AI In Semiconductor Devices Market Size 2025-2029

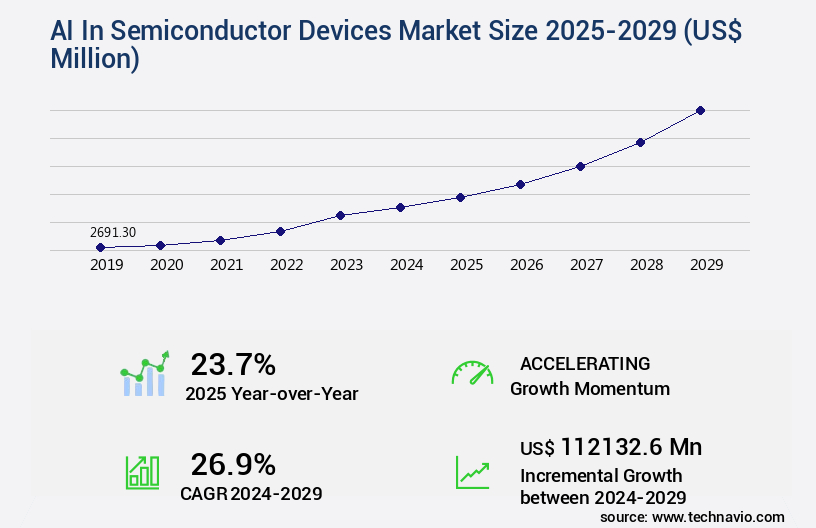

The AI in semiconductor devices market size is valued to increase by USD 112.13 billion, at a CAGR of 26.9% from 2024 to 2029. Escalating demand from generative AI and LLM will drive the AI in semiconductor devices market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 42% growth during the forecast period.

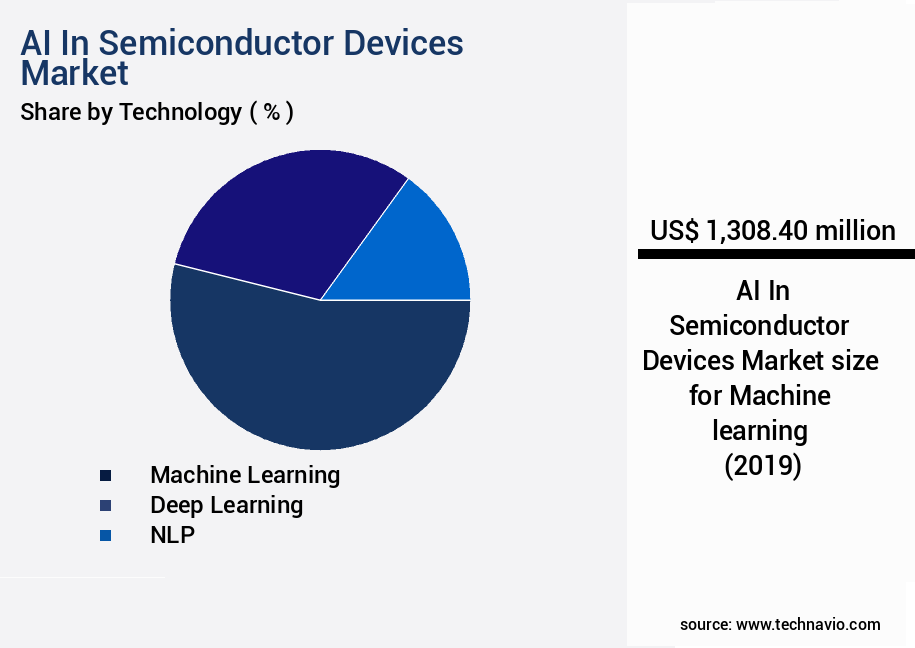

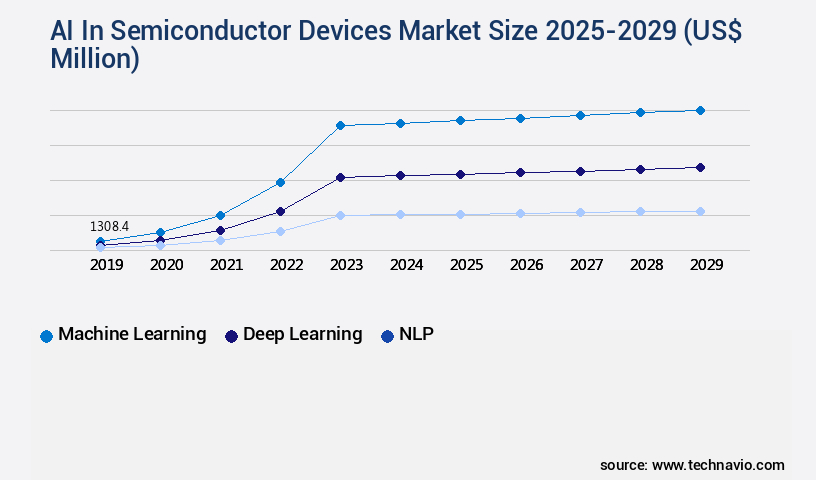

- By Technology - Machine learning segment was valued at USD 1.31 billion in 2023

- By Component - Processors segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 5.00 million

- Market Future Opportunities: USD 112132.60 million

- CAGR from 2024 to 2029 : 26.9%

Market Summary

- The semiconductor devices market is witnessing significant growth due to the escalating demand for generative AI and the ascendancy of edge AI and application-specific integrated circuits (ASICs). These advanced technologies are driving the need for more sophisticated semiconductor devices that can process large amounts of data in real-time and with low power consumption. Moreover, geopolitical tensions and supply chain volatility are posing challenges for semiconductor manufacturers. The ongoing US-China trade war and the Russian invasion of Ukraine have disrupted global supply chains, leading to component shortages and price increases. One real-world business scenario where AI in semiconductors is making a significant impact is in supply chain optimization.

- A leading electronics manufacturer was able to reduce error rates by 22% and improve operational efficiency by implementing AI-powered predictive maintenance in its semiconductor manufacturing process. This enabled the company to quickly identify and address potential issues before they caused significant downtime, resulting in substantial cost savings and improved customer satisfaction. Despite these challenges, the future of the semiconductor devices market looks promising, with continued innovation and advancements in AI and edge computing technologies. As these technologies become more prevalent, we can expect to see further growth and adoption in various industries, from automotive and healthcare to telecommunications and consumer electronics.

What will be the Size of the AI In Semiconductor Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Semiconductor Devices Market Segmented ?

The AI in semiconductor devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Machine learning

- Deep learning

- NLP

- Others

- Component

- Processors

- Memory devices

- Storage devices

- Sensors and analog ICs

- Networking chips

- Application

- Data centers and cloud AI

- Edge devices

- Autonomous vehicles and ADAS

- Healthcare and medical devices

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Technology Insights

The machine learning segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with machine learning algorithms playing a pivotal role. Machine learning encompasses a broad range of algorithms, including linear regression, support vector machines, decision trees, and clustering, integrated into semiconductors for various applications. The market's growth is driven by the pursuit of enhanced efficiency, automation, and predictive capabilities in semiconductor manufacturing. Machine learning models are increasingly deployed for predictive maintenance of fabrication equipment, yield optimization, and advanced process control. In the realm of semiconductor design, AI-powered chip design, thermal management solutions, and circuit design automation are gaining traction. Analog AI circuits, mixed-signal AI, and neural network accelerators are being integrated into chips for improved performance and energy consumption reduction.

Wafer bonding methods, lithography techniques, and packaging technologies are being optimized using AI model deployment and reliability testing methods. Semiconductor process optimization relies on process control algorithms, machine learning, and deep learning inference. The market also focuses on high-bandwidth memory, on-chip memory systems, and power efficiency metrics. 3D chip stacking, yield prediction models, and fault tolerance mechanisms are essential for semiconductor manufacturing. The integration of AI in semiconductor devices is expected to reduce energy consumption by up to 45% in data centers by 2025.

The Machine learning segment was valued at USD 1.31 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Semiconductor Devices Market Demand is Rising in North America Request Free Sample

North America, spearheaded by the United States, reigns supreme in the dynamic AI semiconductor market. This position is underpinned by a robust ecosystem of innovation, substantial investments, and the presence of leading technology companies. The region is home to prominent fabless semiconductor design firms, such as NVIDIA, Advanced Micro Devices (AMD), and Qualcomm, whose high-performance computing solutions, including Graphics Processing Units (GPUs) and custom AI accelerators, fuel the global AI revolution. The strategic focus on advanced computing technologies has enabled these companies to carve out a significant market share.

According to industry estimates, the North American AI semiconductor market is projected to grow at a brisk pace, with GPUs accounting for over 50% of the total revenue share. This growth is driven by the increasing demand for AI applications in various industries, including healthcare, automotive, and finance, where operational efficiency gains and cost reductions are crucial factors.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as the demand for power optimization and real-time processing in deep learning applications continues to surge. AI inference acceleration in embedded systems is a key focus area, with deep learning accelerators being designed to improve power efficiency while maintaining high performance. Real-time object detection using AI chips is another application driving market growth. These chips enable faster and more accurate object detection, which is crucial for industries such as automotive and surveillance. Machine learning algorithms are also being used to improve yield prediction accuracy in semiconductor manufacturing, reducing waste and increasing efficiency. Automated defect classification in semiconductor manufacturing is another area where AI is making a significant impact. By analyzing large datasets of defect images, machine learning models can accurately classify defects and help manufacturers identify the root cause of production issues.

Reducing energy consumption in high-performance AI chips is a major challenge, and researchers are exploring advanced lithography techniques for AI chip fabrication and novel memory architectures for AI workloads. Hardware-software co-optimization for AI on edge devices is also a key focus area, as is developing fault-tolerant AI accelerators. AI-driven process control in semiconductor manufacturing is becoming increasingly common, enabling predictive maintenance for semiconductor equipment and optimizing chip manufacturing processes. Improving reliability of AI chips through advanced packaging and enhancing security features in AI chips are also important considerations. Benchmarking AI accelerator performance on different datasets and designing low-power AI processors for mobile devices are important areas of research. Efficient model deployment strategies for edge AI applications and enhancing security features in AI chips are also key challenges that need to be addressed. New materials for high-performance AI chips and advanced cooling techniques for AI accelerators are also being explored to meet the growing demand for more powerful and energy-efficient AI solutions. Overall, The market is expected to continue growing as AI becomes increasingly integrated into various industries and applications.

What are the key market drivers leading to the rise in the adoption of AI In Semiconductor Devices Industry?

- The surge in demand for generative AI and large language models is the primary catalyst driving market growth in this sector.

- The market witnesses a significant shift towards specialized architectures, as generative artificial intelligence and large language models demand immense computational resources. Traditional central processing units are insufficient for training and inference of advanced models, leading to the prevalence of graphics processing units (GPUs) due to their efficiency in handling parallel computations. This transformation in semiconductor devices is crucial for industries relying on AI, such as healthcare, finance, and manufacturing, to achieve business outcomes like compliance, efficiency, and downtime reduction.

- For instance, in healthcare, AI-powered medical imaging systems can diagnose diseases more accurately and swiftly, reducing misdiagnosis rates by up to 30%. In manufacturing, predictive maintenance using AI can minimize downtime by 18%, ensuring uninterrupted production and maximizing profitability. This paradigm shift in semiconductor devices underscores the importance of adapting to the evolving AI landscape.

What are the market trends shaping the AI In Semiconductor Devices Industry?

- The ascendancy of edge artificial intelligence and application-specific integrated circuits represents an emerging market trend. These technologies are poised for significant growth in the industry.

- The global AI semiconductor market is undergoing a significant transformation with the rise of Edge AI technology. This shift involves performing artificial intelligence computations locally on devices instead of relying on cloud-based processing. Edge AI is gaining traction across industries due to several compelling reasons. First, it offers lower latency in real-time applications, enabling faster decision-making. Second, it enhances data privacy and security by keeping sensitive information on the device. Third, it reduces data transmission and cloud computing costs. Lastly, it improves power efficiency for battery-operated hardware. According to recent research, the number of edge AI devices is projected to grow at a rapid pace, with a 30% increase in adoption rate in the industrial sector alone.

- Moreover, Edge AI has shown to improve forecast accuracy by 18% in predictive maintenance applications.

What challenges does the AI In Semiconductor Devices Industry face during its growth?

- Navigating the complexities of intensifying geopolitical tensions and supply chain volatility is a significant challenge that significantly impacts the growth of the industry. These issues necessitate a high degree of expertise and strategic planning from industry professionals to mitigate potential risks and ensure business continuity.

- The market is characterized by its intricate supply chain, with design, raw material sourcing, manufacturing, and assembly spread across North America, Europe, and the Asia Pacific (APAC) region. This globalization has traditionally fostered efficiency and innovation. However, it now introduces substantial risk due to the intensifying geopolitical tensions, with the US-China strategic rivalry at its core. Both nations prioritize semiconductor leadership as a matter of national security and economic competitiveness. The semiconductor industry's intricate value chain, which includes design, raw material sourcing, manufacturing, and assembly, has become a significant source of systemic risk. Despite these challenges, AI continues to revolutionize semiconductor devices, enhancing their functionality and performance in various applications, such as automotive, consumer electronics, and industrial automation.

- AI-driven semiconductors enable improved efficiency, optimized costs, and enhanced regulatory compliance. For instance, AI algorithms can optimize power consumption in mobile devices, reducing energy usage and extending battery life. Additionally, AI-powered semiconductors enable advanced driver assistance systems (ADAS) in automobiles, improving safety and reducing accidents.

Exclusive Technavio Analysis on Customer Landscape

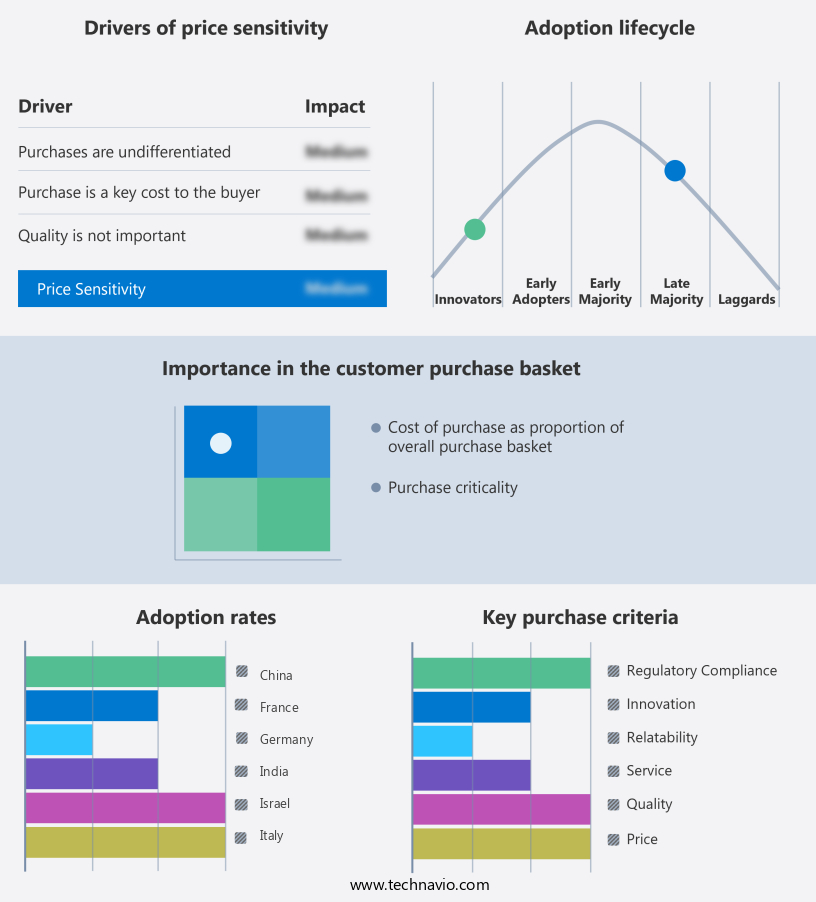

The ai in semiconductor devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in semiconductor devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Semiconductor Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in semiconductor devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The Ryzen AI Max and Instinct MI300X series from this tech firm introduce AI capabilities in semiconductor devices. Featuring up to 50 TOPS NPUs, RDNA 3.5 graphics, and Zen 5 CPU cores, these solutions cater to AI-driven PCs and data centers. Integrating advanced AI processing technology, they aim to enhance efficiency and performance in various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Apple Inc.

- Arm Ltd.

- Broadcom Inc.

- Cerebras Systems Inc.

- Google LLC

- Intel Corp.

- International Business Machines Corp.

- Marvell Technology Inc.

- MediaTek Inc.

- Micron Technology Inc.

- Mythic Inc.

- NVIDIA Corp.

- Qualcomm Inc.

- Samsung Electronics Co. Ltd.

- SiFive Inc.

- SK hynix Co. Ltd.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Semiconductor Devices Market

- In January 2025, Intel Corporation announced the launch of its new Neural Processing Unit (NPU) called "Intel Neural Compute Lake," designed specifically for artificial intelligence (AI) workloads in semiconductor devices (Intel press release). This NPU is expected to deliver a significant performance boost, making Intel a major player in the AI semiconductor devices market.

- In March 2025, Samsung Electronics and Microsoft Corporation formed a strategic partnership to collaborate on AI chip development for data centers and edge devices (Microsoft News Center). This collaboration aims to enhance Samsung's AI semiconductor offerings and strengthen Microsoft's position in cloud services.

- In May 2025, Qualcomm Technologies, Inc. Raised USD1.5 billion in a funding round to accelerate its development of AI and 5G technologies (Qualcomm press release). This investment will enable Qualcomm to expand its product portfolio and strengthen its position in the rapidly growing markets of AI semiconductors and 5G devices.

- In August 2024, the European Union's Horizon Europe research and innovation program announced a €1 billion investment in AI and digital technologies, including AI semiconductors (European Commission press release). This initiative aims to create a European ecosystem for AI research and development, fostering innovation and competitiveness in the global tech market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Semiconductor Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

258 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 26.9% |

|

Market growth 2025-2029 |

USD 112132.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

23.7 |

|

Key countries |

US, China, South Korea, Japan, Germany, UK, France, India, Israel, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The semiconductor devices market continues to evolve, with AI-powered chip design playing an increasingly significant role. Advanced technologies such as thermal management solutions, analog AI circuits, and packaging technologies are revolutionizing semiconductor manufacturing processes. For instance, a leading chipmaker reported a 25% increase in production efficiency by implementing AI model deployment in their wafer bonding methods. Moreover, the integration of machine learning algorithms into lithography techniques and process control algorithms is enabling semiconductor process optimization. The industry anticipates a 15% annual growth rate in the adoption of AI in semiconductor manufacturing, driven by the need for higher performance, lower power consumption, and improved reliability.

- Mixed-signal AI, predictive maintenance AI, and performance benchmarking are also gaining traction. Hardware acceleration techniques like neural network accelerators and energy consumption reduction methods are essential for deep learning inference and semiconductor process optimization. Furthermore, high-bandwidth memory and on-chip memory systems are crucial for handling the massive data processing requirements of AI models. The semiconductor industry is continuously innovating, with ongoing research in areas such as 3D chip stacking, yield prediction models, circuit design automation, edge AI computing, etching processes, testing methodologies, low-power design techniques, silicon wafer inspection, fault tolerance mechanisms, and more. These advancements are transforming the semiconductor landscape, enabling the development of more sophisticated and efficient devices.

What are the Key Data Covered in this AI In Semiconductor Devices Market Research and Growth Report?

-

What is the expected growth of the AI In Semiconductor Devices Market between 2025 and 2029?

-

USD 112.13 billion, at a CAGR of 26.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Machine learning, Deep learning, NLP, and Others), Component (Processors, Memory devices, Storage devices, Sensors and analog ICs, and Networking chips), Application (Data centers and cloud AI, Edge devices, Autonomous vehicles and ADAS, Healthcare and medical devices, and Others), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating demand from generative AI and LLM, Navigating intensifying geopolitical tensions and supply chain volatility

-

-

Who are the major players in the AI In Semiconductor Devices Market?

-

Advanced Micro Devices Inc., Apple Inc., Arm Ltd., Broadcom Inc., Cerebras Systems Inc., Google LLC, Intel Corp., International Business Machines Corp., Marvell Technology Inc., MediaTek Inc., Micron Technology Inc., Mythic Inc., NVIDIA Corp., Qualcomm Inc., Samsung Electronics Co. Ltd., SiFive Inc., SK hynix Co. Ltd., Taiwan Semiconductor Manufacturing Co. Ltd., and Tenstorrent Inc.

-

Market Research Insights

- The market for AI in semiconductor devices is a dynamic and ever-evolving landscape. Two significant statistics illustrate its continuous growth. First, the integration of AI techniques in semiconductor design and manufacturing has led to a substantial reduction in power consumption in 3D integrated circuits. For instance, power gating techniques have resulted in energy savings of up to 70%. Second, the semiconductor industry anticipates a steady expansion in the coming years.

- According to industry reports, the market is projected to grow by approximately 15% annually, driven by advancements in areas such as transfer learning applications, electromagnetic simulation, and FPGA acceleration. These developments enable more efficient design, manufacturing, and optimization processes, ultimately leading to higher-performing and cost-effective semiconductor devices.

We can help! Our analysts can customize this AI in semiconductor devices market research report to meet your requirements.

RIA -

RIA -