Analog AI Chip Market Size 2025-2029

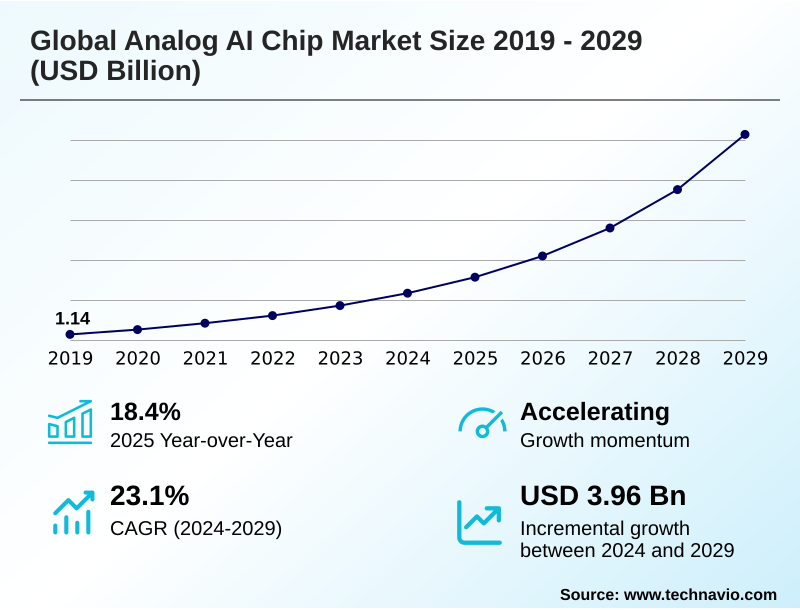

The analog ai chip market size is valued to increase by USD 3.96 billion, at a CAGR of 23.1% from 2024 to 2029. Imperative for enhanced power efficiency in edge computing will drive the analog ai chip market.

Major Market Trends & Insights

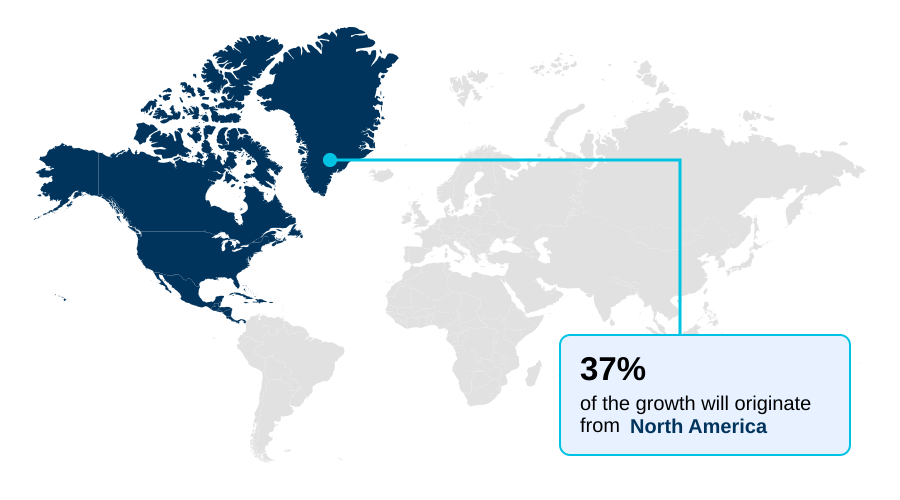

- North America dominated the market and accounted for a 37.3% growth during the forecast period.

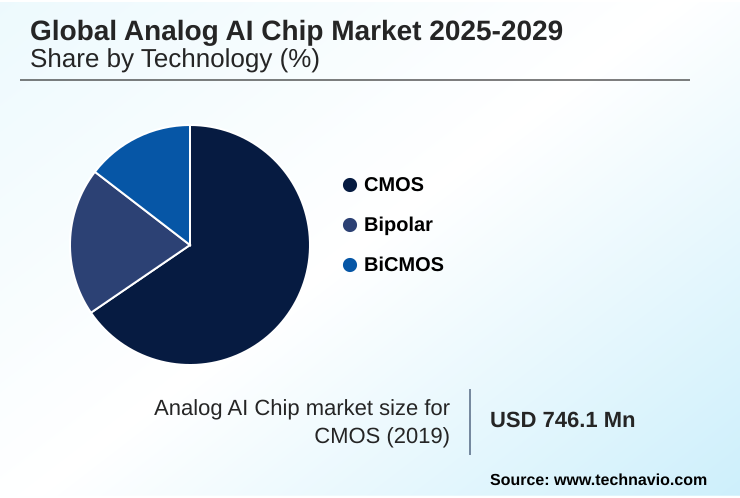

- By Technology - CMOS segment was valued at USD 1.22 billion in 2023

- By Application - Edge computing segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 5.00 billion

- Market Future Opportunities: USD 3.96 billion

- CAGR from 2024 to 2029 : 23.1%

Market Summary

- The analog AI chip market is defined by specialized semiconductors that perform computations using continuous analog signals, fundamentally addressing efficiency limitations in digital processors. By leveraging compute-in-memory architectures, these chips execute complex mathematical operations directly within non-volatile memory arrays, effectively mitigating the von neumann bottleneck that consumes significant energy in traditional systems.

- This architectural shift is driven by the demand for extreme power efficiency and low-latency processing, particularly for on-device AI in edge computing and autonomous systems. In industrial automation, for example, on-premise visual inspection systems can identify microscopic defects in real-time without cloud reliance, ensuring continuous quality control.

- However, the technology faces challenges related to computational precision due to inherent signal noise and process variability. Moreover, the industry is navigating the development of a comprehensive software ecosystem, including specialized compilers and hardware-aware training algorithms, which is essential for wider adoption and unlocking the full potential of this transformative hardware.

What will be the Size of the Analog AI Chip Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Analog AI Chip Market Segmented?

The analog ai chip industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

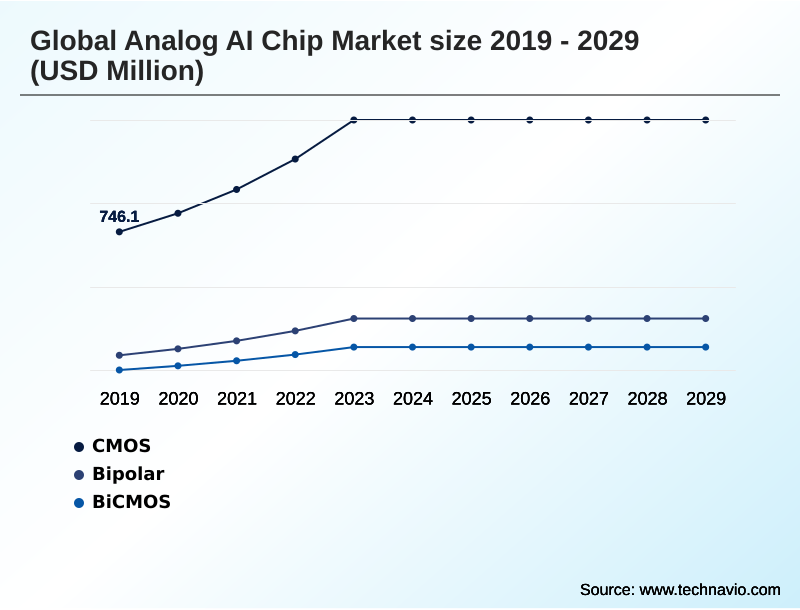

- Technology

- CMOS

- Bipolar

- BiCMOS

- Application

- Edge computing

- Consumer electronics

- Data center

- Automotive

- Healthcare

- Component

- Hardware

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Technology Insights

The cmos segment is estimated to witness significant growth during the forecast period.

The CMOS technology segment is the foundational force in the analog AI chip market, leveraging a mature and cost-effective manufacturing ecosystem.

This technology enables exceptional integration density, which is critical for creating the massively parallel arrays of compute-in-memory cells used in advanced system-on-chip (SoC) design.

The primary advantage of CMOS lies in its low static power, a vital feature for battery-powered edge devices where energy efficiency is a primary constraint.

Applications in consumer electronics and industrial automation benefit from this, with some implementations showing an over 25% improvement in inference task efficiency.

While this approach benefits from processing-in-memory (PIM) and in-sensor computing, it faces challenges from process variation and signal noise, which can affect the precision of medical imaging analysis and smart city infrastructure.

The CMOS segment was valued at USD 1.22 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Analog AI Chip Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is led by North America, which is a hub for research, development, and venture capital, accounting for approximately 37.3% of incremental growth.

This region benefits from a robust ecosystem driving innovation in sensor fusion algorithms and data acquisition for predictive maintenance.

Meanwhile, the APAC region, with its vast manufacturing scale and a projected CAGR of 24.3%, is a critical center for production and has a strategic focus on semiconductor self-sufficiency. Foundries in this region are crucial for visual inspection systems.

Europe carves out a significant role through its powerful automotive and industrial automation sectors, focusing on high-value applications for in-vehicle AI processors. These regional strengths create a competitive and globally interconnected market focused on next-generation deep learning inference.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global analog AI chip market 2025-2029 is advancing through a nuanced cost-benefit analysis of analog AI chips compared to traditional digital hardware. The primary advantages of analog AI for edge devices are rooted in the profound energy efficiency of neuromorphic computing, which is crucial for low-power AI for wearable devices and analog AI for real-time sensor fusion.

- This is evident in compute-in-memory vs digital GPU performance benchmarks, where analog systems demonstrate superior capabilities in handling parallel data streams. The core technology relies on the role of non-volatile memory in analog AI, using ReRAM for synaptic operations to build hardware that mimics neural processes.

- This approach is central to analog AI chip applications in automotive, particularly for analog AI integration with ADAS systems, and for analog processing for voice recognition. However, significant challenges in scaling analog AI production and overcoming noise in analog computing remain.

- The precision limitations of analog hardware necessitate a robust software ecosystem for analog processors, as the development of neuromorphic chips for robotic vision depends on sophisticated design and mapping tools. The analog AI chip manufacturing process is more complex than standard digital fabrication, requiring a hybrid chip design for AI acceleration.

- In industrial IoT, systems using these chips can process sensor data with latency over an order of magnitude lower than cloud-based systems, enabling preemptive failure detection and showcasing the future of compute-in-memory technology.

What are the key market drivers leading to the rise in the adoption of Analog AI Chip Industry?

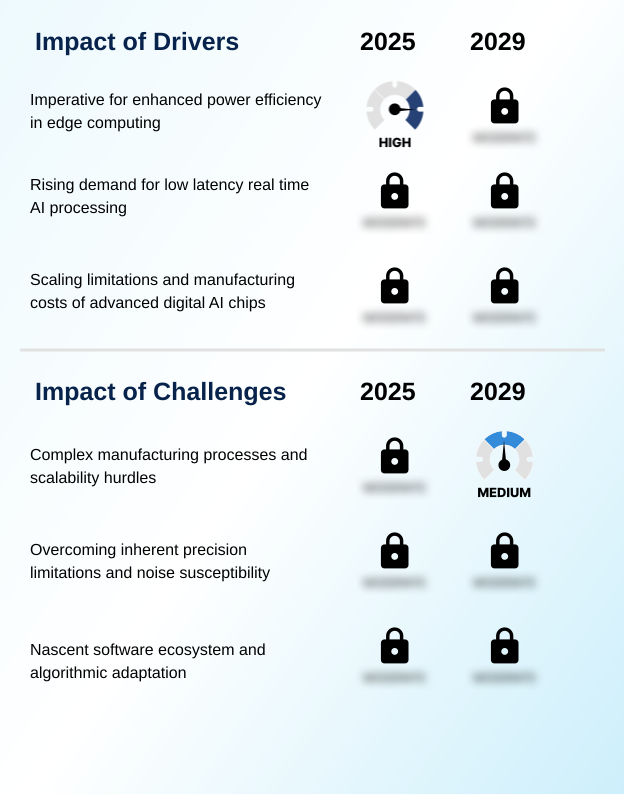

- The imperative for enhanced power efficiency in edge computing applications is a key driver of the market.

- The market is primarily driven by the limitations of digital scaling and the critical need for ultra-low power consumption in a growing number of AI applications.

- Analog architectures, including the analog matrix processor and in-memory computing designs, offer superior computational efficiency by performing parallel data operations directly where data is stored.

- These specialized chips deliver profound improvements in performance-per-watt, with some designs showing up to 100 times greater efficiency than digital counterparts.

- Furthermore, by leveraging mature semiconductor manufacturing processes, the production cost for this hardware can be 30-40% lower compared to leading-edge digital GPUs.

- This economic advantage, coupled with the performance gains from low latency inference and storing synaptic weights locally, makes it a compelling alternative for next-generation hardware.

What are the market trends shaping the Analog AI Chip Industry?

- A primary market trend is the increasing imperative for energy-efficient AI processing at the edge, reflecting a growing demand for on-device intelligence in battery-powered systems.

- A key trend shaping the market is the escalating demand for energy-efficient compute-in-memory (CIM) solutions to enable sophisticated edge AI processing. This shift toward on-device intelligence is driven by the need to overcome the von neumann bottleneck and reduce reliance on cloud connectivity, which enhances data privacy by minimizing raw data transmission by over 90% in certain use cases.

- This approach, leveraging non-volatile memory (NVM) and phase-change memory (PCM), is critical for battery-powered devices requiring always-on sensing capabilities. Architectures based on resistive RAM (ReRAM) deliver real-time responsiveness, with processing delays reduced to microseconds, a significant improvement over some cloud-based alternatives. This trend signals a move toward more powerful and autonomous systems with superior power efficiency.

What challenges does the Analog AI Chip Industry face during its growth?

- Complex manufacturing processes and scalability hurdles represent a key challenge affecting the industry's growth.

- Significant challenges in the market revolve around manufacturing complexities and inherent physical limitations that affect performance. The compute-in-memory architecture, while efficient, is susceptible to process variation, which can introduce calculation errors and reduce model accuracy by up to 5-10% in high-precision tasks. These scalability hurdles complicate the fabrication of hybrid analog-digital chips.

- A nascent software ecosystem and a lack of standardized developer toolchains create another major barrier, as the intellectual property (IP) licensing and electronic design automation (EDA) tools are still evolving. The engineering effort required for neural network deployment can be twice as long compared to development on standard digital hardware, impacting market adoption for machine learning models.

Exclusive Technavio Analysis on Customer Landscape

The analog ai chip market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the analog ai chip market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Analog AI Chip Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, analog ai chip market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - Key offerings include analog matrix processors leveraging compute-in-memory technology, delivering high TOPS performance for energy-efficient edge AI inference.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- Aspinity Inc.

- Infineon Technologies AG

- Intel Corp.

- IBM Corp.

- Micron Technology Inc.

- Mythic Inc.

- NXP Semiconductors NV

- PROPHESEE S.A.

- Qualcomm Inc.

- Rain Neuromorphics Inc.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- SK hynix Co. Ltd.

- Sony Group Corp.

- STMicroelectronics NV

- SynSense

- Syntiant Corp.

- Taiwan Semiconductor Co. Ltd.

- Texas Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Analog ai chip market

- In November 2024, IBM Research unveiled an advanced analog AI chip prototype utilizing phase-change memory technology, demonstrating a substantial reduction in energy consumption for complex AI inference tasks.

- In January 2025, Syntiant Corp. announced a strategic partnership with a major automotive original equipment manufacturer to integrate its next-generation Neural Decision Processors into in-cabin monitoring systems, enabling low-power voice command and driver alertness features.

- In March 2025, Lightmatter announced its Passage platform, a wafer-scale, reconfigurable photonic interconnect designed to directly connect chips and accelerators, addressing data movement bottlenecks in data centers.

- In August 2025, GlobalFoundries announced the expansion of its advanced BiCMOS platform, aimed at enabling next-generation solutions for 6G wireless infrastructure and data center optical interconnects.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Analog AI Chip Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 23.1% |

| Market growth 2025-2029 | USD 3962.1 million |

| Market structure | Concentrated |

| YoY growth 2024-2025(%) | 18.4% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Indonesia, Australia, Germany, UK, France, The Netherlands, Italy, Spain, Saudi Arabia, UAE, South Africa, Egypt, Nigeria, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The analog AI chip market represents a fundamental architectural shift, moving away from the classic von neumann bottleneck by embedding computation directly within memory. This compute-in-memory (CIM) approach utilizes non-volatile memory cells, such as resistive RAM (ReRAM) and phase-change memory (PCM), to perform massively parallel data operations like matrix-vector multiplications.

- The result is ultra-low power consumption, enabling real-time AI processing and on-device intelligence in a way digital tensor processing units (TPUs) cannot match. This trend toward local processing directly informs corporate data governance strategies, as it minimizes cloud data transmission and enhances security compliance.

- Technologies including BiCMOS technology, bipolar junction transistors (BJT), and CMOS technology are leveraged to create these advanced chips, which incorporate analog-to-digital converters (ADCs) and digital-to-analog converters (DACs). Applications are expanding from advanced driver-assistance systems (ADAS) to in-sensor computing and event-based vision systems powered by neural decision processors.

- Specialized hardware like analog front-ends (AFE) and analog matrix processors are key to this evolution. The entire paradigm, including in-memory computing, neuromorphic computing, processing-in-memory (PIM), and even photonic computing, requires hardware-aware training and quantization techniques for effective deployment.

- Early adoptions in smart sensor applications have already demonstrated a power draw reduction of up to 95% for continuous inference tasks compared to conventional microcontroller-based solutions, highlighting the technology's transformative potential.

What are the Key Data Covered in this Analog AI Chip Market Research and Growth Report?

-

What is the expected growth of the Analog AI Chip Market between 2025 and 2029?

-

USD 3.96 billion, at a CAGR of 23.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (CMOS, Bipolar, BiCMOS), Application (Edge computing, Consumer electronics, Data center, Automotive, Healthcare), Component (Hardware, Software, Services) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for enhanced power efficiency in edge computing, Complex manufacturing processes and scalability hurdles

-

-

Who are the major players in the Analog AI Chip Market?

-

Analog Devices Inc., Aspinity Inc., Infineon Technologies AG, Intel Corp., IBM Corp., Micron Technology Inc., Mythic Inc., NXP Semiconductors NV, PROPHESEE S.A., Qualcomm Inc., Rain Neuromorphics Inc., Renesas Electronics Corp., Samsung Electronics Co. Ltd., SK hynix Co. Ltd., Sony Group Corp., STMicroelectronics NV, SynSense, Syntiant Corp., Taiwan Semiconductor Co. Ltd. and Texas Instruments Inc.

-

Market Research Insights

- The market's dynamics are shaped by a strategic pivot toward architectures that prioritize power efficiency and computational efficiency to support demanding AI workloads. This shift enables always-on sensing capabilities in edge devices while consuming up to 75% less power than digital counterparts, significantly extending operational life.

- Furthermore, implementations have demonstrated a reduction in data transmission for inference tasks by up to 90%, directly lowering network bandwidth costs and enhancing data privacy. While the technology is highly specialized, its direct impact on operating expenditures makes it a critical purchase decision for original equipment manufacturers.

- The nascent developer toolchains and the need for neural network deployment expertise represent current adoption hurdles, though the performance benefits are compelling for machine learning models in various sectors.

We can help! Our analysts can customize this analog ai chip market research report to meet your requirements.

RIA -

RIA -