AI Computing Hardware Market Size 2025-2029

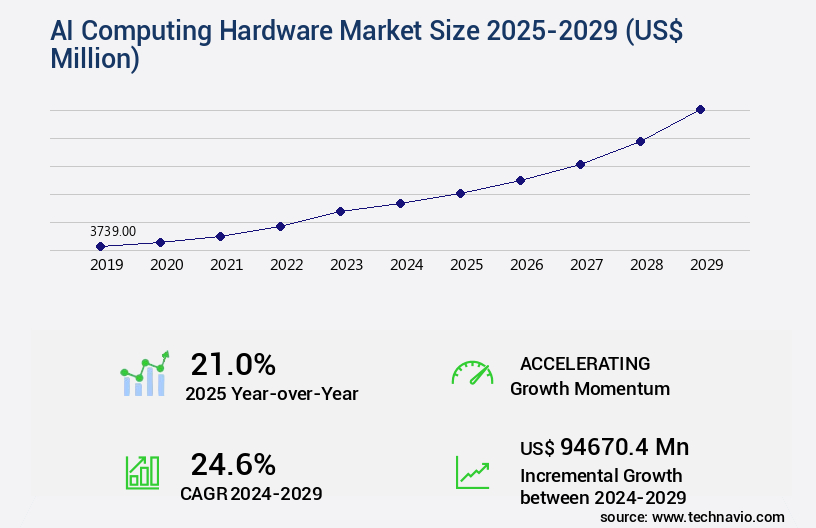

The AI computing hardware market size is valued to increase by USD 94.67 billion, at a CAGR of 24.6% from 2024 to 2029. Proliferation and escalating complexity of generative AI models will drive the ai computing hardware market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 36% growth during the forecast period.

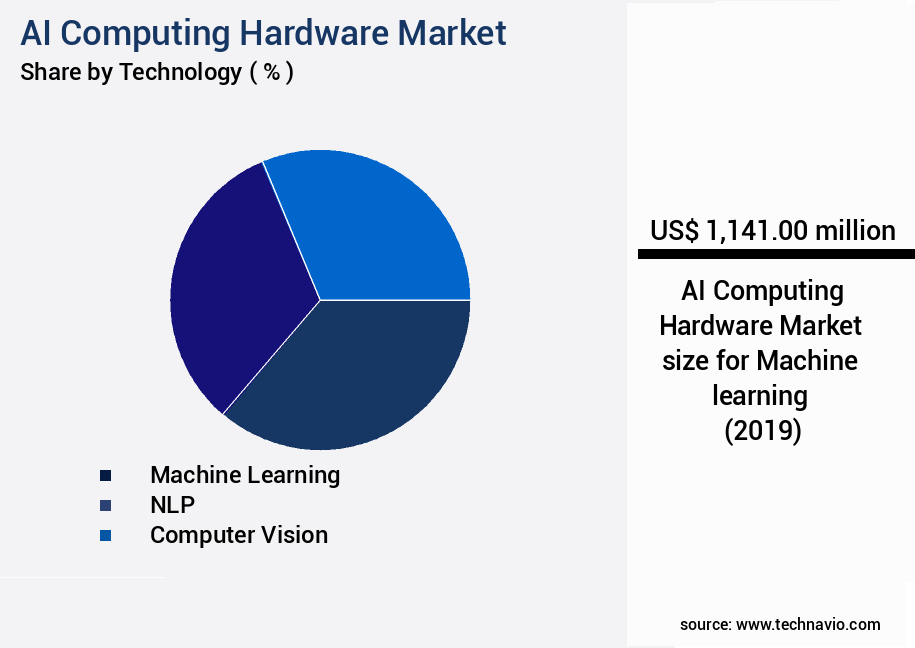

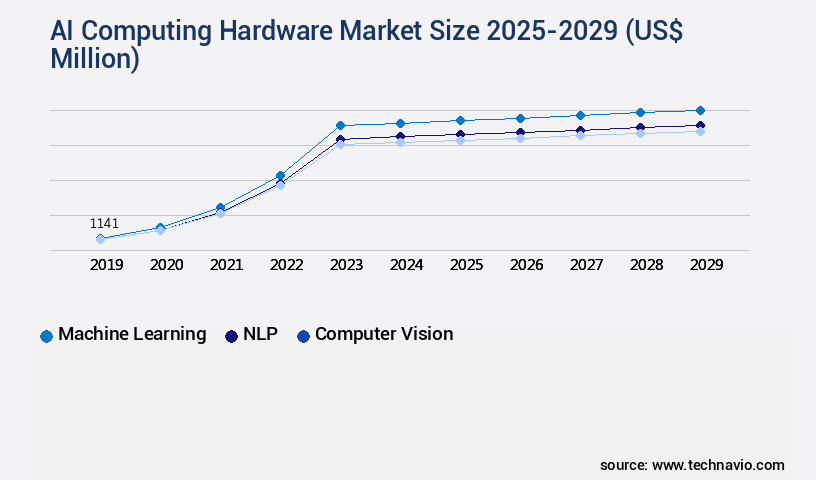

- By Technology - Machine learning segment was valued at USD 1.14 billion in 2023

- By Product Type - GPU segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 3.00 million

- Market Future Opportunities: USD 94670.40 million

- CAGR from 2024 to 2029 : 24.6%

Market Summary

- The market is experiencing unprecedented growth, fueled by the increasing demand for advanced artificial intelligence (AI) applications across various industries. This expansion is driven by the proliferation and escalating complexity of generative AI models, which necessitate increasingly powerful and efficient hardware. Moreover, hyperscalers, such as Google, Microsoft, and Amazon, are leading this evolution by investing in custom silicon and vertical integration. This strategy allows them to optimize hardware for specific AI workloads and reduce reliance on third-party companies.

- However, the market's growth is not without challenges. Supply chain constraints and manufacturing complexities persist, as the production of advanced AI chips requires specialized facilities and expertise. Despite these hurdles, the future of the market looks promising. Innovations in materials science, manufacturing processes, and design are expected to address these challenges and pave the way for even more powerful and energy-efficient AI hardware. As businesses continue to adopt AI to gain a competitive edge, the demand for advanced computing hardware will only grow, making it an exciting space to watch.

What will be the Size of the AI Computing Hardware Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Computing Hardware Market Segmented ?

The ai computing hardware industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Machine learning

- NLP

- Computer vision

- Others

- Product Type

- GPU

- CPU

- ASIC

- Field programmable gate array

- Others

- End-user

- Healthcare

- Automotive

- Financial services

- Retail

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Technology Insights

The machine learning segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant evolution, driven by the surging demand for advanced machine learning (ML) and artificial intelligence (AI) technologies. ML, particularly deep learning, necessitates specialized hardware capable of executing massive parallel computations, primarily matrix multiplications and vector operations, to learn patterns from data. Custom ASICs, GPUs, FPGAs, TPUs, and other processors are designed to meet these requirements, with companies continually innovating to enhance computational throughput, memory bandwidth, and energy efficiency. Heat dissipation and power management are critical concerns, with thermal design power reaching new heights. Cloud computing platforms, data center infrastructure, and edge computing are adopting advanced cooling systems and power management strategies to maintain optimal operating conditions.

Parallel processing, distributed computing, and neural network architectures are other essential elements, with hardware security modules ensuring data encryption and protection. The market is further characterized by the integration of containerization technologies, server virtualization, and software-defined networking to optimize input/output performance, network latency, and cache memory. Instruction set architecture, processor architecture, and inference optimization are ongoing areas of research, while precision computing, quantum computing, and deep learning frameworks are emerging trends. A recent report suggests that the global AI chip market is projected to reach USD118.67 billion by 2027, underscoring the market's immense potential.

The Machine learning segment was valued at USD 1.14 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Computing Hardware Market Demand is Rising in North America Request Free Sample

The market is characterized by its dynamic nature, with North America leading the global landscape. The region, primarily driven by the United States, serves as the hub for the entire ecosystem, encompassing hardware designers such as NVIDIA, AMD, Intel, and Qualcomm, and major consumers including Microsoft, Google, Amazon Web Services, Meta, and OpenAI. This concentration of both supply and demand fosters a self-reinforcing cycle of innovation. The regional market growth is fueled by the substantial investments of hyperscale companies in expanding their data center infrastructure to accommodate the burgeoning generative AI sector.

According to recent reports, the North American market is expected to account for over 45% of the market share by 2027. Furthermore, the Asia Pacific region is projected to witness significant growth, driven by the increasing adoption of AI technologies in countries like China and India.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses and organizations increasingly adopt artificial intelligence (AI) technologies to enhance their operations and gain a competitive edge. One of the key areas of focus in this market is the development and implementation of hardware solutions for training AI models, particularly on GPUs and FPGAs. GPUs offer high computational power for parallel processing, making them ideal for training large neural networks. FPGAs, on the other hand, offer flexibility and configurability, making them suitable for implementing neural networks with specific requirements. However, the high power consumption of AI model training in data centers poses a challenge for the industry. To address this, high-performance computing clusters are being used to optimize energy efficiency and reduce costs.

Distributed deep learning frameworks like TensorFlow and MPI-DNN are also gaining popularity for their ability to distribute workloads across multiple nodes, reducing the time and resources required for training. Memory capacity limitations and efficient data transfer protocols are other critical considerations in the market. Hardware acceleration for inference is also essential, with custom ASIC designs and system-on-a-chip integration becoming increasingly common. Cooling solutions for high-density servers and network optimization for AI workloads are also important, as is data security in AI computing. Edge AI computing deployment is another emerging trend, with AI chip architecture comparisons and parallel processing algorithms being key areas of research. Performance tuning strategies and software-defined networking implementation are also important for optimizing AI workloads, while container orchestration for AI and thermal management techniques ensure reliable and efficient operation. Overall, the market is a dynamic and complex landscape, with ongoing innovation and development driving growth and competition.

What are the key market drivers leading to the rise in the adoption of AI Computing Hardware Industry?

- The relentless expansion and intricacy of generative AI models serve as the primary catalyst for market growth.

- The market is experiencing a significant evolution due to the escalating complexity and insatiable computational demands of generative AI, particularly large language models and multimodal systems. These advanced models, such as OpenAIs GPT-4, require thousands of high-performance accelerators, like GPUs and specialized ASICs, to train effectively. The size of the datasets used for training also directly impacts the computational requirements. This high-intensity workload has created an unprecedented and enduring demand for the most advanced hardware. The release of GPT-4 in March 2023 served as a major inflection point, showcasing the transformative potential of large-scale AI and triggering a global race to acquire the necessary compute power.

- With the increasing number of AI applications across various sectors, including healthcare, finance, and manufacturing, the market for AI computing hardware is poised for continued growth. The market's expansion is driven by the need for hardware that can handle the complex computations required by these advanced AI models, making it a vital investment for businesses seeking to leverage AI technology.

What are the market trends shaping the AI Computing Hardware Industry?

- The rise of custom silicon and vertical integration is an emerging trend in the market for hyperscalers. Hyperscalers are increasingly adopting these strategies to gain a competitive edge.

- The market is undergoing a significant transformation as hyperscale cloud providers adopt an integrated approach to hardware design. This strategic shift is driven by multiple factors. First, the need to optimize hardware for specific software workloads is paramount for these tech giants. Second, reducing long-term operational costs and power consumption is a critical concern. Lastly, gaining control over the supply chain is a strategic imperative. Instead of relying solely on merchant silicon companies, these companies are investing heavily in creating custom Application Specific Integrated Circuits (ASICs) and processors.

- For instance, Google's TPUs (Tensor Processing Units) and Amazon's Graviton processors are testament to this trend. The customization of hardware for AI workloads is expected to increase efficiency and performance, making it a game-changer in the industry.

What challenges does the AI Computing Hardware Industry face during its growth?

- The intricacies of supply chain management and manufacturing complexities pose significant challenges to the industry's growth trajectory.

- The market is undergoing significant transformation, driven by the escalating demand for advanced technologies in various sectors. The production of cutting-edge AI accelerators relies on a specialized and intricate supply chain, with a limited number of key players controlling the manufacturing of leading-edge logic chips. Taiwan Semiconductor Manufacturing Company (TSMC) holds a dominant position in this area, creating considerable bottlenecks due to its monopolistic control. The complexity intensifies with advanced packaging technologies, such as TSMC's Chip-on-Wafer-on-Substrate (CoWoS), which are indispensable for integrating high-bandwidth memory with the processor die.

- The demand for high-performance GPUs, particularly NVIDIA's H100, has surged throughout 2023, leading to severe shortages and extended lead times. Reports suggest waits of over six months, underscoring the market's challenges. Despite these hurdles, the market continues to evolve, offering substantial opportunities for innovation and growth.

Exclusive Technavio Analysis on Customer Landscape

The ai computing hardware market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai computing hardware market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Computing Hardware Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai computing hardware market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - This tech firm specializes in advanced AI computing hardware, including Instinct MI300 accelerators and Ryzen AI processors, delivering superior performance for data-intensive workloads. These innovative solutions empower businesses to make smarter decisions and drive industry advancements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon Web Services Inc.

- Apple Inc.

- Axelera AI B.V.

- Cerebras

- Flex Logix Technologies Inc.

- Google Cloud

- Graphcore Ltd.

- Groq Inc.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- International Business Machines Corp.

- IonQ Inc.

- Microsoft Corp.

- Mythic Inc.

- NVIDIA Corp.

- Qualcomm Inc.

- SambaNova Systems Inc.

- Samsung Electronics Co. Ltd.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Computing Hardware Market

- In January 2024, Intel Corporation announced the launch of its new neuromorphic research chip, Loihi 2, designed for artificial intelligence (AI) workloads. This chip is a significant advancement in AI computing hardware, as it emulates the human brain's structure and function, enabling more efficient and effective AI processing (Intel Press Release, 2024).

- In March 2024, NVIDIA Corporation and Microsoft Corporation announced a strategic partnership to develop and deploy AI solutions using NVIDIA's GPUs on Microsoft's Azure cloud platform. This collaboration is expected to accelerate AI innovation and adoption across industries (Microsoft News Center, 2024).

- In April 2025, Google LLC announced a USD1 billion investment in its AI hardware division, Tensor Processing Units (TPUs), to expand its AI capabilities and maintain its market leadership. This investment underscores Google's commitment to AI technology and its potential impact on various industries (Google Investor Relations, 2025).

- In May 2025, IBM Corporation and Samsung Electronics Co. Ltd. Announced a joint venture to develop and manufacture AI chips based on IBM's AI technology and Samsung's semiconductor expertise. This collaboration aims to address the growing demand for AI computing hardware and reduce the reliance on traditional CPU and GPU architectures (IBM Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Computing Hardware Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

253 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24.6% |

|

Market growth 2025-2029 |

USD 94670.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

21.0 |

|

Key countries |

US, China, Japan, Canada, South Korea, Germany, Mexico, UK, India, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by the increasing demand for advanced technologies in various sectors. Custom ASICs, designed specifically for AI workloads, are gaining traction due to their superior performance and power efficiency. However, the challenge of heat dissipation in these high-performance systems necessitates innovative thermal design power solutions. Cloud computing platforms are at the forefront of this market, offering access to vast computing resources for AI model training and inference. Parallel processing, distributed computing, and containerization technologies enable efficient utilization of these resources. Neural network architectures, such as deep learning frameworks, require massive computational power and memory bandwidth, driving the adoption of GPUs, TPUs, FPGAs, and other specialized hardware.

- High-performance computing applications, including quantum computing and precision computing, further expand the market's scope. Security concerns are addressed through hardware security modules and data encryption, ensuring data integrity and confidentiality. Power management and cooling systems are essential components in optimizing the performance and efficiency of these systems. An example of this market's dynamics is the significant increase in sales of AI-optimized hardware for data center infrastructure. According to recent estimates, the AI hardware market is expected to grow by over 30% annually, driven by the continuous development of neural network architectures and the increasing demand for AI applications across industries.

- Input/output performance, network latency, memory controllers, and cache memory are crucial factors in enhancing the overall performance of these systems. Inference optimization and software-defined networking further improve the efficiency and flexibility of AI computing hardware. In conclusion, the market is a dynamic and evolving landscape, driven by the continuous advancements in AI technologies and their applications across various sectors. The market's growth is expected to remain robust, with ongoing innovations in hardware design, power management, and cooling systems playing a significant role.

What are the Key Data Covered in this AI Computing Hardware Market Research and Growth Report?

-

What is the expected growth of the AI Computing Hardware Market between 2025 and 2029?

-

USD 94.67 billion, at a CAGR of 24.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Machine learning, NLP, Computer vision, and Others), Product Type (GPU, CPU, ASIC, Field programmable gate array, and Others), End-user (Healthcare, Automotive, Financial services, Retail, and Others), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation and escalating complexity of generative AI models, Supply chain constraints and manufacturing complexities

-

-

Who are the major players in the AI Computing Hardware Market?

-

Advanced Micro Devices Inc., Amazon Web Services Inc., Apple Inc., Axelera AI B.V., Cerebras, Flex Logix Technologies Inc., Google Cloud, Graphcore Ltd., Groq Inc., Huawei Technologies Co. Ltd., Intel Corp., International Business Machines Corp., IonQ Inc., Microsoft Corp., Mythic Inc., NVIDIA Corp., Qualcomm Inc., SambaNova Systems Inc., Samsung Electronics Co. Ltd., and Tenstorrent Inc.

-

Market Research Insights

- The market for AI computing hardware is a dynamic and ever-evolving landscape, characterized by continuous advancements in technology and increasing demand for more efficient and scalable solutions. Two notable developments in this domain include the growing adoption of field-programmable gate arrays (FPGAs) and the integration of tensor processing units (TPUs) in data analytics platforms. FPGAs have gained traction due to their flexibility and ability to adapt to various AI workloads. For instance, a leading technology company reported a 4x increase in machine learning inference throughput by implementing FPGAs in their data centers. Moreover, The market is projected to grow at a significant rate, with industry analysts estimating a 25% compound annual growth rate over the next five years.

- These advancements are driven by the need for more energy-efficient algorithms, scalable architectures, and fault tolerance in AI systems. As the market continues to evolve, we can expect further innovations in areas such as hardware-software co-design, data center cooling, and open-source software, among others. The integration of these technologies will enable real-time inference, high-speed interconnect, and cloud-based deployment, ultimately enhancing the overall performance of AI systems.

We can help! Our analysts can customize this AI computing hardware market research report to meet your requirements.

RIA -

RIA -