Application Development And Integration Market Size 2025-2029

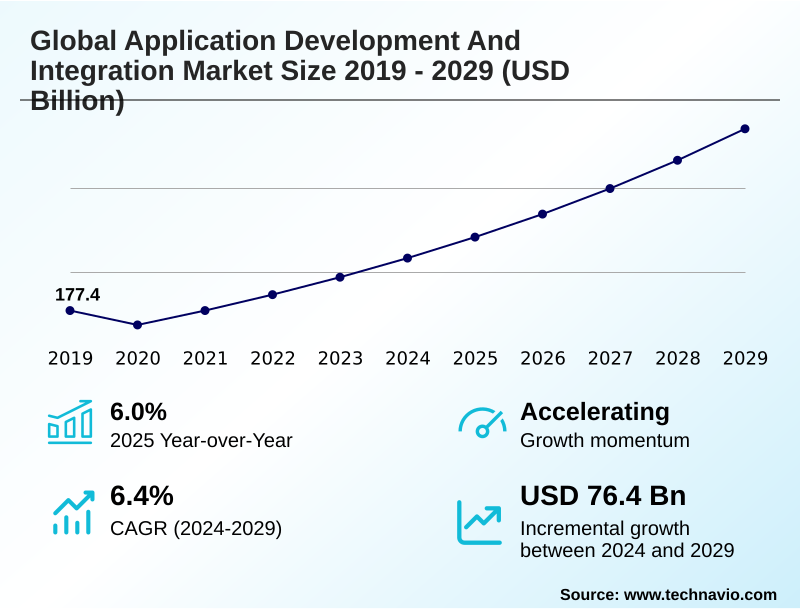

The application development and integration market size is valued to increase by USD 76.4 billion, at a CAGR of 6.4% from 2024 to 2029. Advantage of cost reduction due to operational streamlining will drive the application development and integration market.

Major Market Trends & Insights

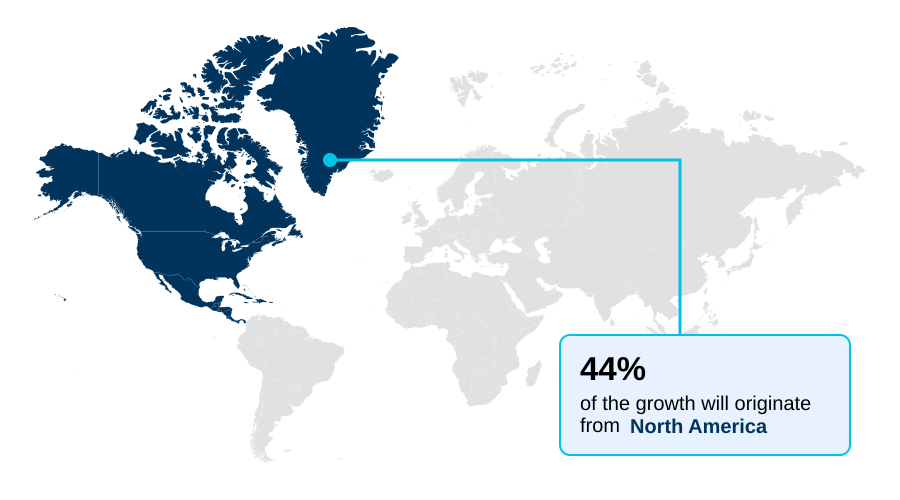

- North America dominated the market and accounted for a 43.6% growth during the forecast period.

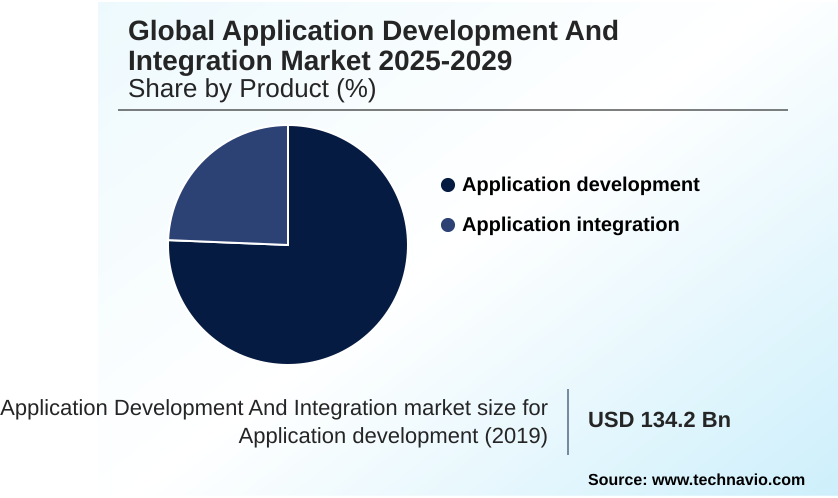

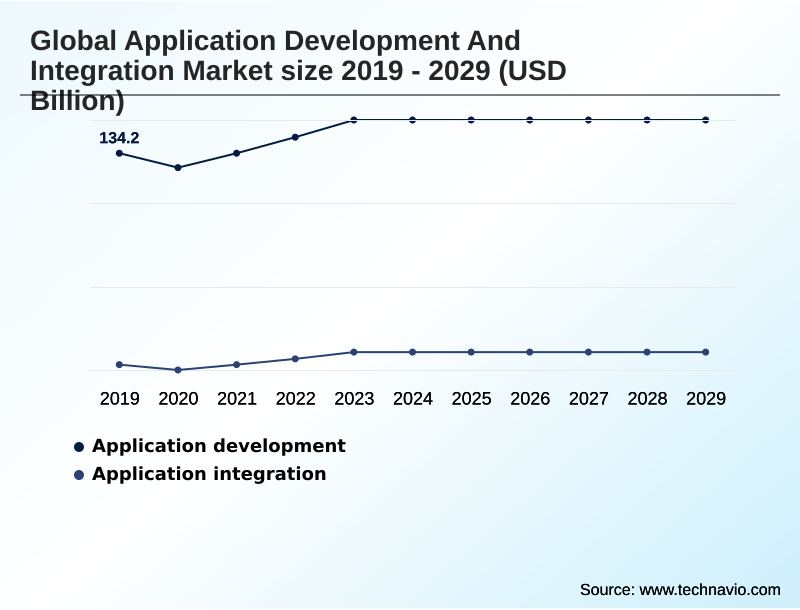

- By Product - Application development segment was valued at USD 148.5 billion in 2023

- By Deployment - On-premises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 107.4 billion

- Market Future Opportunities: USD 76.4 billion

- CAGR from 2024 to 2029 : 6.4%

Market Summary

- The application development and integration market is pivotal to modern digital transformation, enabling enterprises to innovate and streamline operations. Driven by the need for greater agility, organizations are undergoing agile transformation, moving away from monolithic systems toward cloud-native architecture and microservices. This shift necessitates sophisticated system integration strategies, particularly for companies managing a mix of new and legacy systems.

- A key trend is the adoption of iPaaS and low-code platforms, which democratize development and accelerate business process automation. In a typical business scenario, a manufacturing firm might implement a hybrid integration solution to connect its on-premises enterprise resource planning system with a cloud-based customer relationship management platform.

- This real-time data integration allows for a unified view of the supply chain and customer orders, enhancing decision-making. However, the market faces challenges related to data security and interoperability, demanding a strong focus on DevSecOps and secure application development.

- The rise of API-led connectivity and service mesh technologies helps manage these complex, distributed environments, ensuring that both custom-built and SaaS applications can communicate seamlessly and securely.

What will be the Size of the Application Development And Integration Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Application Development And Integration Market Segmented?

The application development and integration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Application development

- Application integration

- Deployment

- On-premises

- Cloud

- Type

- Web applications

- Mobile applications

- Desktop applications

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Product Insights

The application development segment is estimated to witness significant growth during the forecast period.

The application development segment is driven by ongoing business transformation, as enterprises digitalize processes to achieve operational efficiency. Organizations are pursuing agile transformation and adopting agile and devops methodologies to accelerate application lifecycle management.

There is a constant demand for custom application development tailored to specific business needs, resulting in a focus on effective application portfolio management. The process involves utilizing a robust software development kit and ensuring strong DevOps support for continuous delivery.

This segment also sees growing investment in application modernization and advanced capabilities like predictive analytics, with successful system integration projects improving deployment frequency by over 40% and reducing post-launch defects.

This strategic focus ensures that application landscapes evolve to meet dynamic business demands.

The Application development segment was valued at USD 148.5 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Application Development And Integration Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is led by North America, which is a hub for technological innovation in cloud computing and AI. Enterprises in this region are rapidly adopting digital transformation strategies, driving demand for modern application development and integration tools.

This includes the implementation of microservices, scalable backend services, and advanced API management platforms. Stringent data protection regulations in both North America and Europe are fueling a 20% rise in demand for solutions with robust, built-in security features.

In APAC, the proliferation of mobile devices and SMEs is accelerating the adoption of cost-effective integration platform as a service (iPaaS) solutions.

These platforms are essential for connecting disparate systems, including customer relationship management (CRM) software, to create a unified operational view.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in today's digital economy requires a deep understanding of the cost of migrating legacy systems to cloud and the benefits of hybrid application integration technology. Enterprises face significant challenges in enterprise saas application integration, making it crucial to know how to implement a secure devsecops pipeline for risk mitigation.

- Following best practices for api management and governance is no longer optional. A key decision point is choosing between low-code and custom development, a choice that profoundly shapes resource allocation and time-to-market. The impact of ai on application development is accelerating this, with a focus on improving developer productivity with ai tools.

- The necessity of real-time data synchronization across hybrid cloud is driving the adoption of platforms for automating workflows with ipaas solutions. Furthermore, the ubiquity of mobile requires seamless mobile application integration with backend services. Security remains a top concern, centered on securely connecting on-premises and cloud applications.

- For established companies, developing strategies for modernizing monolithic applications is essential for survival, often involving the role of service mesh in microservices. Technical teams frequently perform a cross-platform development frameworks comparison to balance performance and cost. Ultimately, solving enterprise resource planning system integration challenges and customer relationship management data integration methods is fundamental to achieving operational efficiency through process automation.

- In fact, firms that successfully integrate these core systems report operational efficiencies more than 35% higher than their less-integrated peers. This focus extends to integrating iot data with enterprise systems and effectively managing application portfolios for cost optimization.

What are the key market drivers leading to the rise in the adoption of Application Development And Integration Industry?

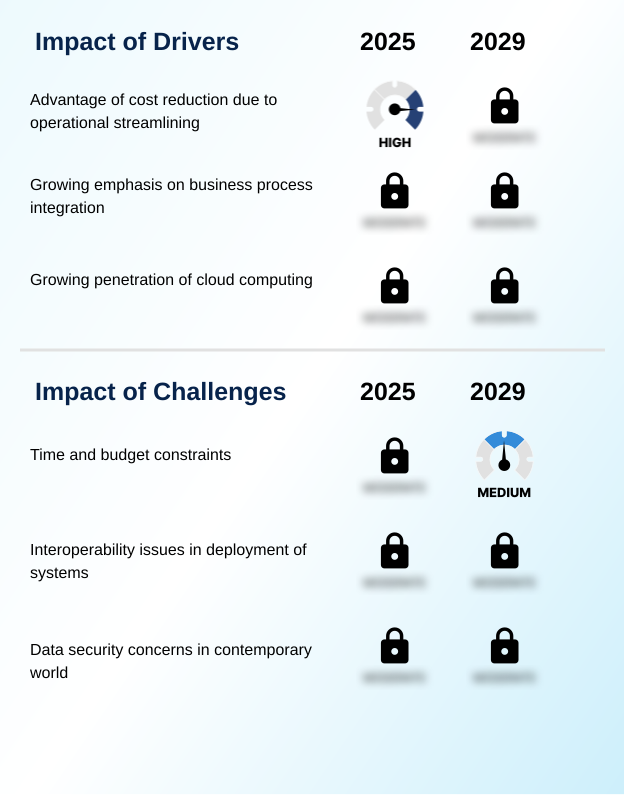

- A primary market driver is the significant cost reduction advantage achieved through operational streamlining enabled by cohesive application development and integration strategies.

- The growing emphasis on efficient business process integration is a significant market driver. Enterprises are investing in IT infrastructure modernization and cloud application development to streamline operations and reduce costs, with some achieving a 20% reduction in operational expenditures.

- The adoption of a cloud-native architecture enables greater flexibility and scalability. This shift necessitates on-premises to cloud migration and legacy migration projects, which rely on robust tools for real-time data integration and data synchronization.

- Automating key functions through business process automation and integrating complex systems like enterprise resource planning (ERP) are critical. These drivers underscore the market's role in helping organizations achieve operational coherence and make informed, data-driven decisions.

What are the market trends shaping the Application Development And Integration Industry?

- The increasing worldwide penetration of integration Platform as a Service (iPaaS) is an emerging market trend, driven by the need for scalable and flexible solutions to handle complex integration scenarios.

- A key trend is the worldwide penetration of platform-as-a-service (PaaS) and iPaaS, which are essential for managing complex enterprise ecosystems. The rise of hybrid integration technology is critical for organizations that use both on-premises and cloud models, where API-led connectivity ensures seamless data flow, improving integration speed by up to 30%.

- Serverless architectures and low-code platforms are democratizing development, allowing for faster creation of applications. We also see wider adoption of service mesh technologies to manage microservices communication. For the modern workforce, mobile application integration within a virtualized workspace is paramount, with some organizations reporting a 25% increase in productivity.

- This trend is supported by workflow automation tools and cross-platform development frameworks that deliver consistent user experiences across devices.

What challenges does the Application Development And Integration Industry face during its growth?

- Significant time and budget constraints for the deployment and long-term maintenance of application development and integration systems pose a considerable challenge to market growth.

- A primary challenge involves the time and budget constraints associated with large-scale digital transformation initiatives. Interoperability issues in deploying enterprise application integration systems can lead to a 15% increase in long-term maintenance costs. Furthermore, data security concerns are paramount in an era of SaaS integration challenges, demanding a focus on secure application development and robust DevSecOps practices.

- Implementing and maintaining CI/CD pipelines require significant investment and skilled personnel. The complexity of data transformation across disparate systems and the need for comprehensive automated testing add to the resource burden. As organizations adopt technologies like containerization to streamline deployments, managing the security of these environments and ensuring effective B2B integration solutions remains a persistent challenge for many.

Exclusive Technavio Analysis on Customer Landscape

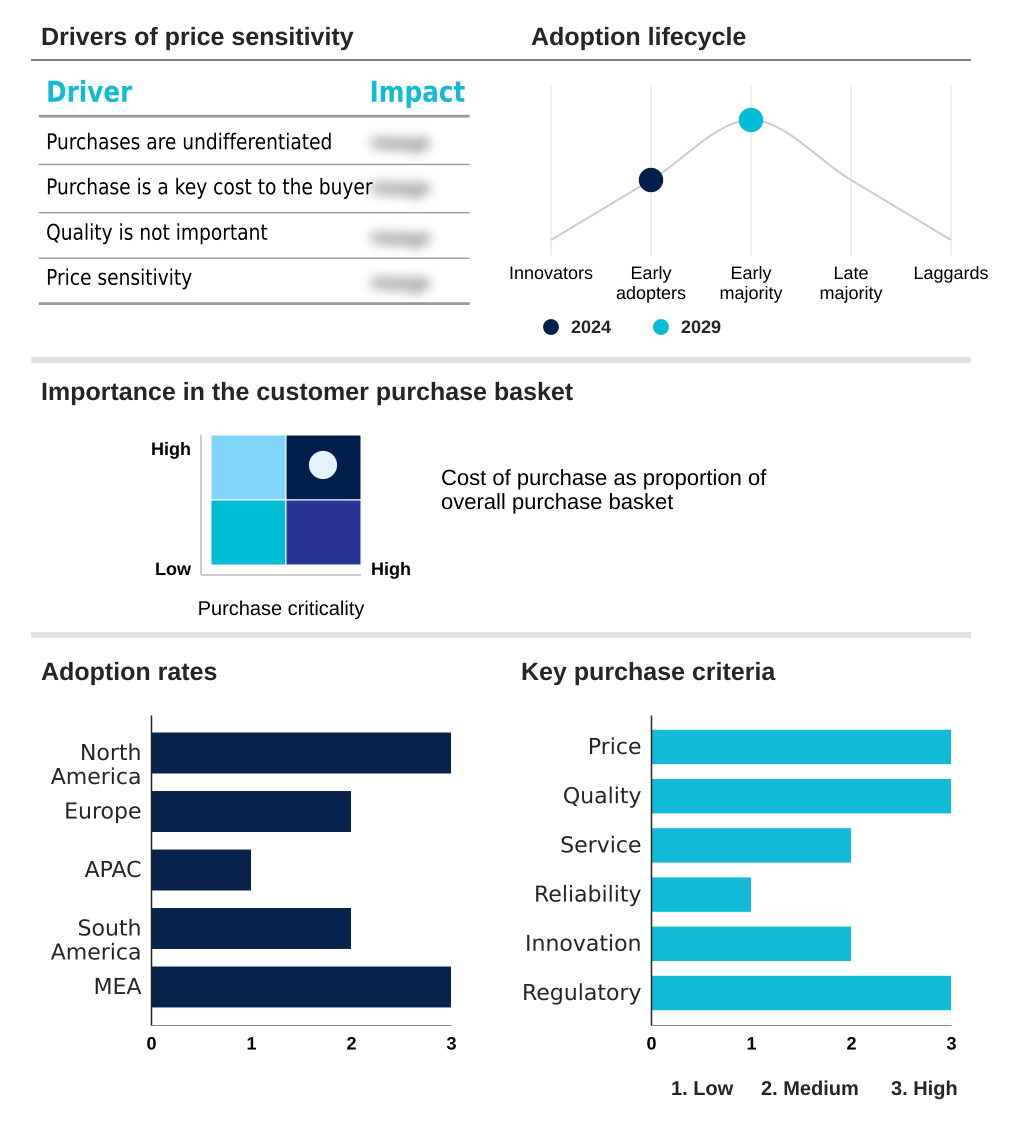

The application development and integration market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the application development and integration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Application Development And Integration Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, application development and integration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - Solutions focus on agile transformation and modernizing application landscapes, enabling organizations to innovate with greater speed and realize enhanced business value.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Atos SE

- Capgemini Service SAS

- Cognizant Technology Solution

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard

- Infosys Ltd.

- IBM Corp.

- Larsen and Toubro Ltd.

- Mahindra and Mahindra Ltd.

- Microsoft Corp.

- Mindteck India Ltd.

- NTT DATA Corp.

- Oracle Corp.

- RSM International Ltd.

- SAP SE

- Tata Consultancy Services

- Unisys Corp.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Application development and integration market

- In November, 2024, Red Hat Inc. announced new capabilities for its Developer Hub, integrating AI to help organizations accelerate the delivery of smarter applications and services.

- In August, 2024, the Tauri framework released its 2.0 beta, a Rust-based tool promising significant performance gains and introducing alpha support for mobile platforms, challenging existing cross-platform solutions.

- In January, 2025, Tata Consultancy Services launched an enhanced service offering focused on migrating complex on-premise application integration platforms to Azure iPaaS for large enterprises.

- In March, 2025, Oracle Corp. expanded its AI-powered low-code toolset, adding new features to its autonomous databases and cloud-native platforms designed to improve developer productivity.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Application Development And Integration Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.4% |

| Market growth 2025-2029 | USD 76.4 billion |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Russia, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, South Africa, UAE, Saudi Arabia, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The application development and integration market is defined by the enterprise-wide push for agile transformation and application modernization. Boardroom decisions increasingly center on the strategic value of a cohesive cloud-native architecture, which is essential for supporting business process automation and deriving insights from predictive analytics.

- The adoption of microservices is not just a technical shift but a core business strategy to enhance agility. This requires robust API management and system integration capabilities, often managed with service mesh technologies. Key processes like legacy migration are complex undertakings that benefit from DevSecOps principles and extensive automated testing within CI/CD pipelines to ensure quality.

- Organizations leveraging this approach report a 40% reduction in critical post-deployment issues. The ecosystem relies on containerization, efficient data transformation, and continuous DevOps support to connect core systems like enterprise resource planning and customer relationship management while enabling advanced functionalities in a virtualized workspace through seamless data synchronization. The use of low-code platforms and iPaaS further accelerates these initiatives.

What are the Key Data Covered in this Application Development And Integration Market Research and Growth Report?

-

What is the expected growth of the Application Development And Integration Market between 2025 and 2029?

-

USD 76.4 billion, at a CAGR of 6.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Application development, and Application integration), Deployment (On-premises, and Cloud), Type (Web applications, Mobile applications, and Desktop applications) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Advantage of cost reduction due to operational streamlining, Time and budget constraints

-

-

Who are the major players in the Application Development And Integration Market?

-

Accenture PLC, Atos SE, Capgemini Service SAS, Cognizant Technology Solution, Fujitsu Ltd., HCL Technologies Ltd., Hewlett Packard, Infosys Ltd., IBM Corp., Larsen and Toubro Ltd., Mahindra and Mahindra Ltd., Microsoft Corp., Mindteck India Ltd., NTT DATA Corp., Oracle Corp., RSM International Ltd., SAP SE, Tata Consultancy Services, Unisys Corp. and Wipro Ltd.

-

Market Research Insights

- The market is shaped by significant digital transformation initiatives that compel organizations to pursue IT infrastructure modernization and custom application development. Effective application portfolio management is critical, with firms leveraging API-led connectivity and workflow automation tools to streamline business process integration.

- The move toward cloud application development addresses SaaS integration challenges and facilitates on-premises to cloud migration, with successful projects reducing infrastructure costs by up to 30%. Real-time data integration is supported by platform-as-a-service (PaaS) and integration platform as a service, while cross-platform development via a modern software development kit ensures broad reach.

- Agile and devops methodologies, combined with a focus on secure application development, underpin the entire application lifecycle management process. This environment also drives demand for mobile application integration, scalable backend services, and sophisticated B2B integration solutions managed through a robust application programming interface.

We can help! Our analysts can customize this application development and integration market research report to meet your requirements.

RIA -

RIA -