AI In Geospatial Technology Market Size 2025-2029

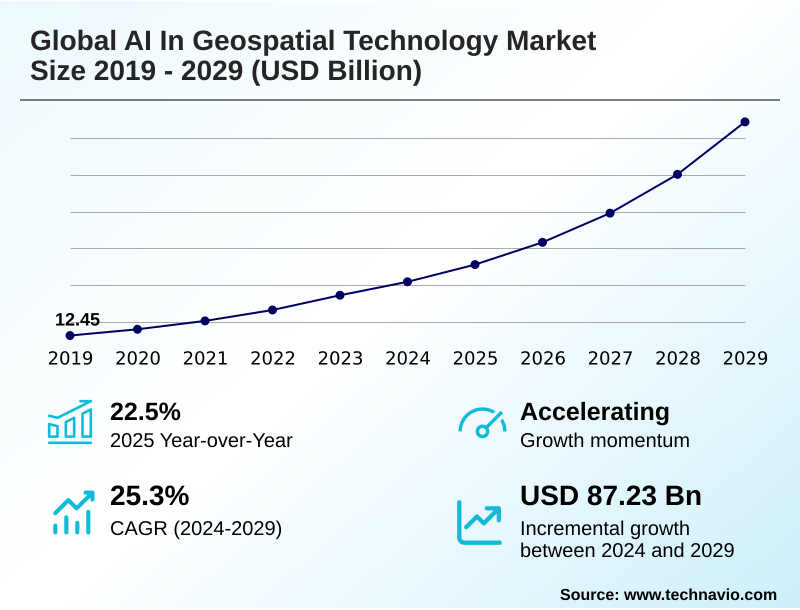

The ai in geospatial technology market size is valued to increase by USD 87.23 billion, at a CAGR of 25.3% from 2024 to 2029. Exponential proliferation of geospatial data sources will drive the ai in geospatial technology market.

Major Market Trends & Insights

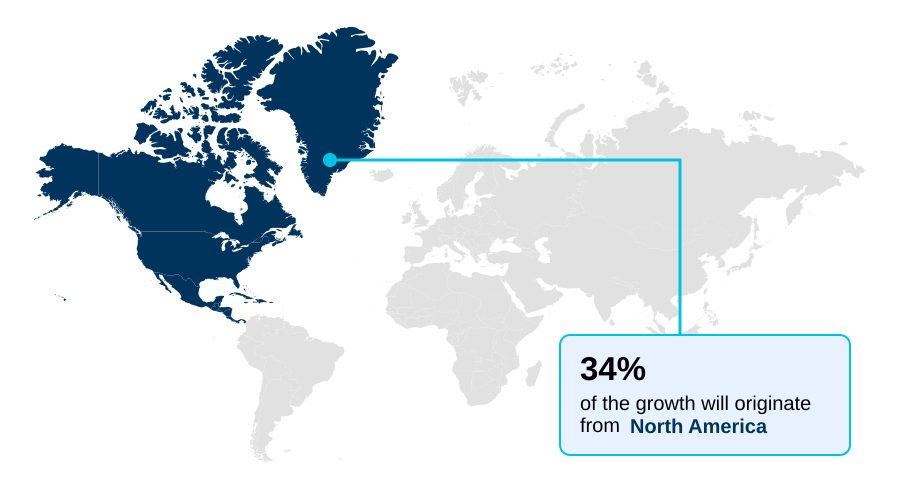

- North America dominated the market and accounted for a 33.5% growth during the forecast period.

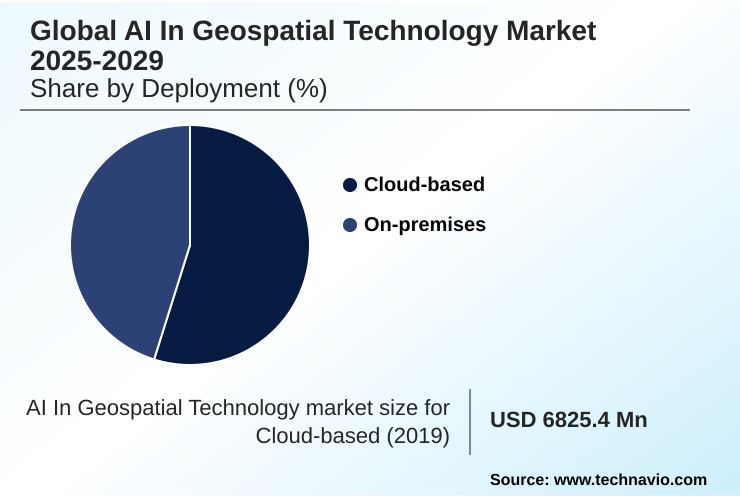

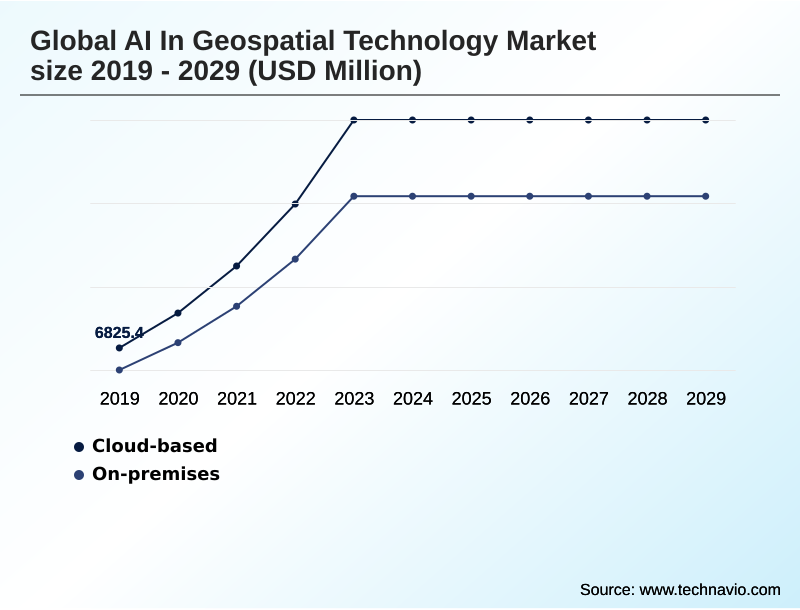

- By Deployment - Cloud-based segment was valued at USD 19.29 billion in 2023

- By End-user - Government and defense segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 116.53 billion

- Market Future Opportunities: USD 87.23 billion

- CAGR from 2024 to 2029 : 25.3%

Market Summary

- The AI In Geospatial Technology Market is defined by the integration of artificial intelligence with spatial data to automate and scale analysis. This convergence is driven by the deluge of data from satellites and sensors, which necessitates advanced processing capabilities beyond manual interpretation.

- Key trends include the rise of geospatial foundation models and AI-powered digital twins, which allow for complex simulations and predictive insights. For instance, a logistics firm can leverage AI to analyze real-time traffic and weather data, optimizing fleet-wide routing to enhance supply chain efficiency and reduce operational costs.

- However, the market's potential is tempered by challenges such as the need for vast quantities of high-quality, labeled training data and a persistent shortage of professionals with the hybrid expertise required to develop and deploy these sophisticated systems. Addressing these issues is critical for unlocking the full value of GeoAI across industries.

What will be the Size of the AI In Geospatial Technology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Geospatial Technology Market Segmented?

The ai in geospatial technology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- End-user

- Government and defense

- Transportation and logistics

- Natural resources

- Utilities

- Others

- Technology

- Machine learning

- Computer vision

- Deep learning

- Natural language processing

- Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The market is heavily segmented by deployment, with the cloud-based model dominating due to its scalability and cost-efficiency. This approach provides access to powerful cloud computing infrastructure and high-performance computing resources, essential for running complex deep learning architectures.

Vendors are increasingly offering platform-as-a-service (PaaS) solutions that embed pre-trained models, allowing organizations to leverage advanced analytics without significant upfront investment in AI accelerators. The rise of low-code/no-code GeoAI platforms is further democratizing access.

This shift is enabling firms to improve analytical workflows through efficient MLOps for geospatial pipelines, which integrate diverse inputs via sensor data fusion and often utilize a flexible hybrid cloud deployment strategy to balance security and scalability, leading to a 40% faster model deployment cycle.

The Cloud-based segment was valued at USD 19.29 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Geospatial Technology Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for over 33% of incremental growth due to strong government and commercial investment.

This region is a hub for developing technologies like automated feature extraction from synthetic aperture radar (SAR) and LiDAR data analysis.

In contrast, APAC is the fastest-growing region, with a CAGR of 25.8%, driven by smart city initiatives and agricultural technology. In Europe, the focus is on environmental monitoring, using advanced raster data analysis and semantic segmentation.

Applications vary regionally, from property risk assessment in mature markets to agricultural monitoring in emerging ones. The adoption of edge computing for GeoAI is a growing trend globally, enabling localized processing and point cloud classification for real-time applications.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The practical application of AI in geospatial technology is expanding, driven by specific, high-value use cases. The use of AI for satellite imagery analysis has become fundamental for large-scale environmental monitoring and commercial intelligence. In urban environments, generative AI in urban planning allows for the simulation of development scenarios with unprecedented detail.

- The core technology often involves deep learning for feature extraction from complex imagery, while machine learning for predictive mapping helps forecast trends like land use change. For asset identification, computer vision for object detection is critical, and natural language processing for geocoding transforms unstructured text into mappable data points.

- Specific applications include AI-driven change detection in forestry to combat illegal logging and geospatial AI for supply chain optimization, which has been shown to improve delivery time predictability by double-digit percentages compared to legacy systems. Other key use cases are automated 3D model generation from LiDAR and real-time traffic flow prediction with AI.

- The concept of an AI-powered digital twin for infrastructure enables predictive maintenance for utility networks. Advanced analytics of hyperspectral data analysis with AI unlocks new insights, while AI models for property risk assessment are reshaping the insurance industry. Furthermore, using AI for precision agriculture insights is boosting yields. During crises, GeoAI for disaster damage assessment accelerates response times.

- All these applications rely on cloud platforms for scalable GeoAI processing. Firms are also focused on mitigating algorithmic bias in GeoAI and addressing ethical considerations in geospatial surveillance, while managing the substantial training data requirements for GeoAI models.

What are the key market drivers leading to the rise in the adoption of AI In Geospatial Technology Industry?

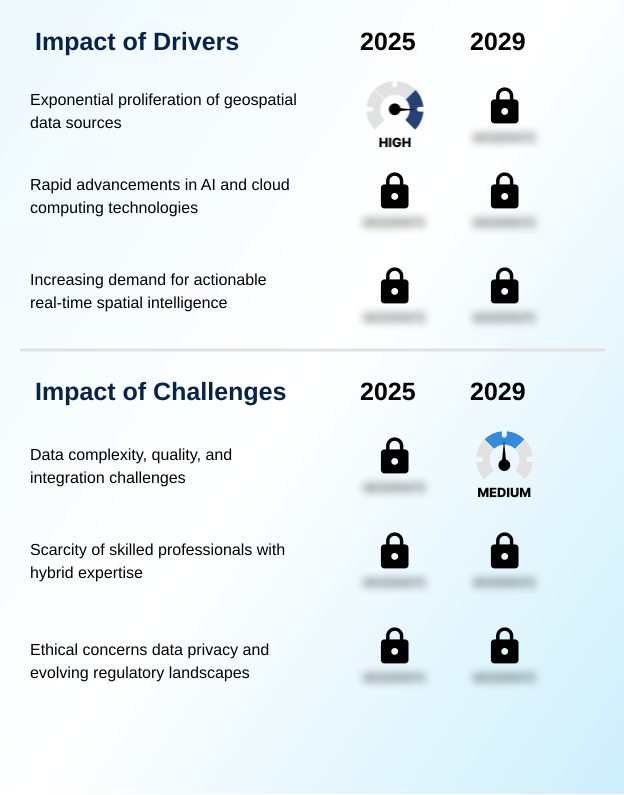

- The exponential proliferation of geospatial data from a multitude of sources is a primary driver fueling market demand for advanced AI-powered analytical solutions.

- Market growth is driven by an escalating demand for actionable real-time intelligence that informs strategic, data-driven decision-making. End-users require sophisticated predictive intelligence and real-time situational awareness, which are delivered by advanced machine learning models.

- These models process vast inputs, including hyperspectral satellite data, to power applications like precision farming optimization, where analysis improves crop yield forecasts by up to 25%. In logistics, enhanced supply chain visibility cuts shipping delays by 15%.

- Even unstructured data is being harnessed through natural language processing (NLP) to generate insights.

- The need to transform raw data into valuable intelligence is also critical in the utilities sector, where AI-driven vegetation management analytics automates risk assessment for critical infrastructure.

What are the market trends shaping the AI In Geospatial Technology Industry?

- The emergence of geospatial foundation models and the application of generative AI represent a paradigm-shifting market trend. This evolution is redefining how users interact with and derive insights from complex spatial data.

- A key trend reshaping the market is the rise of geospatial foundation models, large-scale systems that understand complex spatiotemporal patterns. This has enabled the development of conversational GIS and other applications of generative AI for geospatial analysis, where large language models allow users to query data naturally.

- These technologies are foundational to creating AI-powered digital twins, which provide predictive and prescriptive insights for use cases like proactive infrastructure monitoring, improving risk detection by over 30%. The output of these systems, often in the form of detailed 3D vector map generation, is refined through human-in-the-loop validation to ensure accuracy.

- This trend is moving the industry beyond simple data visualization to dynamic, predictive modeling environments, increasing analytical capabilities for urban planners by 50%.

What challenges does the AI In Geospatial Technology Industry face during its growth?

- Significant challenges related to data complexity, inconsistent quality, and the difficulties of integration are constraining the industry's growth trajectory.

- Despite advancements, significant challenges persist, particularly around data quality and ethics. The efficacy of sophisticated neural network architectures used for tasks like automated target recognition and anomaly detection depends heavily on extensive, high-quality training data. The process of ground truth data creation is a major bottleneck, increasing project costs by up to 40%.

- Furthermore, as computer vision algorithms and change detection algorithms become more powerful, concerns over algorithmic bias mitigation are growing. Organizations must now navigate a complex ethical landscape, adhering to responsible AI principles and strict data sovereignty compliance rules.

- The forthcoming EU AI Act implications will add another layer of regulatory complexity, with non-compliance risks driving up operational oversight costs by an estimated 20% for high-risk applications.

Exclusive Technavio Analysis on Customer Landscape

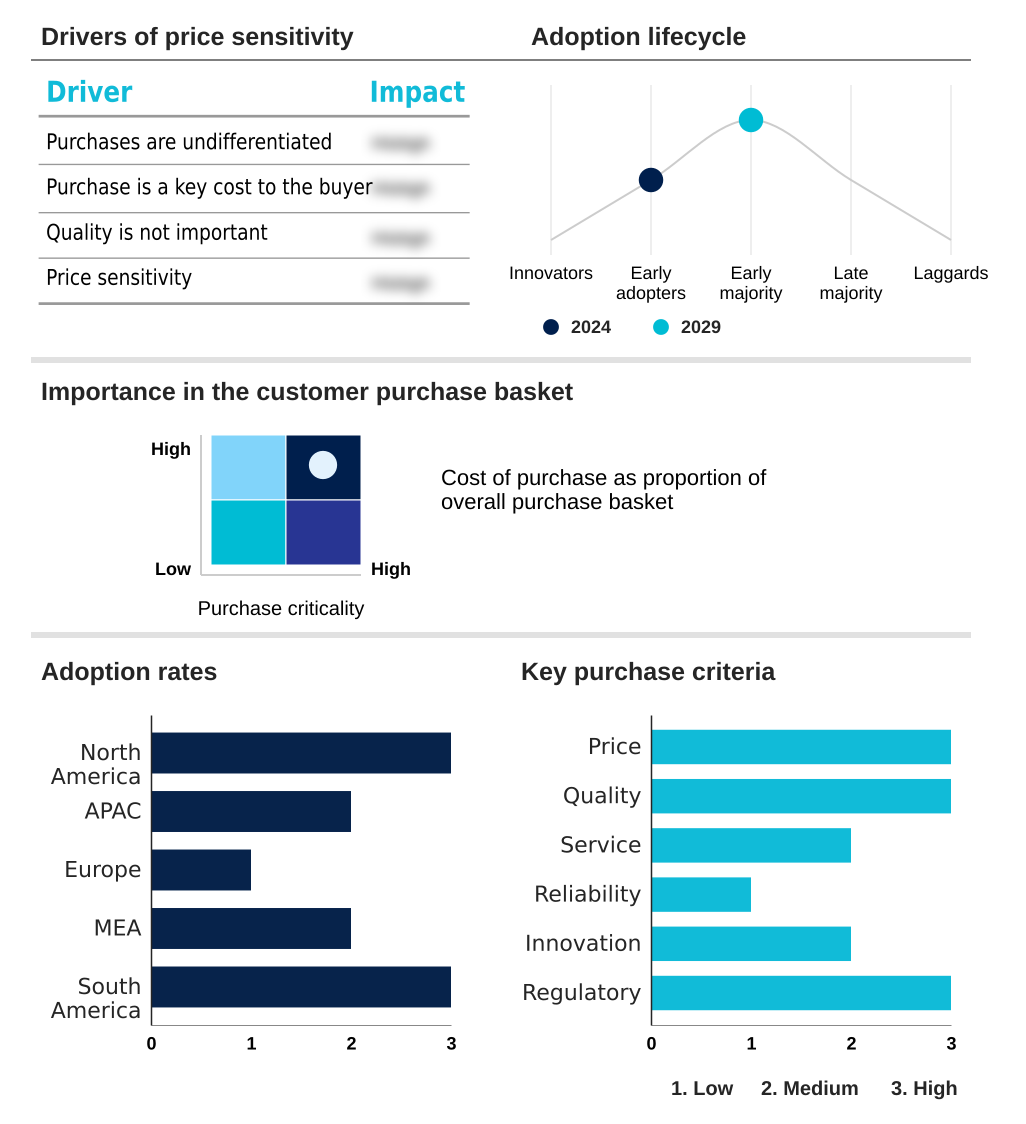

The ai in geospatial technology market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in geospatial technology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Geospatial Technology Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in geospatial technology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Vendors deliver AI-powered geospatial analytics platforms, converting raw satellite and sensor data into predictive intelligence essential for strategic enterprise decisions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Blackshark.ai GmbH

- CAPE Analytics

- CartoDB Inc.

- DroneDeploy Inc.

- EarthDaily Analytics

- Ecopia Tech Corp.

- Esri Global Inc.

- Google LLC

- Hexagon AB

- ICEYE Oy

- Mapbox Inc.

- Maxar Technologies Inc.

- Microsoft Corp.

- Orbital Insight Inc.

- Pixxel Space Technologies Inc.

- Planet Labs PBC

- Satellogic SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in geospatial technology market

- In August 2024, CartoDB Inc. launched its AI Agents in private preview, a feature designed to enable users to interact with complex spatial data using natural language queries.

- In September 2024, CAPE Analytics partnered with Vexcel to expand its high-resolution aerial imagery coverage, enhancing its AI-driven property intelligence for the insurance sector.

- In November 2024, Amazon Web Services and the Taylor Geospatial Institute announced the Generative AI for Geospatial Challenge, providing cloud credits to foster novel application development.

- In January 2025, Mapbox Inc. introduced MapGPT, an AI-powered conversational assistant integrated into its Navigation SDK, to create more intuitive in-vehicle mapping experiences.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Geospatial Technology Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 270 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.3% |

| Market growth 2025-2029 | USD 87225.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 22.5% |

| Key countries | US, Canada, China, India, Japan, South Korea, Australia, Germany, UK, France, Saudi Arabia, UAE, Brazil and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI In Geospatial Technology market is advancing beyond traditional GIS, driven by the operationalization of sophisticated machine learning models and neural network architectures. The development of geospatial foundation models, coupled with accessible cloud computing infrastructure, is creating new commercial opportunities.

- Boardroom decisions are increasingly influenced by the potential of predictive intelligence and real-time situational awareness to de-risk operations and identify new revenue streams. The adoption of computer vision algorithms for automated feature extraction from LiDAR data analysis and hyperspectral satellite data is now standard practice, with firms reporting a reduction in manual data processing times by over 60%.

- This shift enables a focus on high-value tasks like anomaly detection and change detection algorithms. However, leveraging technologies like conversational GIS and AI-powered digital twins requires significant investment in high-performance computing, AI accelerators, and the development of pre-trained models.

- Successfully navigating this landscape depends on a firm's ability to integrate everything from large language models and natural language processing (NLP) to synthetic aperture radar (SAR) and automated target recognition into a cohesive strategy.

What are the Key Data Covered in this AI In Geospatial Technology Market Research and Growth Report?

-

What is the expected growth of the AI In Geospatial Technology Market between 2025 and 2029?

-

USD 87.23 billion, at a CAGR of 25.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises), End-user (Government and defense, Transportation and logistics, Natural resources, Utilities, Others), Technology (Machine learning, Computer vision, Deep learning, Natural language processing) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Exponential proliferation of geospatial data sources, Data complexity, quality, and integration challenges

-

-

Who are the major players in the AI In Geospatial Technology Market?

-

Airbus SE, Blackshark.ai GmbH, CAPE Analytics, CartoDB Inc., DroneDeploy Inc., EarthDaily Analytics, Ecopia Tech Corp., Esri Global Inc., Google LLC, Hexagon AB, ICEYE Oy, Mapbox Inc., Maxar Technologies Inc., Microsoft Corp., Orbital Insight Inc., Pixxel Space Technologies Inc., Planet Labs PBC and Satellogic SA

-

Market Research Insights

- The market is being reshaped by the demand for actionable real-time intelligence, moving beyond static mapping to deliver predictive and prescriptive insights. This shift enables enhanced data-driven decision-making, with organizations achieving up to a 30% improvement in operational planning accuracy. The adoption of platform-as-a-service (PaaS) models and low-code/no-code GeoAI solutions is democratizing access, allowing non-specialists to perform complex analyses.

- These platforms are facilitating proactive infrastructure monitoring, which has been shown to reduce critical asset failures by 25%. As a result, companies are leveraging these tools to gain a competitive edge through superior supply chain visibility and optimized resource management.

We can help! Our analysts can customize this ai in geospatial technology market research report to meet your requirements.

RIA -

RIA -