AI In Procurement Market Size 2025-2029

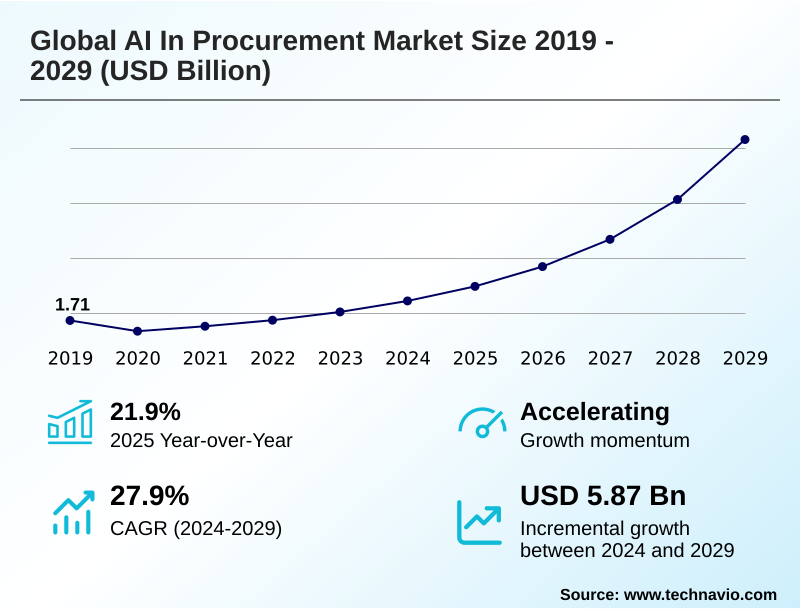

The ai in procurement market size is valued to increase by USD 5.87 billion, at a CAGR of 27.9% from 2024 to 2029. Enhanced decision making and operational efficiency will drive the ai in procurement market.

Major Market Trends & Insights

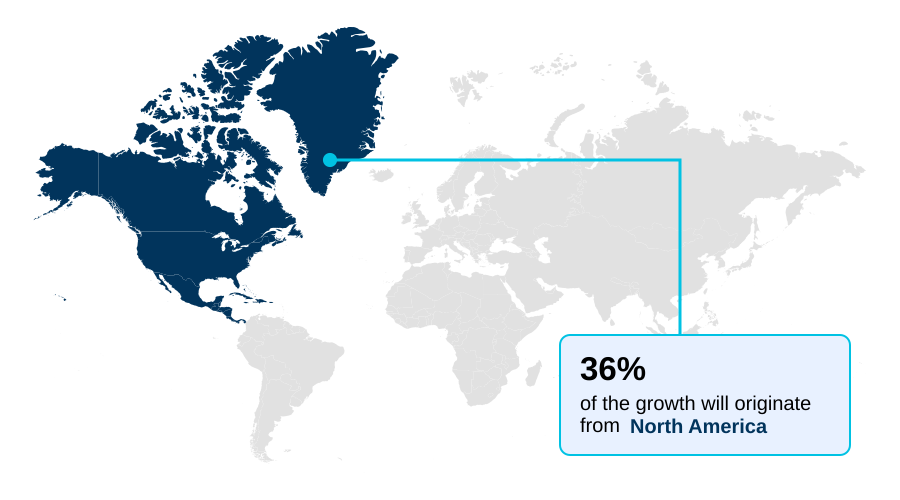

- North America dominated the market and accounted for a 35.9% growth during the forecast period.

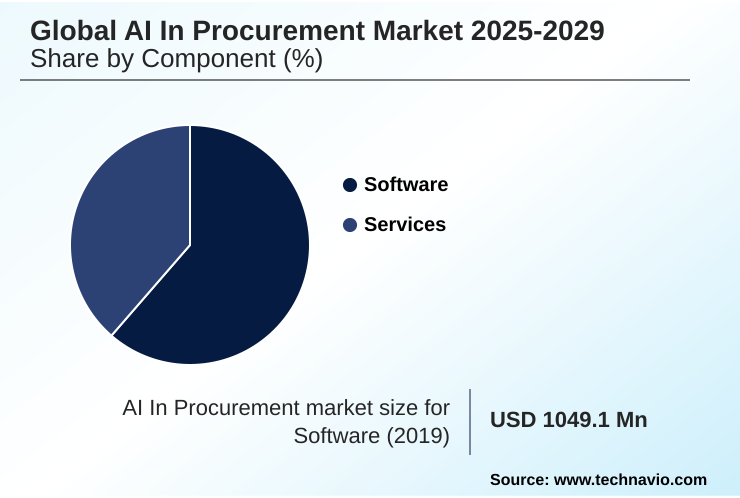

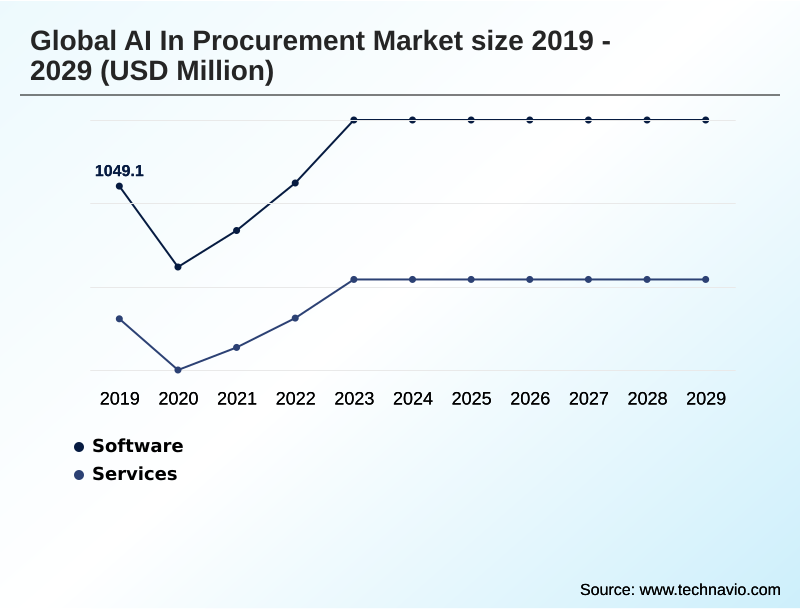

- By Component - Software segment was valued at USD 1.24 billion in 2023

- By End-user - Manufacturing segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 6.58 billion

- Market Future Opportunities: USD 5.87 billion

- CAGR from 2024 to 2029 : 27.9%

Market Summary

- The AI in procurement market is undergoing a significant transformation, moving from a transactional function to a strategic business partner. This shift is driven by the need for enhanced operational efficiency, proactive risk management, and data-driven insights.

- By leveraging technologies such as machine learning and natural language processing, organizations are automating repetitive tasks like invoice processing and purchase order creation, allowing professionals to focus on higher-value activities. For instance, a manufacturing firm can utilize predictive analytics to anticipate supply chain disruptions, analyzing real-time data on supplier performance and geopolitical events to develop alternative sourcing strategies proactively.

- This capability builds resilience in a volatile global market. However, the integration of these sophisticated systems introduces challenges, including the complexity of integrating with legacy platforms, ensuring data security against cyber threats, and addressing the growing talent gap for professionals skilled in both procurement and AI.

- The evolving regulatory environment, including new data privacy and AI governance laws, further complicates adoption, demanding a strategic approach to compliance and risk management.

What will be the Size of the AI In Procurement Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Procurement Market Segmented?

The ai in procurement industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- End-user

- Manufacturing

- Retail and e-commerce

- Healthcare

- Transportation and logistics

- Others

- Technology

- Machine learning

- Natural language processing

- Predictive analytics

- Computer vision

- Robotic process automation

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- South Africa

- Israel

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is defined by a rapidly evolving landscape where advanced AI functionalities are becoming more accessible. Organizations are moving beyond simple task automation, leveraging platforms for strategic partnership.

A key trend involves the use of generative AI tools for procurement data enrichment and payment fraud detection, which can improve data accuracy by over 95%.

These AI-driven category management systems, integrated with procurement chatbots, provide strategic sourcing intelligence and real-time spend visibility.

This shift enables procurement software to act as a strategic partner, offering predictive insights and intelligent invoice processing through natural language processing in sourcing and AI for ESG compliance, supporting complex decision-making across the entire source-to-pay process with robust procurement workflow automation.

The Software segment was valued at USD 1.24 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Procurement Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI in procurement market is led by North America, which accounts for over 35% of the market's incremental growth, driven by early technology adoption and a high concentration of AI providers.

This region leverages AI for predictive sourcing and comprehensive supply chain risk monitoring. In contrast, the APAC region is the fastest-growing market, propelled by rapid digitalization and a strong manufacturing base.

European adoption is shaped by a stringent regulatory environment, with a focus on using AI for spend optimization and ensuring compliance with evolving data laws. AI for supplier negotiation and robotic process automation in P2P are being implemented globally.

South America and the Middle East and Africa are emerging markets, with growing interest in AI for spend analytics and automated supplier vetting to navigate economic pressures and enhance operational stability.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Organizations are increasingly exploring how AI improves procurement efficiency by moving beyond basic automation. A key question is understanding the benefits of generative AI in sourcing, which allows for the rapid creation of complex documents like RFPs and supplier scorecards.

- For strategic planning, firms are focused on AI for mitigating supply chain risks, using predictive analytics for commodity pricing to anticipate market shifts. The challenge of implementing AI in legacy procurement systems remains, but the business case is compelling, with use cases for AI in contract management demonstrating a significant reduction in legal review cycles.

- In retail, AI-driven demand forecasting for retail is critical for inventory optimization. Operationally, robotic process automation for invoice matching and automating the procure-to-pay cycle have become standard practice, while machine learning models for supplier scoring are refining partner selection.

- Firms that leverage natural language processing for RFP analysis can process submissions more than twice as fast as those using manual methods. This efficiency extends to using AI for real-time spend analytics and optimizing tail spend with AI.

- The ability to use AI for strategic supplier discovery is transforming sourcing, while AI-powered negotiation tools for procurement are empowering teams to secure better terms. Furthermore, AI for ensuring procurement policy compliance and reducing procurement fraud with AI are critical for governance, as is AI-driven ESG monitoring in procurement.

- The entire process is being streamlined, from automating supplier onboarding with AI to the strategic evaluation of partners.

What are the key market drivers leading to the rise in the adoption of AI In Procurement Industry?

- The primary driver propelling market growth is the significant enhancement of decision-making capabilities and operational efficiency through AI integration.

- The market is propelled by the significant financial and operational advantages AI delivers.

- A primary driver is substantial cost reduction, with AI-powered spend optimization identifying savings opportunities previously hidden in vast datasets, leading to outcomes like a 15% reduction in purchasing costs for some adopters.

- Enhanced decision-making is another critical factor, as procurement analytics and machine learning for spend analytics provide actionable insights from complex information. This enables a more strategic approach to procurement, moving beyond tactical execution.

- Improved supplier management, facilitated by AI-driven supplier discovery and supplier performance management, builds more resilient and competitive supply chains.

- By automating due diligence and using AI to vet new partners through tools like procurement workflow automation, organizations can better mitigate risks related to performance, compliance, and geopolitical instability, ultimately transforming the procurement function.

What are the market trends shaping the AI In Procurement Industry?

- A key market trend is the drive toward enhanced efficiency and cost reduction through the strategic automation of procurement workflows. This shift liberates resources and accelerates operational cycle times.

- Key market trends revolve around leveraging AI to achieve new levels of operational excellence. The adoption of AI-powered tail spend solutions and conversational AI for procurement automates previously unmanaged expenditure and routine communications, with some firms reporting a 44% reduction in manual tasks.

- A significant trend is the move toward proactive risk management, using predictive risk signals to enhance supply chain resilience in an era of frequent disruptions. For example, continuous risk assessment is critical, as highlighted by a notable increase in supplier bankruptcies last year. This allows procurement teams to shift from a reactive to a proactive stance.

- The use of procurement control tower solutions provides a centralized hub for data-driven insights, enabling more strategic decisions. Furthermore, technologies like computer vision for inventory audit are enhancing accuracy and reducing manual cycle counting, directly improving procurement planning.

What challenges does the AI In Procurement Industry face during its growth?

- A key challenge affecting industry growth stems from concerns over data security and privacy, compounded by an evolving and complex regulatory landscape.

- Market growth faces significant challenges, primarily centered on data governance, system integration, and talent. Data security is a major concern, as AI platforms handling sensitive supplier financial data and contract terms become high-value targets for cyberattacks. The evolving regulatory landscape, exemplified by the EU AI Act with penalties of up to 7% of global revenue, adds complexity to compliance monitoring.

- Implementation complexity and integration with legacy ERP systems present another barrier, as retrofitting AI onto older architectures can be costly and inefficient. This is compounded by a widening talent gap, with a significant shortage of professionals possessing the hybrid skills needed for AI in strategic sourcing and data analytics.

- This forces reliance on external consultants, increasing the overall cost and complexity of AI adoption and hindering the ability to scale solutions effectively.

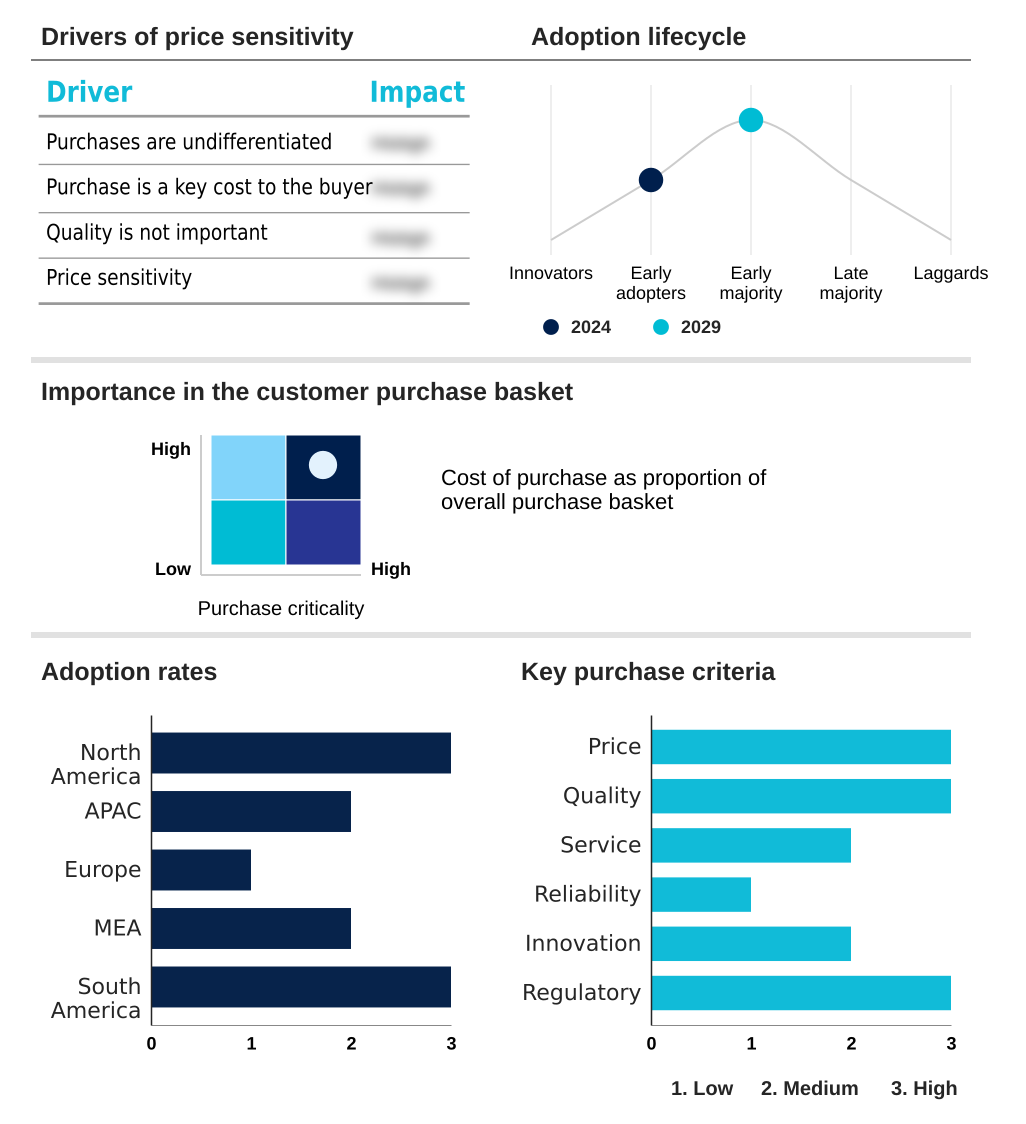

Exclusive Technavio Analysis on Customer Landscape

The ai in procurement market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in procurement market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Procurement Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in procurement market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Basware Corp. - Enables financial automation through AI-driven platforms, optimizing accounts payable and strategic outcomes with predictive analytics and touchless invoice processing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Basware Corp.

- Clarifai Inc.

- Coupa Software Inc.

- GEP

- H2O.ai Inc.

- Intel Corp.

- IBM Corp.

- Ivalua Inc.

- JAGGAER LLC

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Proactis Holdings plc

- SAP SE

- TradeShift Inc.

- Xeeva Inc.

- Zebra Technologies Corp.

- Zycus Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in procurement market

- In September, 2024, IBM Corp. announced the launch of watsonx for Procurement, a new suite of generative AI agents designed to automate complex sourcing events, from RFP generation to advanced supplier negotiation simulations.

- In November, 2024, SAP SE and NVIDIA Corp. revealed a strategic partnership to integrate NVIDIA's AI Enterprise software into the SAP Ariba platform, aiming to accelerate predictive analytics for supply chain risk.

- In February, 2025, Coupa Software Inc. acquired a leading ESG data analytics firm to integrate real-time sustainability and compliance scoring directly into its procurement platform, enhancing supplier vetting.

- In April, 2025, Microsoft Corp. launched its 'Responsible Procurement AI' initiative, providing a new framework and tools within Azure to help organizations ensure their use of AI in procurement complies with the evolving EU AI Act.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Procurement Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.9% |

| Market growth 2025-2029 | USD 5865.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 21.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, UAE, South Africa, Israel, Saudi Arabia, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in procurement market is fundamentally reshaping enterprise operations by embedding intelligence across the entire source-to-pay process. This evolution is marked by a transition from basic purchase order automation and invoice data extraction to sophisticated strategic sourcing intelligence and predictive sourcing. Organizations are deploying AI-driven supplier discovery and supplier onboarding automation to build more resilient networks.

- At the core, spend analysis automation and detailed spend categorization provide unparalleled real-time spend visibility, allowing for proactive tail spend management. For instance, companies leveraging these tools have achieved a 15% enhancement in procurement return on investment. The adoption of procurement analytics, powered by machine learning, facilitates dynamic supplier performance management and robust supplier risk assessment.

- Within the workflow, guided buying systems and procurement chatbots streamline user interactions, while request for proposal (RFP) automation accelerates sourcing cycles. A key boardroom-level driver is compliance monitoring, where AI ensures adherence to internal policies and external regulations, directly impacting corporate governance.

- Advanced functionalities like negotiation support systems and robust payment fraud detection further enhance financial controls and outcomes within e-procurement platforms and contract lifecycle management.

What are the Key Data Covered in this AI In Procurement Market Research and Growth Report?

-

What is the expected growth of the AI In Procurement Market between 2025 and 2029?

-

USD 5.87 billion, at a CAGR of 27.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services), End-user (Manufacturing, Retail and e-commerce, Healthcare, Transportation and logistics, Others), Technology (Machine learning, Natural language processing, Predictive analytics, Computer vision, Robotic process automation) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Enhanced decision making and operational efficiency, Data security, privacy, and evolving regulatory landscapes

-

-

Who are the major players in the AI In Procurement Market?

-

Basware Corp., Clarifai Inc., Coupa Software Inc., GEP, H2O.ai Inc., Intel Corp., IBM Corp., Ivalua Inc., JAGGAER LLC, Microsoft Corp., NVIDIA Corp., Oracle Corp., Proactis Holdings plc, SAP SE, TradeShift Inc., Xeeva Inc., Zebra Technologies Corp. and Zycus Inc.

-

Market Research Insights

- Market dynamics are increasingly influenced by the adoption of advanced AI, with organizations leveraging autonomous sourcing and cognitive spend intelligence to gain a competitive edge. A recent study indicated that nearly a quarter of businesses have already deployed generative AI, achieving a 44% reduction in manual tasks.

- This drive for efficiency is evident as companies use AI-powered supplier collaboration and intelligent procurement intake systems. Firms implementing AI-driven category management have reported a 15% enhancement in procurement ROI.

- Furthermore, the use of a procurement digital twin allows for sophisticated scenario modeling, while agentic AI in procurement helps automate complex negotiations, reflecting a clear trend toward more intelligent and resilient supply chain operations.

We can help! Our analysts can customize this ai in procurement market research report to meet your requirements.

RIA -

RIA -