AI In Transportation Market Size 2026-2030

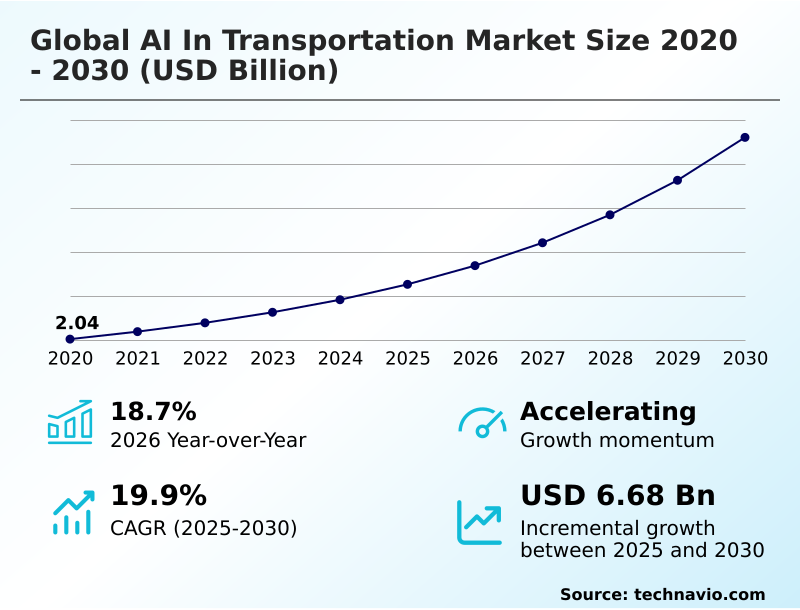

The ai in transportation market size is valued to increase by USD 6.68 billion, at a CAGR of 19.9% from 2025 to 2030. Escalating urban congestion and mandate for enhanced traffic flow efficiency will drive the ai in transportation market.

Major Market Trends & Insights

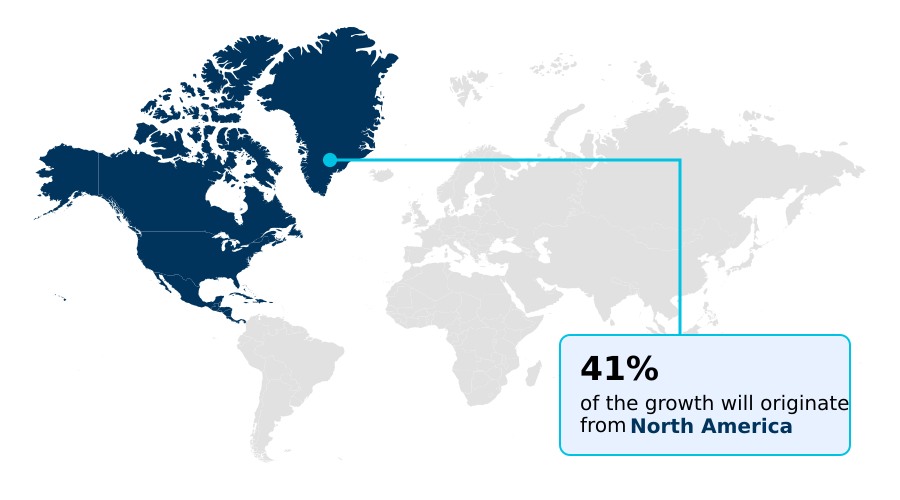

- North America dominated the market and accounted for a 41.4% growth during the forecast period.

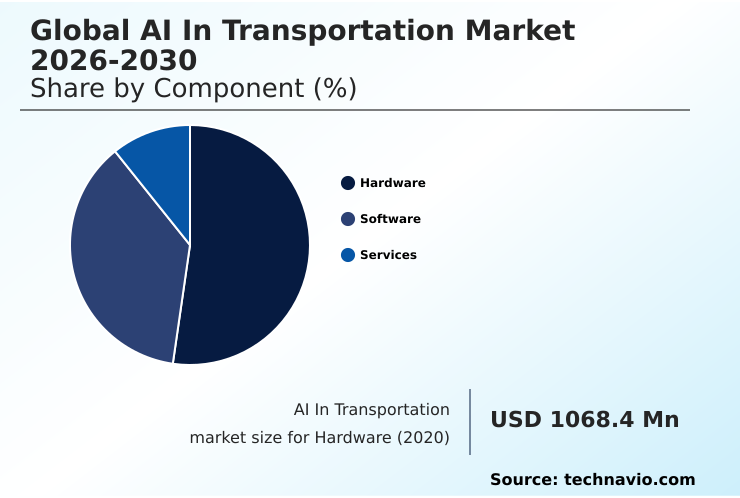

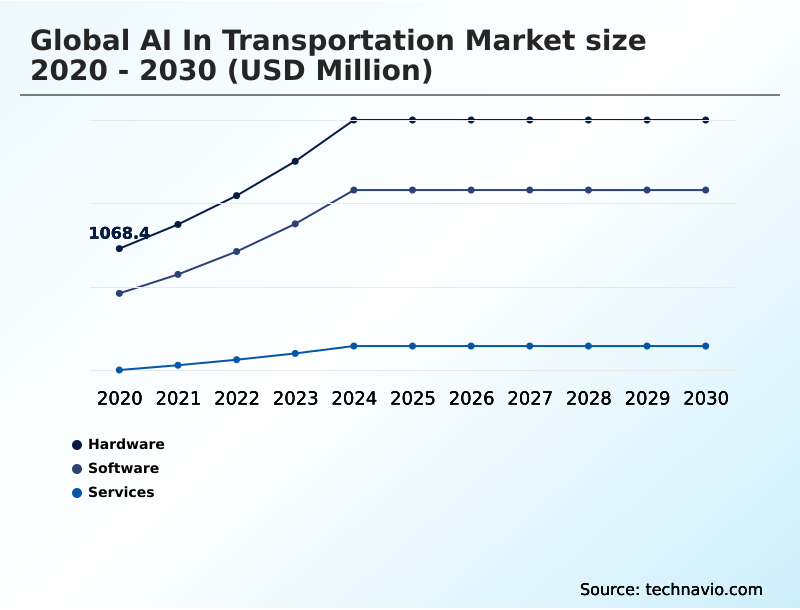

- By Component - Hardware segment was valued at USD 1.97 billion in 2024

- By Application - Autonomous vehicles segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.17 billion

- Market Future Opportunities: USD 6.68 billion

- CAGR from 2025 to 2030 : 19.9%

Market Summary

- The AI in transportation market is fundamentally reshaping mobility and logistics through advanced computational intelligence. This transformation is driven by the escalating need for safer, more efficient, and sustainable transport networks.

- Key applications include autonomous vehicles that use sensor fusion and machine learning to navigate complex environments, intelligent traffic management systems that alleviate urban congestion, and AI-powered logistics platforms that optimize global supply chains.

- For instance, a freight company can leverage AI to analyze real-time traffic, weather, and delivery schedules, automatically rerouting its entire fleet to minimize fuel consumption and ensure on-time arrivals. While the potential benefits are immense, the industry also navigates significant challenges, including evolving regulatory frameworks, ensuring data privacy, and the high capital investment required for infrastructure modernization.

- The continued advancement of technologies like deep learning and computer vision promises to unlock new capabilities, from predictive maintenance that prevents vehicle downtime to personalized mobility services that enhance the passenger experience. This technological evolution is fostering a dynamic ecosystem where innovation in algorithms and hardware is paramount for competitive advantage and operational excellence.

What will be the Size of the AI In Transportation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Transportation Market Segmented?

The ai in transportation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Services

- Application

- Autonomous vehicles

- Traffic management

- Freight management

- Predictive maintenance

- Others

- Technology

- Machine learning

- Deep learning

- Computer vision

- Natural language processing

- Context aware computing

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment serves as the physical backbone for the global AI in transportation market 2026-2030, enabling complex operations from logistics fulfillment to enhanced road safety.

This includes high-performance computing units essential for deep learning and computer vision tasks, alongside a suite of sensors for environmental perception.

The increasing demand to mitigate urban congestion and improve traffic flow efficiency drives innovation in edge computing devices, which process data locally to reduce latency for critical applications like autonomous navigation systems.

As the industry advances, the focus shifts toward specialized processors that support real-time predictive maintenance and reduce human error.

These integrated systems are foundational to developing solutions that address complex supply chain solutions, with component-level processing speeds improving by over 20% in recent designs.

The Hardware segment was valued at USD 1.97 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Transportation Market Demand is Rising in North America Get Free Sample

The global AI in transportation market 2026-2030 is geographically diverse, with North America leading, contributing over 41% of incremental growth, driven by advanced R&D in connected car platforms and mobility as a service.

The region's leadership is built on sophisticated machine learning applications and robust telematics networks. Europe follows, with a strong focus on regulatory frameworks supporting public transit optimization and rail automation.

Meanwhile, APAC is the fastest-growing region, aggressively implementing smart city infrastructure and V2X communications to manage urban expansion. In these smart cities, AI-powered route optimization has demonstrated the ability to improve traffic flow by nearly 25%.

This global expansion relies on technologies like sensor fusion, digital twins for simulation, and natural language processing for user interfaces, addressing both commercial and passenger-focused asset lifecycle optimization.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global AI in transportation market 2026-2030 is marked by a wide array of specialized applications designed to enhance safety and efficiency. The implementation of AI for real-time traffic control and dynamic traffic signal optimization is critical for reducing urban congestion with AI.

- In logistics, deep learning in autonomous trucking and AI algorithms for demand forecasting are revolutionizing how goods are moved, while intelligent speed assistance systems and automated freight platooning efficiency promise further gains. Safety remains a paramount concern, addressed by technologies like V2X for intersection safety, computer vision for pedestrian detection, and robust AI-based fleet safety monitoring.

- Driver drowsiness detection systems are becoming standard in commercial fleets, contributing to a significant reduction in fatigue-related incidents compared to vehicles without such monitoring. The scope of innovation extends to predictive maintenance for rail networks, where digital twin for vehicle simulation helps anticipate failures.

- On the consumer side, natural language processing for infotainment is improving the in-vehicle experience, while AI in public transit scheduling and last-mile delivery drone coordination are reshaping urban mobility. Even administrative functions like managing supply chain with AI and deploying AI-powered toll collection systems are becoming more intelligent and automated.

What are the key market drivers leading to the rise in the adoption of AI In Transportation Industry?

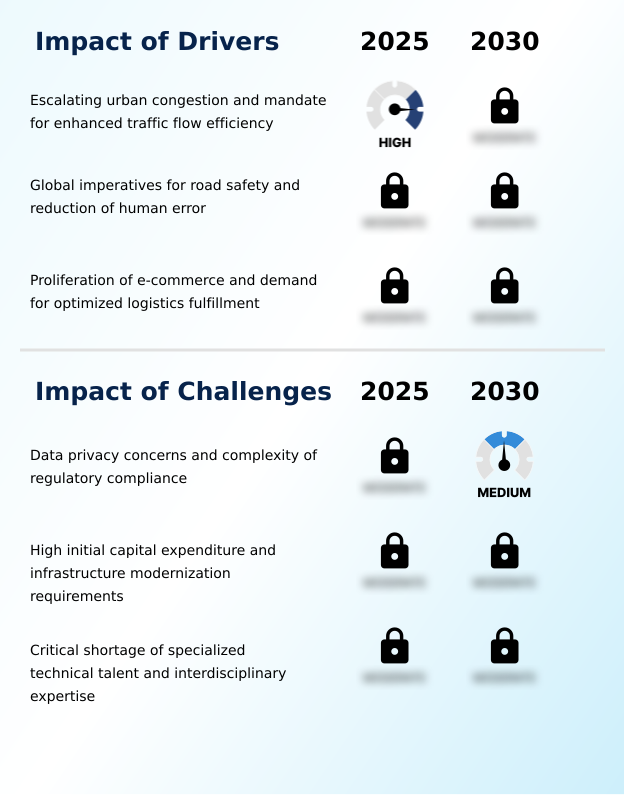

- Escalating urban congestion and the mandate for enhanced traffic flow efficiency are key drivers propelling market growth.

- The primary drivers for the global AI in transportation market 2026-2030 are the pressing needs for efficiency, safety, and sustainability.

- Intelligent traffic management systems are being deployed globally to combat urban density, leveraging path planning algorithms to improve vehicle flow by over 20%.

- The push for enhanced safety is fueling the adoption of driver monitoring systems, which use real-time data processing to detect and alert for fatigue.

- In public and commercial sectors, robotic process automation and automated traffic enforcement are streamlining operations and ensuring compliance, while transport planning software helps design smarter, more resilient networks.

- The growth of e-commerce necessitates advanced smart mobility solutions and connected operations platforms to manage logistics.

- This is driving investment in on-demand transit and intelligent transport systems, with a clear focus on mobility risk management and the efficiency gains from technologies like rail automation.

What are the market trends shaping the AI In Transportation Industry?

- The integration of autonomous navigation systems and advanced driver-assistance functionalities is emerging as a significant trend. This development is shaping the future of mobility and vehicle automation.

- Key trends shaping the global AI in transportation market 2026-2030 center on increasing autonomy and operational intelligence. The proliferation of advanced driver assistance systems that incorporate automated emergency braking is a critical step toward broader adoption of autonomous trucking and driverless ride-hailing services. These systems directly address safety, with some achieving a 40% reduction in specific types of collisions.

- In parallel, logistics optimization is being revolutionized by AI-powered freight management, where demand forecasting models have improved accuracy by up to 25%. This enables more efficient fleet management and last-mile delivery. The convergence of these trends is facilitated by an autonomous freight network and V2X (Vehicle-to-Everything) communication, creating a connected ecosystem where passenger information systems provide real-time, dynamic updates.

What challenges does the AI In Transportation Industry face during its growth?

- Data privacy concerns and the complexity of regulatory compliance present a key challenge affecting industry growth.

- Navigating the challenges of the global AI in transportation market 2026-2030 requires addressing complex technical and operational hurdles. The need for high-quality data annotation to train reliable models is a significant bottleneck, with costs increasing project budgets by up to 30% in some cases.

- Developing a robust AI-native operating system demands significant high-performance computing resources and a high degree of interdisciplinary expertise, a resource for which demand outstrips supply by nearly five to one. Furthermore, ensuring situational awareness in diverse conditions is a constant challenge, alongside managing data privacy concerns which necessitate advanced data anonymization techniques.

- The substantial cost of infrastructure modernization and regulatory compliance adds another layer of complexity. Firms must balance these challenges with the push for innovation in operational analytics, predictive analytics, and automated haulage to maintain a competitive edge.

Exclusive Technavio Analysis on Customer Landscape

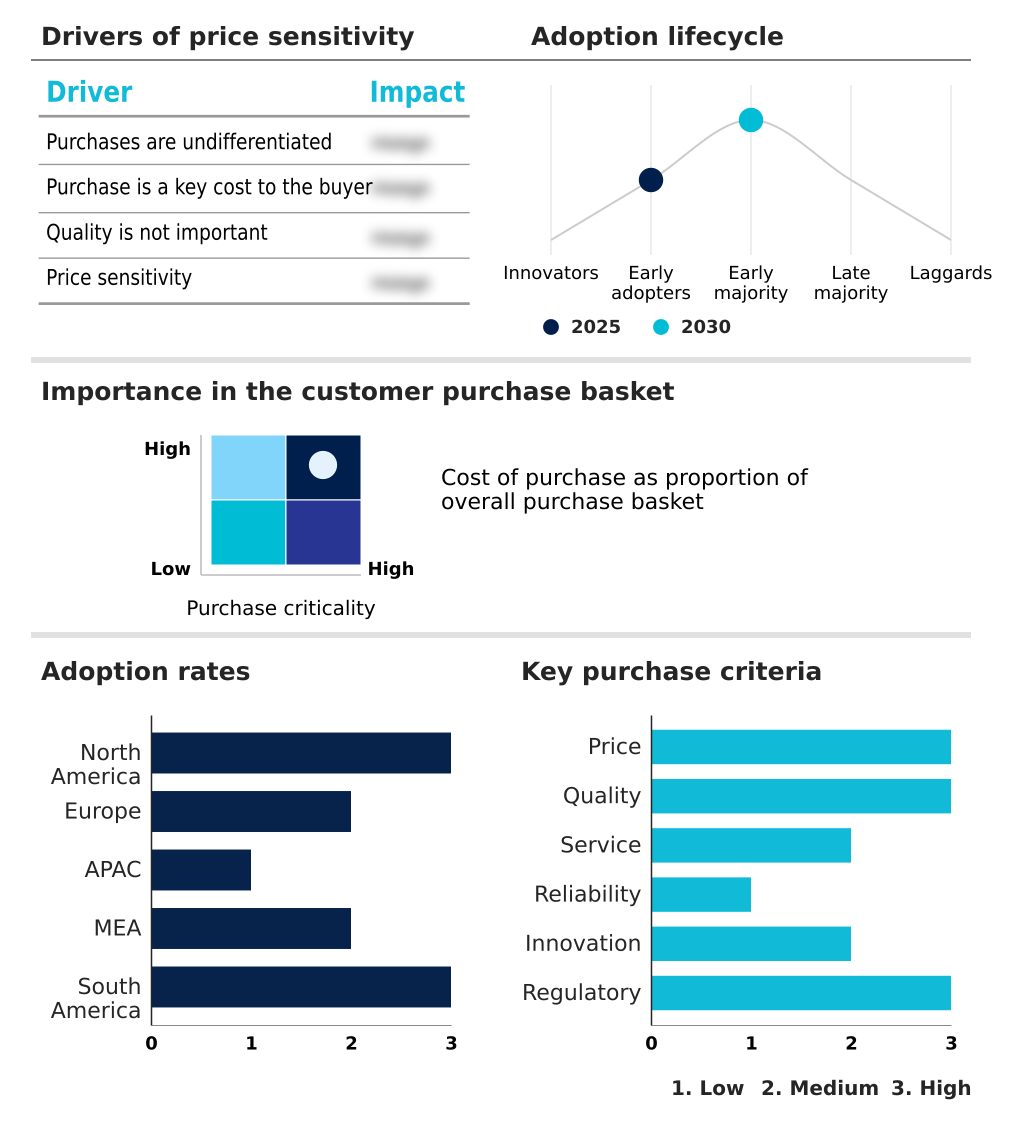

The ai in transportation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in transportation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Transportation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in transportation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Derq Inc. - The company offers AI in transportation through intelligent transportation systems that use computer vision and predictive analytics to monitor road users, optimize traffic flow, and prevent collisions using real-time data insights.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Derq Inc.

- Descartes Systems Group Inc.

- Einride AB

- Geotab Inc.

- Hayden AI Technologies Inc.

- Hitachi Ltd.

- Motive Technologies Inc.

- NetraDyne Inc.

- Nuro Inc.

- PlusAI Inc.

- PTV Planung Transport Verkehr

- Samba Holdings Inc.

- Samsara Inc.

- Siemens AG

- Tesla Inc.

- Transporeon GmbH

- Via Transportation Inc.

- Waabi

- Waymo LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in transportation market

- In April 2025, The European Commission ratified the Pan-European Autonomous Mobility Act, establishing a unified regulatory framework for Level 4 and Level 5 autonomous systems across all member states to streamline cross-border deployment.

- In February 2025, Waymo LLC announced a significant software update for its Waymo Driver technology, enhancing its performance in adverse weather conditions and complex urban environments based on data from millions of driven miles.

- In November 2024, Einride AB secured a new funding round to accelerate the deployment of its autonomous electric trucks and charging infrastructure across key logistics corridors in North America and Europe.

- In September 2024, Siemens AG partnered with a major US city to implement its AI-powered traffic management platform, which aims to reduce urban congestion and improve traffic flow during peak hours.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Transportation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.9% |

| Market growth 2026-2030 | USD 6681.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global AI in transportation market 2026-2030 is defined by the convergence of high-performance computing, sophisticated path planning algorithms, and real-time data processing. Core technologies such as machine learning and deep learning form the basis for systems that deliver situational awareness and operational analytics, enabling applications from autonomous trucking to automated haulage.

- The integration of sensor fusion platforms with computer vision and telematics allows for precise environmental interpretation, crucial for collision avoidance and advanced driver assistance systems. This technological synergy is driving a shift toward proactive operational strategies, exemplified by predictive maintenance and predictive analytics, which have been shown to reduce unplanned asset downtime by over 30%.

- Furthermore, innovations in natural language processing and facial recognition are enhancing user interaction and security. The development of AI-native operating systems and digital twins supports scalable solutions for fleet management, freight management, and logistics optimization, while V2X communications and edge computing provide the low-latency connectivity required for smart mobility and intelligent traffic management.

- Success hinges on mastering these interconnected technologies, including data annotation and robotic process automation, to deliver reliable and efficient transportation solutions.

What are the Key Data Covered in this AI In Transportation Market Research and Growth Report?

-

What is the expected growth of the AI In Transportation Market between 2026 and 2030?

-

USD 6.68 billion, at a CAGR of 19.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Application (Autonomous vehicles, Traffic management, Freight management, Predictive maintenance, and Others), Technology (Machine learning, Deep learning, Computer vision, Natural language processing, and Context aware computing) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating urban congestion and mandate for enhanced traffic flow efficiency, Data privacy concerns and complexity of regulatory compliance

-

-

Who are the major players in the AI In Transportation Market?

-

Derq Inc., Descartes Systems Group Inc., Einride AB, Geotab Inc., Hayden AI Technologies Inc., Hitachi Ltd., Motive Technologies Inc., NetraDyne Inc., Nuro Inc., PlusAI Inc., PTV Planung Transport Verkehr, Samba Holdings Inc., Samsara Inc., Siemens AG, Tesla Inc., Transporeon GmbH, Via Transportation Inc., Waabi and Waymo LLC

-

Market Research Insights

- The market's dynamic landscape is shaped by the tangible efficiencies AI delivers, with implementations of connected car platforms showing a significant reduction in operational costs. Firms leveraging mobility as a service models report higher asset utilization rates compared to traditional transport fleets.

- The strategic deployment for public transit optimization in smart city infrastructure is reducing commute times by over 15% in pilot programs. Furthermore, a focus on asset lifecycle optimization through AI has decreased maintenance expenditures by up to 30% for early adopters.

- This quantifiable return on investment is accelerating the integration of AI-driven last-mile delivery orchestration and other advanced supply chain solutions.

We can help! Our analysts can customize this ai in transportation market research report to meet your requirements.

RIA -

RIA -