Alternating Current Power System Market Size 2026-2030

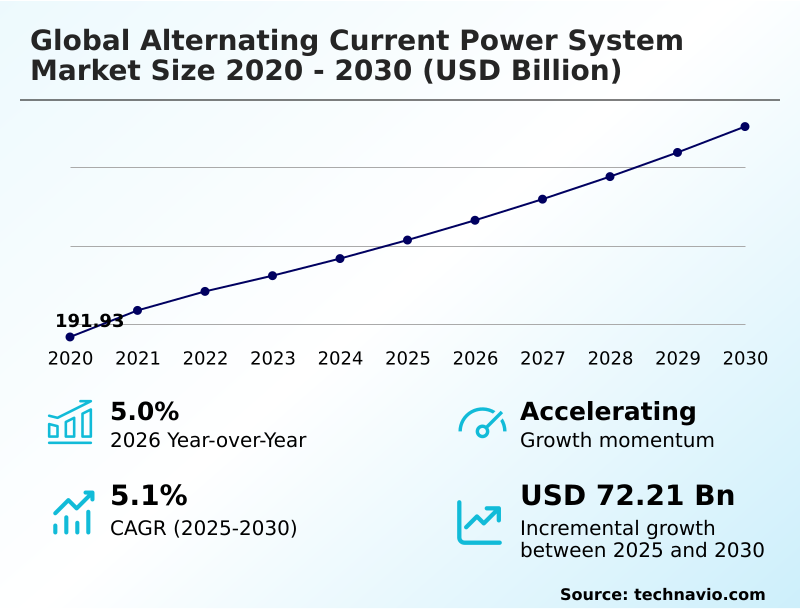

The alternating current power system market size is valued to increase by USD 72.21 billion, at a CAGR of 5.1% from 2025 to 2030. High-density hyperscale data centers and rise of AI-native AC power distribution units will drive the alternating current power system market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 62.1% growth during the forecast period.

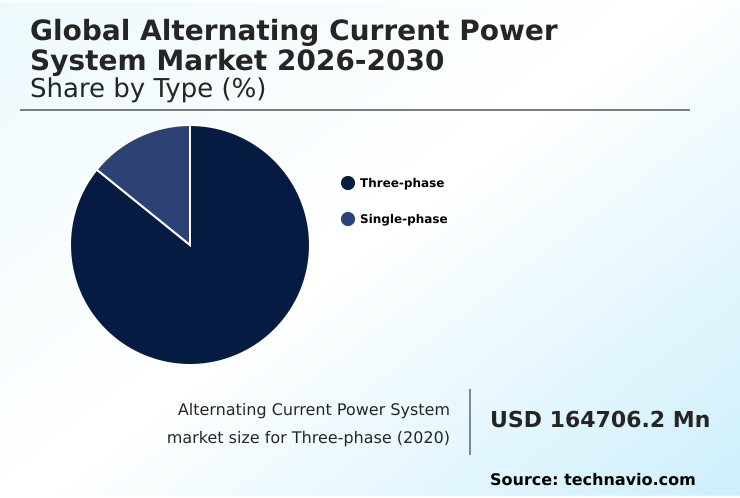

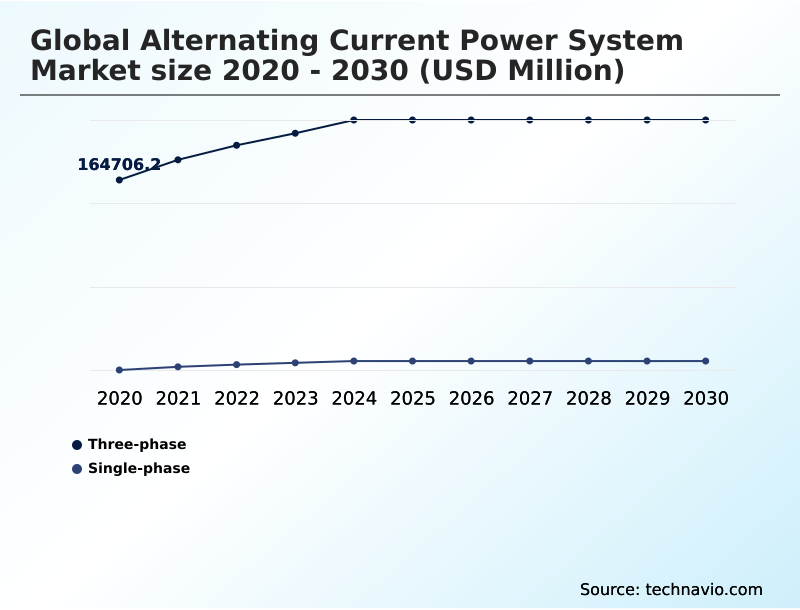

- By Type - Three-phase segment was valued at USD 208.11 billion in 2024

- By End-user - Non-residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 133.89 billion

- Market Future Opportunities: USD 72.21 billion

- CAGR from 2025 to 2030 : 5.1%

Market Summary

- The alternating current power system market is undergoing a profound structural transformation, driven by the dual imperatives of grid modernization and the aggressive integration of variable renewable energy sources.

- This expansion is fundamentally characterized by a shift from traditional, centralized power architectures toward highly flexible, intelligent AC networks capable of managing bi-directional power flow and high-frequency fluctuations from inverter-based resources (IBRs). As nations strive to meet decarbonization targets, the replacement of aging fossil-fuel-based generation necessitates a massive overhaul of existing AC infrastructure.

- This includes the deployment of advanced power conditioning systems and solid state transformers (SST) to maintain voltage stability. One key business scenario involves a utility deploying grid-forming (GFM) inverters and flexible AC transmission systems (FACTS) to manage a portfolio of decentralized energy resources.

- This allows the utility to improve power quality management, prevent outages from weak-AC conditions, and defer costly physical upgrades, thereby enhancing grid resilience and financial performance in an era of rapid energy transition.

- This digital pivot, combined with the expansion of ultra-high-voltage AC (UHVAC) networks in emerging economies, underscores the convergence of power electronics and digital controls as the primary engine of market evolution.

What will be the Size of the Alternating Current Power System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Alternating Current Power System Market Segmented?

The alternating current power system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Three-phase

- Single-phase

- End-user

- Non-residential

- Residential

- Product

- Switchgear

- Generator

- UPS

- PDU

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- Turkey

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The three-phase segment is estimated to witness significant growth during the forecast period.

Three-phase power systems form the backbone of industrial and utility-scale power infrastructure, providing the high-capacity energy essential for heavy machinery, large-scale motors, and expansive commercial facilities.

These systems utilize three distinct alternating currents, offering constant and efficient power flow that reduces motor vibration and allows for more economical wiring compared to high-power single-phase setups.

The primary driver is the global expansion of energy-intensive industries, including semiconductor fabrication and data centers. As metropolitan areas grow, demand for robust three-phase distribution networks to support high-rise buildings and transit systems escalates.

Projects involving high-voltage substations with sophisticated protection systems are increasing, highlighting the role of three-phase infrastructure in enabling efficient power evacuation for utility-scale renewables and industrial hubs, supporting voltage requirements up to 765 kilovolts.

The integration of wide-bandgap semiconductors and digital twin testing is enhancing the reliability of three-phase inverters and converters, allowing for more precise grid synchronization and power quality management.

The Three-phase segment was valued at USD 208.11 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 62.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Alternating Current Power System Market Demand is Rising in APAC Get Free Sample

The APAC region represents the most dynamic geography, contributing to approximately 85% of global electricity demand growth and holding a dominant market share of 62%.

Rapid urbanization and manufacturing expansion in China and India are creating an insatiable appetite for robust and scalable AC power infrastructure, including three-phase power systems and high-voltage AC (HVAC) transmission networks.

This demand is amplified by a surge in data center installations, which are a primary driver for advanced uninterruptible power supplies (UPS) and power conditioning systems in Japan and Southeast Asia.

The proliferation of 5G telecommunications infrastructure also requires specialized gas-insulated switchgear (GIS) and modular power solutions to ensure uninterrupted service.

While facing some supply chain challenges, the region's overall trajectory is defined by rapid expansion and the adoption of smart grid technologies and advanced power semiconductor technologies to leapfrog legacy systems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic deployment of advanced alternating current power systems is becoming central to global economic competitiveness, driven by the intense energy needs of high-density hyperscale data center power and the rise of AI-native AC power distribution units. To support this, grid-forming inverter technology for decarbonization is being adopted to stabilize networks as they integrate more renewables.

- In parallel, electrified heating with VFD retrofitting is enhancing energy efficiency in buildings. The backbone of this transformation is the use of digital twin for grid virtualization, which allows for predictive modeling and management. Key hardware innovations like solid state transformers in AC grids are enabling more flexible and efficient power conversion.

- Ensuring cyber-physical resilience in power systems is a top priority, addressed through AI-enabled security frameworks. Operationally, managing interconnection queue bottlenecks is a major focus, alongside efforts to mitigate rotational inertia erosion risks. Addressing the capital requirements for grid modernization remains a persistent challenge. The market is seeing a clear divergence between three-phase vs single-phase power efficiency for different applications.

- The reliability of UPS systems for critical infrastructure and the intelligence of PDU for server rack power management are non-negotiable. Modern switchgear for alternating current loads and generators for standby power redundancy provide essential control and backup. Furthermore, AC to AC converters for industrial machinery are crucial for operational continuity.

- Both residential AC power system upgrades and non-residential power quality management are experiencing growth, facilitated by smart grid technologies for AC networks and HVAC transmission for renewable integration. Modernization efforts have demonstrated the ability to reduce grid losses by a figure that is more than double the efficiency gains from previous-generation hardware, directly improving operational profitability for utilities.

What are the key market drivers leading to the rise in the adoption of Alternating Current Power System Industry?

- The market is significantly driven by the demands of high-density hyperscale data centers and the corresponding rise of AI-native AC power distribution units.

- Market growth is significantly propelled by the rise of high-density hyperscale data centers, which require AI-native high-density power distribution units (PDUs) to manage unprecedented thermal and electrical loads.

- This segment alone is driving a market expansion valued at over four times its previous state, as operators adopt intelligent AC power management systems for real-time monitoring.

- Another key driver is the transition toward grid-forming (GFM) inverters to industrialize inertia-supportive AC infrastructure, which stabilizes grids with high renewable penetration.

- Furthermore, the strategic adoption of electrified heating and cooling, coupled with the demand for variable frequency drive (VFD) retrofitting, is transforming AC motor control systems.

- VFD retrofits often provide a return on investment within 18 months through reduced electricity consumption, turning passive AC systems into active, energy-optimizing assets, especially when integrated with industrial internet of things (IIoT) platforms.

What are the market trends shaping the Alternating Current Power System Industry?

- The institutionalization of digital twin technology is transforming network management. This is coupled with a move toward high-fidelity grid virtualization for enhanced predictive analytics.

- Key trends are reshaping the alternating current power system market, led by the institutionalization of digital twin technology. This shift from static modeling to dynamic, real-time virtual replicas enables predictive fault management, with some large grid operators successfully reducing maintenance costs by approximately 30% and extending the operational life of assets like transformers by up to 20%.

- Another significant trend is the proliferation of solid state transformers (SST) and hybrid AC-DC conversion nodes. Utilizing advanced power semiconductor technologies, SSTs provide superior voltage regulation and facilitate bi-directional power flow, which is crucial for integrating renewable inputs.

- Concurrently, the expansion of cyber-physical resilience through AI-enabled zero-trust security is becoming standard, moving beyond perimeter defenses to protect increasingly digitized and connected grid infrastructure from automated threats. This includes advanced substation automation and power quality management techniques.

What challenges does the Alternating Current Power System Industry face during its growth?

- A critical challenge affecting industry growth is the crisis of interconnection bottlenecks, which leads to grid saturation in high-growth regions.

- The market faces critical challenges, primarily the crisis of interconnection queue management, where backlogs have surged to approximately 2,500 gigawatts globally. This congestion stalls new renewable projects due to the physical saturation of existing AC transmission infrastructure. A second major challenge is the erosion of rotational inertia as traditional synchronous generators are replaced by inverter-based resources (IBRs).

- This transition increases sensitivity to weak-AC conditions and the risk of instability, necessitating a redesign of protective schemes and the deployment of grid-enhancing technologies (GETS). Finally, the market is constrained by immense financial pressure, with a requirement to add or replace approximately 80 million kilometers of power lines.

- This, combined with regulatory friction and the fiscal fragility of distribution utilities, creates a formidable barrier to mobilizing the necessary capital for grid modernization and advanced hosting-capacity analytics.

Exclusive Technavio Analysis on Customer Landscape

The alternating current power system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the alternating current power system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Alternating Current Power System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, alternating current power system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offerings include high-efficiency power conversion and grid stability solutions, with a focus on enhancing excitation and synchronization technologies for complex industrial and utility-scale operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Advanced Energy Industries

- AEG Power Solutions BV

- AMETEK Inc.

- Borri SpA

- Delta Electronics Inc.

- Eaton Corp. Plc

- EnerSys

- Fuji Electric Co. Ltd.

- GE Vernova Inc.

- Generac Power Systems Inc.

- Hitachi Energy Ltd.

- Keysight Technologies Inc.

- Legrand SA

- LS ELECTRIC Co. Ltd.

- Mitsubishi Electric Corp.

- Schaefer Inc.

- Schneider Electric SE

- Toshiba Corp.

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Alternating current power system market

- In April 2025, ABB announced a strategic partnership with E.ON, Germany's largest DSO, to supply next-generation, sulfur-hexafluoride-free air-insulated switchgear for its secondary distribution network.

- In March 2025, Hartek Group secured cumulative orders worth USD 80.8 million across nine Indian states to strengthen regional and interstate transmission networks with high-voltage substations.

- In February 2025, TE Connectivity finalized its USD 2.3 billion acquisition of Richards Manufacturing, a move designed to broaden its footprint in the electrical utilities sector and support critical grid infrastructure upgrades.

- In September 2024, GE Vernova unveiled its GridBeats Automation and Protection System (APS), a software-defined grid solution designed to modernize electrical substations by consolidating multiple protection and control applications onto a single digital platform.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Alternating Current Power System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.1% |

| Market growth 2026-2030 | USD 72211.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.0% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, Italy, UK, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, Turkey, South Africa, UAE and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The alternating current power system market is pivoting toward intelligent, digitized infrastructure, moving beyond conventional hardware to integrated systems. The core of this evolution lies in the adoption of digital twin technology and smart grid technologies, which enable predictive and automated grid management. This shift has allowed some operators to achieve a 30% reduction in maintenance costs.

- Key enabling hardware includes grid-forming (gfm) inverters and solid state transformers (sst), which are critical for integrating variable inverter-based resources (ibrs) and ensuring grid stability. The deployment of flexible ac transmission systems (facts) and reactive power compensation assets addresses issues of bi-directional power flow and voltage control.

- In high-demand environments like data centers, high-density power distribution is managed through advanced power distribution units (pdu) and modular power solutions. Security is paramount, with a focus on ai-enabled zero-trust security and cyber-physical resilience.

- The market continues to rely on foundational components like three-phase power systems, uninterruptible power supplies (ups), and synchronous generators, but with enhanced capabilities driven by new power semiconductor technologies and advanced power conditioning systems.

- Upgrades are also evident in gas-insulated switchgear (gis), medium-voltage ac drives, and high-voltage ac (hvac) transmission networks, while grid-enhancing technologies (gets) are being deployed to maximize existing infrastructure capacity.

What are the Key Data Covered in this Alternating Current Power System Market Research and Growth Report?

-

What is the expected growth of the Alternating Current Power System Market between 2026 and 2030?

-

USD 72.21 billion, at a CAGR of 5.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Three-phase, and Single-phase), End-user (Non-residential, and Residential), Product (Switchgear, Generator, UPS, PDU, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

High-density hyperscale data centers and rise of AI-native AC power distribution units, Crisis of interconnection bottlenecks and grid saturation in high-growth regions

-

-

Who are the major players in the Alternating Current Power System Market?

-

ABB Ltd., Advanced Energy Industries, AEG Power Solutions BV, AMETEK Inc., Borri SpA, Delta Electronics Inc., Eaton Corp. Plc, EnerSys, Fuji Electric Co. Ltd., GE Vernova Inc., Generac Power Systems Inc., Hitachi Energy Ltd., Keysight Technologies Inc., Legrand SA, LS ELECTRIC Co. Ltd., Mitsubishi Electric Corp., Schaefer Inc., Schneider Electric SE, Toshiba Corp. and Vertiv Holdings Co.

-

Market Research Insights

- The market dynamics for alternating current power systems are shaped by the critical need for AC power infrastructure modernization and the management of increasingly complex energy flows. The global transition toward renewable sources is a major factor, with electricity demand projected to grow 2.5 times faster than overall energy demand.

- This shift necessitates intelligent AC power management and inertia-supportive AC infrastructure to stabilize grids. In regions transitioning to green energy, system losses can average as high as 16%, creating a significant incentive for investment in advanced hosting-capacity analytics and predictive fault management systems.

- The emergence of hybrid AC-DC conversion nodes and automated thermal management further reflects a move toward more efficient and resilient power distribution networks capable of supporting both legacy systems and next-generation demands.

We can help! Our analysts can customize this alternating current power system market research report to meet your requirements.

RIA -

RIA -