Aneurysm Coiling And Embolization Devices Market Size 2025-2029

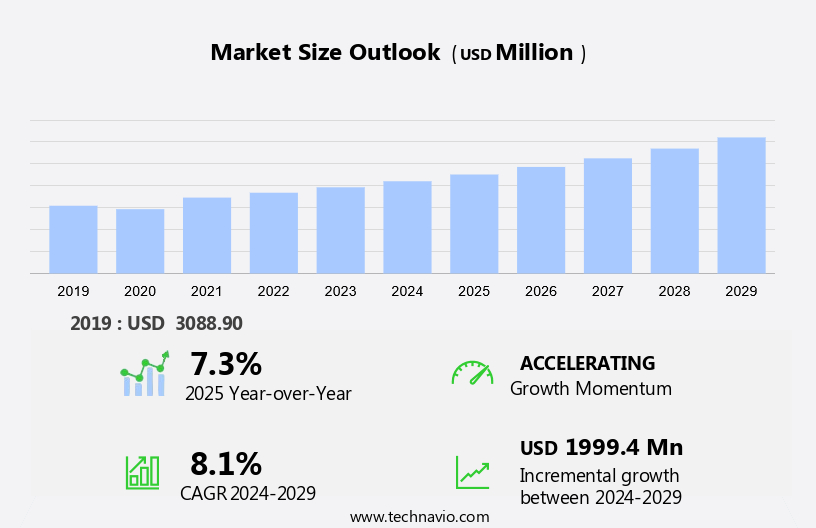

The aneurysm coiling and embolization devices market size is forecast to increase by USD 2 billion at a CAGR of 8.1% between 2024 and 2029.

- The market is witnessing significant growth due to the increasing prevalence of intracranial aneurysms (IAs) and associated risk factors. Neurovascular coiling and embolization techniques have emerged as the preferred treatment options for IAs, driving market growth. Furthermore, the growing demand for flow diversion as an alternative to neurovascular coiling is expected to boost market expansion. However, the high cost of these advanced medical devices remains a major challenge for the market. The report provides a comprehensive analysis of these trends and growth factors, offering valuable insights into the market.

What will be the Size of the Aneurysm Coiling And Embolization Devices Market During the Forecast Period?

- The market encompasses innovative solutions designed to address various neurological conditions, primarily focusing on brain aneurysms and vascular malformations. This market is driven by the increasing prevalence of cerebrovascular diseases, neurological complications, and neurological rehabilitation needs. Neurological assessment, brain imaging, and brain health awareness are significant factors fueling market growth. Minimally invasive procedures, such as endovascular neurosurgery, have gained traction due to their ability to reduce neurological complications and physical disability associated with traditional brain surgery. Neurovascular devices, including aneurysm coiling and embolization systems, play a crucial role in stroke prevention and neurological care. The market is expected to continue expanding as advancements in vascular surgery and brain health technologies contribute to improved neurological outcomes.

How is this Aneurysm Coiling And Embolization Devices Industry segmented and which is the largest segment?

The aneurysm coiling and embolization devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

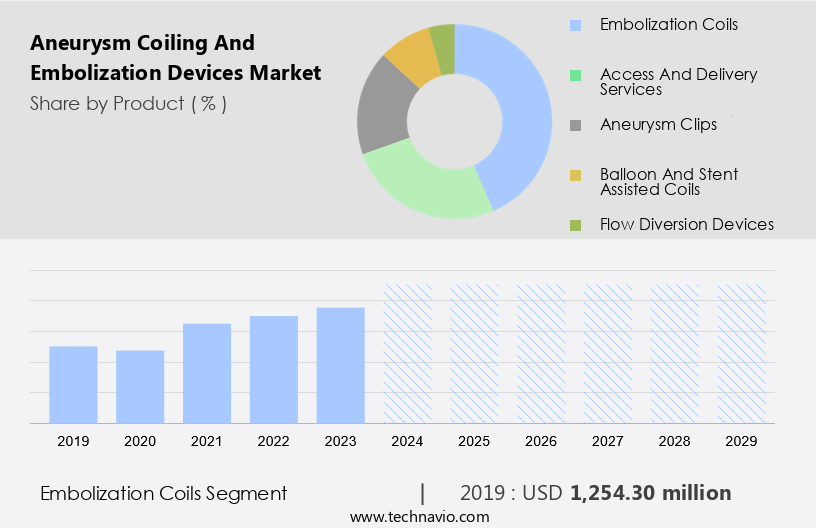

- Product

- Embolization coils

- Access and delivery services

- Aneurysm clips

- Balloon and stent assisted coils

- Flow diversion devices

- Geography

- North America

- Canada

- Mexico

- US

- Europe

- Germany

- UK

- Sweden

- Denmark

- Asia

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Product Insights

- The embolization coils segment is estimated to witness significant growth during the forecast period.

Endovascular coiling, a minimally invasive procedure, is utilized for treating intracranial aneurysms (IAs) and other neurovascular abnormalities, including arteriovenous malformations (AVM) and arteriovenous fistulas. This technique, also known as embolization, involves filling the aneurysm sac with material, thereby reducing the risk of bleeding. Compared to surgical clipping, coiling is less invasive, resulting in shorter hospitalization and recovery times. Consequently, it is often preferred for older patients who may not be suitable for open surgery. Coiling allows controlled filling of the aneurysm sac and is more adaptable to various aneurysm shapes. Early detection and timely treatment of neurovascular illnesses, such as ischemic strokes and vascular diseases, are crucial.

Neurovascular embolization devices, including liquid embolic agents and intrasaccular devices, play a significant role in these therapies. Technological advancements, such as shield technology and AI-driven innovations, have improved the efficiency and safety of these devices. Healthcare infrastructure, alongside neurosurgeons, continues to drive market growth, with emerging revenue pockets in product approvals and commercialization of technological innovations. The value chain is optimized through medical reimbursements, AI analytics, and import/export analysis. Neurovascular conditions, such as stenosis and cerebral aneurysms, necessitate the continued development and refinement of neurovascular devices, with AI aiding in diagnosis and treatment planning.

Get a glance at the market report of share of various segments Request Free Sample

The Embolization coils segment was valued at USD 1.25 billion in 2019 and showed a gradual increase during the forecast period.

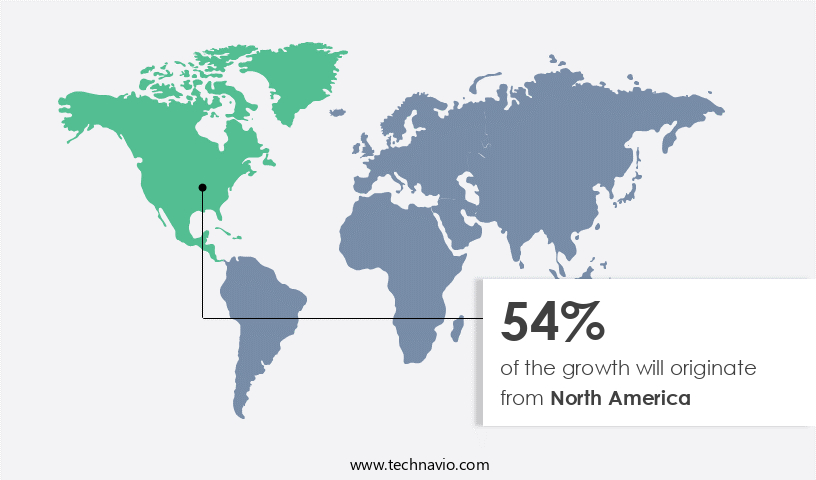

Regional Analysis

- North America is estimated to contribute 54% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market experienced significant growth in 2023, with North America leading as the largest market. The US and Canada were the major contributors to this region's revenue, driven by the increasing number of neuro-endovascular procedures, strong company presence, and healthcare expenditure. The aging population, with one billion people aged 60 and above by 2030, further boosts market growth due to the higher prevalence of intracranial aneurysms (IAs) and related risk factors. Technological advancements, such as liquid embolic agents, intrasaccular devices, and shield technology, have enhanced the efficiency of neurovascular embolization devices. Neurosurgeons increasingly prefer endovascular therapy over traditional clipping methods for treating neurovascular conditions like aneurysms, arteriovenous malformations, ischemic strokes, and vascular diseases.

Product approvals and technological innovations continue to shape the market landscape, with emerging revenue pockets in Asia Pacific and Europe. The value chain is optimized through efficient neurovascular devices and medical reimbursements.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Aneurysm Coiling And Embolization Devices Industry?

Increasing prevalence of IAs and associated risk factors is the key driver of the market.

- The global neurovascular illness market, specifically focusing on aneurysm coiling and embolization devices, is witnessing significant growth due to the rising prevalence of ischemic strokes and arteriovenous malformations (AVMs). Early detection and treatment of these neurovascular conditions are crucial to mitigate the risk of cognitive disability and neurological illnesses. Technological advancements have led to the development of various neurovascular embolization devices, such as intrasaccular devices, embolic coils, and liquid embolic agents. Neurosurgeons increasingly rely on endovascular therapy, including aneurysm clips and shield technology, for efficient neurovascular device implementation. The market dynamics are influenced by product approvals, technological innovations, and medical reimbursements.

- Neurovascular diseases, including intracranial aneurysms, cerebral aneurysms, and vascular diseases, are major drivers of revenue growth. Fistulas and stenosis are other neurovascular conditions that contribute to market expansion. Import export analysis indicates emerging revenue pockets in developing regions. The value chain optimization of neurovascular devices is essential to ensure efficient production analysis and cater to the increasing demand for these devices. The market landscape is characterized by the presence of various neurovascular conditions, necessitating continuous innovation and commercialization of neurovascular devices. Overall, the neurovascular illness market, including aneurysm coiling and embolization devices, is poised for substantial growth.

What are the market trends shaping the Aneurysm Coiling And Embolization Devices Industry?

Growing demand for flow diversion as alternative to neurovascular coiling is the upcoming market trend.

- IAs, or intracranial aneurysms, are a type of neurovascular illness that can lead to ischemic strokes and cognitive disability. Traditional treatments, such as aneurysm clips and surgical clipping procedures, have limitations and risks, including high morbidity and mortality rates. Alternative procedures like SAC and BAC have also shown less-than-desirable efficacy due to recanalization. In response, technological advancements in neurovascular embolization devices have emerged, including flow diversion procedures. These procedures offer several advantages, such as a lower complication rate, higher cure rate, increased safety, reduced risk of re-aneurysm formation, shorter recovery period, and less radiation exposure. Neurosurgeons increasingly prefer these efficient neurovascular devices for the treatment of complex IAs, including giant, wide-necked, and fusiform aneurysms.

- Liquid embolic agents, intraocular devices, and neurovascular embolization devices have undergone significant product approvals and technological innovations. The healthcare infrastructure continues to invest In these neurovascular therapies, creating emerging revenue pockets. The value chain optimization of these devices includes import and export analysis, production analysis, and medical reimbursements. Neurovascular conditions, such as arteriovenous malformations, fistulas, stenosis, and cerebral aneurysms, are increasingly being addressed with these advanced neurovascular devices. As the market for these devices continues to evolve, the focus remains on creating efficient, safe, and effective solutions for neurovascular diseases.

What challenges does the Aneurysm Coiling And Embolization Devices Industry face during its growth?

High cost of treatment is a key challenge affecting the industry growth.

- Aneurysm coiling and embolization devices are essential tools In the treatment of neurovascular illnesses, including ischemic strokes and arteriovenous malformations. Early detection and efficient neurovascular devices, such as embolic coils and intrasaccular devices, play a crucial role in minimizing cognitive disability and preventing complications. Technological advancements, including shield technology and liquid embolic agents, continue to enhance the effectiveness of neurovascular embolization devices. Neurosurgeons utilize these devices In the treatment of various neurovascular conditions, including aneurysms, cerebral aneurysms, and vascular diseases. The high cost of aneurysm coiling and embolization devices remains a significant barrier to their widespread adoption. The average annual cost for a patient with an intracranial aneurysm (IA) treated by clipping is approximately USD 42,000, while the cost for neuroendovascular coiling for a patient with a ruptured IA is nearly USD 45,000.

- Patients also incur additional expenses for related procedures, such as angiograms, complications, and adverse effects. The price range for embolic coils varies depending on their thickness, length, and features, ranging from USD 500 to USD 3,000. The cost of a stent used in stenosis treatment is around USD 5,000 to USD 5,500. Despite the high costs, emerging revenue pockets and product approvals continue to drive the commercialization of neurovascular devices. Technological innovations, such as advanced coil designs and improved delivery systems, offer opportunities for value chain optimization and medical reimbursements. The neurovascular devices market also faces challenges from import and export analysis and the need for efficient neurovascular devices to address conditions like fistulas and stenosis.

- Overall, the market for neurovascular embolization devices is dynamic, with ongoing research and development efforts to address the unmet needs of patients with neurovascular diseases.

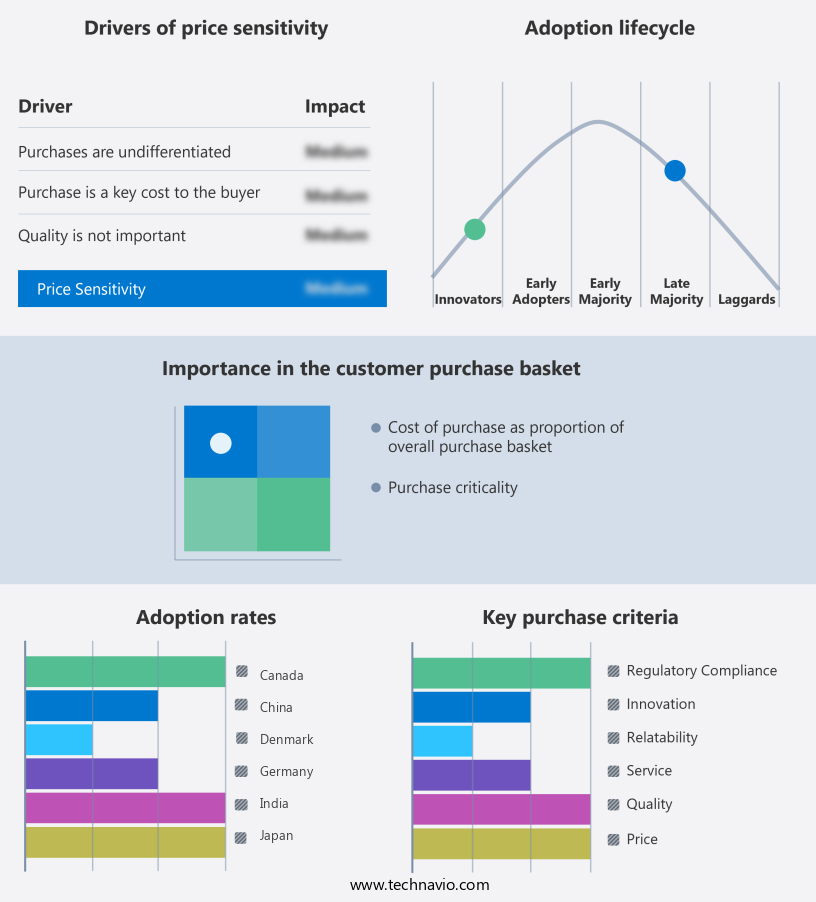

Exclusive Customer Landscape

The aneurysm coiling and embolization devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aneurysm coiling and embolization devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aneurysm coiling and embolization devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acandis GmbH

- Asahi Intecc Co. Ltd.

- B.Braun SE

- BALT Group

- Braile Biomedica

- Cook Group Inc.

- Integer Holdings Corp.

- Johnson and Johnson Inc.

- Kaneka Corp.

- Lepu Medical Technology Beijing Co. Ltd.

- Medtronic Plc

- MicroPort Scientific Corp.

- Penumbra Inc.

- phenox GmbH

- Stryker Corp.

- Terumo Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The neurovascular illness market encompasses a range of conditions that affect the blood vessels In the brain, including aneurysms and arteriovenous malformations (AVMs). Early detection and effective treatment are crucial in mitigating potential complications, such as ischemic strokes and cognitive disability. Neurovascular diseases, including intracranial aneurysms and cerebral aneurysms, are a significant contributor to neurovascular conditions. Aneurysms are weakened areas In the wall of a blood vessel that bulge outward. They can be classified based on their location and size. Neurovascular embolization devices, such as intrasaccular devices and embolic coils, have emerged as effective treatment options for aneurysms.

These devices are designed to block the blood flow to the aneurysm, preventing it from rupturing and causing further damage. Technological advancements have played a pivotal role In the evolution of neurovascular embolization devices. For instance, the introduction of shield technology has enhanced the safety and efficacy of embolization procedures. This technology provides protection against the migration of embolic materials, reducing the risk of complications. The neurovascular embolization devices market is driven by the increasing prevalence of neurovascular diseases and the growing awareness and acceptance of endovascular therapy as a viable treatment option. The market is also influenced by regulatory approvals for new products and technological innovations.

Bare detachable coils and liquid embolic agents are among the commonly used neurovascular embolization devices. The production analysis of these devices reveals that the market is highly competitive, with several players vying for market share. The import and export analysis of these devices also indicates that there is a global demand for efficient neurovascular devices. Neurosurgeons and neurologists are the primary users of neurovascular embolization devices. The healthcare infrastructure and medical reimbursements play a crucial role In the commercialization of these devices. The value chain optimization of neurovascular devices is a key focus area for market participants, as they strive to reduce costs and improve patient outcomes.

Neurovascular conditions, such as ischemic stroke, vascular disease, and fistulas, also contribute to the market growth. The emerging revenue pockets In the market include the development of new technologies and the expansion of the market in developing regions. The neurovascular illness market is a dynamic and evolving landscape, driven by technological advancements, regulatory approvals, and the growing demand for effective treatment options for neurovascular diseases. The market is highly competitive, with several players vying for market share. The focus on value chain optimization and the development of new technologies are key trends shaping the future of the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

184 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2025-2029 |

USD 2 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.3 |

|

Key countries |

US, Denmark, China, Canada, India, Sweden, Germany, Mexico, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aneurysm Coiling And Embolization Devices Market Research and Growth Report?

- CAGR of the Aneurysm Coiling And Embolization Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aneurysm coiling and embolization devices market growth of industry companies

We can help! Our analysts can customize this aneurysm coiling and embolization devices market research report to meet your requirements.

RIA -

RIA -