Aircraft Fly-By-Wire System Market Size 2025-2029

The aircraft fly-by-wire system market size is forecast to increase by USD 2.69 billion at a CAGR of 6.9% between 2024 and 2029.

- The market is driven by the increasing demand for fuel-efficient aircraft, as airlines seek to reduce operational costs and minimize environmental impact. This trend is further fueled by the transition towards more electric aircraft, as advancements in battery technology and electric propulsion systems gain traction. However, the market faces significant challenges, including the high development and certification costs associated with these advanced systems. Manufacturers must navigate these hurdles to bring new products to market, while also addressing safety concerns and ensuring regulatory compliance.

- To capitalize on market opportunities and navigate challenges effectively, companies must focus on innovation, collaboration, and cost optimization. By investing in research and development, forming strategic partnerships, and implementing lean manufacturing processes, they can stay competitive and meet the evolving demands of the aviation industry. Additionally, the rise in demand for in-flight entertainment and connectivity (IFEC) systems is fueling market growth.

What will be the Size of the Aircraft Fly-By-Wire System Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- In the aerospace and defense industry, the fly-by-wire system market is experiencing significant advancements, driven by the integration of technology such as stability augmentation, data analytics, and adaptive control. Autopilot functions and flight control optimization are becoming increasingly essential for modern aircraft, enabling weight reduction and fuel efficiency. Machine learning and predictive control are also key trends, enabling precise management of control inputs and emissions reduction. Pilot training commonality is another area of focus, as electronic interfaces streamline the learning process. Flight envelope protection and autonomous flight control are also critical for accident risk reduction, particularly in the context of aircraft engine control.

- Overall, the aviation industry is embracing these technologies to enhance safety, improve performance, and reduce operational costs. One key trend is the modernization and upgrade of commercial aircraft cabin designs, leading to an increased demand for advanced electrical switches and human-machine interfaces (HMIs).

How is this Aircraft Fly-By-Wire System Industry segmented?

The aircraft fly-by-wire system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Commercial aviation

- Military aviation

- Business aviation

- Technology

- Digital fly-by-wire

- Analog fly-by-wire

- Component

- Flight control computers

- Actuators

- Cockpit controls

- Sensors

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

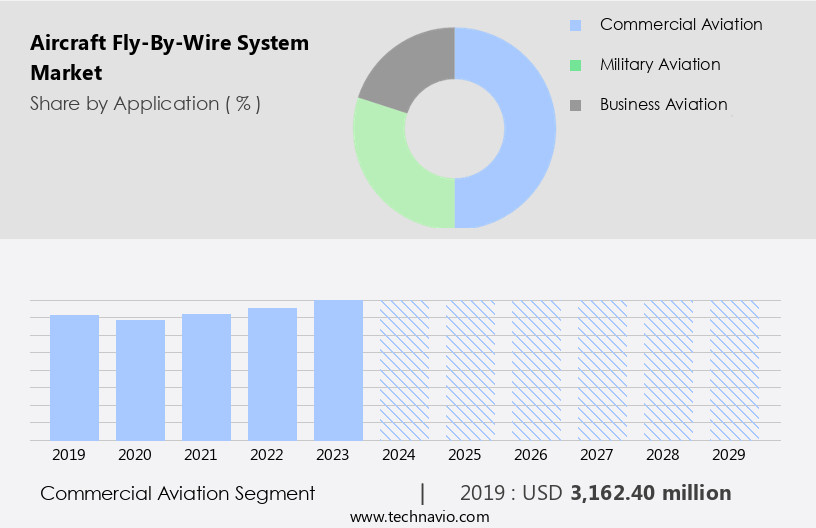

The commercial aviation segment is estimated to witness significant growth during the forecast period. The market is witnessing significant growth, particularly in the commercial aviation sector. Replacing conventional control systems with digital flight control systems, FBW technology has become a standard feature in modern aircraft. This transition is essential for enhancing flight safety, improving fuel efficiency, and enabling higher levels of automation. The commercial aviation industry is under increasing pressure to meet operational, environmental, and regulatory demands, making FBW systems a preferred choice. High-purity quartz sand and white sand are integral components in manufacturing control surfaces and electrical components for FBW systems. The space industry also leverages FBW technology for agility and damage tolerance in military aircraft and electric aircraft.

Military aviation relies on FBW systems for flight envelope protection and agility, while business aviation benefits from weight reduction and ease of handling. Electrical signals transmitted through FBW systems control the movement of control surfaces, optimizing aerodynamic performance and reducing aircraft weight. FBW systems have been adopted in advanced aircraft such as the Airbus A320neo and Boeing 787, demonstrating significant performance gains. The emphasis on fuel efficiency and emissions reduction in the aviation industry further drives the adoption of FBW technology. Brake support systems, including anti-skid brakes, are integral components of aircraft braking systems.

The Commercial aviation segment was valued at USD 3.16 billion in 2019 and showed a gradual increase during the forecast period.

The Aircraft Fly-By-Wire System Market is advancing rapidly, especially with increasing demands for enhanced military aircraft agility in modern aerial combat. Fly-by-wire technology replaces traditional manual controls with electronic interfaces, allowing for superior maneuverability and control precision, critical factors in defense aviation. Interestingly, parallel industries such as hydraulic fracturing are influencing component innovation, with crossover technologies improving system durability in extreme environments. Materials like frac sand, known for their strength and thermal resistance, are being explored in lightweight composites and structural components to enhance aircraft system resilience.

The Aircraft Fly-By-Wire System Market is gaining momentum as the aviation industry prioritizes safety, performance, and automation. These systems replace traditional mechanical flight controls with sophisticated electronic interfaces, enabling faster and more precise responses to pilot inputs. Such digital advancements not only enhance aircraft handling but also reduce the margin for pilot error by incorporating built-in safeguards and automated responses in critical situations. Carbon fiber construction and electronics segment innovations contribute to enhanced performance and reliability.

Regional Analysis

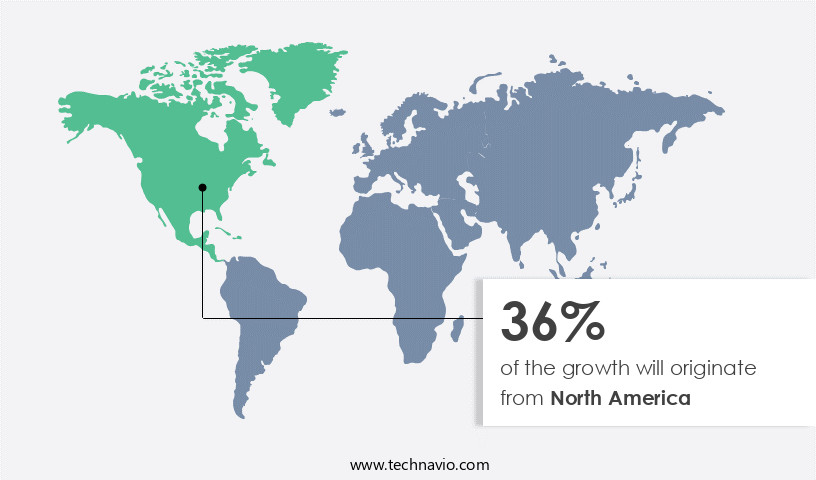

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Aircraft Fly-By-Wire (FBW) system market in North America is experiencing significant growth, fueled by robust defense spending, commercial aviation expansion, and technological advancements. The region's leadership is underpinned by the United States, which houses the world's largest aerospace manufacturing industry and military budget. In Fiscal Year 2024, the U.S. allocated a record USD 1.27 trillion to defense, with USD 874.5 billion earmarked for military operations. Canada and Mexico also contribute to regional demand with defense budgets of USD 33.7 billion and USD 7.5 billion, respectively. Military aviation plays a pivotal role in FBW system demand in North America. The industry's focus on weight reduction and damage tolerance further propels the market's growth.

High-purity quartz sand, a crucial component in producing electronic parts, fuels the production of electrical signals essential for FBW systems. The integration of FBW systems in commercial aviation, business jets, and the space industry is expanding the market's reach. Despite the dominance of conventional control systems, the military aviation sector's emphasis on agility and flight envelope protection accelerates the adoption of FBW systems. The aircraft industry's ongoing transition to electric aircraft is also expected to create new opportunities for FBW systems. The commercial aviation sector, comprising narrow-body, wide-body, and regional aircraft, experiences continuous growth due to the increasing consumer preference for air travel.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Aircraft Fly-By-Wire System market drivers leading to the rise in the adoption of Industry?

- The primary market force is the increasing demand for fuel-efficient aircraft, driven by growing concerns for environmental sustainability and economic efficiency in the aviation industry. The global aircraft industry is witnessing a shift towards fuel-efficient and environmentally sustainable technologies, driving the adoption of Fly-By-Wire (FBW) systems. FBW systems, which replace conventional mechanical and hydraulic flight control systems with electrically controlled alternatives, offer significant advantages in terms of structural efficiency and precise control. The increasing focus on reducing fuel consumption and carbon emissions, coupled with rising fuel costs, is compelling airlines and aircraft manufacturers to prioritize FBW systems.

- Electric aircraft, a growing segment in commercial aviation, is expected to benefit significantly from the adoption of FBW systems. These systems are essential for the successful implementation of electric propulsion systems, which are gaining popularity due to their potential to offer significant fuel savings and reduced environmental impact. The demand for FBW systems is set to increase as the aviation industry continues its transition towards more fuel-efficient and sustainable technologies. These systems eliminate heavy mechanical linkages and hydraulic lines, resulting in substantial weight reduction and, consequently, lower fuel consumption. Moreover, FBW systems enable more responsive and precise control of control surfaces, facilitating smoother aerodynamic adjustments and enhancing overall flight performance.

What are the Aircraft Fly-By-Wire System market trends shaping the Industry?

- The transition to more electric aircraft is an emerging market trend. It reflects a growing demand for sustainable and eco-friendly aviation solutions. The global aircraft fly-by-wire (FBW) system market is experiencing significant growth due to the transition to more electric aircraft (MEA). MEA platforms are reducing reliance on traditional hydraulic and pneumatic systems by adopting electrically powered alternatives. This shift enhances efficiency, decreases emissions, and enables new aircraft configurations. The demand for compact, lightweight, and highly integrated FBW architectures is increasing as a result. Recent developments, such as Archer Aviation's agreement with Soracle, a joint venture between Japan Airlines and Sumitomo Corporation, for the potential purchase of up to 100 Midnight electric aircraft, highlight the momentum behind MEA adoption.

- FBW systems play a crucial role in this evolution by providing enhanced flight control and stability, enabling advanced avionics, and improving overall aircraft performance. Military aviation and business aviation sectors are expected to drive market growth due to their focus on advanced technology and performance. Flight envelope protection, a critical feature of FBW systems, ensures safe flight operations by preventing pilots from exceeding the aircraft's design limits. The future of FBW systems lies in their ability to adapt to the evolving aviation landscape and meet the demands of MEA platforms. The military sector also invests in advanced aircraft brake systems, utilizing carbon brakes and steel brakes, from leading manufacturers like Safran Landing Systems.

How does Aircraft Fly-By-Wire System market faces challenges during its growth?

- The high development and certification costs pose a significant challenge to the growth of the industry. This obstacle necessitates substantial investments in research and development, as well as rigorous testing and regulatory compliance, which can hinder the industry's expansion. Fly-by-wire (FBW) systems, which replace traditional mechanical flight control systems with electronic ones, have become essential components in modern aircraft and the space industry. The integration of advanced electronics, high-performance computing, and fault-tolerant architectures necessitates substantial investments in research, engineering, and testing.

- Weight reduction and damage tolerance are significant advantages of FBW systems. Despite the financial challenges, the benefits of FBW systems, including enhanced flight control, fuel efficiency, and improved safety, make them indispensable in the aviation and space industries. Custom-designed for each aircraft type, FBW platforms incorporate specialized flight control computers, redundant data buses, and precision sensors. Certification of these systems by aviation authorities, such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), involves rigorous standards to ensure safety and reliability.

Exclusive Customer Landscape

The aircraft fly-by-wire system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aircraft fly-by-wire system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aircraft fly-by-wire system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - The company specializes in advanced aircraft control systems, including primary flight control computers (FCC), active inceptor systems (AIS), and actuator control electronics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- BAE Systems Plc

- Collins Aerospace

- Curtiss Wright Corp.

- Dassault Aviation SA

- Eaton Corp. plc

- Embraer SA

- General Electric Co.

- Honeywell International Inc.

- Liebherr International AG

- Lockheed Martin Corp.

- Moog Inc.

- Nabtesco Corp.

- Northrop Grumman Corp.

- Parker Hannifin Corp.

- Saab AB

- Safran SA

- Textron Inc.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aircraft Fly-By-Wire System Market

- In January 2024, Honeywell Aerospace received approval from the Federal Aviation Administration (FAA) for its new generation fly-by-wire system, the Primus Autopilot 2000, to be installed on various business jet models (Honeywell, 2024). This approval marked a significant advancement in the fly-by-wire systems market, enabling increased automation and improved safety features for business jets.

- In March 2024, Thales and Safran signed a strategic partnership agreement to collaborate on the development and production of advanced fly-by-wire systems for commercial aircraft (Thales, 2024). This collaboration aimed to combine Thales' expertise in flight control systems and Safran's experience in aircraft engines, potentially leading to more efficient and cost-effective solutions for aircraft manufacturers.

- In April 2025, Collins Aerospace announced the successful completion of flight tests for its new advanced fly-by-wire system, the Smart Flight Control System, on a Bombardier CRJ Series aircraft (Collins Aerospace, 2025). This achievement represented a significant technological advancement in the fly-by-wire systems market, as the new system promised improved fuel efficiency, reduced emissions, and enhanced safety features.

- In May 2025, Garmin International received FAA approval for its fly-by-wire system, the GFC 700 Autopilot, to be installed on Cessna's single-engine aircraft models (Garmin, 2025). This approval expanded Garmin's presence in the general aviation market and provided Cessna's customers with a more advanced and cost-effective autopilot solution.

Research Analyst Overview

The fly-by-wire system market continues to evolve, with applications expanding across various sectors, including the space industry, aircraft industry, and military aviation. This market dynamics is driven by the ongoing development of electrical flight control systems, enabling fully fly-by-wire controls in both commercial and military aircraft. In the aircraft industry, weight reduction and damage tolerance are critical factors driving the adoption of fly-by-wire systems. High-purity quartz sand, also known as white sand, is increasingly used in the production of electronic components, contributing to the miniaturization and lightweighting of control systems. Brown sand, a type of quartz sand, is also gaining attention due to its potential use in the production of electric aircraft components.

The integration of electric aircraft into commercial aviation is expected to further fuel the demand for advanced flight control systems. Military aviation is another significant market for fly-by-wire systems, with a focus on flight envelope protection and aircraft agility. The continuous advancements in this technology are enabling military aircraft to perform more complex maneuvers and respond faster to changing flight conditions. The space industry is also adopting fly-by-wire systems to enhance the control and maneuverability of spacecraft. The evolving nature of this market is driven by the increasing demand for advanced technologies to support space exploration and satellite deployment.

Overall, the fly-by-wire system market is characterized by continuous innovation and development, driven by the need for lighter, more efficient, and more responsive flight control systems across various industries. The market is subject to stringent regulations, flight cancellations, and e-commerce services, necessitating safety improvement initiatives and reliability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aircraft Fly-By-Wire System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

238 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.9% |

|

Market growth 2025-2029 |

USD 2.69 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.4 |

|

Key countries |

US, France, Germany, China, UK, Japan, India, Canada, Brazil, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aircraft Fly-By-Wire System Market Research and Growth Report?

- CAGR of the Aircraft Fly-By-Wire System industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aircraft fly-by-wire system market growth of industry companies

We can help! Our analysts can customize this aircraft fly-by-wire system market research report to meet your requirements.

RIA -

RIA -