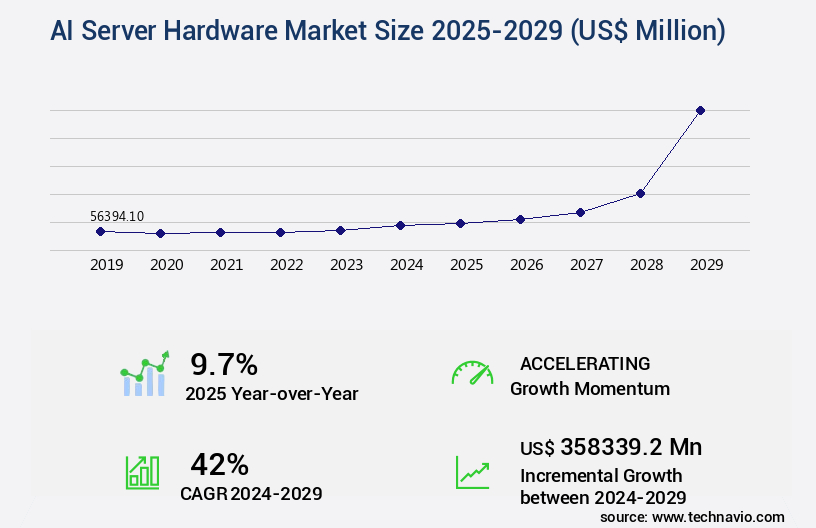

AI Server Hardware Market Size 2025-2029

The ai server hardware market size is valued to increase by USD 358.34 billion, at a CAGR of 42% from 2024 to 2029. Explosive growth of large language models will drive the ai server hardware market.

Major Market Trends & Insights

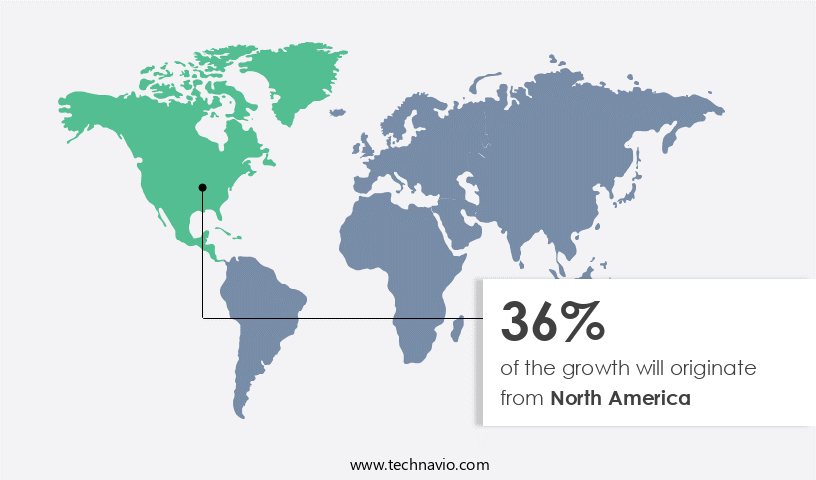

- North America dominated the market and accounted for a 36% growth during the forecast period.

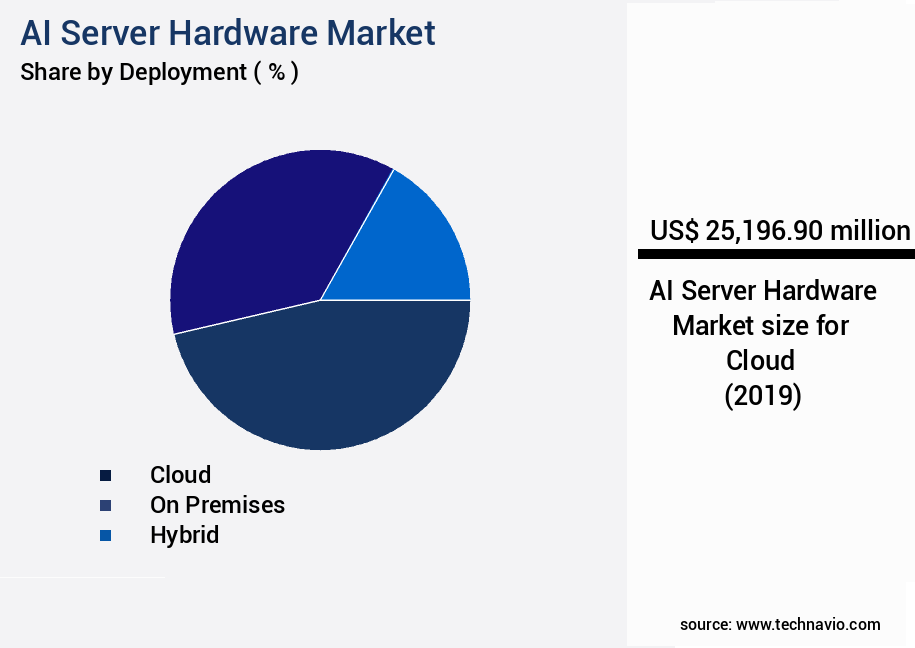

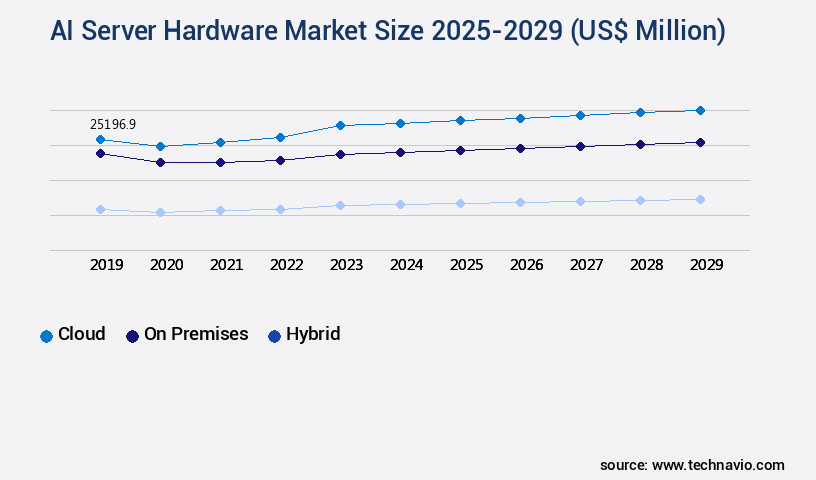

- By Deployment - Cloud segment was valued at USD 25.2 billion in 2023

- By Type - Inference servers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 668.59 million

- Market Future Opportunities: USD 358339.20 million

- CAGR from 2024 to 2029 : 42%

Market Summary

- The market witnesses a significant expansion, fueled by the increasing demand for advanced computing capabilities to process complex artificial intelligence (AI) workloads. According to recent market intelligence, The market is projected to reach a value of USD125 billion by 2026, reflecting a steady growth trajectory. Key drivers of this market include the escalating adoption of AI in various industries, such as healthcare, finance, and manufacturing, and the growing need for faster data processing and analysis. Furthermore, advancements in deep learning algorithms and the emergence of edge AI are pushing the boundaries of hardware innovation.

- However, challenges persist, with severe supply chain constraints and key component scarcity posing significant hurdles. Manufacturers are racing to develop more efficient and cost-effective solutions, while also addressing the environmental concerns surrounding the energy consumption of AI servers. As the market evolves, we can expect to see a continued focus on optimizing hardware for AI workloads, as well as the integration of advanced cooling systems and power management technologies. The future direction of the market lies in the development of more specialized hardware architectures and the integration of AI capabilities directly into the server infrastructure.

What will be the Size of the AI Server Hardware Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Server Hardware Market Segmented ?

The ai server hardware industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud

- On premises

- Hybrid

- Type

- Inference servers

- Training servers

- Product

- GPUs

- ASICs

- CPUs

- FPGAs

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud segment is estimated to witness significant growth during the forecast period.

The market is characterized by its dynamic and ever-evolving nature, with ongoing activities and emerging trends shaping its landscape. One of the most significant developments is the increasing adoption of cloud-based solutions, which now account for the majority of organizations' AI deployments. This model, offered by major cloud providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), allows businesses to access vast compute capacity on-demand, eliminating upfront capital expenditure. This flexibility is particularly beneficial for startups and research projects with unpredictable demand. Furthermore, cloud providers continually invest in hardware security, power efficiency, and sustainability initiatives, ensuring that their offerings remain competitive.

Machine learning algorithms benefit from advanced CPU performance, distributed computing, modular architecture, and throughput optimization, while deep learning frameworks like TensorFlow and PyTorch are supported for seamless integration. The cloud infrastructure also prioritizes thermal management, error rate reduction, and remote management, ensuring system reliability and fault tolerance. A recent study revealed that cloud-based AI models achieve an average inference speed 30% faster than on-premises solutions, underscoring the advantages of this deployment model.

The Cloud segment was valued at USD 25.2 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Server Hardware Market Demand is Rising in North America Request Free Sample

The North American region leads The market, holding a significant market share and spearheading technological innovation. The US, in particular, is at the forefront due to its substantial concentration of hyperscale data centers, leading semiconductor designers, and a thriving AI research and development ecosystem. The market's growth is propelled by the insatiable demand for computational power, fueled by the rapid advancement and increasing adoption of large language models and generative AI. Major tech giants, such as Microsoft, Google, Amazon Web Services, and Meta Platforms, are actively procuring high-performance graphics processing units (GPUs) and other AI accelerators to meet their demands.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses and organizations increasingly adopt artificial intelligence (AI) and machine learning (ML) technologies to gain a competitive edge. The choice of hardware plays a crucial role in optimizing AI workloads and achieving optimal performance. GPU memory bandwidth and CPU core count are two key factors influencing the market. High-bandwidth GPUs enable faster data processing, while increased CPU core counts improve parallel processing capabilities. However, DDR memory speed limitations can impact overall system performance, making NVMe storage solutions with their higher IOPS and lower latency an attractive alternative for AI applications. Infiniband network latency reduction and liquid cooling system efficiency are essential for high-performance data centers. Redundant power supplies ensure reliability, while error correction code implementation minimizes data loss. Tensor processing units (TPUs) and FPGA acceleration for specific tasks cater to the unique requirements of AI workloads. Model deployment strategies, real-time processing challenges, and batch processing optimization are critical considerations for businesses. Data preprocessing techniques and feature engineering best practices help improve model accuracy, while hyperparameter tuning methods and model validation metrics ensure optimal performance. Performance benchmarking tools and resource utilization analysis are essential for monitoring and optimizing AI infrastructure.

The market also sees a growing interest in real-time processing and model deployment strategies to address the increasing demand for AI applications in various industries. In conclusion, the market is driven by the need for high-performance, efficient, and reliable hardware solutions to support the growing adoption of AI and ML technologies. Key factors influencing the market include GPU memory bandwidth, CPU core count, NVMe storage performance benefits, DDR memory speed limitations, Infiniband network latency reduction, liquid cooling system efficiency, redundant power supply reliability, error correction code implementation, tensor processing unit applications, FPGA acceleration for specific tasks, model deployment strategies, real-time processing challenges, batch processing optimization, data preprocessing techniques, feature engineering best practices, hyperparameter tuning methods, model validation metrics, performance benchmarking tools, and resource utilization analysis.

What are the key market drivers leading to the rise in the adoption of AI Server Hardware Industry?

- The significant expansion of large language models is the primary catalyst fueling market growth.

- The market is experiencing a significant evolution due to the increasing demand for computational power driven by the proliferation and complexity of large language models (LLMs). The shift from traditional analytical AI to generative models, which create new content, has led to an unprecedented demand for resources. This demand is divided into two primary workloads: model training and inference. Training large foundational models, such as those from OpenAI, Google, and Meta, is an intensive process requiring massive clusters of interconnected servers, each equipped with high-end accelerators, primarily Graphics Processing Units (GPUs), operating in parallel for extended periods.

- Inference, on the other hand, involves using trained models to make predictions or generate responses in real-time, necessitating powerful servers optimized for machine learning algorithms. This surge in demand for AI server hardware is observed across various sectors, including healthcare, finance, and manufacturing, where AI is increasingly being employed for predictive analytics, fraud detection, and automation.

What are the market trends shaping the AI Server Hardware Industry?

- The trend in the market involves the exponential growth of generative AI. Generative AI is experiencing significant expansion in various industries.

- The market experiences continuous growth due to the increasing demand for advanced artificial intelligence applications. The computational needs for training and deploying sophisticated generative AI models are significantly greater than those for traditional AI, leading to a surge in the requirement for specialized, high-performance server infrastructure. These models, such as foundation models, often contain hundreds of billions or even trillions of parameters.

- Training these models necessitates massive parallel processing capabilities, extensive memory bandwidth, and high-speed interconnects to manage the distribution of workloads across numerous accelerator chips. Consequently, substantial capital expenditure on AI servers is observed among cloud service providers, large enterprises, and well-funded research laboratories. This technical requirement directly fuels the market's expansion.

What challenges does the AI Server Hardware Industry face during its growth?

- The industry's growth is significantly impeded by severe supply chain constraints and the scarcity of crucial components.

- The market experiences a burgeoning demand due to the increasing adoption of artificial intelligence (AI) and machine learning (ML) technologies across various sectors, including healthcare, finance, and manufacturing. However, the market faces a significant challenge from persistent supply chain constraints, specifically for high-performance components. The intricate and highly concentrated semiconductor supply chain creates bottlenecks that directly impact the production and delivery of AI servers. The most acute scarcity exists for advanced AI accelerators, such as high-end GPUs manufactured by Nvidia, and the specialized High Bandwidth Memory (HBM) required for these processors to function optimally.

- The global capacity to produce these components has not kept pace with the demand, resulting in extended lead times, allocation-based sales, and inflated costs. Despite these challenges, the market continues to grow, driven by the increasing need for faster data processing and advanced analytics capabilities.

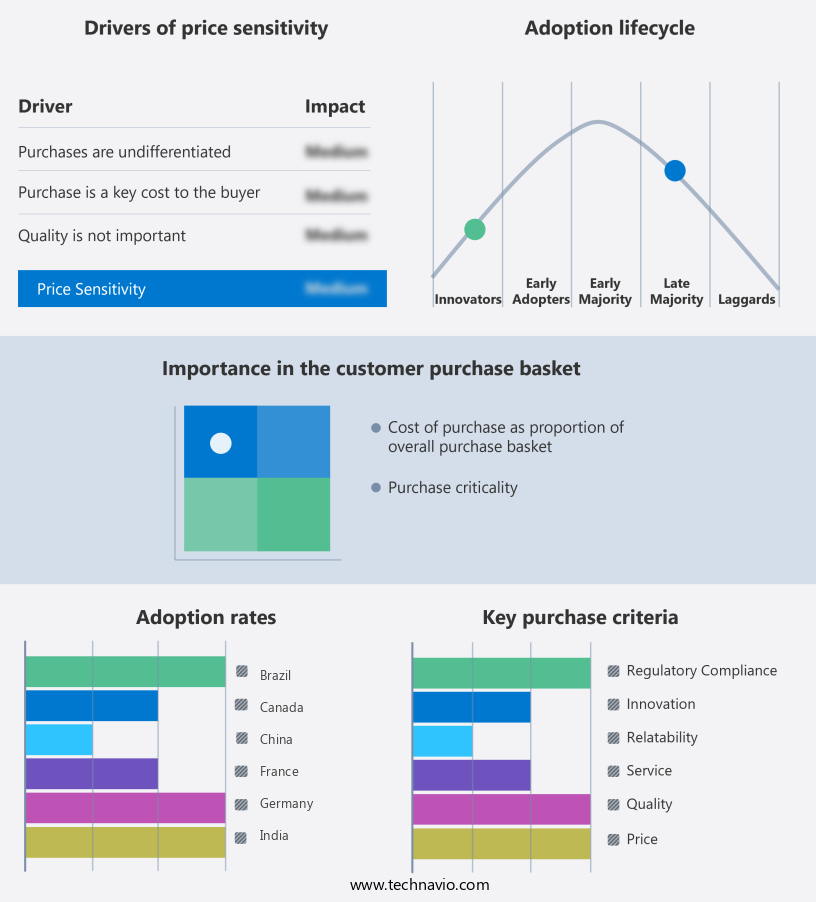

Exclusive Technavio Analysis on Customer Landscape

The ai server hardware market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai server hardware market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Server Hardware Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai server hardware market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The Instinct MI300X/MI300A GPUs from an unspecified technology provider present a competitive alternative to NVIDIA GPUs and AMD EPYC CPUs, commonly utilized in artificial intelligence servers. These GPUs offer comparable performance and functionality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Baidu Inc.

- Broadcom Inc.

- Cerebras

- Cisco Systems Inc.

- Dell Technologies Inc.

- Google Cloud

- Graphcore Ltd.

- Hewlett Packard Enterprise Co.

- Inspur Group.

- Intel Corp.

- International Business Machines Corp.

- Lenovo Group Ltd.

- Microsoft Corp.

- NVIDIA Corp.

- SambaNova Systems Inc.

- Super Micro Computer Inc.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Server Hardware Market

- In January 2024, Intel unveiled its new Neural Compute Server, designed specifically for artificial intelligence (AI) workloads. The server, featuring Intel's latest processors, aimed to deliver improved performance and energy efficiency for data centers (Intel Press Release, 2024).

- In March 2024, NVIDIA and Microsoft announced a strategic partnership to develop and deploy AI solutions using NVIDIA's GPUs on Microsoft's Azure cloud platform. This collaboration was expected to accelerate AI innovation and adoption across industries (NVIDIA Press Release, 2024).

- In May 2024, Google announced a USD1 billion investment in its data centers to support its AI and machine learning initiatives. This significant investment was aimed at expanding its computing capacity and improving its AI capabilities (Google Press Release, 2024).

- In January 2025, IBM and NEC Corporation entered into a strategic partnership to develop AI servers using IBM Power Systems and NEC's supercomputing technologies. The collaboration aimed to address the growing demand for AI solutions in various industries (IBM Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Server Hardware Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

241 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 42% |

|

Market growth 2025-2029 |

USD 358339.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.7 |

|

Key countries |

US, China, Germany, UK, Japan, France, Canada, Brazil, Italy, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in machine learning algorithms and the increasing demand for high-performance computing across various sectors. Recall metrics and hardware security are becoming increasingly important, with power efficiency being a key consideration for data centers. CPU performance and throughput optimization are essential for handling complex machine learning workloads, while sustainability initiatives, such as cooling systems and energy consumption reduction, are gaining traction. For instance, a leading technology company reported a 30% reduction in training time by implementing a modular architecture with distributed computing and GPU acceleration. The industry is expected to grow at a robust pace, with estimates suggesting a 20% annual increase in deep learning framework usage.

- Hardware security, thermal management, and error rate reduction are critical components of AI server hardware, ensuring system reliability and fault tolerance. Inference speed and parallel processing are crucial for real-time applications, while network bandwidth and storage latency optimization are essential for handling large datasets. Furthermore, server virtualization, RAM capacity, and lifecycle management are becoming increasingly important for managing and scaling AI infrastructure. Data encryption, precision metrics, and model accuracy are essential for maintaining data security and ensuring the effectiveness of AI applications. In conclusion, the market is a dynamic and evolving landscape, with continuous innovation in areas such as hardware security, power efficiency, and machine learning algorithms driving growth and shaping the future of AI infrastructure.

What are the Key Data Covered in this AI Server Hardware Market Research and Growth Report?

-

What is the expected growth of the AI Server Hardware Market between 2025 and 2029?

-

USD 358.34 billion, at a CAGR of 42%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud, On premises, and Hybrid), Type (Inference servers and Training servers), Product (GPUs, ASICs, CPUs, FPGAs, and Others), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Explosive growth of large language models, Severe supply chain constraints and key component scarcity

-

-

Who are the major players in the AI Server Hardware Market?

-

Advanced Micro Devices Inc., Baidu Inc., Broadcom Inc., Cerebras, Cisco Systems Inc., Dell Technologies Inc., Google Cloud, Graphcore Ltd., Hewlett Packard Enterprise Co., Inspur Group., Intel Corp., International Business Machines Corp., Lenovo Group Ltd., Microsoft Corp., NVIDIA Corp., SambaNova Systems Inc., Super Micro Computer Inc., and Tenstorrent Inc.

-

Market Research Insights

- The market is a dynamic and ever-evolving landscape, with continuous advancements in technology driving innovation. Two significant trends characterize this market. First, the increasing demand for AI applications in various industries has led to a surge in the deployment of AI models, requiring substantial hardware upgrades. For instance, the adoption of AI in healthcare has resulted in a 30% increase in the use of virtual machines for model deployment. Second, industry growth expectations remain strong, with a projected industry-wide growth rate of 25% annually. This growth is fueled by the increasing need for operational efficiency, with organizations seeking to optimize resource utilization and improve performance benchmarking through the use of advanced hardware solutions, such as DDR memory, liquid cooling, and redundant power supplies.

- Additionally, the integration of tensor processing units and FPGA acceleration has led to significant improvements in real-time processing capabilities. These advancements are crucial in enabling organizations to effectively manage large datasets and complex workloads, such as batch processing and feature engineering, while maintaining security protocols and ensuring access control.

We can help! Our analysts can customize this ai server hardware market research report to meet your requirements.

RIA -

RIA -