Ambulatory Healthcare Service Market Size 2024-2028

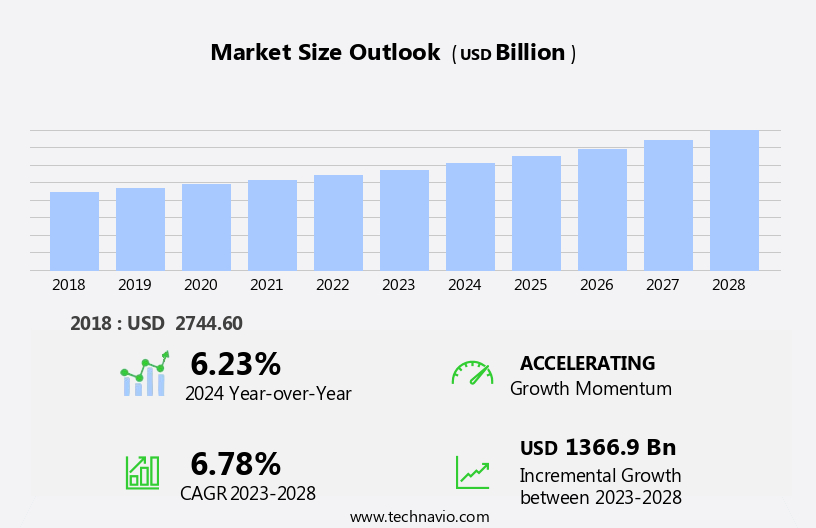

The ambulatory healthcare service market size is forecast to increase by USD 1366.9 billion, at a CAGR of 6.78% between 2023 and 2028.

- The Ambulatory Healthcare Services Market is witnessing significant growth, driven by the increasing prevalence of infectious diseases and favorable reimbursement policies. The rise in chronic diseases and the subsequent need for continuous care outside of hospitals have fueled the demand for ambulatory healthcare services. Furthermore, reimbursement policies that encourage patients to seek care in ambulatory settings rather than hospitals are boosting market growth. However, intensifying company competition poses a significant challenge for market players. As more players enter the market, price competition intensifies, putting pressure on providers to differentiate themselves through quality care and innovative services.

- To capitalize on market opportunities and navigate challenges effectively, companies must focus on delivering high-quality care, leveraging technology to enhance patient experience, and building strategic partnerships to expand their reach.

What will be the Size of the Ambulatory Healthcare Service Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the increasing demand for accessible, efficient, and personalized healthcare solutions. Care coordination models are increasingly being adopted to streamline patient care and improve health outcomes. On-demand healthcare services, such as virtual physician visits and virtual physical therapy, enable patients to access medical expertise from the comfort of their homes. Medical billing software and rehabilitation programs facilitate seamless billing processes and effective treatment plans for chronic diseases. Healthcare compliance standards ensure regulatory adherence, while preventive health screenings and patient portal access empower patients to take an active role in managing their health.

Mental health telehealth services expand access to mental health care, and electronic health records enable efficient data sharing among healthcare providers. Remote patient monitoring and healthcare data analytics enable proactive care and early intervention, while home healthcare services and medication adherence support cater to the needs of vulnerable populations. Value-based care models incentivize quality care and positive health outcomes, and mobile health applications offer convenient access to health information and resources. The market dynamics of the ambulatory healthcare service sector are continually unfolding, with new technologies and care delivery models emerging to meet the evolving needs of patients and healthcare providers.

Integrated care pathways and health outcome metrics facilitate coordinated care, while diagnostic imaging services and specialty medical clinics offer specialized treatments. Appointment scheduling systems and telemedicine platforms streamline patient access to care, and claims processing systems and outpatient procedures ensure efficient and effective healthcare delivery. In summary, the market is characterized by ongoing innovation and adaptation to meet the evolving needs of patients and healthcare providers. From care coordination models and on-demand healthcare to healthcare data analytics and value-based care models, the sector is continually evolving to deliver more accessible, efficient, and personalized healthcare solutions.

How is this Ambulatory Healthcare Service Industry segmented?

The ambulatory healthcare service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

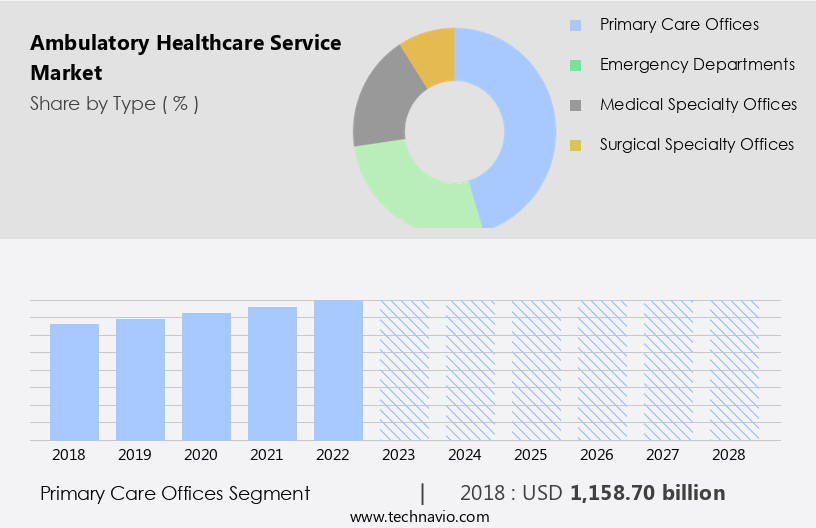

- Primary care offices

- Emergency departments

- Medical specialty offices

- Surgical specialty offices

- Application

- Ophthalmology

- Gastroenterology

- Orthopedics

- Pain management

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Type Insights

The primary care offices segment is estimated to witness significant growth during the forecast period.

The market encompasses a range of entities that aim to enhance patient care and population health management. Primary care offices, led by primary care physicians (PCPs) such as family medicine doctors, gynecologists, and pediatricians, form a significant segment. With an aging population and the increasing prevalence of chronic diseases, this sector's growth is anticipated. Integrated care pathways, health outcome metrics, and chronic disease management are essential components of primary care. Virtual physician visits, virtual physical therapy, remote patient monitoring, and healthcare data analytics further expand the scope of care. Diagnostic imaging services, specialty medical clinics, claims processing systems, appointment scheduling systems, telemedicine platforms, urgent care facilities, and wearable health sensors are other integral parts.

Care coordination models, on-demand healthcare, medical billing software, rehabilitation programs, and healthcare compliance standards ensure efficient and effective care delivery. Preventive health screenings, patient portal access, mental health telehealth, electronic health records, home healthcare services, medication adherence support, mobile health applications, walk-in clinics, patient communication tools, outpatient procedures, value-based care models, and patient engagement tools further enrich the market. The market is evolving, integrating advanced technologies and innovative care models to cater to diverse patient needs.

The Primary care offices segment was valued at USD 1158.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

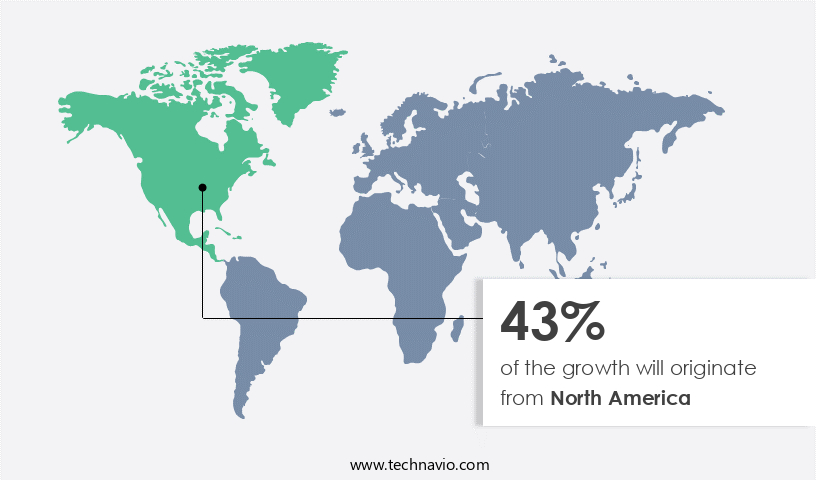

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth due to several factors. The aging population, with an increasing number of individuals aged 65 and above, is driving the expansion of healthcare services in this region. In response to the growing demand for efficient and effective care delivery, healthcare facilities are adopting automated solutions. These include patient satisfaction surveys, population health management, integrated care pathways, health outcome metrics, chronic disease management, diagnostic imaging services, virtual physician visits, virtual physical therapy, remote patient monitoring, healthcare data analytics, specialty medical clinics, claims processing systems, appointment scheduling systems, telemedicine platforms, urgent care facilities, wearable health sensors, care coordination models, on-demand healthcare, medical billing software, rehabilitation programs, healthcare compliance standards, preventive health screenings, patient portal access, mental health telehealth, electronic health records, home healthcare services, medication adherence support, mobile health applications, walk-in clinics, patient communication tools, outpatient procedures, value-based care models, and patient engagement tools.

These technologies and services enable healthcare providers to deliver high-quality care while maintaining regulatory compliance and improving patient outcomes. Additionally, the presence of key companies and strong regulations implemented by government organizations on environmental monitoring in healthcare facilities further propels the market's growth in North America.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Ambulatory Healthcare Service Industry?

- The escalating incidence of infectious diseases serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to various factors. Infectious diseases, fueled by multi-drug resistance among microorganisms and new bacterial and viral diseases, continue to pose a significant health concern worldwide. Recent outbreaks of Ebola, Zika, dengue, Middle East respiratory syndrome, influenza, and severe acute respiratory syndrome have heightened global health awareness. Additionally, population growth, lifestyle changes, and climate change contribute to the increasing prevalence of infectious diseases. Moreover, the demand for emergency medical relief and the need for prompt transfers to medical facilities to save lives further boost the demand for ambulatory healthcare services.

- The ongoing COVID-19 pandemic has presented substantial growth opportunities for market participants. Patient satisfaction surveys, population health management, integrated care pathways, health outcome metrics, chronic disease management, diagnostic imaging services, virtual physician visits, and virtual physical therapy are key trends shaping the market. These trends aim to improve patient care, enhance patient engagement, and optimize healthcare resource utilization. The need for efficient and effective healthcare delivery, coupled with the convenience and affordability of ambulatory care services, is driving market growth. As the healthcare industry continues to evolve, ambulatory healthcare services will play a crucial role in addressing the changing healthcare landscape.

What are the market trends shaping the Ambulatory Healthcare Service Industry?

- Favorable reimbursement policies are increasingly becoming a market trend. It is essential for businesses to offer such policies to remain competitive in today's healthcare industry.

- The market experiences significant growth due to favorable reimbursement policies for these services. In the US, Medicare covers ground and air ambulance transportation for medically necessary services, ensuring patient safety and access to critical healthcare facilities. This policy encourages the expansion of ambulatory healthcare services, including remote patient monitoring, healthcare data analytics, specialty medical clinics, and telemedicine platforms. Furthermore, urgent care facilities and appointment scheduling systems enhance the efficiency and convenience of healthcare delivery. Wearable health sensors and claims processing systems also contribute to the market's growth by enabling continuous patient monitoring and streamlined insurance processing.

- European countries similarly offer attractive reimbursements for ambulance services, further fueling market expansion. The integration of technology and data-driven approaches in ambulatory healthcare services enhances patient care and improves operational efficiency.

What challenges does the Ambulatory Healthcare Service Industry face during its growth?

- The intensification of company competition poses a significant challenge to the industry's growth trajectory. In this competitive landscape, businesses must differentiate themselves through innovation, quality, and customer service to maintain market share and succeed.

- The market encompasses a diverse range of providers delivering care coordination models, on-demand healthcare, rehabilitation programs, and preventive health screenings. companies in this market are increasingly focusing on innovative solutions, such as medical billing software, patient portal access, mental health telehealth, and healthcare compliance standards. The market's competitiveness stems from the presence of numerous regional and local companies, ensuring no single player holds a monopoly. Service differentiation is the primary competitive strategy, with companies offering advantages in service quality, consulting, delivery time, air and road ambulance services, and long-term engagement with buyers.

- The market's growth is driven by the need for efficient, accessible, and personalized healthcare solutions, particularly in the context of an aging population and rising chronic conditions. companies must navigate regulatory requirements and technological advancements to remain competitive and meet evolving consumer demands.

Exclusive Customer Landscape

The ambulatory healthcare service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ambulatory healthcare service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, ambulatory healthcare service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aspen Healthcare Ltd. - This London-based organization specializes in providing comprehensive ambulatory healthcare services, including a renowned Cancer Center. With a focus on patient-centric care, the company leverages advanced technologies and innovative treatments to deliver exceptional outcomes. Their expertise in oncology and other medical specialties sets them apart in the global healthcare landscape.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aspen Healthcare Ltd.

- Ayala Corp.

- DaVita Inc.

- EBOS Group Ltd.

- Envision Healthcare

- Fresenius SE and Co. KGaA

- HCA Healthcare Inc.

- Medical Facilities Corp.

- NueHealth

- SCA health

- Sonic Healthcare Ltd.

- Suomen Terveystalo Oy

- Surgery Partners Inc.

- Tenet Healthcare Corp.

- Universal Health Services Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ambulatory Healthcare Service Market

- In January 2024, Fresenius Medical Care and DaVita Inc., two leading providers of kidney care services, announced a strategic partnership to expand their ambulatory dialysis services in the United States. This collaboration aimed to improve patient access to dialysis care and enhance operational efficiency (Fresenius Medical Care press release, 2024).

- In March 2024, Teladoc Health, a telehealth services provider, acquired Livongo Health, a digital health company specializing in chronic condition management. This acquisition enabled Teladoc Health to expand its offerings in the ambulatory healthcare market, particularly in remote patient monitoring and chronic care management (Teladoc Health press release, 2024).

- In May 2025, the U.S. Centers for Medicare & Medicaid Services (CMS) announced a new rule to increase reimbursement rates for ambulatory surgery centers (ASCs) that meet certain quality requirements. This policy change aimed to incentivize high-quality care and drive growth in the ASC sector (CMS press release, 2025).

- In the same month, UnitedHealth Group, a major health insurer, launched a new virtual primary care service called "Optum Everyday" in partnership with Walgreens. This service aimed to provide patients with convenient access to primary care services through telehealth and in-person visits at Walgreens retail clinics (UnitedHealth Group press release, 2025).

Research Analyst Overview

- In the market, performance monitoring dashboards enable providers to assess operational efficiency and quality improvement initiatives. Remote monitoring devices and mHealth technology facilitate patient-centered care, while medical record integration and health information exchange streamline data access. Specialty care coordination and physician workflow optimization enhance provider network management. Telehealth solutions and home health technology expand access to care, particularly in rural areas. Risk management strategies, patient safety protocols, and data security protocols prioritize patient care and privacy. Predictive analytics models and clinical decision support systems inform evidence-based care, driving cost reduction strategies and revenue cycle management. Personalized medicine and healthcare interoperability pave the way for more effective treatment plans.

- Ambulatory surgery centers and ambulatory care facilities prioritize efficiency and patient-centered care, while staff training programs ensure a skilled workforce. Provider networks and patient engagement strategies remain key focus areas, with telehealth solutions and patient portals fostering stronger relationships between patients and providers. Quality improvement initiatives and cost reduction strategies continue to shape the market, with a growing emphasis on value-based care and population health management. Remote monitoring devices, mHealth technology, and telehealth solutions are transforming ambulatory care delivery, enabling real-time patient monitoring and remote consultations. Healthcare operational efficiency, patient safety, and cost reduction are top priorities, with providers leveraging technology to optimize workflows and reduce readmissions.

- Provider network management and patient engagement strategies are essential for success in the market. Telehealth solutions and patient portals enable stronger relationships between patients and providers, while predictive analytics models and clinical decision support systems inform evidence-based care. Quality improvement initiatives, patient safety protocols, and data security protocols are critical components of the market. Performance monitoring dashboards and telehealth solutions facilitate real-time data analysis and patient care, while cost reduction strategies and revenue cycle management optimize financial performance. Healthcare interoperability and predictive analytics models are driving innovation in the market. Telehealth solutions and remote monitoring devices expand access to care and enable more personalized treatment plans, while patient safety protocols and data security protocols prioritize patient privacy and security.

- The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, mHealth technology, and remote monitoring devices are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies remain essential for success, with a growing emphasis on value-based care and population health management. Ambulatory healthcare services are evolving to prioritize operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care.

- Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is experiencing significant growth, driven by advances in technology and a shift towards value-based care. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a focus on operational efficiency, patient safety, and cost reduction. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction.

- Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management.

- In the market, technology is driving innovation and transformation. Telehealth solutions, remote monitoring devices, and mHealth technology are expanding access to care and enabling more personalized treatment plans. Predictive analytics models and clinical decision support systems inform evidence-based care, while provider network management and patient engagement strategies foster stronger relationships between patients and providers. The market is experiencing significant growth, driven by advances in technology and a shift towards value-based care. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a focus on operational efficiency, patient safety, and cost reduction.

- The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care.

- Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction.

- Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is experiencing significant growth, driven by advances in technology and a shift towards value-based care. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a focus on operational efficiency, patient safety, and cost reduction.

- The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care.

- Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction.

- Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management.

- The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care.

- Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction.

- Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management.

- The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care.

- Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction.

- Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management.

- The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care.

- Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction.

- Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is characterized by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management.

- The market is driven by a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care. Provider network management and patient engagement strategies are essential for success, with a growing emphasis on value-based care and population health management. The market is undergoing significant change, with a focus on operational efficiency, patient-centered care, and cost reduction. Telehealth solutions, remote monitoring devices, and mHealth technology are transforming care delivery, while predictive analytics models and clinical decision support systems inform evidence-based care

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ambulatory Healthcare Service Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 1366.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, Germany, China, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Ambulatory Healthcare Service Market Research and Growth Report?

- CAGR of the Ambulatory Healthcare Service industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the ambulatory healthcare service market growth of industry companies

We can help! Our analysts can customize this ambulatory healthcare service market research report to meet your requirements.

RIA -

RIA -