AI Robot Dog Market Size 2025-2029

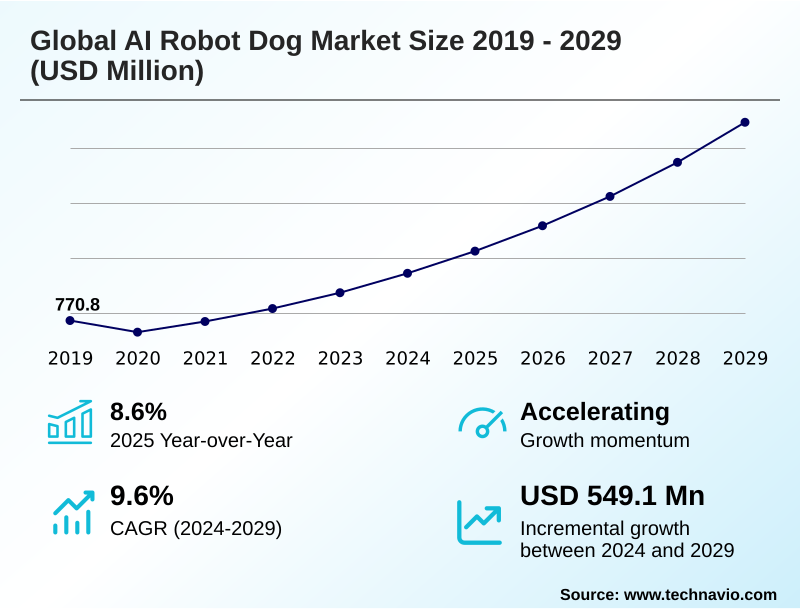

The ai robot dog market size is valued to increase by USD 549.1 million, at a CAGR of 9.6% from 2024 to 2029. Rapid advancements in AI and robotics technology will drive the ai robot dog market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.8% growth during the forecast period.

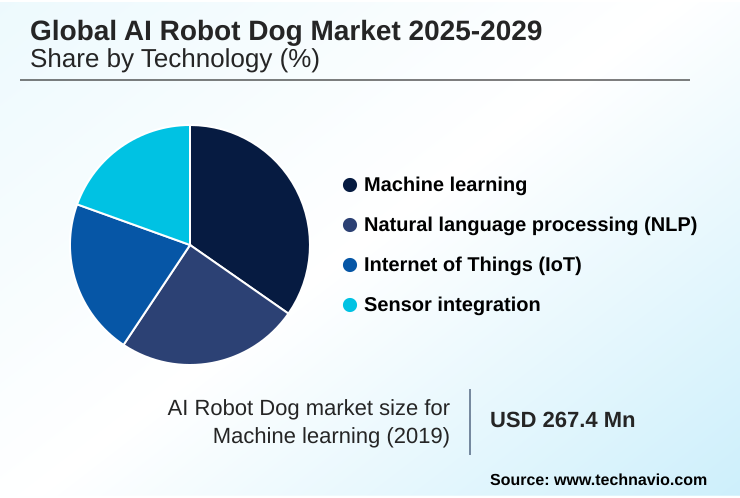

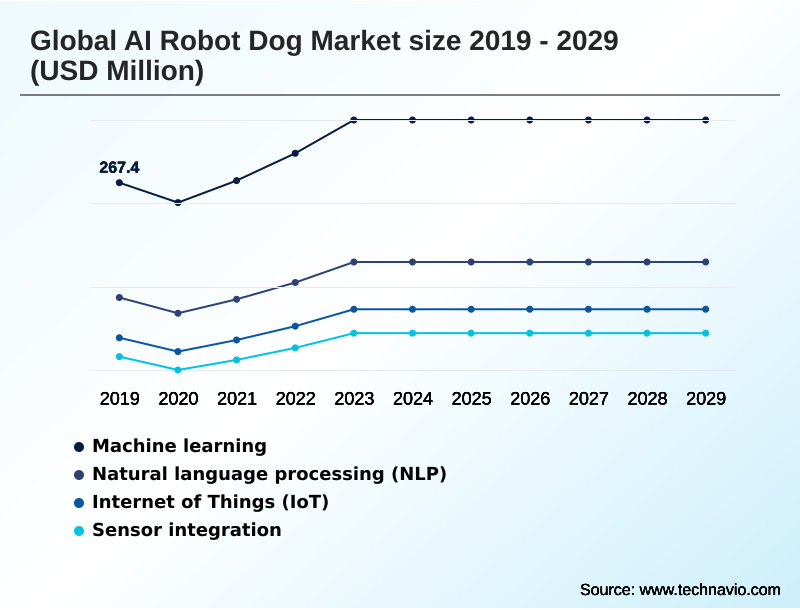

- By Technology - Machine learning segment was valued at USD 309.6 million in 2023

- By Service Type - Express delivery services segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 720.9 million

- Market Future Opportunities: USD 549.1 million

- CAGR from 2024 to 2029 : 9.6%

Market Summary

- The AI robot dog market is experiencing accelerated growth, transitioning from research projects to tangible assets across industries. This expansion is driven by advancements in artificial intelligence, sensor fusion, and mechatronic engineering, enhancing mobility, autonomy, and utility. Adoption is increasing for industrial inspection, security, and public safety, where the technology provides advantages over traditional methods.

- In the energy and manufacturing sectors, for instance, these robots are used for routine equipment inspection, detecting anomalies like gas leaks, and thermal monitoring, which minimizes downtime and reduces the need for human entry into hazardous areas. Key market players are catalyzing growth through innovation, expanding capabilities, and improving user-friendliness for non-specialist operators.

- Concurrent developments in foundational AI models are creating more intelligent robots capable of understanding natural language and performing complex tasks. This convergence of hardware maturation and sophisticated AI sets the stage for the next growth phase, where AI robot dogs become increasingly autonomous and integrated into core operational workflows of diverse industries.

What will be the Size of the AI Robot Dog Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Robot Dog Market Segmented?

The ai robot dog industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Machine learning

- Natural language processing (NLP)

- Internet of Things (IoT)

- Sensor integration

- Service type

- Express delivery services

- Regular parcel delivery

- Micro-mobility logistics

- End-user

- Industrial

- Commercial

- Military and defense

- Residential

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- Rest of World (ROW)

- APAC

By Technology Insights

The machine learning segment is estimated to witness significant growth during the forecast period.

Machine learning, and specifically deep reinforcement learning, serves as the cognitive engine for the AI robot dog market, enabling advanced autonomy.

Through AI-driven control algorithms and enhanced on-board processing power, these platforms achieve sophisticated dynamic obstacle avoidance and complex human-robot interaction models.

Innovations in sim-to-real transfer are critical, with recent academic frameworks demonstrating the ability to master walking gaits in minutes, a drastic reduction from previous training timelines. This progress is pivotal for applications in industrial inspection automation and hazardous environment operation.

As these systems are integrated into smart factory integration frameworks and used for tasks like construction site monitoring or last-mile delivery robotics, the underlying AI for robotics (AI4R) continues to drive practical, real-world capabilities and market expansion.

The Machine learning segment was valued at USD 309.6 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Robot Dog Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the AI robot dog market is increasingly shaped by the APAC region, which is set to expand at a rate nearly 15% faster than Europe, driven by advanced manufacturing and significant government investment in technology.

Countries like China and South Korea are at the forefront, fostering innovation in both industrial and consumer-grade models.

A recent strategic acquisition saw a South Korean firm take a 60% controlling stake in a leading US-based robotics company, underscoring the region's ambition. This activity highlights a focus on integrating advanced sensor integration and multi-modal sensor fusion.

Progress in developing a robust autonomous navigation stack and computer vision for robotics is enabling new applications in energy facility inspection and remote asset monitoring.

These collaborative robotic systems, leveraging proprioceptive sensor feedback and real-time kinematic positioning, are becoming crucial for companion robotics for elderly and smart home security, extending beyond industrial use.

Market Dynamics

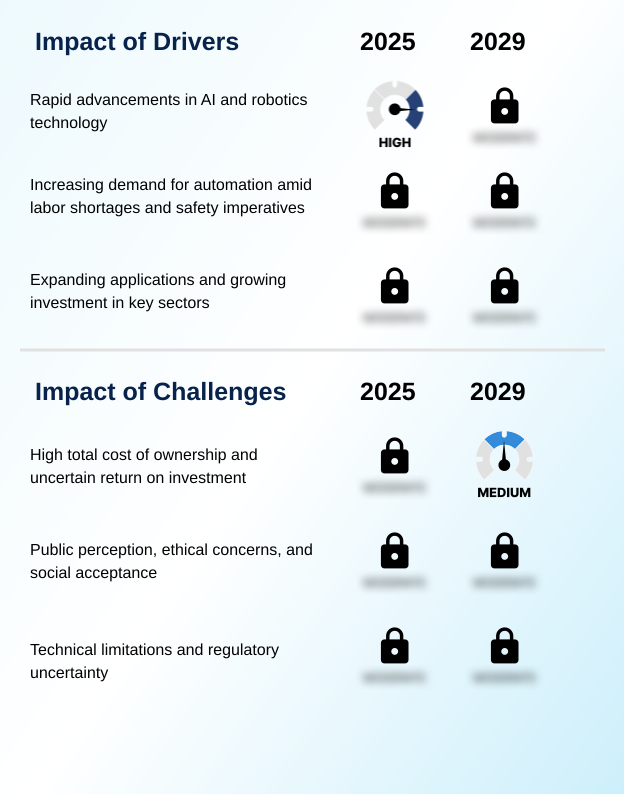

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions around the global AI robot dog market 2025-2029 increasingly involve a detailed analysis of quadrupedal robot vs wheeled robot mobility, especially for industrial applications where navigating complex terrain is critical.

- Businesses evaluating the cost of ownership for enterprise AI robot dogs must also consider the AI robot dog for industrial inspection ROI, which is influenced by factors like AI robot dog battery life and endurance limitations.

- As companies look to deploy AI robot dogs in construction sites, they face technical hurdles but also see opportunities for AI robot dogs for predictive maintenance tasks.

- The development of natural language processing for robot commands is making these systems more accessible, while training AI robot dogs with reinforcement learning and advanced sensor fusion techniques in quadrupedal robots are pushing performance boundaries. This is crucial for using AI robot dogs for last-mile delivery, which faces significant regulatory challenges for autonomous delivery robots.

- The industry is also exploring human-robot collaboration models in logistics to mitigate these issues. Meanwhile, the ethical implications of armed robotic dogs remain a contentious topic, influencing social acceptance of robots in public safety.

- As companies compare consumer vs industrial robot dogs, the ability to leverage generative AI applications in robotics control and develop applications on open-source robot platforms is a key differentiator, with platforms like the Unitree B2 industrial robot use cases demonstrating specialized capabilities beyond the well-known Boston Dynamics Spot payload integration capabilities or the Ghost Robotics Vision 60 for defense applications.

What are the key market drivers leading to the rise in the adoption of AI Robot Dog Industry?

- Rapid advancements in AI and robotics technology are a key driver of the market, enhancing the autonomy and capabilities of quadrupedal systems.

- Market growth is significantly driven by the dual pressures of labor shortages and a heightened focus on workplace safety, positioning AI robot dogs as powerful force-multiplying robotic systems.

- Companies are deploying these platforms for advanced robotic inspection and autonomous data collection in hazardous environments, reducing human risk. For example, one global aluminum producer is now trialing two prototype robots for high-risk inspection tasks.

- In public safety robotics, their role as a law enforcement de-escalation tool is growing, with one major US police department adopting a robot for high-risk tactical support.

- These mobile observation platforms, equipped with high-endurance battery packs and running on robust robotic operating systems (ROS), are becoming essential for autonomous perimeter security and logistics automation solutions.

- The data gathered also feeds predictive maintenance algorithms, enhancing operational uptime and delivering a clear return on investment.

What are the market trends shaping the AI Robot Dog Industry?

- A dominant market trend is the evolution of the quadruped from a specialized device into a versatile, multi-purpose platform. This shift allows for customization with a wide array of payloads to address a multitude of tasks.

- Key trends in the AI robot dog market center on the evolution of quadrupeds into versatile, multi-purpose platforms through an expanding robotic payload ecosystem. The introduction of ruggedized hardware designs with IP-rated enclosure systems is enabling deployment in harsh industrial settings.

- For instance, new industrial models offer a 100% increase in sustained load capacity and a 200% boost in endurance, making them suitable for demanding infrastructure inspection robot roles. This specialization is supported by innovations like hybrid locomotion systems, which combine wheeled efficiency with legged agility.

- The development of cloud-native fleet management software, often using real-time location systems (RTLS), allows for the coordination of entire fleets, supporting Robotics-as-a-Service (RaaS) models. This trend, coupled with open-source robotics development, is transforming the technology from a niche product into a flexible asset for warehouse automation robotics and entertainment robotics platforms.

What challenges does the AI Robot Dog Industry face during its growth?

- The high total cost of ownership and uncertain return on investment present a key challenge affecting industry growth and widespread adoption.

- Significant challenges constrain the market, primarily revolving around public perception and ethical concerns, especially regarding the use of a quadrupedal unmanned ground vehicle in public-facing or security roles. The prospect of AI-enabled weapon systems on these platforms raises profound ethical questions that impact social acceptance for roles in tactical reconnaissance or as an explosive ordnance disposal (EOD) robot.

- Technical limitations also persist; many man-portable robotic platforms have an operational uptime of only a few hours, insufficient for persistent surveillance.

- Furthermore, while legged locomotion systems are superior in complex terrain, the technology's high cost and the difficulty in demonstrating a clear ROI for applications in search and rescue robotics or mining automation platforms remain substantial barriers for many organizations, slowing widespread adoption.

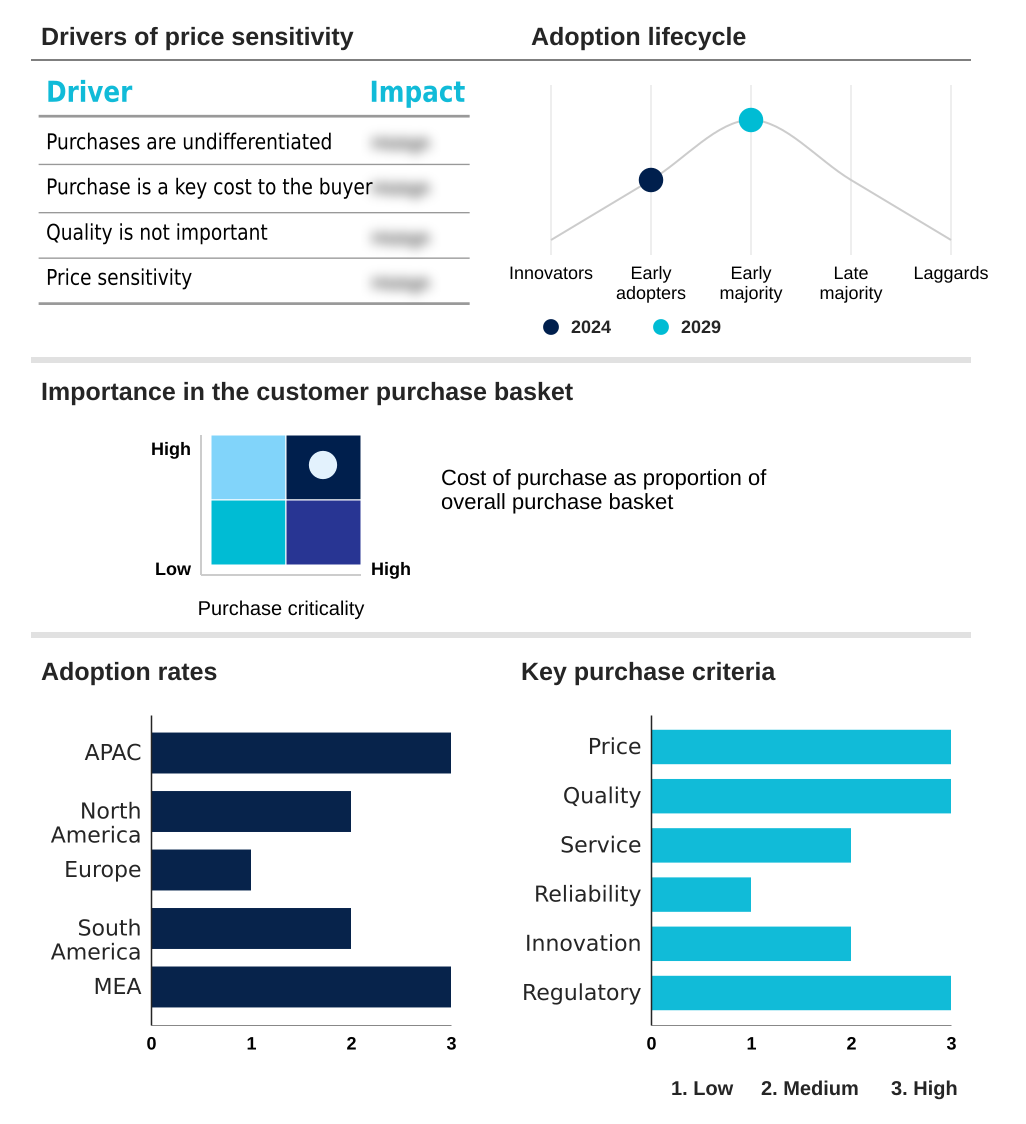

Exclusive Technavio Analysis on Customer Landscape

The ai robot dog market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai robot dog market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Robot Dog Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai robot dog market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ageless Innovation - Key offerings center on highly mobile, quadrupedal robots designed for autonomous data capture, inspection, and operations in complex and unstructured environments across various industrial sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ageless Innovation

- ANYbotics

- Boston Dynamics Inc.

- Ghost Robotics Corp.

- HangZhou YuShu Technology Co. Ltd.

- KEYi Robot

- Leju Shenzhen Robotics Co.Ltd.

- Mech Mind Robotics Technologies Co Ltd.

- NOVVA

- Sanbot Robot Co. Ltd.

- Sarcos Technology and Robotics Corp.

- Sega Corp.

- Tombot Inc.

- TOMY International Inc.

- WowWee Group Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai robot dog market

- In April 2025, Evri announced a UK-first trial in partnership with the Swiss AI firm RIVR to utilize a quadrupedal robot to assist human couriers with last-mile parcel delivery.

- In February 2025, Boston Dynamics partnered with the Robotics and AI Institute to establish a shared reinforcement learning training pipeline, aiming to develop dynamic and broadly applicable mobile manipulation behaviors for its robotic platforms.

- In January 2025, the Colombian government reinforced its commitment to digital transformation by publishing a strategic plan prioritizing the use of AI, IoT, and big data to modernize institutional processes across the public sector.

- In September 2024, Boston Dynamics released a major software update for its Spot robot, which included the full integration of new specialized sensor payloads like the Fluke SV600 acoustic imaging sensor and the Leica BLK ARC laser scanner for enhanced industrial data collection.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Robot Dog Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.6% |

| Market growth 2025-2029 | USD 549.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 8.6% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Colombia, UAE, Saudi Arabia, Israel, South Africa and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global AI robot dog market 2025-2029 is defined by relentless technological advancement, where quadrupedal unmanned ground vehicles are evolving into highly autonomous platforms. Core to this are high-torque density actuators and sophisticated legged locomotion systems, governed by AI-driven control algorithms.

- Deep reinforcement learning and sim-to-real transfer techniques are enabling these machines to perform complex tasks, from industrial inspection using specialized sensor payloads to tactical missions with AI-enabled weapon systems. For instance, new industrial models demonstrate a 100% increase in sustained load capacity, directly impacting operational efficiency.

- This capability informs boardroom decisions on capital expenditure, as companies weigh the benefits of autonomous data collection and predictive maintenance algorithms against integration costs. The shift toward a robotic payload ecosystem, supported by cloud-native fleet management and digital twin data integration, signifies a move toward scalable, enterprise-wide deployments.

- As such, the market is not just about hardware but about creating an integrated network of collaborative robotic systems for diverse, mission-critical applications.

What are the Key Data Covered in this AI Robot Dog Market Research and Growth Report?

-

What is the expected growth of the AI Robot Dog Market between 2025 and 2029?

-

USD 549.1 million, at a CAGR of 9.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Machine learning, Natural language processing (NLP), Internet of Things (IoT), Sensor integration), Service Type (Express delivery services, Regular parcel delivery, Micro-mobility logistics), End-user (Industrial, Commercial, Military and defense, Residential) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid advancements in AI and robotics technology, High total cost of ownership and uncertain return on investment

-

-

Who are the major players in the AI Robot Dog Market?

-

Ageless Innovation, ANYbotics, Boston Dynamics Inc., Ghost Robotics Corp., HangZhou YuShu Technology Co. Ltd., KEYi Robot, Leju Shenzhen Robotics Co.Ltd., Mech Mind Robotics Technologies Co Ltd., NOVVA, Sanbot Robot Co. Ltd., Sarcos Technology and Robotics Corp., Sega Corp., Tombot Inc., TOMY International Inc. and WowWee Group Ltd.

-

Market Research Insights

- The market dynamics for AI robot dogs are shaped by a push for tangible operational gains and measurable business outcomes. The introduction of platforms with a 100% increase in sustained load capacity and a 200% improvement in endurance directly addresses industrial demands for higher productivity in logistics automation solutions.

- This evolution is enabling new high-risk tactical support roles where mobile observation platforms must carry heavier payloads for longer durations. Furthermore, the focus on smart factory integration is driving adoption, as these systems provide a flexible alternative to fixed automation.

- The development of a robust robotic payload ecosystem, supported by RaaS models and open-source robotics development, allows companies to customize platforms for specific tasks, from infrastructure inspection to entertainment robotics, thereby improving ROI and expanding the addressable market for tele-operated ground drones and warehouse automation robotics.

We can help! Our analysts can customize this ai robot dog market research report to meet your requirements.

RIA -

RIA -