AI In Mining Market Size 2025-2029

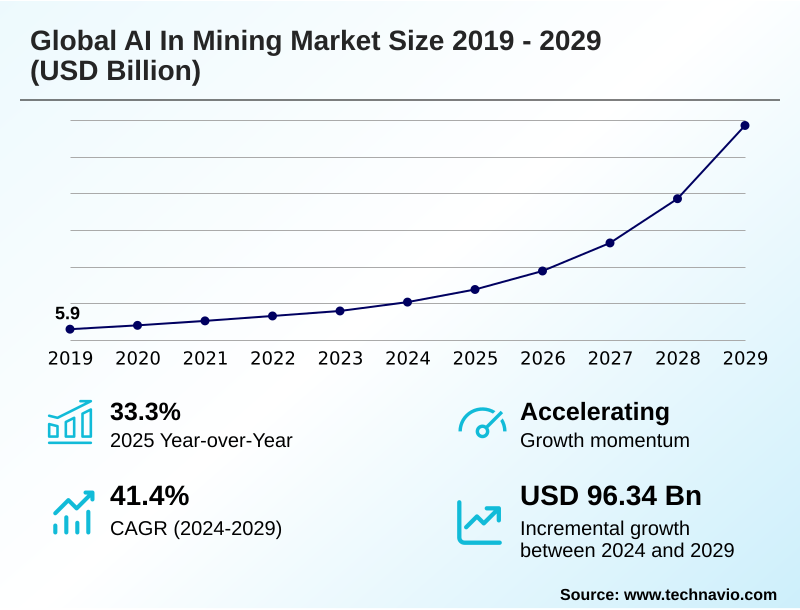

The ai in mining market size is valued to increase by USD 96.34 billion, at a CAGR of 41.4% from 2024 to 2029. Intensifying focus on worker safety and environmental, social and governance (ESG) compliance will drive the ai in mining market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.8% growth during the forecast period.

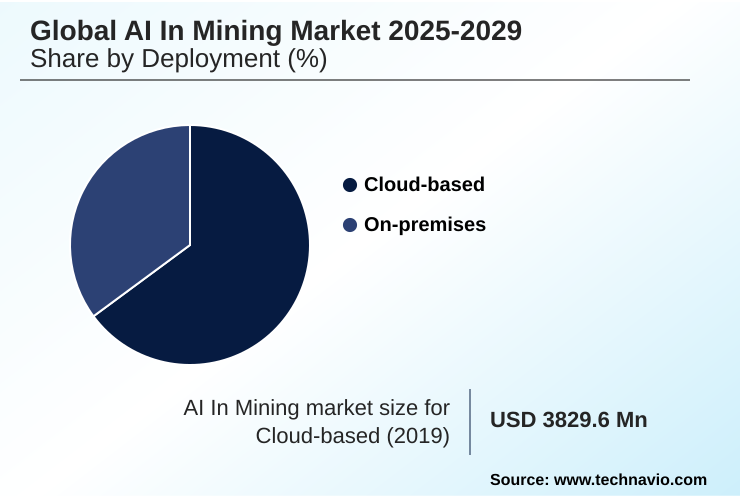

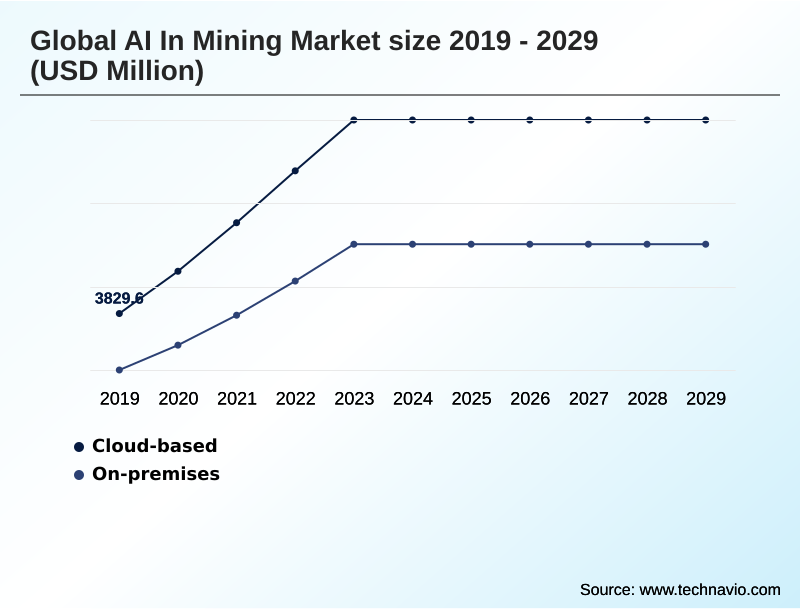

- By Deployment - Cloud-based segment was valued at USD 9.85 billion in 2023

- By Type - Surface mining segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 111.11 billion

- Market Future Opportunities: USD 96.34 billion

- CAGR from 2024 to 2029 : 41.4%

Market Summary

- The AI in mining market is undergoing a fundamental transformation, shifting from traditional operational methods to a data-centric model driven by intelligent technologies. This evolution is not merely about technological adoption but a strategic necessity to address persistent pressures for improved productivity, enhanced safety, and greater sustainability. Core applications span the entire mining lifecycle, from exploration to reclamation.

- For instance, companies are leveraging machine learning to analyze vast geological datasets, increasing the probability of discovering new, economically viable deposits. In operations, the deployment of autonomous haulage systems is becoming more widespread, removing personnel from hazardous environments and optimizing material transport around the clock.

- A key business scenario involves the use of predictive maintenance, where AI algorithms analyze real-time sensor data from critical machinery, such as haul trucks and crushers. By forecasting potential component failures, operators can move from a reactive to a proactive maintenance schedule, minimizing costly unplanned downtime and extending asset life, thereby directly impacting financial resilience and operational continuity.

- This shift toward prescriptive management, enabled by AI, is reshaping how mining enterprises create value and maintain their social license to operate.

What will be the Size of the AI In Mining Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Mining Market Segmented?

The ai in mining industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Type

- Surface mining

- Underground mining

- Technology

- ML and deep learning

- Robotics and automation

- Computer vision

- NLP

- Others

- Geography

- APAC

- China

- Australia

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- APAC

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud deployment model is reshaping the global AI in mining market by offering scalable computational power without significant upfront capital expenditure.

This approach is critical for processing vast datasets essential for advanced applications like AI-powered mineral exploration and comprehensive resource characterization.

Mining companies are leveraging cloud platforms to run complex simulations and train sophisticated models for energy consumption management and intelligent mine ventilation. The flexibility of the cloud enables dynamic adjustments to computational resources, ensuring cost-efficiency.

For instance, using cloud-based platforms for drone-based surveying data analysis has led to a reduction in survey processing times by over 40%.

The model also facilitates collaboration across geographically dispersed teams and supports emerging technologies like generative AI in mining and AI for tailings dam monitoring, enabling subsurface 3D mapping and more accurate predictive analytics.

The Cloud-based segment was valued at USD 9.85 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Mining Market Demand is Rising in APAC Get Free Sample

The geographic landscape for AI in mining is led by APAC, which is set to contribute nearly 39% of the market's incremental growth, driven by large-scale operations in Australia and modernization mandates in China.

In this region, real-time data analytics is fundamental for managing vast supply chain logistics.

North America follows, with a strong focus on optimizing existing mines in the United States and Canada, where advanced seismic event monitoring systems have reduced false alerts by over 40%.

The use of natural language processing (NLP) to analyze decades of geological reports is also gaining traction, accelerating resource discovery. Europe emphasizes sustainability and deep mining, using AI for blast fragmentation analysis to improve efficiency.

Across all regions, the goal is to achieve real-time operational control and smart mine transformation.

This is supported by predictive analytics deployment for resource management optimization and robotic process automation (RPA) for repetitive tasks, demonstrating a global shift towards integrated, intelligent operations.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The adoption of artificial intelligence in mining is advancing beyond pilot projects into core operational strategies, addressing specific, high-value challenges across the value chain. A primary hurdle is the AI integration with legacy mining systems, which requires significant investment in both technology and workforce training to overcome the AI skills gap in mining.

- In safety, computer vision for PPE compliance tracking is becoming standard, improving worker safety with AI monitoring. Operationally, the focus is on tangible returns, such as using fleet management AI for fuel consumption reduction.

- Predictive maintenance for haul truck fleets is now a critical application, with some operators reporting a reduction in unexpected failures that is more than double what was achievable with traditional preventative schedules. The application of machine learning for ore grade estimation is refining mine-to-mill efficiency.

- Operators are using digital twins for mine simulation to test new extraction methods, while autonomous drilling impact on blast outcomes is closely studied to improve downstream processing. Deeper insights are being unlocked through NLP for analyzing geological survey reports and AI-driven exploration for critical raw materials.

- Robotic systems for underground mine inspection are removing humans from hazardous areas, and AI algorithms for seismic hazard prediction enhance safety in deep mines. Optimizing mineral processing with AI, alongside AI applications in mine water management and optimizing ventilation on demand with AI, showcases AI's role in reducing mining's carbon footprint.

- The increased connectivity, however, raises cybersecurity challenges in connected mines, while drone technology for stockpile volume calculation and real-time data analytics for operational bottlenecks provide unprecedented visibility.

What are the key market drivers leading to the rise in the adoption of AI In Mining Industry?

- An intensifying focus on worker safety and environmental, social, and governance (ESG) compliance is a key driver of market growth.

- Market growth is primarily driven by the imperative for enhanced safety and productivity.

- The deployment of autonomous haulage systems and robotic drilling systems directly addresses this by removing personnel from hazardous environments, contributing to a documented 50% reduction in vehicle-related safety incidents at mature sites.

- Concurrently, the push for environmental footprint minimization is accelerating the adoption of intelligent systems like ventilation on demand, which can lower energy costs by up to 20%.

- The need for critical mineral discovery acceleration is another major driver, with AI-powered geological modeling and analysis platforms increasing the success rate of exploration campaigns.

- These technologies contribute to supply chain resilience and personnel safety monitoring, enabling an unplanned downtime reduction and an overall increase in the mineral recovery rate increase across the value chain.

What are the market trends shaping the AI In Mining Industry?

- The imperative for enhanced operational efficiency and cost reduction is a defining trend. This is driving the adoption of intelligent technologies across the mining value chain.

- Key trends in the AI in mining market are centered on achieving tangible operational efficiency enhancement and cost reduction strategies. The application of predictive maintenance using sophisticated machine learning models has become a cornerstone, with leading operators reporting up to a 40% decrease in critical equipment failures.

- This is complemented by the use of computer vision systems for real-time monitoring, which enhances worker safety improvement efforts. The creation of a digital twin for mining operations allows for holistic simulation and optimization, driving asset utilization maximization.

- Furthermore, advanced ore sorting technology is being deployed to improve mineral recovery, with some systems demonstrating a 10% increase in head grade before processing. These trends collectively support ESG compliance automation by optimizing resource use and minimizing waste, cementing data-driven intelligence as a competitive necessity.

What challenges does the AI In Mining Industry face during its growth?

- High initial capital expenditure and complex integration with legacy systems represent a key challenge affecting industry growth.

- Key challenges revolve around integration complexity and data management. The process of legacy system integration can be a significant hurdle, often requiring extensive capital and specialized expertise from workforce upskilling programs. Ensuring robust cybersecurity for OT systems is paramount, as a single breach could halt operations managed from a remote operations center.

- Effective mine planning optimization and process control optimization depend on high-quality, accessible data, which requires strong data governance frameworks. Even with advanced fleet management systems, achieving true data-driven decision making is difficult when data is siloed. Moreover, accurately predicting events like geotechnical instability prediction requires massive, clean datasets that are difficult to compile.

- Despite these challenges, the benefits are clear, with successful integrations showing a 15-20% improvement in process efficiency.

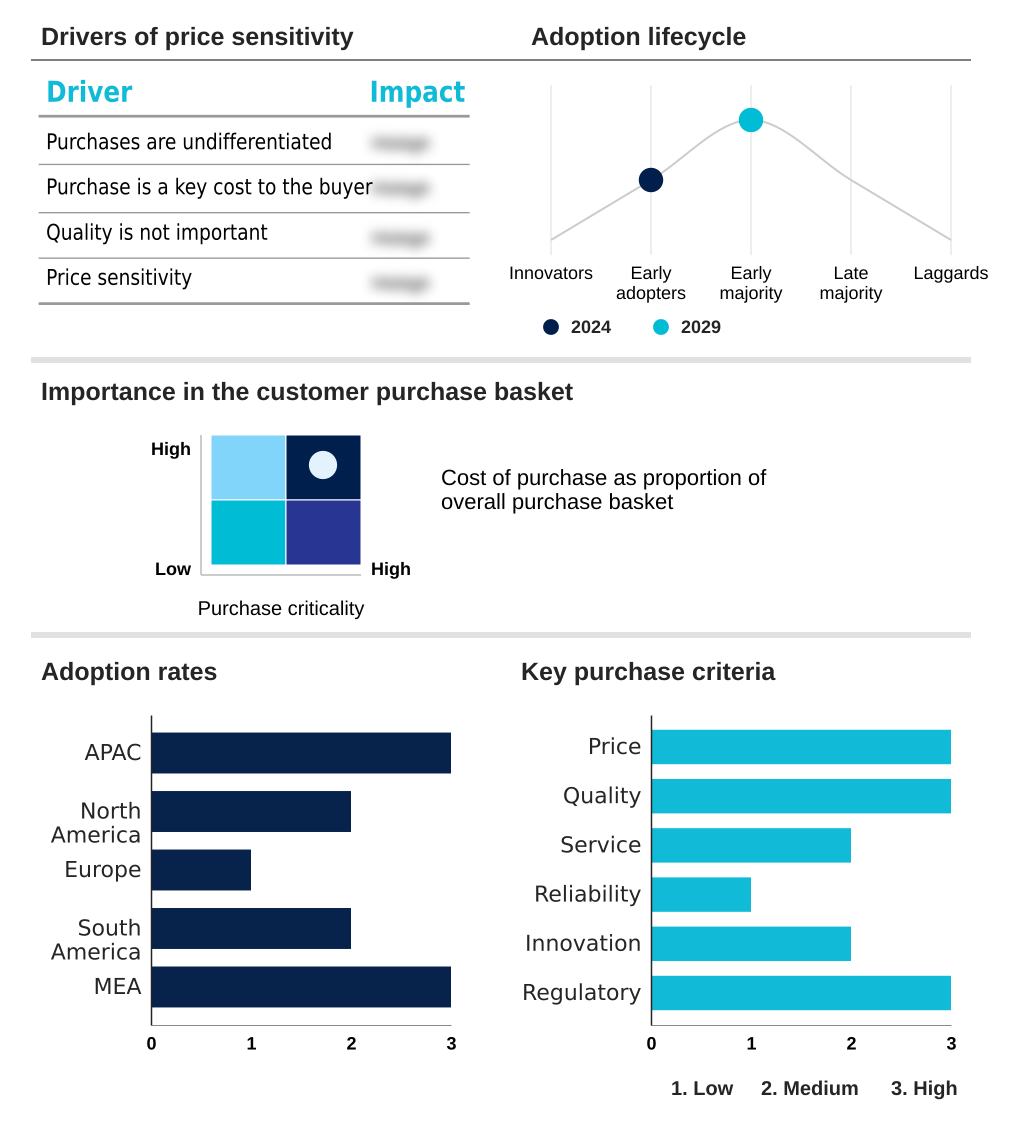

Exclusive Technavio Analysis on Customer Landscape

The ai in mining market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in mining market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Mining Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in mining market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Delivers industrial IoT solutions, leveraging predictive analytics and process optimization to enhance asset performance and operational intelligence across mining value chains.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Anglo American plc

- Barrick Gold Corp.

- BHP Group Ltd.

- Caterpillar Inc.

- FLSmidth and Co. AS

- Fortescue Metals Group Ltd.

- Glencore Plc

- IBM Corp.

- KoBold Metals

- Komatsu Ltd.

- Microsoft Corp.

- Newmont Corp.

- Rio Tinto Ltd.

- Sandvik AB

- SAP SE

- Teck Resources Ltd.

- The Weir Group Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in mining market

- In May, 2025, BHP Group Ltd. announced a new AI-driven initiative aimed at achieving a 15% reduction in Scope 1 emissions across its Western Australia Iron Ore operations by integrating autonomous fleet data with renewable energy grid management.

- In January, 2025, Epiroc announced the commercial rollout of its next-generation battery-electric vehicle fleet, which integrates advanced AI for predictive battery management and automated charging cycles to maximize uptime.

- In October, 2024, NVIDIA confirmed a strategic collaboration with several industrial software partners to deploy its Omniverse platform, creating physics-based digital twins of mine sites to simulate and optimize operational workflows.

- In August, 2024, EarthLabs Inc. reported the successful identification of new critical mineral deposits for a client using its proprietary AI exploration platform, validating the technology's ability to accelerate discovery timelines.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Mining Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 41.4% |

| Market growth 2025-2029 | USD 96343.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 33.3% |

| Key countries | China, Australia, India, Japan, South Korea, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in mining market is defined by a strategic pivot toward data-centric operations, where machine learning models and real-time data analytics are foundational. The deployment of autonomous haulage systems and robotic drilling systems is transitioning from niche applications to standard practice in large-scale operations, driven by the need to enhance safety and productivity.

- A critical focus area is predictive maintenance, which leverages sensor data to anticipate equipment failures, with some implementations achieving a 30% reduction in unplanned downtime for critical assets. The creation of a comprehensive digital twin of a mine allows for advanced mine planning optimization and geological modeling.

- This is complemented by technologies like computer vision for personnel safety monitoring and ore sorting technology for process control optimization. In underground environments, ventilation on demand systems managed by AI are improving safety and energy consumption management.

- The entire operation is often managed from a remote operations center, coordinating everything from fleet management systems and supply chain logistics to resource characterization. Advanced techniques like blast fragmentation analysis, seismic event monitoring, and drone-based surveying are being refined by AI, while natural language processing (NLP) unlocks insights from unstructured data, supporting AI-powered mineral exploration.

What are the Key Data Covered in this AI In Mining Market Research and Growth Report?

-

What is the expected growth of the AI In Mining Market between 2025 and 2029?

-

USD 96.34 billion, at a CAGR of 41.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), Type (Surface mining, and Underground mining), Technology (ML and deep learning, Robotics and automation, Computer vision, NLP, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Intensifying focus on worker safety and environmental, social and governance (ESG) compliance, High initial capital expenditure and complex integration

-

-

Who are the major players in the AI In Mining Market?

-

ABB Ltd., Anglo American plc, Barrick Gold Corp., BHP Group Ltd., Caterpillar Inc., FLSmidth and Co. AS, Fortescue Metals Group Ltd., Glencore Plc, IBM Corp., KoBold Metals, Komatsu Ltd., Microsoft Corp., Newmont Corp., Rio Tinto Ltd., Sandvik AB, SAP SE, Teck Resources Ltd. and The Weir Group Plc

-

Market Research Insights

- The AI in mining market is driven by a clear business case for operational efficiency enhancement and cost reduction strategies. Deployments focusing on asset utilization maximization through predictive analytics deployment have demonstrated an ability to achieve unplanned downtime reduction by over 25%.

- Concurrently, pressures for worker safety improvement and ESG compliance automation are fueling smart mine transformation projects, which include AI for tailings dam monitoring and intelligent mine ventilation. While legacy system integration and the need for robust data governance frameworks and workforce upskilling programs present challenges, the move toward data-driven decision making is irreversible.

- Firms that successfully implement real-time operational control report a mineral recovery rate increase of up to 15%. This trend is further supported by the need for critical mineral discovery acceleration, leveraging subsurface 3D mapping and generative AI in mining to strengthen supply chain resilience and environmental footprint minimization.

- Managing cybersecurity for OT systems remains a critical component of this evolution toward complete resource management optimization and robotic process automation (RPA).

We can help! Our analysts can customize this ai in mining market research report to meet your requirements.

RIA -

RIA -