AI In Supply Chain Management Market Size 2025-2029

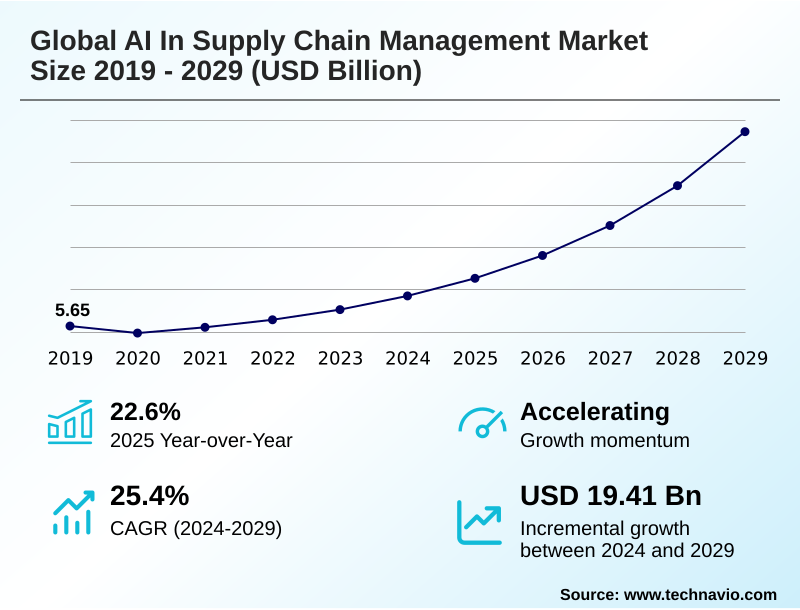

The ai in supply chain management market size is valued to increase by USD 19.41 billion, at a CAGR of 25.4% from 2024 to 2029. Increasing demand for enhanced visibility and transparency will drive the ai in supply chain management market.

Major Market Trends & Insights

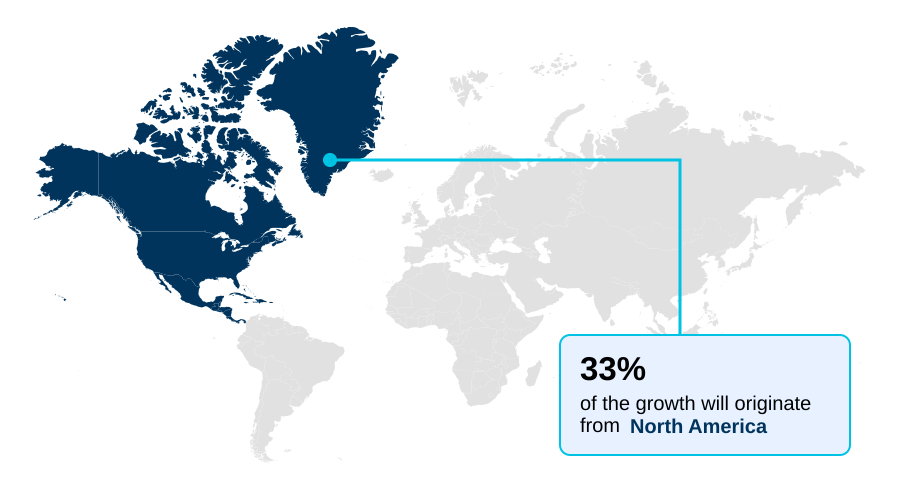

- North America dominated the market and accounted for a 32.6% growth during the forecast period.

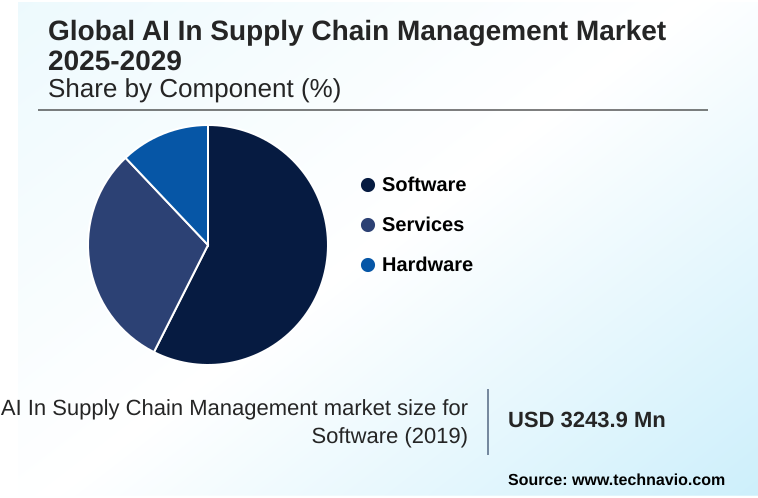

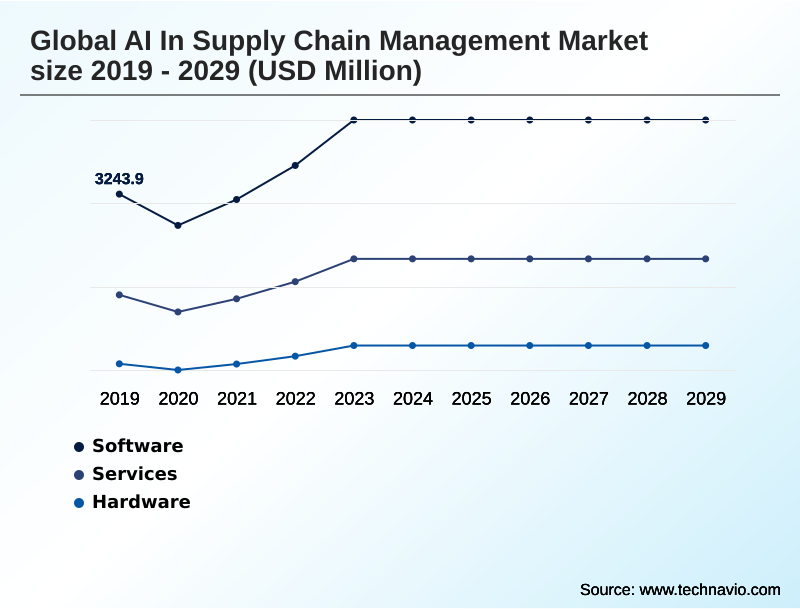

- By Component - Software segment was valued at USD 4.36 billion in 2023

- By Application - Demand planning and forecasting segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 22.97 billion

- Market Future Opportunities: USD 19.41 billion

- CAGR from 2024 to 2029 : 25.4%

Market Summary

- The AI in supply chain management market is undergoing a fundamental transformation, moving from traditional, reactive models to predictive, autonomous operational frameworks. This evolution is driven by the imperative for enhanced operational efficiency, cost reduction, and greater resilience in the face of global volatility.

- Key technologies such as machine learning algorithms, predictive analytics, and generative AI are being integrated to automate complex processes and provide deeper data-driven insights. For example, a global consumer goods company can leverage AI-driven demand forecasting, which analyzes not just historical sales but also real-time market signals for more accurate inventory optimization. This prevents stockouts and reduces carrying costs.

- However, adoption is not without challenges. Integrating disparate data sources and ensuring data security are significant hurdles. The pronounced talent gap for professionals skilled in both supply chain logistics and data science further constrains progress.

- The proliferation of hyper-automation and intelligent warehousing solutions, powered by technologies like computer vision and autonomous mobile robots (AMRs), signals the market's trajectory toward creating highly efficient, self-optimizing, and transparent supply networks that offer a distinct competitive advantage.

What will be the Size of the AI In Supply Chain Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Supply Chain Management Market Segmented?

The ai in supply chain management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Hardware

- Application

- Demand planning and forecasting

- Inventory management

- Transportation management

- Others

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the intelligence layer of the AI in supply chain management market, crucial for achieving end-to-end visibility. It encompasses solutions using machine learning algorithms and predictive analytics for autonomous decision making.

These platforms provide real-time visibility, enabling supply chain orchestration and intelligent automation. Capabilities extend to using natural language processing for unstructured data analysis and computer vision for quality checks, where implementations have reduced inspection errors by over 25%.

This cognitive automation transforms operations from reactive to proactive, providing a unified, strategic view. The market segmentation reveals software as the dominant component, driving the shift toward more resilient and data-driven supply networks through advanced computational analysis and process optimization.

The Software segment was valued at USD 4.36 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Supply Chain Management Market Demand is Rising in North America Get Free Sample

North America leads the cognitive supply chain market, driven by mature infrastructure and high adoption rates, with the US accounting for over 27% of market value in 2024.

The region focuses on AI-driven demand forecasting and risk management to counter disruptions. In contrast, the APAC market, with a projected CAGR of 26.4%, is the fastest-growing region, leveraging AI for logistics and network optimization to manage vast e-commerce volumes.

European firms prioritize inventory optimization and predictive maintenance, with some achieving a 15% reduction in logistics costs through AI integration.

Across these regions, technologies like demand sensing and concurrent planning are becoming standard for building resilient operations, while predictive shipment tracking enhances customer satisfaction and operational control.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The practical application of AI in supply chain management is rapidly expanding into specialized, high-impact areas. For instance, AI for last-mile delivery optimization is critical for e-commerce, directly addressing the most expensive part of the fulfillment journey. Beyond logistics, generative AI in network design allows companies to model and build more resilient supply routes from the ground up.

- The use of predictive analytics for disruption is becoming a standard proactive measure, moving beyond simple alerts to offer actionable mitigation strategies. At the core of planning, machine learning for demand forecasting consistently outperforms traditional methods, with some companies seeing forecast accuracy improvements that are twice as effective at reducing stockouts.

- The focus on cost control is evident in how AI is reducing logistics costs through better asset utilization and fuel management. Within facilities, AI in warehouse automation and the use of computer vision for quality control are increasing throughput and accuracy.

- Other key applications include natural language processing in procurement for better contract analysis, the deployment of digital twins for supply chain simulation, and leveraging IoT data for predictive maintenance on critical equipment. Furthermore, AI for dynamic route optimization, optimizing inventory with prescriptive analytics, and hyper-automation in fulfillment centers are becoming widespread.

- Strategic gains are also found in multi-echelon inventory optimization strategy, agentic AI for task orchestration, and AI-driven spend analytics savings. The goal of enhancing visibility with cognitive automation, improving resilience with risk sensing, and ensuring product integrity through AI applications in cold chain logistics highlights the technology's pervasive impact.

- The connection between smart manufacturing and AI integration is creating a seamless flow of data from production to consumer.

What are the key market drivers leading to the rise in the adoption of AI In Supply Chain Management Industry?

- The increasing demand for enhanced visibility and transparency across the entire value chain is a primary driver for the accelerated adoption of AI in supply chain management.

- Market drivers center on the need for enhanced supply chain resilience and efficiency. The adoption of digital transformation is accelerating, with companies leveraging generative AI to improve operational intelligence.

- Intelligent warehousing, utilizing automated guided vehicles (AGVs) and prescriptive analytics, has demonstrated the ability to reduce inventory levels by up to 35%.

- The use of digital twins for simulating network performance and edge computing for real-time decision-making is becoming more common. These technologies support advanced risk sensing, enabling organizations to proactively mitigate disruptions identified through AI analysis.

- The imperative for cost reduction remains a powerful catalyst, as AI-driven optimization has been shown to lower transport costs by up to 30%, building a strong business case for investment.

What are the market trends shaping the AI In Supply Chain Management Industry?

- The proliferation of generative AI in supply chain operations is a primary market trend. This technology is fundamentally altering strategic and operational paradigms beyond traditional analytics.

- Key market trends are redefining operational efficiency. The use of autonomous mobile robots (AMRs) is surging, with some fulfillment centers increasing picking productivity by over 40%. Concurrently, the integration of data from IoT sensors, RFID tags, and GPS trackers is enabling sophisticated supply chain modeling and logistics orchestration. This trend supports smart manufacturing integration, where AI agents execute complex decisions.

- In procurement automation, AI-powered business planning tools are delivering substantial savings, with early adopters reporting cost reductions of up to 10%. These advancements reflect a move toward hyper-automated environments where physical and digital processes are seamlessly interconnected, driving a new level of performance and resilience in supply chain operations.

What challenges does the AI In Supply Chain Management Industry face during its growth?

- The multifaceted challenges of data security, complex systems integration, and evolving regulatory compliance represent a primary obstacle to widespread AI implementation in supply chain management.

- Despite significant opportunities, market adoption faces notable challenges. The talent gap remains a primary constraint, with one analysis noting that only 35% of employees have received any AI-related training, hindering the effective use of tools for AI-enhanced demand planning and spend analytics.

- High implementation costs and uncertain ROI also temper investment in advanced systems like agentic AI for autonomous fulfillment or platforms for multi-echelon inventory optimization. Furthermore, integrating these technologies for functions like intelligent fleet management and dynamic route optimization with fragmented legacy systems is a significant technical hurdle.

- Successfully deploying hyper-automation requires a strategic approach to overcome these data integration and workforce transformation issues, which can otherwise stall progress and diminish returns.

Exclusive Technavio Analysis on Customer Landscape

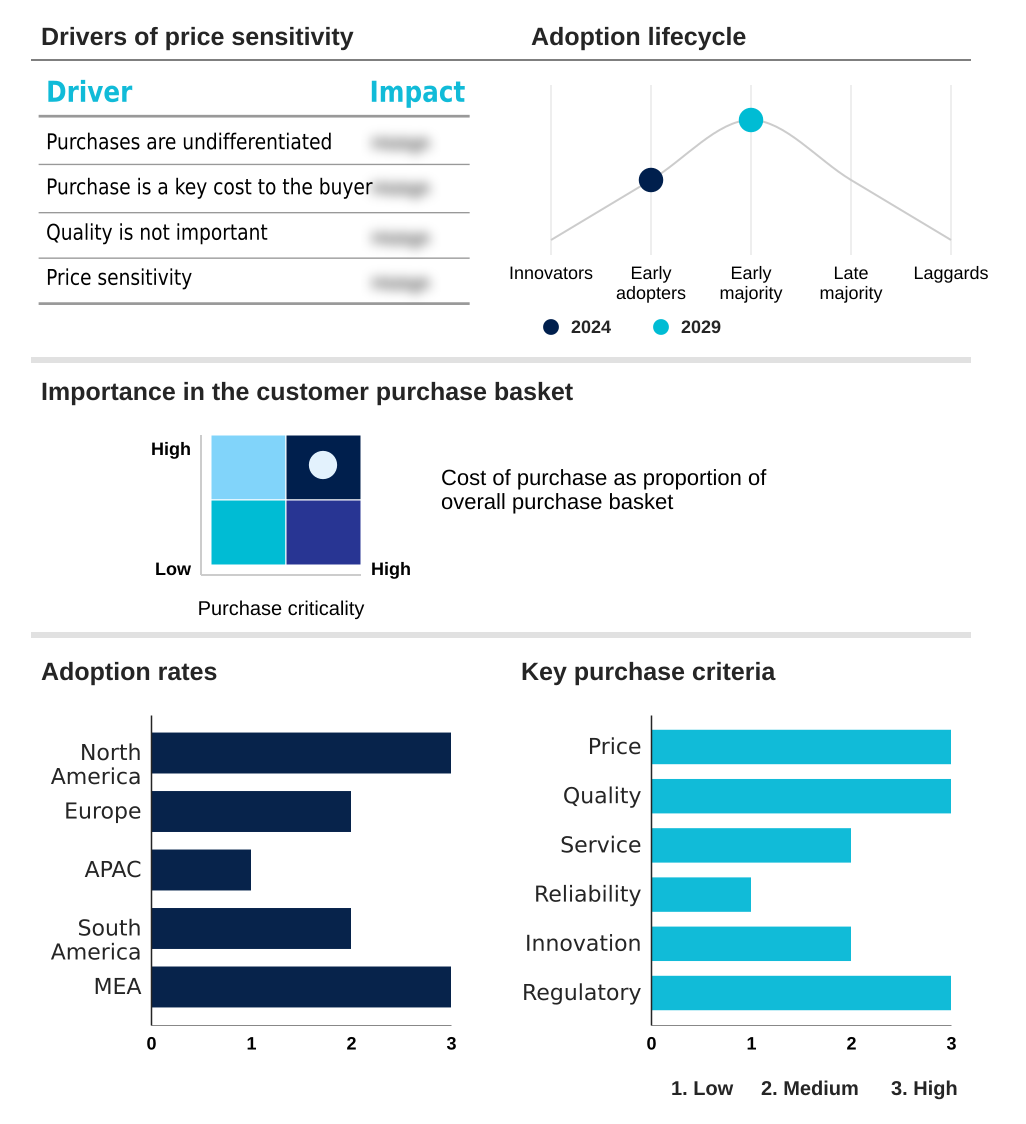

The ai in supply chain management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in supply chain management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Supply Chain Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in supply chain management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Group Holding Ltd. - Provides AI-driven demand forecasting and intelligent logistics to enhance e-commerce supply chain performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Group Holding Ltd.

- Amazon Web Services Inc.

- Blue Yonder Group Inc.

- Coupa Software Inc.

- Descartes Systems Group Inc.

- DHL International GmbH

- E2open Parent Holdings Inc.

- Fourkites Inc.

- Google LLC

- Infor Inc.

- IBM Corp.

- Kinaxis Inc.

- Manhattan Associates Inc.

- Microsoft Corp.

- Oracle Corp.

- Samsung SDS

- SAP SE

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in supply chain management market

- In August 2024, technology leaders including Amazon Web Services Inc. and Microsoft Corp. made significant strides by integrating advanced AI into their supply chain management tools to improve decision-making.

- In December 2024, Italy secured a major European High-Performance Computing Joint Undertaking project, IT4LIA AI Factory, to host a European AI supercomputer supporting strategic sectors like manufacturing supply chains.

- In February 2025, the Colombian government approved its National Artificial Intelligence Policy, CONPES 4144, committing approximately $115.9 million through 2030 to foster AI research, development, and adoption in key economic sectors.

- In March 2025, France's public investment bank, Bpifrance, announced a major initiative to mobilize substantial capital by 2029, aimed at supporting the entire AI value chain from startups to infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Supply Chain Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.4% |

| Market growth 2025-2029 | USD 19408.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 22.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in supply chain management market is characterized by intense innovation, with companies integrating a suite of advanced technologies to build intelligent, autonomous systems. Core components include machine learning algorithms for predictive analytics and generative AI for novel problem-solving. These are augmented by natural language processing for unstructured data insights and computer vision for automated inspections.

- The physical layer is transformed by IoT sensors, RFID tags, and GPS trackers feeding data into systems that control autonomous mobile robots (AMRs) and automated guided vehicles (AGVs). This shift enables sophisticated demand forecasting, inventory optimization, and logistics and network optimization.

- To manage volatility, firms are implementing robust risk management and predictive maintenance protocols, often powered by digital twins that simulate network behavior. The adoption of prescriptive analytics and agentic AI is driving a move toward hyper-automation, particularly in procurement automation and multi-echelon inventory optimization.

- A key boardroom consideration is the investment in edge computing to reduce latency, as some firms have achieved a 15% reduction in logistics costs by deploying AI-driven spend analytics and real-time decision-making capabilities, demonstrating a clear return on investment.

What are the Key Data Covered in this AI In Supply Chain Management Market Research and Growth Report?

-

What is the expected growth of the AI In Supply Chain Management Market between 2025 and 2029?

-

USD 19.41 billion, at a CAGR of 25.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services, and Hardware), Application (Demand planning and forecasting, Inventory management, Transportation management, and Others), Deployment (Cloud-based, On-premises, and Hybrid) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for enhanced visibility and transparency, Data security, integration, and regulatory compliance

-

-

Who are the major players in the AI In Supply Chain Management Market?

-

Alibaba Group Holding Ltd., Amazon Web Services Inc., Blue Yonder Group Inc., Coupa Software Inc., Descartes Systems Group Inc., DHL International GmbH, E2open Parent Holdings Inc., Fourkites Inc., Google LLC, Infor Inc., IBM Corp., Kinaxis Inc., Manhattan Associates Inc., Microsoft Corp., Oracle Corp., Samsung SDS, SAP SE and Siemens AG

-

Market Research Insights

- The market's digital transformation is creating a cognitive supply chain where intelligent automation delivers enhanced operational intelligence. This evolution enables end-to-end visibility and real-time visibility, allowing for superior supply chain orchestration and concurrent planning. By adopting AI-driven demand forecasting and demand sensing, firms are increasing forecast accuracy by over 10%.

- Further efficiencies are gained through advanced logistics orchestration and predictive shipment tracking. Intelligent warehousing, driven by AI agents, is boosting productivity in autonomous fulfillment by up to 45%. This push for supply chain resilience is supported by sophisticated supply chain modeling and risk sensing.

- AI-enhanced demand planning, dynamic route optimization, and intelligent fleet management are now central to smart manufacturing integration.

We can help! Our analysts can customize this ai in supply chain management market research report to meet your requirements.

RIA -

RIA -