AI Vision Inspection Market Size 2025-2029

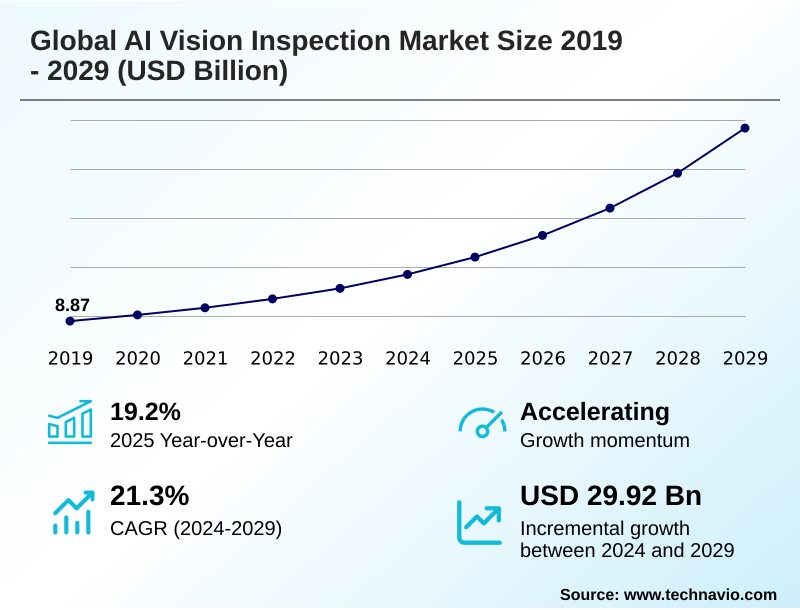

The ai vision inspection market size is valued to increase by USD 29.92 billion, at a CAGR of 21.3% from 2024 to 2029. Increasing demand for automation and enhanced quality control in manufacturing will drive the ai vision inspection market.

Major Market Trends & Insights

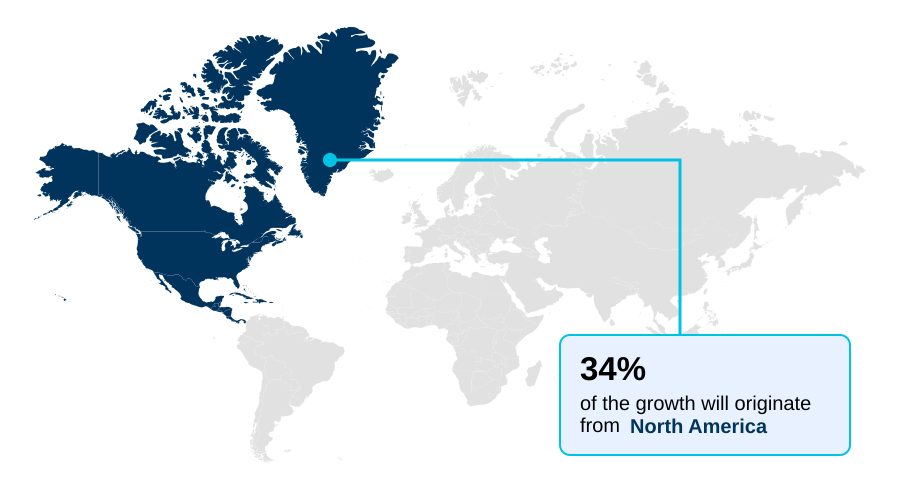

- North America dominated the market and accounted for a 34.4% growth during the forecast period.

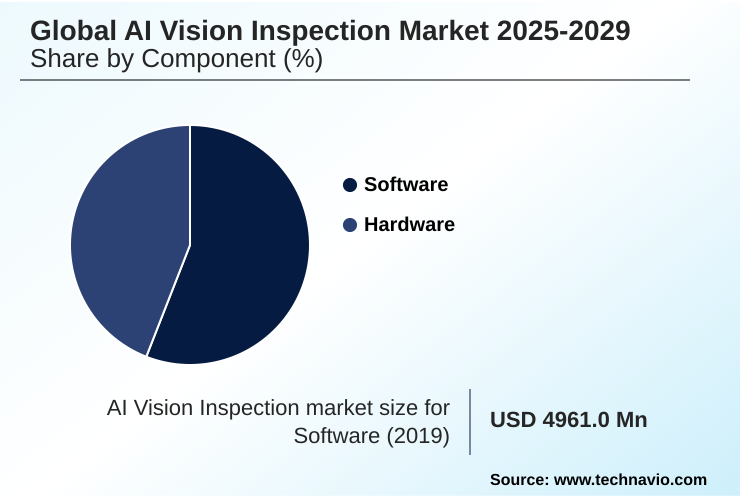

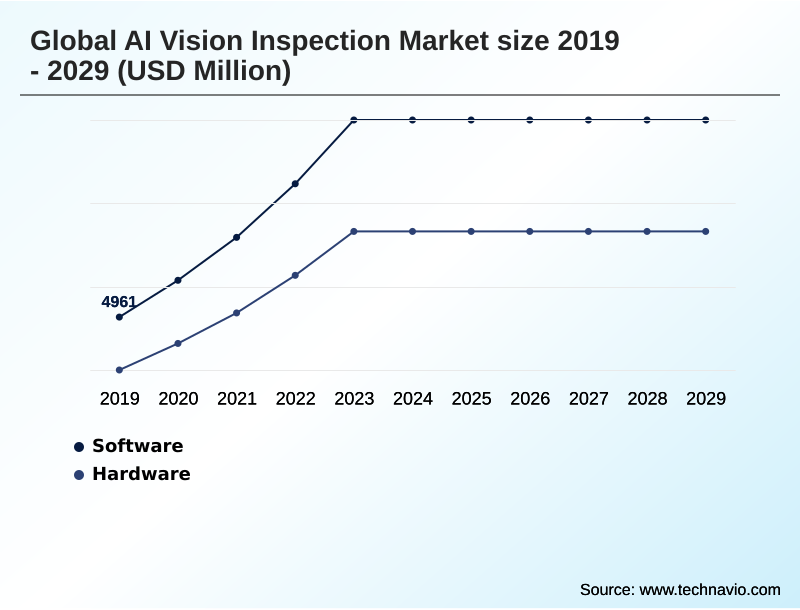

- By Component - Software segment was valued at USD 8.89 billion in 2023

- By Application - Training segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 39.47 billion

- Market Future Opportunities: USD 29.92 billion

- CAGR from 2024 to 2029 : 21.3%

Market Summary

- The AI vision inspection market is fundamentally transforming quality assurance across industries by replacing manual, error-prone processes with intelligent automation. This evolution is driven by the integration of advanced technologies like deep learning and edge AI, which enable systems to detect minute defects with exceptional speed and accuracy.

- In high-volume sectors such as electronics manufacturing, these systems are critical for identifying microscopic flaws on printed circuit boards that could lead to product failure, thereby safeguarding brand reputation and reducing costly rework.

- The market's momentum is further sustained by the push toward Industry 4.0, where interconnected smart factories rely on real-time data from vision systems for process optimization and predictive maintenance. However, widespread adoption is tempered by challenges, including the complexity of integrating new technologies with legacy infrastructure and the significant initial capital investment required.

- The need for specialized talent to develop and maintain these systems, coupled with an evolving regulatory environment around data privacy, also presents considerable hurdles for organizations seeking to leverage these powerful quality control solutions.

What will be the Size of the AI Vision Inspection Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Vision Inspection Market Segmented?

The ai vision inspection industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Hardware

- Application

- Training

- Inference

- End-user

- Consumer electronics

- Automotive

- Manufacturing

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is central to the AI vision inspection market, driven by the need for platforms that enable automated visual inspection.

These systems leverage sophisticated machine learning algorithms and computer vision systems to perform high-speed inspection tasks, including object recognition and image segmentation.

The evolution of AI vision inspection platforms is focused on democratizing access, allowing for predictive quality analytics without extensive coding knowledge.

However, successful implementation is not without challenges, as 48% of technology leaders cite a lack of specialized AI skills as a primary barrier.

This highlights a critical need for intuitive machine vision software that can be deployed for anomaly detection and defect detection by a broader range of industrial users, often integrated with vision-guided robotics.

The Software segment was valued at USD 8.89 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Vision Inspection Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI vision inspection market is led by North America, which is projected to account for 34.4% of the market's growth, with the US being a key contributor.

This is driven by advanced manufacturing capabilities and significant investments in industrial automation, especially in automotive manufacturing and pharmaceutical quality control.

Meanwhile, the APAC region is forecast to exhibit the fastest growth, with a CAGR of 21.6%, fueled by rapid industrialization and the adoption of smart factory initiatives.

Key applications in the region include food and beverage inspection and automated weld inspection, where smart cameras and 3D vision sensors are crucial.

In Europe, Germany's focus on Industry 4.0 makes it a major market for technologies like 3D imaging for quality control and AI in automotive quality control to inspect for subtle surface defects.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Businesses evaluating the adoption of AI-powered visual inspection must consider the total cost of AI vision inspection systems against their long-term benefits. The benefits of AI in quality control are substantial, particularly in high-stakes industries. For instance, implementing real-time quality control in pharmaceuticals ensures regulatory compliance and patient safety.

- Similarly, AI-powered defect detection in automotive manufacturing is critical for identifying subtle flaws that impact vehicle integrity. When comparing AI vision vs traditional machine vision, AI's ability to handle complex and variable defects with deep learning for surface defect detection offers a distinct advantage, often showing ROI more than double that of rule-based systems.

- A key aspect of how to implement AI vision inspection involves addressing the challenges of integrating AI vision with legacy systems. For companies facing a lack of diverse defect data, using generative AI for synthetic defect data is an emerging best practice for training AI inspection models.

- Furthermore, the role of AI vision in Industry 4.0 extends to applications like AI vision for robotic bin picking and predictive maintenance using visual data. Specific use cases, such as automated inspection systems for food processing and 3D vision systems for assembly verification, highlight the technology's versatility.

- Success also hinges on ensuring data privacy in cloud-based AI vision and leveraging edge AI for real-time industrial inspection to minimize latency in critical processes like AI-based optical character recognition (OCR) and inspection in semiconductor manufacturing.

What are the key market drivers leading to the rise in the adoption of AI Vision Inspection Industry?

- The increasing demand for automation and enhanced quality control within the manufacturing sector serves as a key driver for market growth.

- The market is primarily driven by the convergence of Industry 4.0 integration and the widespread demand for industrial automation. As smart factory vision systems become standard, AI-powered analytics are enabling unprecedented levels of operational efficiency and process optimization.

- A notable 76% of organizations are now using automation to streamline workflows, with AI vision for manufacturing at the forefront of this shift.

- This is further evidenced in the automotive sector, where 56% of UK business leaders are integrating computer vision in industrial automation.

- The adoption of automated quality control systems, powered by robotic process automation and Industrial IoT (IIoT) and vision systems, is no longer a competitive advantage but a necessity for quality control automation.

- This push is fundamentally reshaping production, with AI for process optimization ensuring higher quality and throughput.

What are the market trends shaping the AI Vision Inspection Industry?

- The market is witnessing a significant trend toward the adoption of advanced deep learning and machine learning algorithms. These technologies are instrumental in enhancing defect detection and quality control with unprecedented accuracy.

- Key market trends are centered on advancing real-time processing capabilities through the proliferation of edge AI and hybrid cloud computing platforms. This architectural shift allows sophisticated deep learning models to perform real-time visual inspection directly on the factory floor, a critical factor for immediate decision-making.

- The use of generative AI is also transforming the space, with generative AI in manufacturing enabling the creation of high-fidelity synthetic data. This approach of synthetic data for AI training accelerates the development of robust models without requiring physical defect examples.

- As machine vision software evolves, the trend of edge computing for AI vision is becoming standard, with some sectors seeing a deployment increase of over 40% in edge devices. This integration of deep learning for visual inspection with cloud-based vision AI offers a scalable and secure framework for modern quality control.

What challenges does the AI Vision Inspection Industry face during its growth?

- The scarcity of skilled personnel, compounded by an evolving regulatory landscape, presents a key challenge to the industry's growth.

- A significant challenge facing the market is the complexity of AI vision integration challenges, particularly with legacy systems. This hurdle is compounded by stringent data privacy regulations, which govern the use of high-resolution imaging and require robust data security in AI vision architectures.

- The financial barrier remains substantial, as justifying the ROI of AI vision inspection requires a detailed analysis of potential gains, such as a 0.1% yield improvement that can translate to millions in revenue for semiconductor inspection. Furthermore, the scarcity of expertise for AI model training for inspection persists, with nearly 95% of technology leaders reporting difficulties in finding skilled talent.

- These issues affect specialized applications like printed circuit board (PCB) inspection and ensuring parts traceability, making the deployment of automated inspection for electronics a complex undertaking that requires careful planning around predictive maintenance and assembly verification.

Exclusive Technavio Analysis on Customer Landscape

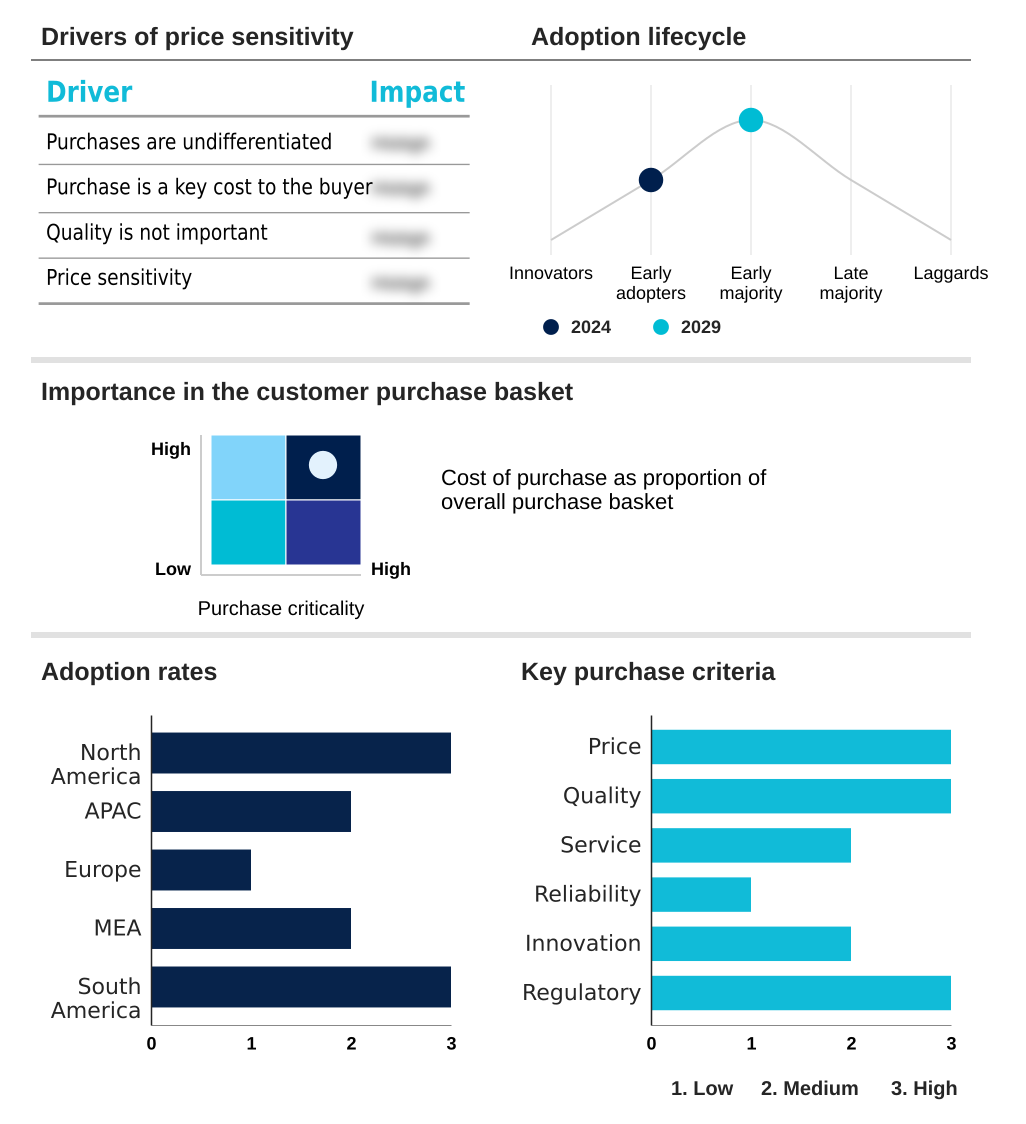

The ai vision inspection market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai vision inspection market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Vision Inspection Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai vision inspection market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AI Superior GmbH - Provides a cloud-based platform leveraging machine learning to detect visual anomalies, enhancing quality control in industrial processes through automated inspection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AI Superior GmbH

- Amazon Web Services Inc.

- Apera AI

- Averroes.ai Inc.

- Basler AG

- Chooch Intelligence Technologies Co.

- Cognex Corp.

- Google LLC

- Hailo Technologies Ltd.

- Intel Corp.

- IBM Corp.

- Keyence Corp.

- Landing AI

- Microsoft Corp.

- NVIDIA Corp.

- OMRON Corp.

- Qualcomm Inc.

- Robovision BV

- SenseTime Group Inc.

- Symphony Innovation LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai vision inspection market

- In August 2024, the European Union's Artificial Intelligence Act entered into force, establishing a harmonized, risk-based legal framework for AI with a global impact on businesses.

- In September 2024, Basler AG launched its Pylon AI software, a solution designed to integrate advanced AI capabilities into machine vision applications for more effective image processing and analysis.

- In January 2025, NVIDIA expanded its partnerships with major automotive players, including Toyota and Continental, to accelerate the development of next-generation highly automated vehicle fleets using advanced AI.

- In March 2025, Cybord introduced its Real-Time Interceptor (RTI) solution, which utilizes deep learning algorithms to proactively identify and eliminate defective electronic components before integration into circuit boards.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Vision Inspection Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.3% |

| Market growth 2025-2029 | USD 29919.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 19.2% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI vision inspection market is defined by the deployment of automated visual inspection for quality control automation, moving beyond human capabilities in speed and accuracy. Central to this are deep learning models and sophisticated machine learning algorithms that power computer vision systems for tasks like defect detection and anomaly detection.

- The technological landscape includes 3D vision sensors and high-resolution imaging for detailed surface inspection, as well as smart cameras enabling real-time processing at the edge. A key boardroom consideration is the adoption of edge AI, which directly impacts data privacy regulations by keeping sensitive operational data on-premises, a critical factor for compliance.

- Applications are expanding into semiconductor inspection, automotive manufacturing, and pharmaceutical quality control, where AI-powered analytics facilitate predictive maintenance and process optimization. The impact is significant, with AI-powered analysis in some sectors reducing diagnosis and inspection times by up to 30%.

- This drive for operational efficiency is fostering innovation in machine vision software, printed circuit board (PCB) inspection, and parts traceability within the broader Industry 4.0 integration.

What are the Key Data Covered in this AI Vision Inspection Market Research and Growth Report?

-

What is the expected growth of the AI Vision Inspection Market between 2025 and 2029?

-

USD 29.92 billion, at a CAGR of 21.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Hardware), Application (Training, Inference), End-user (Consumer electronics, Automotive, Manufacturing, Healthcare, Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for automation and enhanced quality control in manufacturing, Scarcity of skilled personnel and evolving regulatory landscape

-

-

Who are the major players in the AI Vision Inspection Market?

-

AI Superior GmbH, Amazon Web Services Inc., Apera AI, Averroes.ai Inc., Basler AG, Chooch Intelligence Technologies Co., Cognex Corp., Google LLC, Hailo Technologies Ltd., Intel Corp., IBM Corp., Keyence Corp., Landing AI, Microsoft Corp., NVIDIA Corp., OMRON Corp., Qualcomm Inc., Robovision BV, SenseTime Group Inc. and Symphony Innovation LLC

-

Market Research Insights

- The market dynamics for AI vision inspection are shifting from standalone quality checks to integrated process optimization, driven by machine learning for defect detection. This transition is delivering measurable business outcomes, with some implementations reducing manufacturing defects by over 20% and associated downtime by 15%.

- As AI for anomaly detection becomes more sophisticated, its role in industrial automation expands, enabling high-speed inspection systems that enhance throughput. The adoption of AI vision inspection platforms is also influenced by ROI considerations, where the value of predictive quality analytics in preventing large-scale recalls outweighs the initial investment.

- This focus on tangible benefits is accelerating the deployment of vision-guided robotics and other automated solutions across the factory floor, making computer vision a cornerstone of modern manufacturing efficiency.

We can help! Our analysts can customize this ai vision inspection market research report to meet your requirements.

RIA -

RIA -