AI Orchestration Platform Market Size 2025-2029

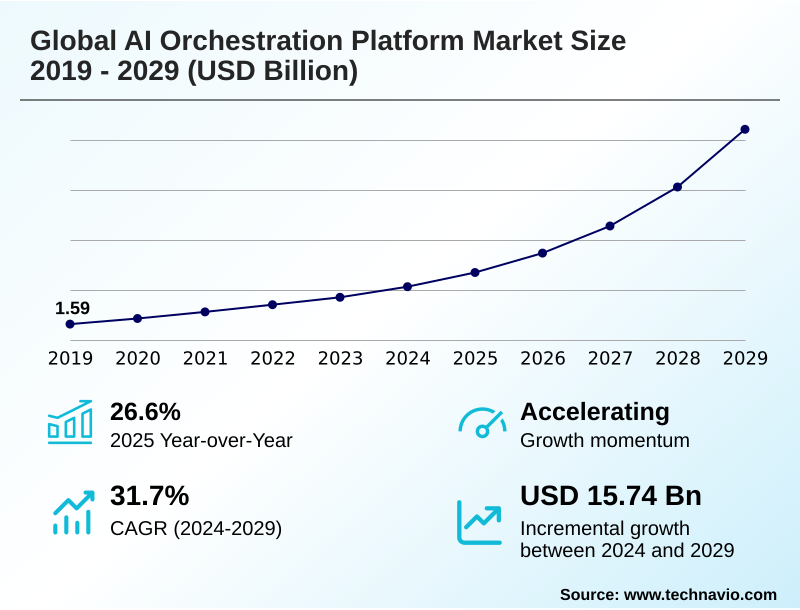

The ai orchestration platform market size is valued to increase by USD 15.74 billion, at a CAGR of 31.7% from 2024 to 2029. Increasing complexity and scale of AI models will drive the ai orchestration platform market.

Major Market Trends & Insights

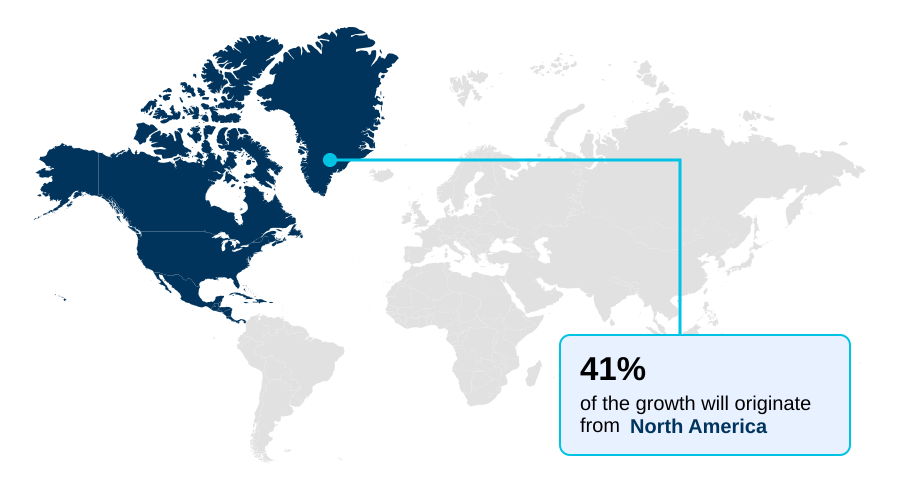

- North America dominated the market and accounted for a 41.4% growth during the forecast period.

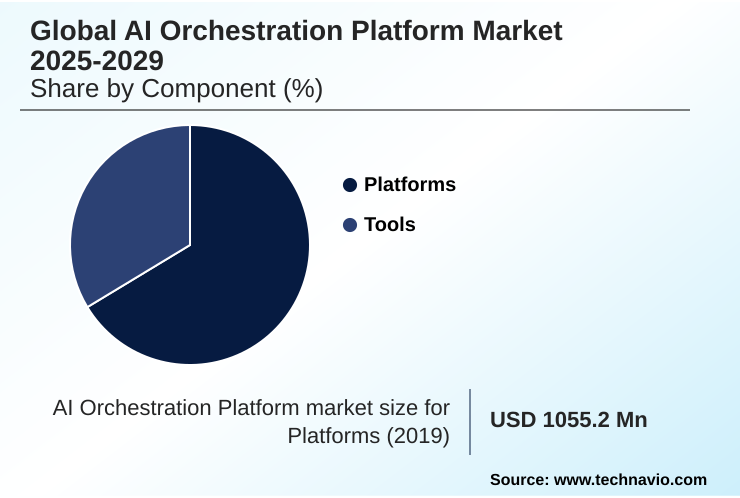

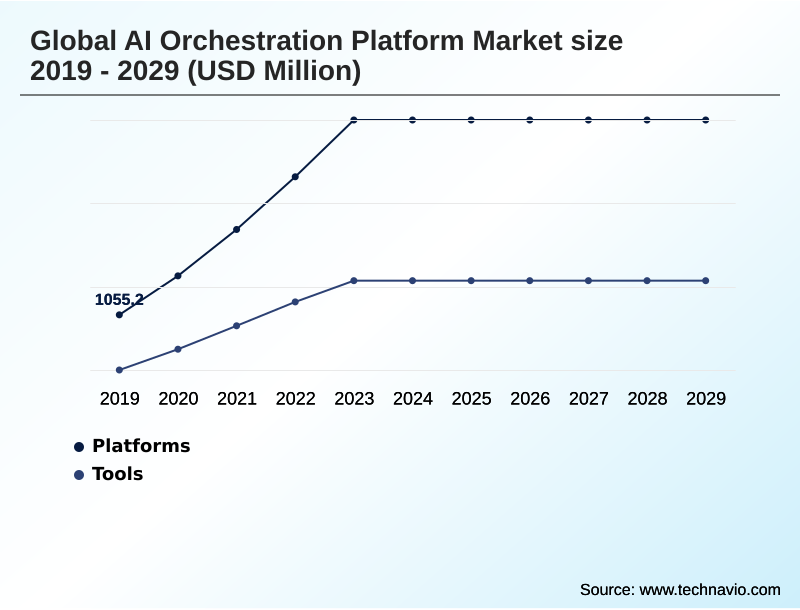

- By Component - Platforms segment was valued at USD 2.89 billion in 2023

- By Deployment - On-premises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 19.48 billion

- Market Future Opportunities: USD 15.74 billion

- CAGR from 2024 to 2029 : 31.7%

Market Summary

- The AI orchestration platform market is expanding rapidly as organizations move beyond experimental AI projects to scalable, production-grade operations. This shift is driven by the need to manage the complexities of the modern machine learning lifecycle, from data ingestion and model training to deployment and continuous monitoring.

- These platforms serve as the technological backbone for MLOps, enabling automated, reproducible, and auditable workflows that accelerate time-to-value and ensure model reliability. In the financial sector, for example, a bank deploying thousands of fraud detection models requires a robust system for AI orchestration for financial services.

- The platform automates the retraining and deployment of models based on new transaction data, monitors for performance degradation or drift, and provides a complete audit trail for every prediction. This level of centralized model governance and compliance is impossible to achieve manually at scale and is essential for meeting strict regulatory requirements.

- The emergence of generative AI has further intensified demand, creating a need for specialized orchestration to manage large language models, their intricate data pipelines, and their unique governance challenges, solidifying the market's critical role in enterprise technology stacks.

What will be the Size of the AI Orchestration Platform Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Orchestration Platform Market Segmented?

The ai orchestration platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Platforms

- Tools

- Deployment

- On-premises

- Cloud-based

- Application

- ML workflow

- LLM agent

- Data pipeline automation

- AI workflow scheduling

- Others

- Geography

- North America

- US

- Canada

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Component Insights

The platforms segment is estimated to witness significant growth during the forecast period.

Core platforms form the foundational layer of the market, providing an integrated software suite that functions as a comprehensive infrastructure abstraction layer.

These solutions deliver a unified control plane for managing multi-stage AI workflows and complex model dependency issues inherent in state-of-the-art AI models.

Key functionalities include a centralized model registry and a unified feature store, which are essential for managing the lifecycle of assets.

As the industry moves toward intelligent process automation and LLMOps platform adoption, these systems incorporate advanced AIOps integration and robust model risk management capabilities.

Through model validation automation, these platforms can reduce deployment errors by over 35%, ensuring that containerized AI workloads are both reliable and compliant from development through production, enabling effective AI pipeline orchestration.

The Platforms segment was valued at USD 2.89 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Orchestration Platform Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which is projected to account for over 41% of the market's incremental growth, driven by mature enterprise adoption of production AI systems.

In this region, there is a strong focus on AI governance frameworks, end-to-end MLOps, and time-to-value acceleration. Companies prioritize solutions with robust algorithmic bias detection and immutable model versioning.

Concurrently, the APAC region is expanding rapidly, with a projected growth rate exceeding 33%, fueled by cloud-native adoption and a focus on technologies like serverless model inference and inference latency optimization.

Effective AI pipeline monitoring and AI model observability are becoming standard requirements across all leading regions to ensure system reliability and performance.

Market Dynamics

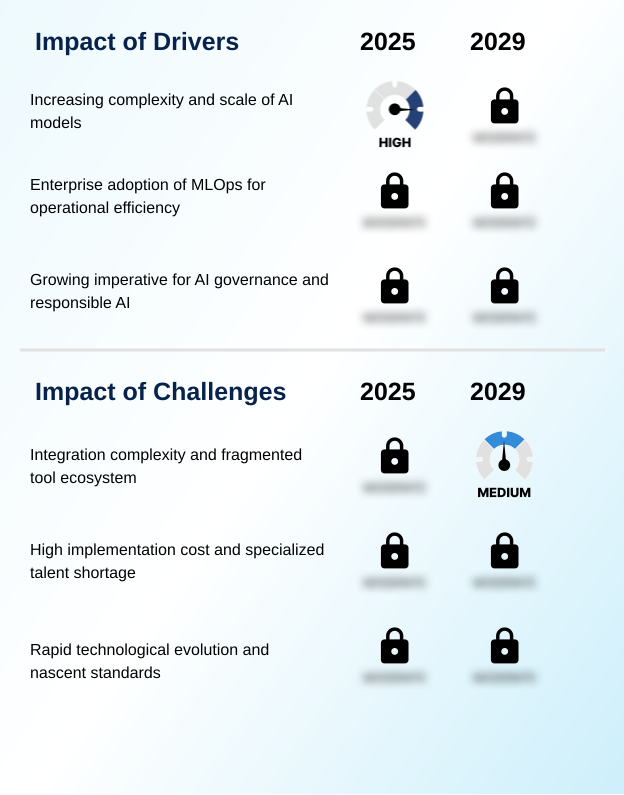

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The adoption of sophisticated AI orchestration platforms is accelerating as enterprises focus on enterprise MLOps for operational efficiency. A core objective is the end-to-end AI model lifecycle automation, which involves streamlining ML workflow with automation and implementing robust CI/CD integration for machine learning.

- Organizations are actively automating AI model deployment pipelines and optimizing AI infrastructure with orchestration to achieve scalable operations. This includes managing GPU clusters for AI training and using a serverless AI model serving platform for efficient inference. A major focus is on AI orchestration for large language models, which requires orchestrating retrieval-augmented generation workflows and complex generative AI applications.

- This has given rise to the need for LLM agent orchestration in enterprise settings. Centralized model governance and compliance is paramount, driving demand for automating AI governance and compliance and implementing AI orchestration for responsible AI principles. These AI model lifecycle management tools provide the necessary AI infrastructure resource management and AI workflow scheduling and management.

- The market is also seeing specialization, with dedicated solutions for AI orchestration for financial services and AI orchestration in the healthcare sector. Data pipeline automation for machine learning is foundational, while hybrid cloud MLOps platform features enable multi-cloud AI workload portability and support for AI workload management for on-premises deployments.

- Companies using these integrated systems often see regulatory reporting cycles shorten by more than half compared to those using fragmented, manual approaches.

What are the key market drivers leading to the rise in the adoption of AI Orchestration Platform Industry?

- The increasing complexity and computational scale of modern artificial intelligence models serves as a primary market driver.

- The drive for MLOps lifecycle automation is a primary market catalyst, enabling enterprise-grade AI deployment in high-stakes AI applications. Effective GPU resource management and computational resource allocation are critical for cost-effective model training and ensuring model reliability enhancement.

- Organizations are adopting hybrid cloud AI orchestration and Kubernetes-based AI scheduling to create a scalable AI infrastructure that supports distributed training optimization. These platforms are instrumental for responsible AI implementation, providing auditable machine learning processes that are essential for governance.

- The adoption of these systems improves resource utilization by up to 30% and reduces manual deployment errors by more than 50%, underscoring their value in complex operational environments.

What are the market trends shaping the AI Orchestration Platform Industry?

- A defining market trend is the emergence of specialized LLMOps, which provides orchestration capabilities tailored to the unique lifecycle of generative AI and large language models.

- A defining market trend is the rise of specialized capabilities for the generative AI lifecycle, leading to Data AI platform convergence. This shift supports complex foundation model operations through advanced prompt engineering pipelines and retrieval-augmented generation. The emergence of the autonomous agent framework, managed via workflow-as-code principles, enables sophisticated, multi-step task execution.

- These innovations in a data-centric AI platform provide a collaborative development environment that also facilitates AI workload portability across different infrastructures. Such platforms improve real-time inference serving latency by over 40% while also handling batch processing optimization. Furthermore, advancements in AI supercomputer management enhance processing for both training and inference tasks, with some systems achieving 2x faster model training cycles.

What challenges does the AI Orchestration Platform Industry face during its growth?

- Significant market growth is challenged by integration complexities that arise from a fragmented and diverse tool ecosystem.

- A significant market challenge is achieving seamless AI workflow automation across fragmented toolsets, which complicates the implementation of reproducible AI pipelines and MLOps standardization. Although a multi-cloud control plane promises flexibility, integrating disparate systems for CI/CD for machine learning and automated data lineage remains complex and can increase initial setup costs by over 50%.

- This fragmentation hinders the goals of achieving reduced manual overhead and consistent access control enforcement. Furthermore, implementing critical governance features like model drift monitoring, explainable AI integration, and regulatory audit trails requires significant engineering effort. This complexity is a barrier to adopting advanced practices like AI asset versioning and governance-as-code, with many firms reporting implementation timelines 40% longer than anticipated.

Exclusive Technavio Analysis on Customer Landscape

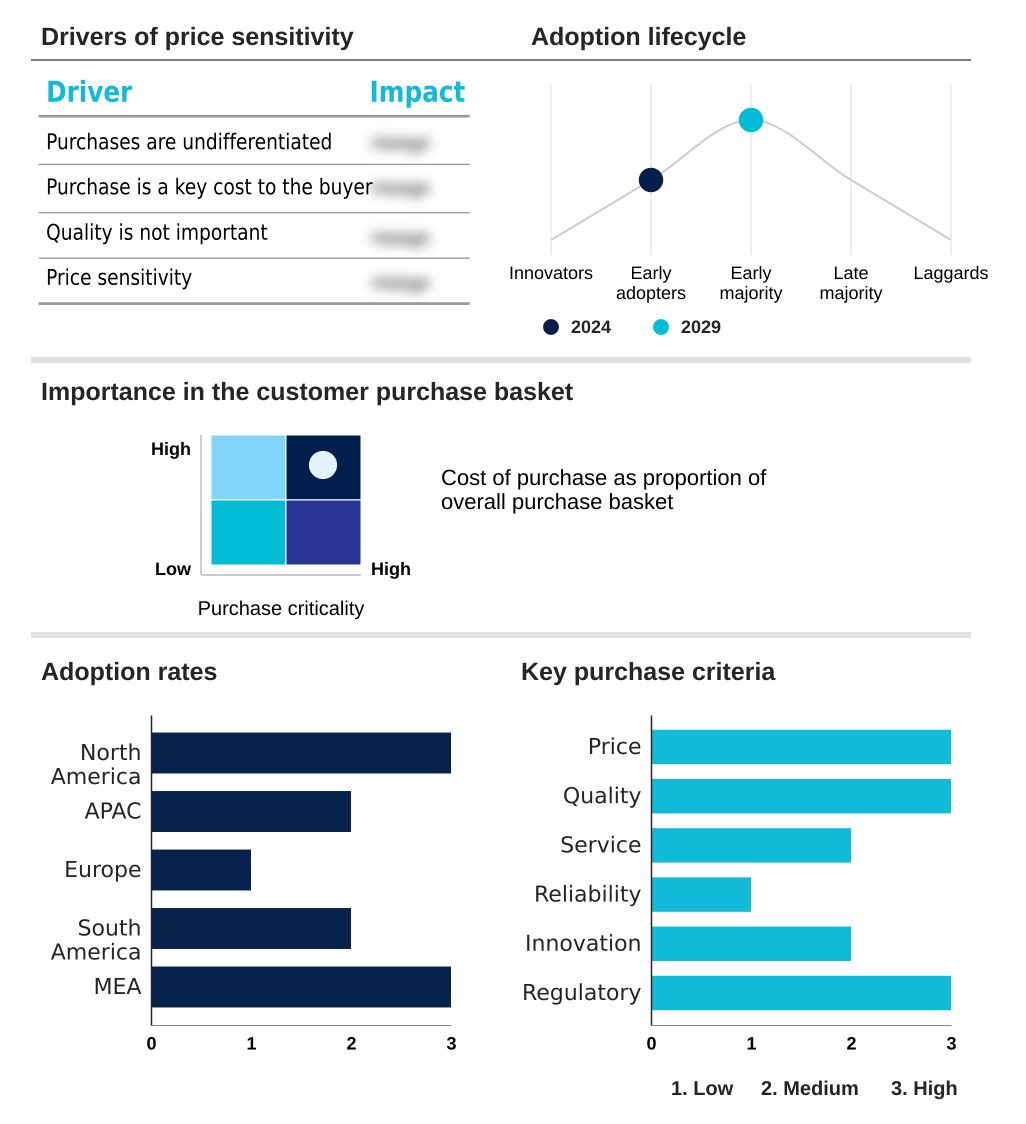

The ai orchestration platform market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai orchestration platform market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Orchestration Platform Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai orchestration platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - Providing a unified software framework for automating the end-to-end AI model lifecycle, ensuring scalability, governance, and operational efficiency from development to production.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- ActiveEon SAS

- Amazon.com Inc.

- Apptio Inc.

- BMC Software Inc.

- Fujitsu Ltd.

- Google LLC

- HashiCorp Inc.

- Hewlett Packard

- IBM Corp.

- Microsoft Corp.

- New Relic Inc.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

- TIBCO Software Inc.

- VMware Inc.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai orchestration platform market

- In May, 2025, Nvidia announced its acquisition of Run.ai, a company specializing in orchestrating AI workloads and managing GPU resources across both on-premises data centers and cloud environments.

- In February, 2025, GitLab announced a deeper native integration with DVC, an open-source data version control tool, reinforcing the convergence of software development and machine learning workflows.

- In November, 2024, Amazon Web Services launched Agents for Amazon Bedrock, a managed service created specifically to orchestrate multi-step generative AI applications, enabling them to interact with enterprise data and APIs.

- In September, 2024, Databricks announced its acquisition of MosaicML, a company specializing in technology to make the training of large-scale AI models more cost-effective and efficient.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Orchestration Platform Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 266 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 31.7% |

| Market growth 2025-2029 | USD 15742.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 26.6% |

| Key countries | US, Canada, China, India, Japan, South Korea, Australia, Germany, UK, France, Brazil, Argentina, Saudi Arabia and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI orchestration market is defined by a push toward comprehensive MLOps lifecycle automation and AI workflow automation, which are critical for enterprise-grade AI deployment. Effective GPU resource management, Kubernetes-based AI scheduling, and distributed training optimization are central to managing production AI systems, especially for high-stakes AI applications.

- A unified feature store and centralized model registry with immutable model versioning and automated data lineage support this process. The rise of the LLMOps platform is driving demand for prompt engineering pipelines and retrieval-augmented generation, while AIOps integration and intelligent process automation support broader efficiency goals.

- For governance, AI governance frameworks with model risk management, regulatory audit trails, and algorithmic bias detection are crucial, often supported by explainable AI integration. The technological backbone includes a multi-cloud control plane for hybrid cloud AI orchestration, enabling containerized AI workloads and CI/CD for machine learning.

- This focus on operational excellence, which improves processing times by over 30%, is geared toward optimizing both real-time inference serving and batch processing optimization, reducing inference latency optimization and ensuring robust model drift monitoring within an autonomous agent framework adhering to workflow-as-code principles.

What are the Key Data Covered in this AI Orchestration Platform Market Research and Growth Report?

-

What is the expected growth of the AI Orchestration Platform Market between 2025 and 2029?

-

USD 15.74 billion, at a CAGR of 31.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Platforms, and Tools), Deployment (On-premises, and Cloud-based), Application (ML workflow, LLM agent, Data pipeline automation, AI workflow scheduling, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing complexity and scale of AI models, Integration complexity and fragmented tool ecosystem

-

-

Who are the major players in the AI Orchestration Platform Market?

-

Accenture PLC, ActiveEon SAS, Amazon.com Inc., Apptio Inc., BMC Software Inc., Fujitsu Ltd., Google LLC, HashiCorp Inc., Hewlett Packard, IBM Corp., Microsoft Corp., New Relic Inc., Oracle Corp., Salesforce Inc., SAP SE, ServiceNow Inc., TIBCO Software Inc., VMware Inc. and Wipro Ltd.

-

Market Research Insights

- The market is driven by the need for MLOps standardization and end-to-end MLOps to achieve time-to-value acceleration in deploying state-of-the-art AI models. By providing an infrastructure abstraction layer, these platforms enable cost-effective model training and model reliability enhancement, with some users reporting a 30% reduction in computational resource allocation costs.

- Key functions include AI pipeline orchestration and AI pipeline monitoring to manage complex model dependency issues across multi-stage AI workflows, leading to reproducible AI pipelines. This approach facilitates a collaborative development environment and ensures AI workload portability across a scalable AI infrastructure.

- With a focus on responsible AI implementation and auditable machine learning, platforms offer access control enforcement and governance-as-code, including model behavior guardrails. Automating the generative AI lifecycle and foundation model operations improves AI model observability, while AI asset versioning is crucial for compliance.

- Strategic AI infrastructure optimization, including AI supercomputer management, can improve resource utilization by up to 45%, significantly reducing manual overhead.

We can help! Our analysts can customize this ai orchestration platform market research report to meet your requirements.

RIA -

RIA -