Ai Platform Cloud Service Market Size and Growth Forecast 2026-2030

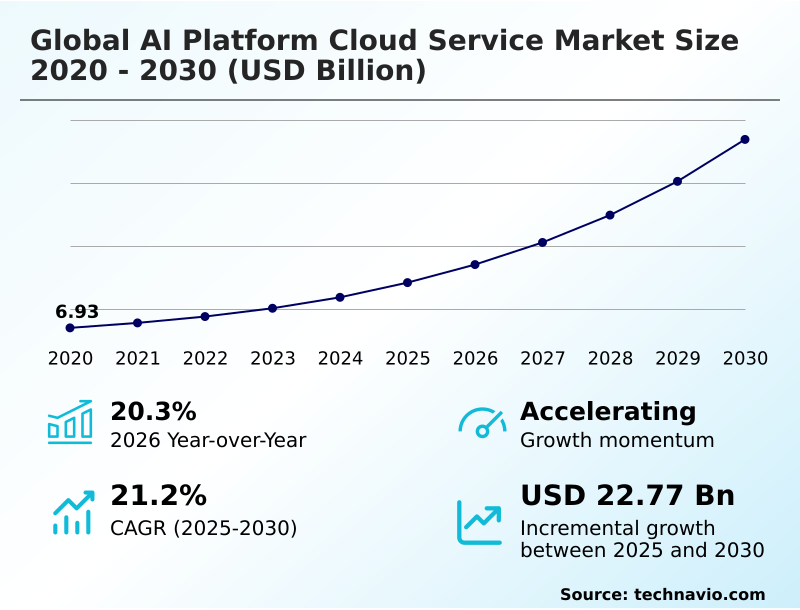

The Ai Platform Cloud Service Market size was valued at USD 14.13 billion in 2025 growing at a CAGR of 21.2% during the forecast period 2026-2030.

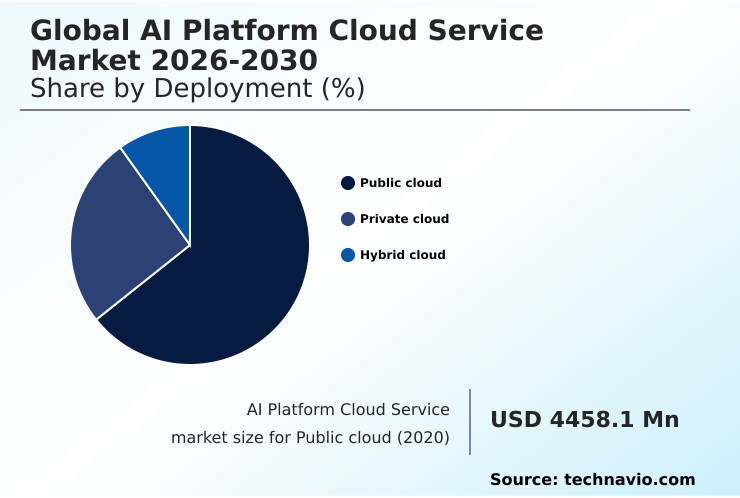

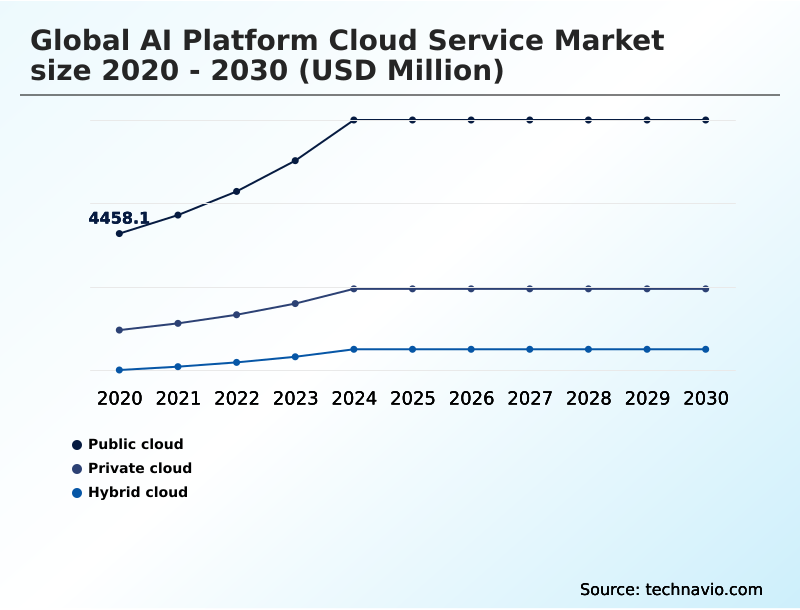

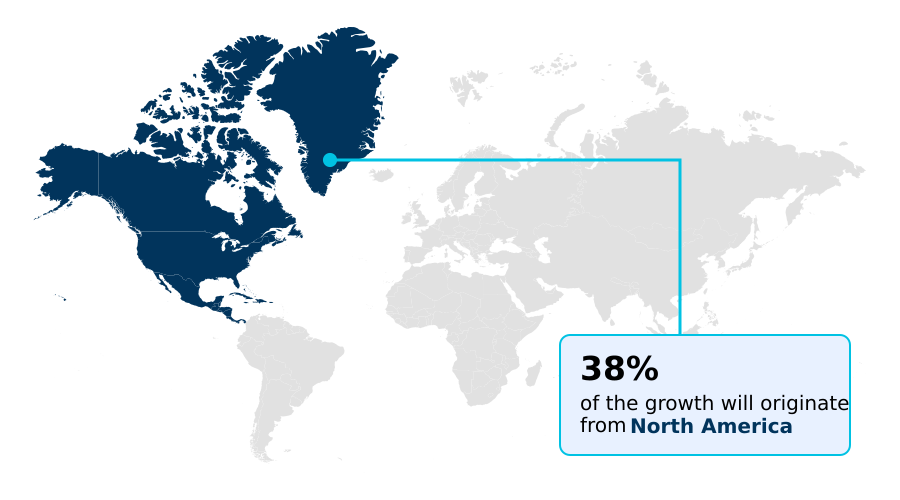

North America accounts for 37.6% of incremental growth during the forecast period. The Public cloud segment by Deployment was valued at USD 7.60 billion in 2024, while the IT and telecom segment holds the largest revenue share by End-user.

The market is projected to grow by USD 29.97 billion from 2020 to 2030, with USD 22.77 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Ai Platform Cloud Service Market Overview

The AI platform cloud service market is defined by a rapid enterprise shift toward AI-powered automation and intelligence embedded within core business processes. With North America accounting for 37.57% of the market, the region’s high adoption is driven by the availability of sophisticated AI platform as a service (AI PaaS) offerings. These platforms provide the crucial GPU-accelerated computing resources necessary for training complex models. A key dynamic is the move from standalone AI projects to comprehensive enterprise AI integration, where conversational AI platforms and predictive analytics engines are built into existing workflows. For instance, a large financial services firm implements AI ethics frameworks to govern its automated loan-processing system, using cloud-based tools to monitor for bias and ensure model fairness in compliance with fair lending laws. This integration not only improves decision accuracy but also provides auditable trails for regulators. The market's trajectory is shaped by the need for scalable, secure, and responsible AI deployment, making cloud platforms the default infrastructure for businesses aiming to maintain a competitive edge through data-driven innovation.

Drivers, Trends, and Challenges in the Ai Platform Cloud Service Market

The AI platform cloud service market's expansion is increasingly tied to the operational realities of enterprise adoption, where technical capabilities intersect with stringent regulatory frameworks. Automating MLOps pipelines using serverless AI services is no longer a niche practice but a core requirement for achieving agility.

However, procurement decisions are complicated by the challenges of multi-cloud AI strategy implementation and the need for securing AI workloads against adversarial attacks in the cloud. For instance, a European financial institution leveraging AutoML for rapid AI prototype development must simultaneously ensure every model is compliant with the EU AI Act's transparency requirements.

This necessitates building responsible AI applications with MLaaS that provide robust governance and explainability. The cost of training large language models on cloud platforms remains a significant budget item, prompting a focus on the ROI of adopting low-code AI development platforms to empower business units.

Integrating hybrid cloud AI with legacy enterprise systems proves to be a major hurdle, often requiring more investment in data engineering than the AI models themselves, a factor that significantly influences total cost of ownership calculations and vendor selection.

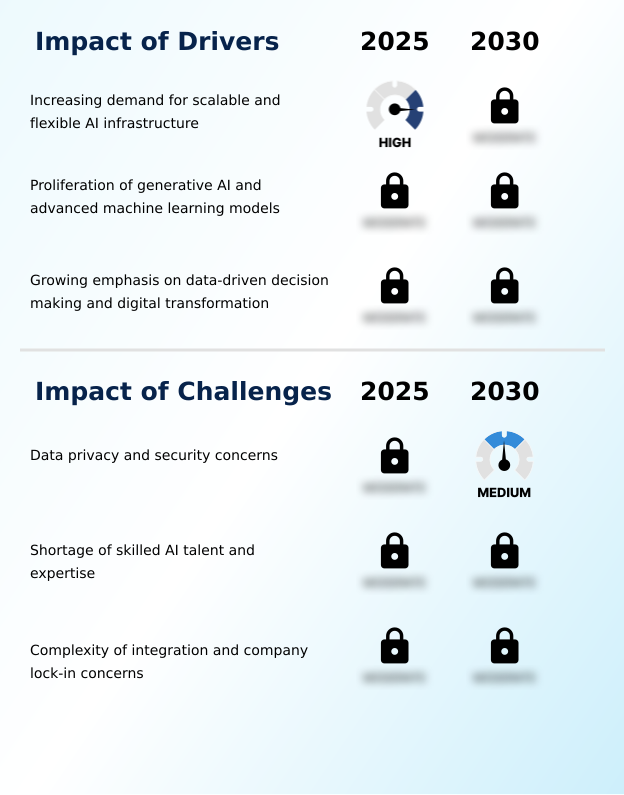

Primary Growth Driver: The increasing demand for scalable and flexible infrastructure is a primary driver for the AI platform cloud service market.

The market's primary driver is the proliferation of generative AI frameworks, which require the scalable AI architecture that only cloud platforms can provide.

The public cloud segment, which captured the majority of market revenue in 2024, continues to expand as organizations prioritize cloud-native AI development. This shift enables sophisticated MLOps lifecycle management, which is essential for deploying and maintaining models in production environments.

The intense computational demand for training and deploying these advanced models makes on-premises solutions impractical for most enterprises.

This reliance on the cloud solidifies the trend of data-driven decision making, as companies leverage accessible, powerful AI tools to gain a competitive advantage and automate complex business processes.

Emerging Market Trend: The democratization of AI through no-code and low-code platforms is a prominent trend. It is reshaping the AI platform cloud service market by lowering technical barriers to entry.

Key trends are reshaping market dynamics, with a clear move towards AI solution verticalization to meet specific industry needs. While general-purpose platforms are prevalent, there is a growing demand for industry-specific AI solutions, especially in regulated sectors like finance and healthcare.

This is coupled with the democratization of AI tools, where low-code AI development platforms enable business analysts to create and deploy models. Growth in APAC, with a CAGR of 23.3%, is outpacing Europe's 21.6% due to aggressive adoption of AI copilot integration in enterprise software.

This push for accessibility is balanced by an increasing emphasis on responsible AI principles, forcing vendors to embed governance features directly into their platforms to ensure ethical and compliant deployment.

Key Industry Challenge: Data privacy and security concerns represent a significant challenge affecting the growth of the AI platform cloud service market.

A significant challenge restraining market growth is the complexity of AI governance and compliance, particularly with regulations like GDPR. This forces enterprises to carefully vet platforms for robust security features and transparent data handling policies, slowing adoption. The difficulty of enterprise AI integration with legacy systems adds another layer of complexity and cost, often creating unforeseen hurdles in project timelines.

While technologies like federated learning systems offer potential solutions for privacy, their implementation remains complex. The market also faces a persistent AI talent gap mitigation issue, as the expertise required to manage secure and compliant AI systems is scarce.

Consequently, a core challenge for vendors is not only providing tools for adversarial attack detection but also simplifying the operational burden of maintaining a secure AI ecosystem.

Explore Full Market Dynamics Analysis Request Free Sample

Ai Platform Cloud Service Market Segmentation

The ai platform cloud service industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

The public cloud segment is estimated to witness significant growth during the forecast period.

The public cloud segment represents the largest share of the AI platform cloud service market, accounting for over 64% of deployments.

This dominance is driven by enterprises' need for on-demand access to highly scalable AI architecture and specialized hardware without significant capital expenditure.

Public cloud offerings excel in AI workload optimization, providing services like MLaaS and serverless AI inference that enable rapid model development and deployment.

The elasticity of these platforms is critical for handling the fluctuating computational demands of AI model monitoring and training.

For organizations executing an enterprise AI integration strategy, public cloud providers offer a comprehensive suite of managed services that accelerate time-to-value and reduce the operational burden on internal IT teams, aligning with standards like ISO/IEC 27017 for cloud security.

The Public cloud segment was valued at USD 7.60 billion in 2024 and showed a gradual increase during the forecast period.

Ai Platform Cloud Service Market by Region: North America Leads with 37.6% Growth Share

North America is estimated to contribute 37.6% to the growth of the global market during the forecast period.

The geographic landscape of the AI platform cloud service market is characterized by distinct regional growth patterns and priorities, with North America contributing 37.57% of the market.

This maturity is contrasted by APAC, the fastest-growing region, where demand for MLaaS and AI-powered network orchestration in the telecom sector is surging.

European adoption is heavily influenced by data residency controls under GDPR, driving demand for hybrid AI environments and sovereign cloud options.

Effective AI infrastructure management and a cohesive multi-cloud AI strategy are critical for multinationals navigating these fragmented regulatory and operational landscapes.

This regional divergence impacts procurement decisions, pushing global enterprises to seek platforms that offer flexible deployment models and robust, localized compliance features to manage data and AI workloads effectively across geographies.

Customer Landscape Analysis for the Ai Platform Cloud Service Market

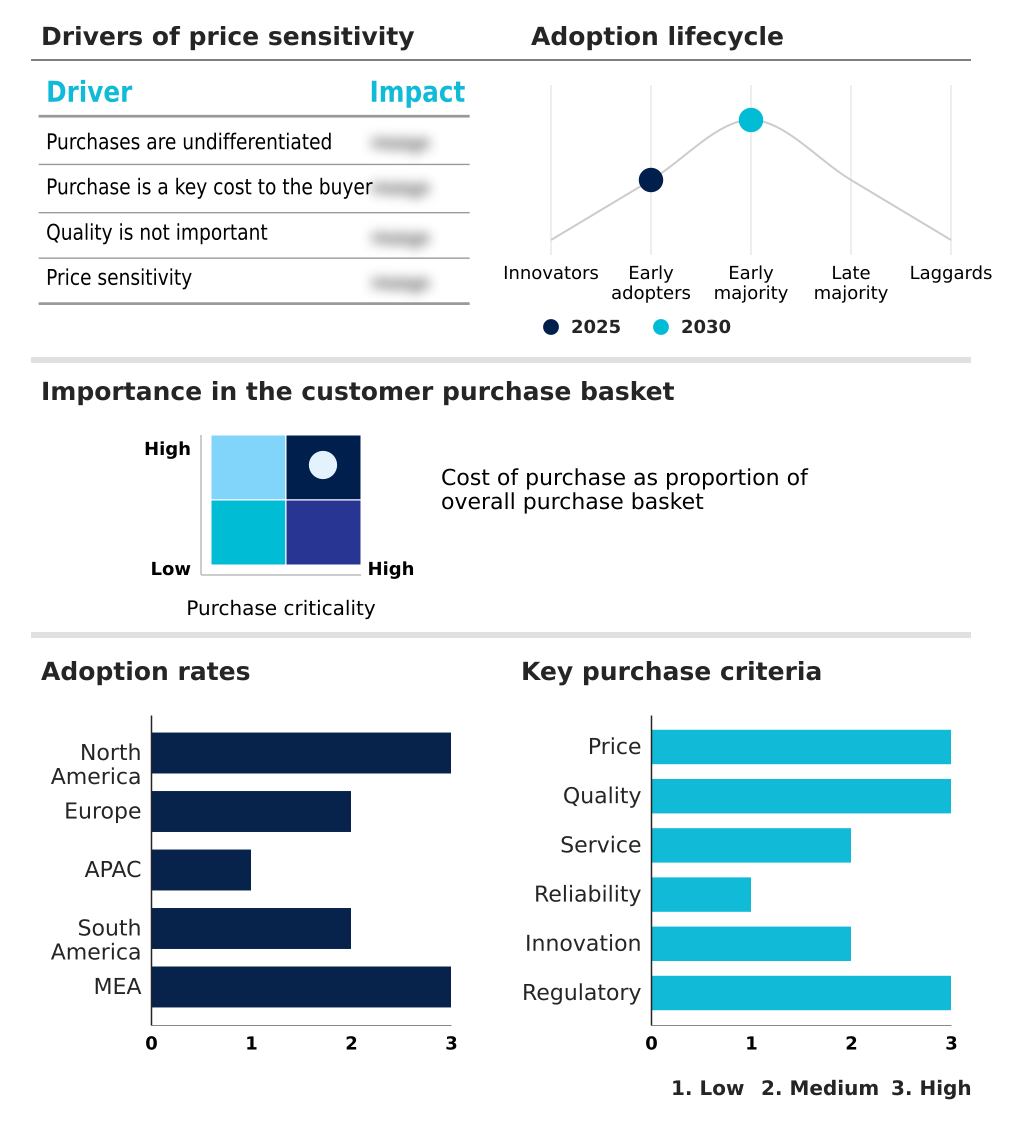

The ai platform cloud service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai platform cloud service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Ai Platform Cloud Service Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the ai platform cloud service market industry.

Alibaba Group Holding Ltd. - Providers offer comprehensive, scalable AI platforms enabling organizations to build, deploy, and manage solutions, from model development to enterprise-grade MLOps and governance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Group Holding Ltd.

- Amazon Web Services Inc.

- Baidu Inc.

- Cloudera Inc.

- Google LLC

- Hewlett Packard

- Informatica Inc.

- Infosys Ltd.

- IBM Corp.

- Microsoft Corp.

- NVIDIA Corp.

- OpenAI

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Snowflake Inc.

- Tencent Holdings Ltd.

- Wipro Ltd.

- Yandex NV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Ai Platform Cloud Service Market

- In November, 2024, Microsoft Corp. announced a strategic partnership with NVIDIA Corp. to offer dedicated, full-stack NVIDIA DGX Cloud infrastructure integrated directly within Azure AI Studio, enabling enterprise customers to train and fine-tune foundation models up to 50% faster.

- In January, 2025, Google LLC launched its new 'Vertex AI for Supply Chain' solution, a suite of industry-specific AI tools on its cloud platform, designed to provide demand forecasting, logistics optimization, and inventory management for retail and manufacturing clients, leveraging its Gemini models.

- In March, 2025, Amazon Web Services Inc. acquired 'ModelZ', a startup specializing in AI governance and model risk management, for an estimated USD 450 million, integrating its technology into Amazon SageMaker to enhance responsible AI capabilities, including automated bias detection and explainability reports.

- In May, 2025, IBM Corp. completed the expansion of its watsonx private cloud offering, enabling deployment of its generative AI and data platform on-premises across sovereign clouds in Europe and Asia-Pacific, backed by a USD 1.2 billion investment in hybrid cloud R&D.

Research Analyst Overview: Ai Platform Cloud Service Market

The AI platform cloud service market is exhibiting strong momentum, with year-over-year growth of 20.3% driven by enterprise demand for scalable MLOps lifecycle management and generative AI frameworks. Boardroom decisions now focus on the total cost of ownership of AI, weighing the benefits of AI-powered automation against the complexities of AI governance and compliance.

The forthcoming EU AI Act is a critical factor, compelling the adoption of explainable AI (XAI) toolkits and platforms that support responsible AI principles to mitigate regulatory risk. The technology stack is evolving rapidly, with a clear shift towards multimodal AI models and containerized AI workloads that can be deployed across hybrid cloud AI environments.

Within a high-throughput logistics center, digital twin simulation, powered by real-time data from IoT sensors and processed via computer vision APIs, is used to optimize routing and predictive maintenance, directly impacting operational margins. This practical application underscores the need for robust NLP pipelines and GPU-accelerated computing, making platform selection a strategic, not just tactical, decision.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Platform Cloud Service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.2% |

| Market growth 2026-2030 | USD 22773.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, Australia, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Ai Platform Cloud Service Market: Key Questions Answered in This Report

-

What is the expected growth of the Ai Platform Cloud Service Market between 2026 and 2030?

-

The Ai Platform Cloud Service Market is expected to grow by USD 22.77 billion during 2026-2030, registering a CAGR of 21.2%. Year-over-year growth in 2026 is estimated at 20.3%%. This acceleration is shaped by increasing demand for scalable and flexible ai infrastructure, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Public cloud, Private cloud, and Hybrid cloud), End-user (IT and telecom, Banking, Healthcare, Retail, and Others), Technology (Machine learning platform, Natural language processing, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Public cloud segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 37.6% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, Australia, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increasing demand for scalable and flexible ai infrastructure, which is accelerating investment and industry demand. The main challenge is data privacy and security concerns, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Ai Platform Cloud Service Market?

-

Key vendors include Alibaba Group Holding Ltd., Amazon Web Services Inc., Baidu Inc., Cloudera Inc., Google LLC, Hewlett Packard, Informatica Inc., Infosys Ltd., IBM Corp., Microsoft Corp., NVIDIA Corp., OpenAI, Oracle Corp., Salesforce Inc., SAP SE, Snowflake Inc., Tencent Holdings Ltd., Wipro Ltd. and Yandex NV. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Ai Platform Cloud Service Market Research Insights

Market dynamics are increasingly shaped by regulatory pressures and the strategic need for AI model interpretability. The emphasis on responsible AI governance, underscored by frameworks like the NIST AI Risk Management Framework, compels organizations to adopt platforms with robust transparency tools. This trend favors providers offering industry-specific AI solutions with built-in compliance modules.

For example, a healthcare provider implementing a diagnostic AI tool must ensure HIPAA compliance and clear model explainability, making a multi-cloud AI strategy complex without unified governance. Geographically, while North America leads, the growth in APAC is outpacing Europe, reflecting differing priorities in AI-ready infrastructure development.

Organizations are moving beyond basic services toward platforms that enable sophisticated AI-powered automation and support hybrid AI environments, balancing public cloud innovation with private cloud control.

We can help! Our analysts can customize this ai platform cloud service market research report to meet your requirements.

RIA -

RIA -