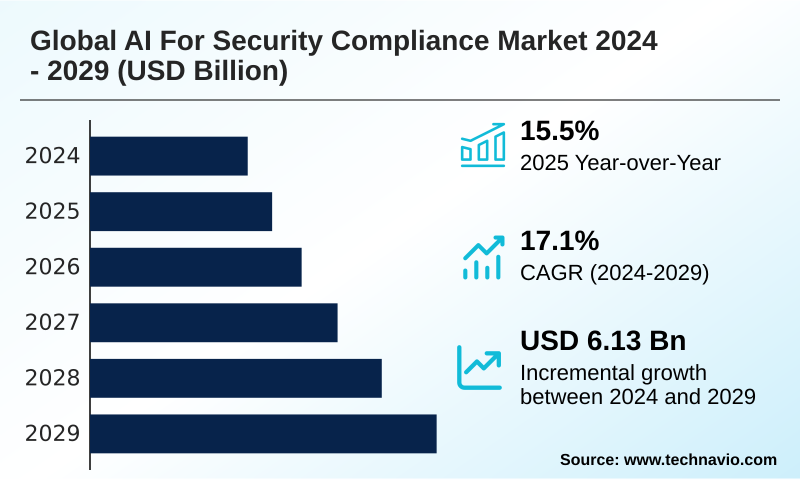

The ai for security compliance market size is valued to increase by USD 6.13 billion, at a CAGR of 17.1% from 2024 to 2029. Rising regulatory complexity and global compliance mandates will drive the ai for security compliance market.

Major Market Trends & Insights

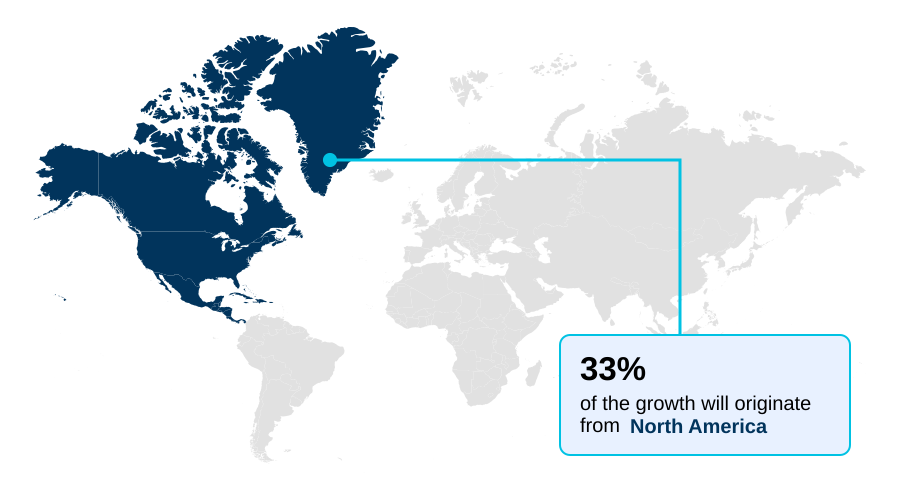

- North America dominated the market and accounted for a 32.6% growth during the forecast period.

- CAGR from 2024 to 2029 : 17.1%

Market Summary

- The AI for security compliance market is fundamentally reshaping how organizations manage regulatory adherence and cybersecurity. Enterprises are moving beyond manual checks, adopting AI-driven systems for continuous compliance and robust data governance. These platforms leverage natural language processing to interpret evolving legal texts and employ machine learning models for predictive compliance analytics, identifying potential violations before they occur.

- For instance, a financial institution can deploy an AI solution for automated security audits, using behavioral analytics to monitor transactions for AML and KYC compliance, thereby improving detection accuracy by over 30% while ensuring complete, real-time audit trails.

- This shift toward intelligent, proactive frameworks like zero-trust architecture is driven by the need for greater precision in a landscape of increasing threats. The adoption of AI copilot for security and AI-powered risk assessment tools is becoming standard as businesses seek to fortify their security posture and automate security incident response effectively.

- Ultimately, these technologies enable a more resilient and efficient approach to navigating complex compliance demands.

What will be the Size of the AI For Security Compliance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI For Security Compliance Market Segmented?

The ai for security compliance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029.

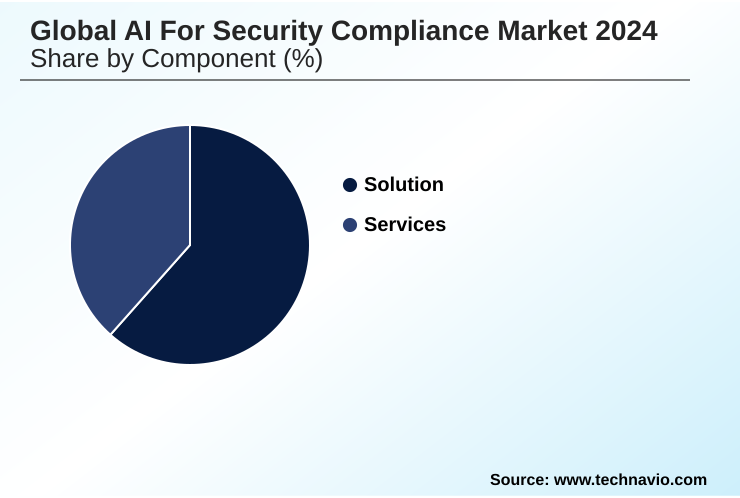

- Component

- Solution

- Services

- Business segment

- Large enterprises

- Small and medium enterprises

- End-user

- BFSI

- Government and public utilities

- IT and telecom

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- Japan

- South Korea

- China

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The solution segment is estimated to witness significant growth during the forecast period.

The market's solution segment provides software platforms essential for navigating complex regulatory landscapes. These tools facilitate compliance automation through a policy enforcement engine and provide real-time audit trails for verification.

Organizations are leveraging AI for HIPAA compliance and AI for GDPR compliance, with nearly 40% of enterprise users utilizing these systems for automated data classification.

Key functionalities include a risk scoring engine and policy-as-code frameworks that enable proactive risk management and automated policy validation.

This intelligent compliance platform integrates machine learning models and offers AI-driven GRC capabilities, streamlining operations and ensuring adherence to standards like PCI-DSS through AI for pci-dss compliance.

Regional Analysis

North America is estimated to contribute 32.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI For Security Compliance Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for 32.6% of the market's incremental growth, driven by advanced regulatory frameworks and high enterprise adoption of compliance monitoring tools.

In this region, 69% of firms now consider AI essential for cybersecurity, utilizing AI-driven threat detection for insider threat detection and automated evidence collection.

Europe is a close second, with its stringent EU AI Act mandating high standards for AI in internal controls and data loss prevention. This has accelerated the adoption of AI for data privacy and data residency management.

Both regions are pioneering the use of AI-based auditing and ai-powered audit techniques, setting global benchmarks for responsible and effective regulatory technology.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly adopting specialized AI solutions to address nuanced compliance challenges across various sectors. The use of AI for security compliance in financial services is now standard practice, with platforms focused on predictive compliance for anti-money laundering and real-time fraud detection.

- In parallel, healthcare organizations are leveraging AI-driven policy enforcement in healthcare to protect patient data and manage regulatory adherence. A critical development is automating GDPR compliance with machine learning, which allows for dynamic consent management and data processing verification, showing efficiency gains of over 50% in audit preparation compared to manual methods.

- The push for transparency is being met by using explainable AI for audit trail generation, which provides clear, defensible logs for regulators. In cloud-native organizations, continuous compliance monitoring for cloud environments and SaaS compliance automation for remote workforces have become essential. These systems rely on AI-powered risk scoring for cybersecurity threats to prioritize alerts and automate remediation of compliance violations.

- The application of natural language processing for regulatory text analysis helps legal teams stay current, while identity governance and access management with AI strengthens security perimeters. Furthermore, generative AI governance for enterprise data and tools for mitigating LLM risks with AI governance tools are emerging to address new threat vectors.

- This comprehensive approach, encompassing everything from AI-powered data classification for privacy protection to integrating threat intelligence with compliance AI, defines the modern GRC strategy.

What are the key market drivers leading to the rise in the adoption of AI For Security Compliance Industry?

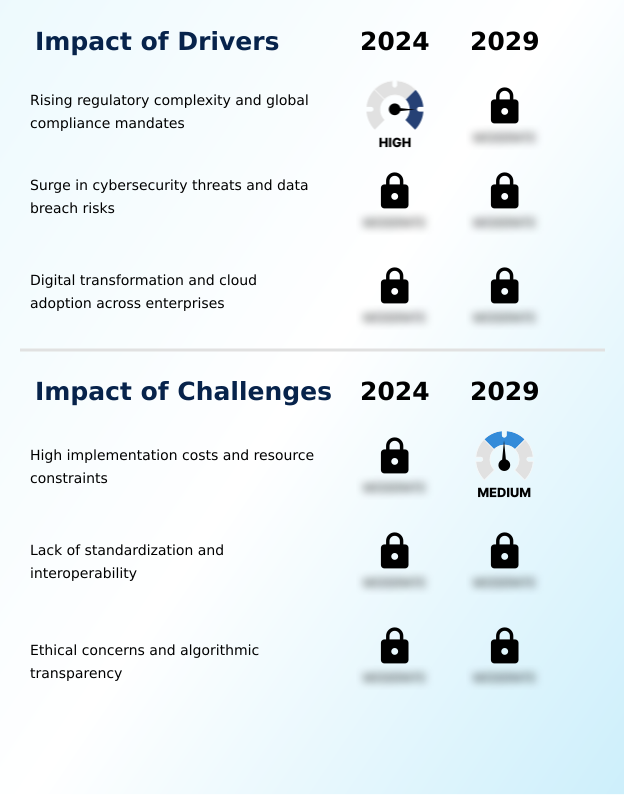

- The market is significantly driven by the escalating complexity of regulations and the growing number of global compliance mandates.

- Market growth is fueled by escalating regulatory complexity and a heightened threat landscape. With cybercrime increasing by over 50% in recent years, organizations are compelled to adopt AI-driven GRC frameworks for robust security incident response and proactive risk management.

- Digital transformation is another primary catalyst, as migration to cloud platforms multiplies compliance exposure, making manual oversight untenable. AI-powered risk assessment and compliance reporting automation are essential for managing this complexity.

- Consequently, 69% of firms now view AI as critical for maintaining their cybersecurity posture and achieving regulatory change management.

- This has spurred demand for solutions that provide compliance as a service, featuring capabilities like regulatory text analysis and AI-based forensics, to ensure resilience and operational integrity.

What are the market trends shaping the AI For Security Compliance Industry?

- The increasing demand for transparency in automated decision-making is a primary factor driving the rise of explainable AI (XAI). This trend is becoming critical within compliance workflows.

- Key market trends are centered on enhancing transparency, integration, and real-time oversight. The rise of explainable AI is driven by regulatory demands for clear justifications, with over 70% of enterprises expected to require model transparency for compliance workflows. This push for algorithmic transparency and AI bias detection is reshaping product development.

- Simultaneously, the integration of intelligent compliance platform tools with cloud security platforms is creating a unified approach to governance, enabling automated security audits and security policy automation across hybrid environments. This trend supports continuous compliance monitoring for cloud environments and AI-enhanced SIEM capabilities.

- Firms adopting these integrated systems report up to a 50% reduction in mean time to resolution for compliance-related incidents, underscoring the shift toward proactive, embedded governance with automated compliance monitoring.

What challenges does the AI For Security Compliance Industry face during its growth?

- Industry growth is notably constrained by high implementation costs and significant resource limitations, particularly for smaller enterprises.

- Significant market challenges hinder widespread adoption, primarily high implementation costs and a lack of standardization. The initial investment in AI infrastructure is prohibitive for many, with fewer than 30% of small to medium-sized enterprises able to deploy advanced AI-powered systems. The fragmented ecosystem lacks interoperability, making AI model governance and cloud security posture management difficult to unify across different platforms.

- Furthermore, ethical concerns surrounding black-box algorithms persist, as over 60% of current models lack full transparency, complicating compliance orchestration and regulatory technology integration. This opacity poses legal risks and slows trust-building, requiring a greater focus on developing standardized, ethical AI in compliance and LLM risk management solutions that are accessible to a broader market.

Exclusive Technavio Analysis on Customer Landscape

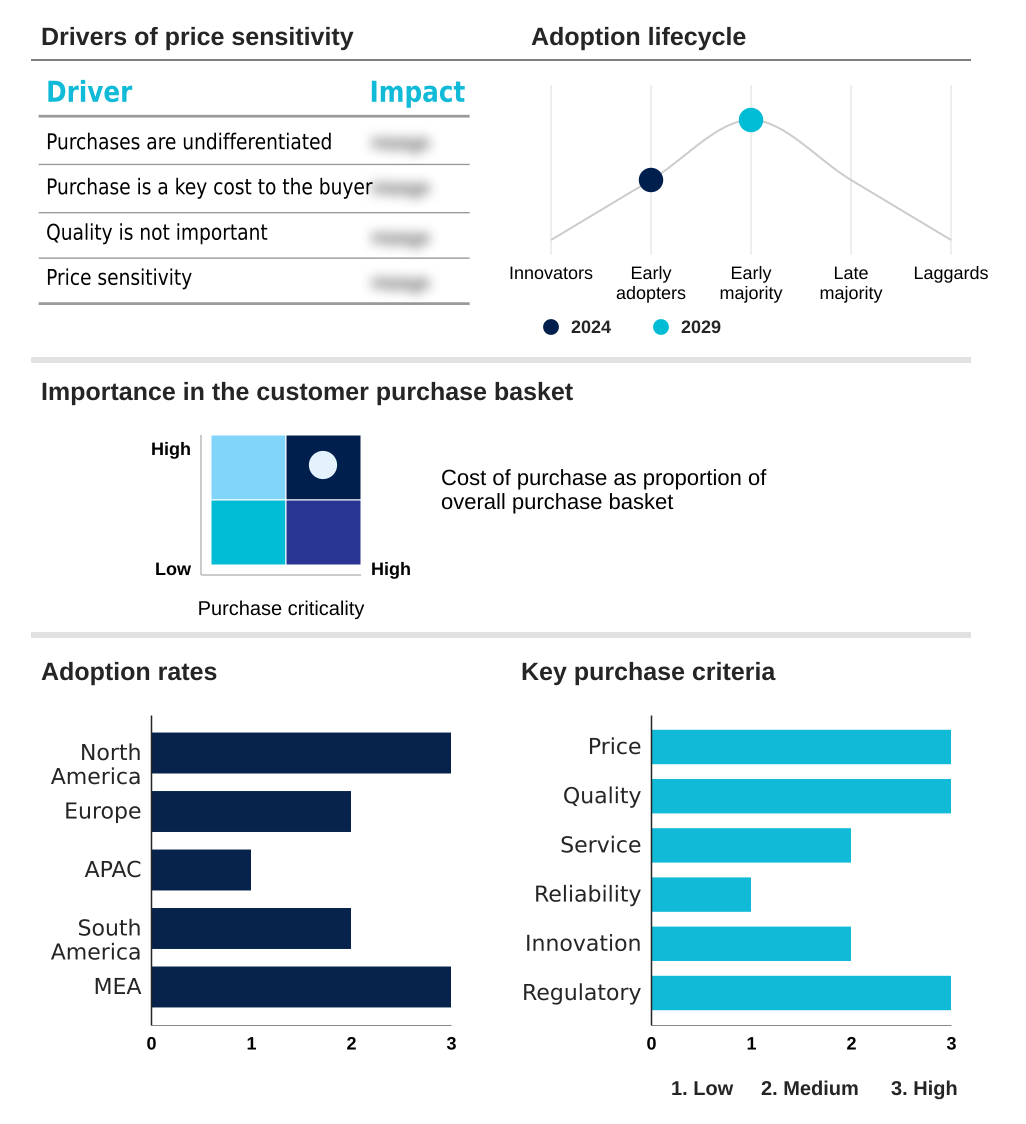

The ai for security compliance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai for security compliance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI For Security Compliance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai for security compliance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offerings include AI-driven solutions for advanced threat detection and streamlined compliance orchestration, enhancing security posture across enterprise environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Arctic Wolf Networks Inc.

- S.C. BITDEFENDER S.R.L.

- Check Point Software Tech Ltd.

- Cisco Systems Inc.

- CrowdStrike Inc.

- CyberArk Software Ltd.

- Fortinet Inc.

- Google LLC

- IBM Corp.

- Microsoft Corp.

- Okta Inc.

- Palo Alto Networks Inc.

- Qualys Inc.

- Sentinelone Inc.

- Trend Micro Inc.

- Trust Arc Inc.

- Zscaler Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai for security compliance market

- In August 2024, Atos and Ooredoo launched an AI-powered cybersecurity framework designed for Qatar's TASMU Smart City initiative, integrating intelligent threat detection and compliance analytics.

- In February 2025, Banorte initiated an AI-powered compliance engine to monitor financial transactions, using deep learning to detect behavioral anomalies aligned with anti-money laundering standards.

- In April 2025, MedStack introduced an AI-powered audit engine for healthcare providers, which cross-references patient data with privacy regulations in real-time to improve compliance accuracy.

- In July 2025, Lleverage launched a compliance orchestration platform incorporating risk scoring and data lineage tracking, tailored to meet both GDPR and EU AI Act requirements for fintech firms.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI For Security Compliance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 283 |

| Base year | 2024 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.1% |

| Market growth 2025-2029 | USD 6127.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 15.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Japan, South Korea, China, India, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market has reached a critical inflection point where AI is no longer a peripheral tool but the core engine of modern governance, risk, and compliance frameworks. Boardroom decisions are now centered on deploying systems that offer not just compliance automation but also strategic foresight through predictive compliance analytics.

- The integration of natural language processing for regulatory mapping and machine learning models for anomaly detection has become standard. Advanced capabilities like generative AI governance, AI security posture management, and automated remediation are defining competitive differentiation.

- We are seeing a decisive shift toward platforms offering continuous compliance and a robust risk scoring engine, enabling organizations to move from a reactive to a proactive stance. These systems facilitate real-time control validation and vulnerability management. Explainable AI is now a key purchasing criterion, as organizations must justify automated decisions to auditors and regulators.

- Systems that embed a zero-trust architecture and strong data sovereignty controls are gaining traction, with some firms reporting a 40% reduction in false-positive alerts, directly improving security operations efficiency. This evolution underscores a strategic pivot toward holistic, AI-driven resilience.

What are the Key Data Covered in this AI For Security Compliance Market Research and Growth Report?

-

What is the expected growth of the AI For Security Compliance Market between 2025 and 2029?

-

USD 6.13 billion, at a CAGR of 17.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solution, Services), Business Segment (Large enterprises, Small and medium enterprises), End-user (BFSI, Government and public utilities, IT and telecom, Healthcare, Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising regulatory complexity and global compliance mandates, High implementation costs and resource constraints

-

-

Who are the major players in the AI For Security Compliance Market?

-

Amazon Web Services Inc., Arctic Wolf Networks Inc., S.C. BITDEFENDER S.R.L., Check Point Software Tech Ltd., Cisco Systems Inc., CrowdStrike Inc., CyberArk Software Ltd., Fortinet Inc., Google LLC, IBM Corp., Microsoft Corp., Okta Inc., Palo Alto Networks Inc., Qualys Inc., Sentinelone Inc., Trend Micro Inc., Trust Arc Inc. and Zscaler Inc.

-

Market Research Insights

- The market is defined by a shift toward proactive, intelligent compliance frameworks. Enterprises are adopting AI in regulatory technology to automate complex processes, with firms leveraging AI for data privacy seeing up to a 60% improvement in response times to data subject requests.

- The integration of AI for financial compliance is critical, where AI-enhanced SIEM systems and AI-based forensics are reducing investigation times by more than 40%. The demand for algorithmic transparency and AI bias detection is shaping vendor offerings, pushing for more ethical AI in compliance.

- As organizations adopt cloud compliance automation and DevSecOps integration, the focus on digital risk protection and AI model governance is intensifying, establishing a new standard for operational resilience.

We can help! Our analysts can customize this ai for security compliance market research report to meet your requirements.

RIA -

RIA -