AI In Space Exploration Market Size 2025-2029

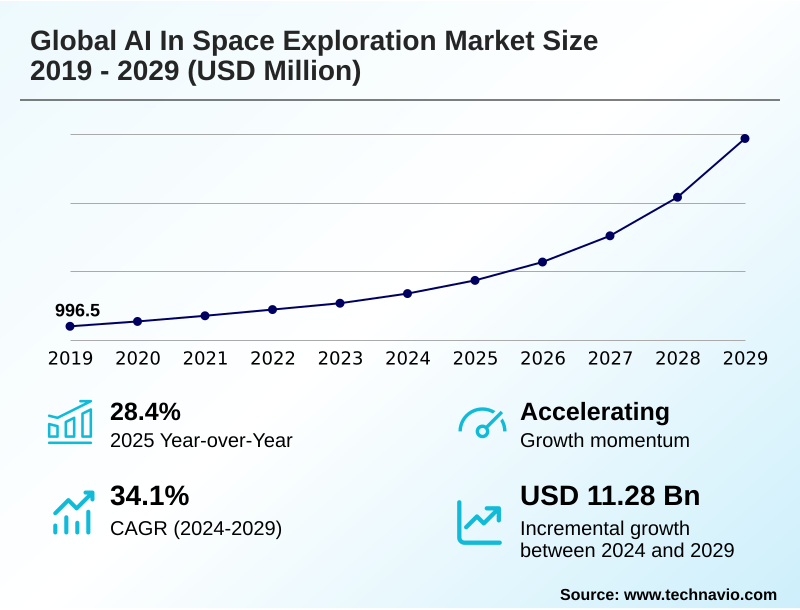

The ai in space exploration market size is valued to increase by USD 11.28 billion, at a CAGR of 34.1% from 2024 to 2029. Increasing investment and strategic initiatives in space exploration will drive the ai in space exploration market.

Major Market Trends & Insights

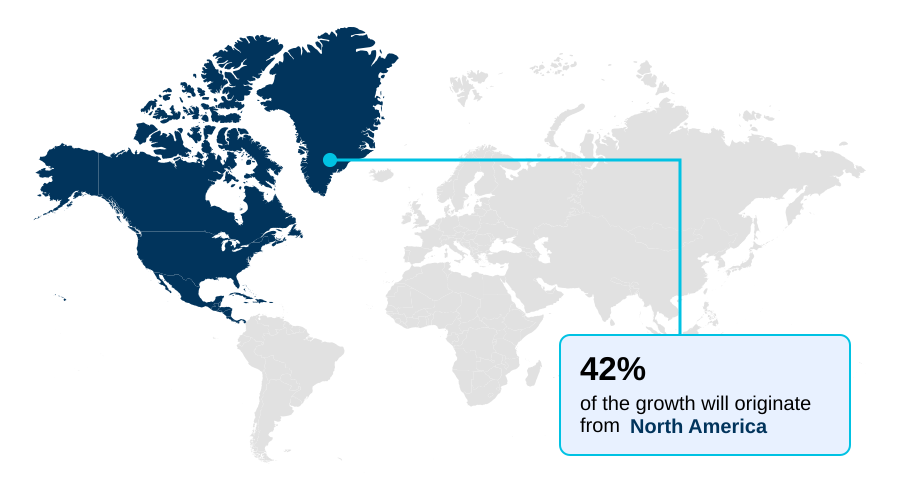

- North America dominated the market and accounted for a 41.8% growth during the forecast period.

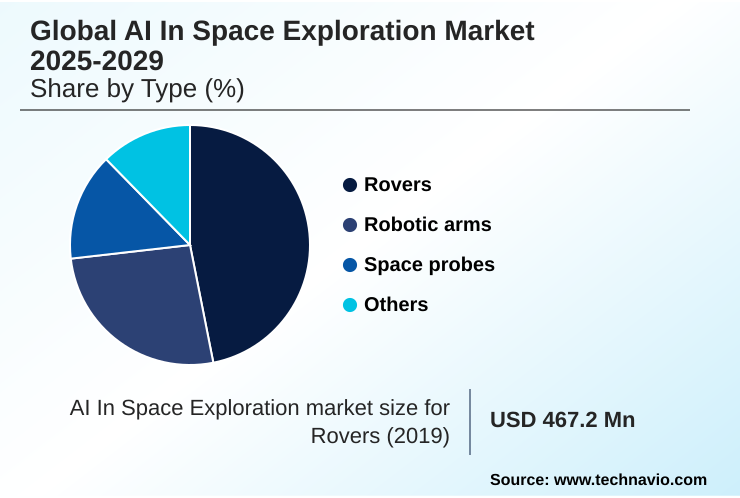

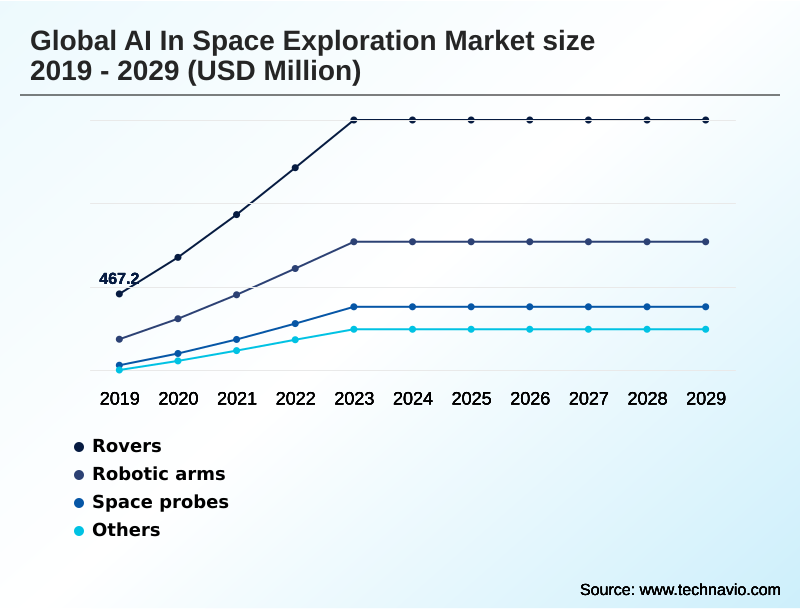

- By Type - Rovers segment was valued at USD 1.25 billion in 2023

- By Application - Robotics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 13.66 billion

- Market Future Opportunities: USD 11.28 billion

- CAGR from 2024 to 2029 : 34.1%

Market Summary

- The AI in space exploration market involves the application of advanced computing, including machine learning and deep learning models, to automate and enhance space missions. This technology is instrumental for optimizing AI in mission planning, enabling autonomous navigation, and performing telemetry data analysis.

- Its primary applications span across planetary rovers, robotic arms, and sophisticated space probes, all of which benefit from enhanced operational efficiency and reduced mission risk. The integration of AI represents a pivotal advancement, transforming the feasibility of contemporary space endeavors by enabling greater spacecraft autonomy.

- For instance, in satellite constellation management, predictive analytics for spacecraft health are used to forecast component failures, allowing operators to schedule maintenance proactively and reroute data traffic, thereby preventing service disruptions and costly in-orbit failures.

- This shift from reactive to proactive management, powered by on-board AI processing and intelligent ground systems, underscores AI's role in accelerating scientific discovery and building a sustainable presence in space. The continuous evolution of these technologies ensures a dynamic and expanding landscape for the AI in space exploration market.

What will be the Size of the AI In Space Exploration Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Space Exploration Market Segmented?

The ai in space exploration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Rovers

- Robotic arms

- Space probes

- Others

- Application

- Robotics

- Manned vehicles launch

- Communications

- Remote sensing and monitoring

- Others

- End-user

- Government

- Commercial

- Geography

- North America

- US

- Canada

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Type Insights

The rovers segment is estimated to witness significant growth during the forecast period.

The segment for planetary rovers showcases a significant shift toward greater spacecraft autonomy, driven by machine learning for space robotics.

These autonomous planetary rovers are integral to modern robotics in space exploration, leveraging computer vision systems and sensor fusion to navigate challenging extraterrestrial terrains.

AI-driven scientific analysis is enhanced as rovers use intelligent resource management to prioritize targets, leading to profound scientific discovery.

Advanced reinforcement learning models enable dynamic pathfinding and hazard avoidance, with some systems demonstrating a 40% improvement in navigational efficiency over pre-programmed routes.

This capacity for on-the-fly decision-making, coupled with robust anomaly detection and capabilities for AI for celestial navigation, is crucial for long-duration missions where direct human control is unfeasible, defining the next frontier of exploration.

The Rovers segment was valued at USD 1.25 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Space Exploration Market Demand is Rising in North America Get Free Sample

The global landscape is led by North America, projected to contribute over 41% of the market's incremental growth, with the APAC region demonstrating the fastest expansion rate.

North America's dominance is sustained by robust government and private investment in autonomous space exploration and AI for satellite operations. Advanced mission control systems in the region leverage sophisticated telemetry data analysis and fault detection systems to manage complex operations.

Innovation in radiation-hardened processors enables more powerful on-board AI processing, which has improved data downlink efficiency by 25% in recent Earth observation missions. Europe is also a key region, focusing on on-orbit servicing AI and autonomous docking technologies.

Meanwhile, APAC's growth is fueled by national initiatives centered on celestial body mapping and developing AI-enhanced communication networks for automated mission control and AI in Earth observation.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The practical implementation of AI in space exploration is advancing through highly specialized applications. For instance, AI algorithms for autonomous rover navigation are now fundamental for traversing extraterrestrial surfaces, while reinforcement learning for robotic arm control enables intricate manipulation tasks.

- In astrophysics, machine learning models for exoplanet detection and the AI-powered analysis of astronomical data are dramatically accelerating the pace of discovery.

- The commercial viability of space is being enhanced by deep learning applications in satellite imagery and the use of AI for optimizing satellite orbital paths, with the latter showing potential to reduce propellant consumption by over 10% compared to traditional maneuvers, directly impacting the operational lifetime and profitability of satellite constellations.

- Security and mission success are bolstered by AI in real-time mission control and robust systems for fault detection in spacecraft using AI. Further, the push for a sustainable space presence is driven by AI-driven in-situ resource utilization and AI applications for space debris mitigation.

- The development of next-generation spacecraft relies on generative AI for spacecraft design simulation and edge computing for on-board satellite processing. Human-centric missions are also being transformed, with natural language processing for astronaut assistance reducing cognitive load, and explainable AI in mission-critical systems building trust in automated decisions.

- From computer vision for asteroid characterization to swarm robotics for multi-agent exploration and AI in planetary science data analysis, the use of AI for deep space communication and autonomous docking systems using AI is making previously theoretical missions achievable.

What are the key market drivers leading to the rise in the adoption of AI In Space Exploration Industry?

- Increasing investment from public and private sectors, alongside numerous strategic initiatives in space exploration, serves as a key driver propelling market growth.

- Market growth is propelled by escalating investments and the increasing demand for autonomous systems. The proliferation of large satellite constellations generates vast amounts of Earth observation data, necessitating advanced machine learning algorithms for telemetry data analysis and automated mission control.

- This has led to a 40% reduction in data processing latency on the ground. The demand for autonomous vehicle navigation in deep space, where communication delays can exceed 20 minutes, makes on-board AI processing essential.

- Innovations in machine learning for space robotics are enabling more complex tasks for AI-driven scientific analysis and AI in space manufacturing.

- Furthermore, advancements in AI-enhanced communication networks and fault detection systems are improving mission reliability, while emerging fields like quantum machine learning promise to solve previously intractable optimization problems for space logistics.

What are the market trends shaping the AI In Space Exploration Industry?

- A primary market trend involves significant advancements in autonomous navigation and mission control systems. These developments are enabling more complex, self-directed operations with minimized human intervention.

- Key market trends are centered on enhancing spacecraft autonomy and accelerating AI-driven scientific analysis. The use of deep learning models in autonomous space exploration is enabling capabilities from autonomous docking to swarm robotics, with simulations showing a 60% increase in mission area coverage for coordinated rovers.

- Predictive maintenance algorithms, a key aspect of AI for satellite operations, are reducing unexpected component failures by up to 30%, extending the lifespan of valuable assets. Furthermore, AI in mission planning is evolving toward in-situ resource utilization, optimizing extraction and processing.

- In scientific domains, deep learning in astrophysics and AI-powered space telescopes leverage real-time data processing to analyze celestial phenomena, accelerating the discovery of exoplanets by a factor of two in some recent surveys.

What challenges does the AI In Space Exploration Industry face during its growth?

- The high development and implementation costs associated with specialized AI solutions for space present a key challenge affecting the industry's growth trajectory.

- Significant market challenges persist, primarily concerning high development costs and data security. The creation of resilient mission control systems that incorporate explainable AI (XAI) and natural language processing can increase software development costs by over 25%.

- Furthermore, securing data analytics for space missions against adversarial attacks, such as those using generative adversarial networks, requires extensive digital twin simulation and testing, adding an estimated 15% to project timelines. The complexity of applications like hyperspectral imaging analysis for AI for asteroid mining and AI for space weather forecasting demands substantial investment in both specialized hardware and talent.

- Ensuring the reliability of crew health monitoring AI and intelligent life support systems in long-duration missions remains a critical validation hurdle, as does securing the vast AI for deep space network against potential breaches.

Exclusive Technavio Analysis on Customer Landscape

The ai in space exploration market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in space exploration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Space Exploration Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in space exploration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Delivers AI-driven solutions for satellite mission planning, enhanced Earth observation image processing, and autonomous space vehicle navigation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- BAE Systems Plc

- Blue Origin Enterprises LP

- Booz Allen Hamilton Corp.

- Capella Space Corp.

- D-Orbit

- Hewlett Packard

- ICEYE Oy

- IBM Corp.

- Lockheed Martin Corp.

- Maxar Technologies Inc.

- Northrop Grumman Corp.

- OHB System AG

- Planet Labs PBC

- Spire Global Inc.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in space exploration market

- In September, 2024, IBM Corp. announced a strategic partnership with The Boeing Co. to develop a next-generation AI platform for managing deep space communication networks, aiming to reduce data latency by 20%.

- In November, 2024, Planet Labs PBC launched its new AI-powered analytics suite, which automates the detection of environmental changes from satellite imagery with over 95% accuracy.

- In January, 2025, Capella Space Corp. secured $150 million in Series C funding to expand its constellation of SAR satellites and enhance its on-board AI processing capabilities for real-time intelligence.

- In April, 2025, Lockheed Martin Corp., under a new NASA contract valued at $80 million, successfully demonstrated an autonomous navigation system for lunar rovers that uses reinforcement learning to self-correct pathways in real-time.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Space Exploration Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 280 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 34.1% |

| Market growth 2025-2029 | USD 11278.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 28.4% |

| Key countries | US, Canada, China, Japan, India, Australia, South Korea, Germany, UK, France, Brazil, Argentina, Saudi Arabia and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in space exploration market is defined by a convergence of advanced technologies enabling unprecedented spacecraft autonomy. The deployment of radiation-hardened processors is facilitating complex on-board AI processing and edge computing in space, which is critical for real-time data processing.

- Machine learning algorithms and deep learning models are the bedrock of systems for predictive maintenance, anomaly detection, and fault detection systems, with some operators reporting a 30% reduction in unexpected satellite component failures. For boardroom decisions, this directly impacts budgeting by extending asset lifespan and reducing insurance premiums.

- Computer vision systems are essential for autonomous docking, celestial body mapping, and space debris tracking. Applications extend from the control of robotic arms and planetary rovers to the management of vast satellite constellations. In scientific domains, reinforcement learning and generative adversarial networks are accelerating scientific discovery, particularly in exoplanet detection and hyperspectral imaging analysis.

- Core technologies like sensor fusion, natural language processing for crew interaction, and cognitive radio for adaptive communications are maturing. The development of explainable AI (XAI) is addressing transparency concerns in mission control systems, while digital twin simulation and quantum machine learning represent the next frontier.

- This technological momentum, from swarm robotics to space situational awareness, is fundamentally reshaping mission capabilities and economic models.

What are the Key Data Covered in this AI In Space Exploration Market Research and Growth Report?

-

What is the expected growth of the AI In Space Exploration Market between 2025 and 2029?

-

USD 11.28 billion, at a CAGR of 34.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Rovers, Robotic arms, Space probes, and Others), Application (Robotics, Manned vehicles launch, Communications, Remote sensing and monitoring, and Others), End-user (Government, and Commercial) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing investment and strategic initiatives in space exploration, High development and implementation costs

-

-

Who are the major players in the AI In Space Exploration Market?

-

Airbus SE, BAE Systems Plc, Blue Origin Enterprises LP, Booz Allen Hamilton Corp., Capella Space Corp., D-Orbit, Hewlett Packard, ICEYE Oy, IBM Corp., Lockheed Martin Corp., Maxar Technologies Inc., Northrop Grumman Corp., OHB System AG, Planet Labs PBC, Spire Global Inc., Thales Group and The Boeing Co.

-

Market Research Insights

- The market is driven by AI in mission planning and automated mission control, where AI in spacecraft design and launch vehicle systems are reducing development cycles by over 40%. Autonomous space exploration is realized through machine learning for space robotics and autonomous vehicle navigation, crucial for autonomous planetary rovers.

- AI for satellite operations and space traffic management enables on-orbit servicing AI and on-orbit manufacturing. Concurrently, AI-driven scientific analysis via AI-powered space telescopes and deep learning in astrophysics powers data analytics for space missions. AI in remote sensing and Earth observation is a key application. AI-enhanced communication networks and the AI for deep space network improve data throughput by 30%.

- Future applications include intelligent resource management for AI for asteroid mining, predictive analytics for spacecraft, crew health monitoring AI, intelligent life support systems, and AI for space weather forecasting, all underpinning the next wave of robotics in space exploration and AI for celestial navigation.

We can help! Our analysts can customize this ai in space exploration market research report to meet your requirements.

RIA -

RIA -