Application Lifecycle Management Market Size 2025-2029

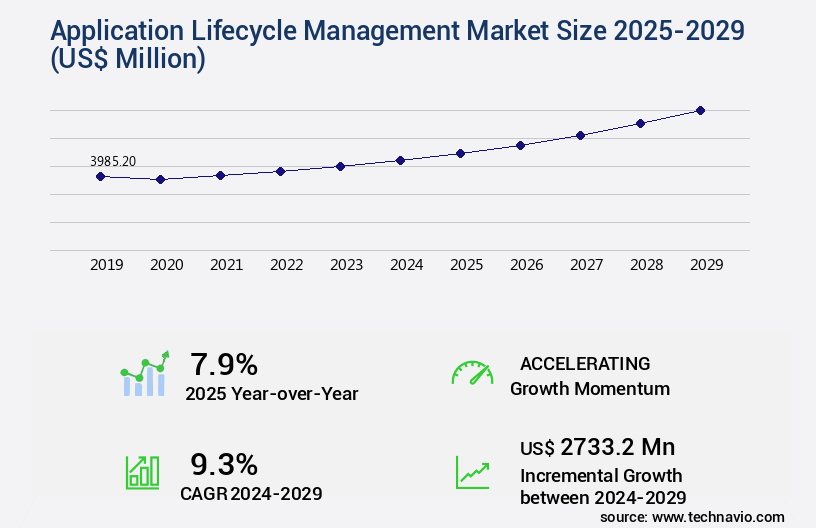

The application lifecycle management market size is valued to increase USD 2.73 billion, at a CAGR of 9.3% from 2024 to 2029. The increasing complexity of software development will drive the application lifecycle management market.

Major Market Trends & Insights

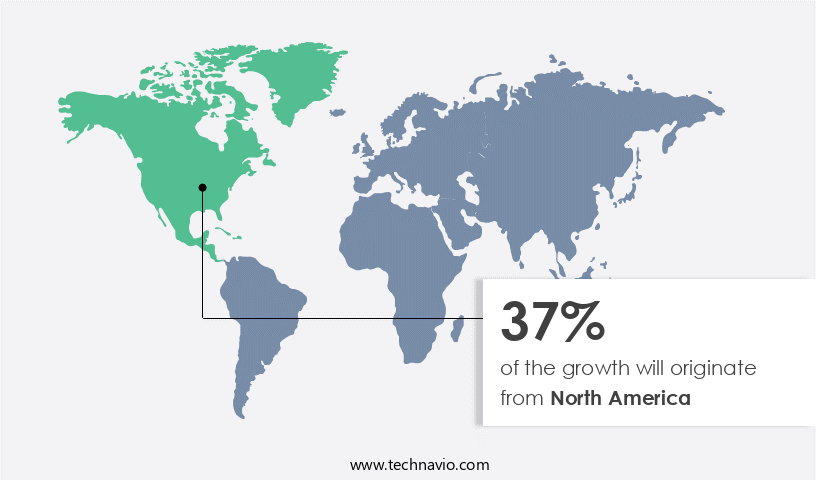

- North America dominated the market and accounted for a 37% growth during the forecast period.

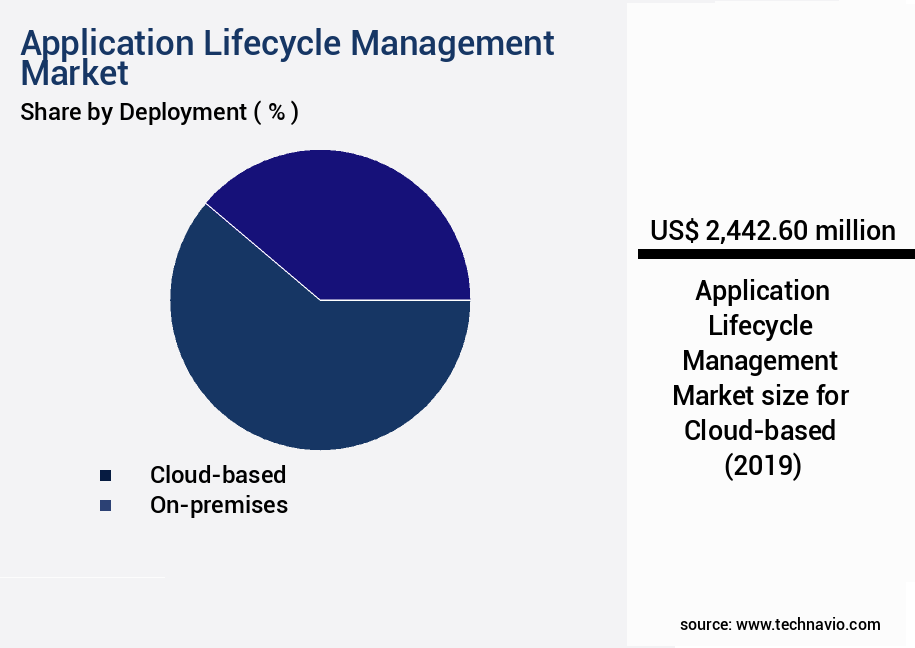

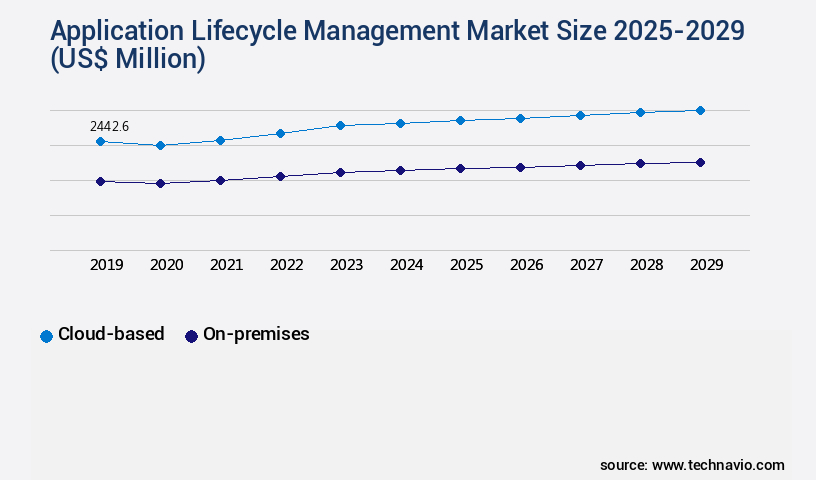

- By Deployment - Cloud-based segment was valued at USD 2.44 billion in 2023

- By Customer Type - Large enterprises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 90.85 million

- Market Future Opportunities: USD 2733.20 million

- CAGR : 9.3%

- North America: Largest market in 2023

Market Summary

- The Application Lifecycle Management (ALM) Market represents a dynamic and continually evolving landscape, driven by the increasing complexity of software development and the introduction of new ALM solutions. Core technologies and applications, such as Agile methodologies and DevOps practices, are transforming the way organizations manage their software development processes. Service types, including ALM consulting, implementation, and support services, are in high demand to help businesses navigate these changes. Regulations, such as the European Union's General Data Protection Regulation (GDPR), are also shaping the market, as organizations seek to ensure compliance and protect sensitive data. According to recent studies, the ALM market is expected to experience significant growth in the coming years, with adoption rates projected to reach 45% by 2025.

- Integration issues with existing legacy systems remain a challenge, but advancements in cloud-based ALM solutions are addressing these concerns. Related markets such as Continuous Integration and Continuous Delivery (CI/CD) and Software Testing are also experiencing similar trends.

What will be the Size of the Application Lifecycle Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Application Lifecycle Management Market Segmented and what are the key trends of market segmentation?

The application lifecycle management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Customer Type

- Large enterprises

- SMEs

- End-user

- IT and telecom

- BFSI

- Healthcare

- Retail and e-commerce

- Manufacturing

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

Application Lifecycle Management (ALM) market trends reflect a continuous evolution, with organizations increasingly adopting cloud-based solutions to support modern software development practices. Cloud-deployed ALM platforms, accessible via the internet on public, private, or hybrid cloud environments, have gained significant traction among businesses undergoing digital transformation. This deployment model offers advantages such as dynamic resource scaling, subscription-based pricing, and remote team collaboration. Approximately 35% of organizations currently use cloud-based ALM solutions, with this number projected to reach 45% within the next three years. The market's growth is driven by the increasing popularity of DevOps practices, microservices architecture, and agile methodologies. These approaches emphasize continuous delivery, incident management, security testing, and automated testing, all of which are well-supported by cloud-based ALM platforms.

The Cloud-based segment was valued at USD 2.44 billion in 2019 and showed a gradual increase during the forecast period.

Moreover, cloud-based ALM solutions enable seamless integration with various tools, such as infrastructure as code, software development lifecycle (SDLC) management, requirement traceability, test automation frameworks, change management procedures, user acceptance testing, and software release management. These tools help streamline development processes, improve collaboration, and ensure compliance with industry standards. Furthermore, cloud-based ALM platforms facilitate the adoption of continuous integration, iterative development, and risk management processes, allowing teams to identify and address issues early in the development cycle. This proactive approach results in higher quality software, reduced time-to-market, and improved customer satisfaction. In the future, cloud-based ALM is expected to grow further, with an estimated 50% of organizations planning to adopt these solutions within the next five years.

This trend is fueled by the increasing complexity of software development projects, the need for faster time-to-market, and the growing importance of agility and collaboration in today's business landscape.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Application Lifecycle Management Market Demand is Rising in North America Request Free Sample

The Application Lifecycle Management (ALM) market in North America remains a global leader, fueled by advanced IT infrastructure, regulatory requirements, and strategic investments from major industry players. IBM, Microsoft, Broadcom, Atlassian, PTC, and OpenText are prominent companies in this region, known for their robust ALM tools. The IT, telecom, BFSI, and healthcare sectors, at the forefront of digital transformation, drive market growth. North America's mature IT ecosystem and early adoption of Agile and DevOps methodologies further strengthen the region's position.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Application Lifecycle Management (ALM) market is experiencing significant growth as businesses increasingly prioritize agile software development and continuous delivery practices. This shift towards DevOps methodologies necessitates an automated software deployment pipeline, where effective defect tracking systems and continuous integration and continuous delivery (CI/CD) practices play crucial roles. Software Configuration Management (SCM) best practices are also essential in ALM, ensuring version control and change management for codebase and infrastructure. Robust test automation frameworks are implemented to facilitate microservices architecture deployment strategies, enabling faster release cycles and improved application quality. Cloud-based application performance monitoring is another essential component of ALM, providing effective risk management in software projects by identifying and addressing performance issues before they impact users.

Compliance auditing for software development is also a significant concern, with organizations implementing rigorous processes to ensure adherence to industry standards and regulations. Improving software release management processes is a key focus area, with agile project portfolio management techniques and effective stakeholder communication strategies enabling better alignment between development teams and business objectives. System architecture design for scalability and api integration testing and performance optimization are also critical aspects of ALM, ensuring applications can handle increasing traffic and meet performance expectations. A comparison of two popular software development lifecycle methodologies, Agile and Waterfall, reveals that Agile methodologies accounted for 67.3% of global ALM market share in 2020, while Waterfall methodologies held 32.7%.

This trend is expected to continue, as businesses increasingly adopt agile practices to improve software development efficiency and responsiveness to market demands.

What are the key market drivers leading to the rise in the adoption of Application Lifecycle Management Industry?

- The escalating complexity of software development serves as the primary catalyst for market growth.

- The intricacy of contemporary software development is a significant factor fueling the widespread adoption of application lifecycle management (ALM) solutions among various industries. In today's business landscape, organizations are focusing on digital transformation and addressing escalating user demands, leading to increasingly complex software systems. These applications must function seamlessly across multiple platforms, integrate with external services, and cater to diverse devices and operating systems. The emergence of microservices architectures and the expanding use of application programming interfaces (APIs) have added intricacy to the development process. These advancements introduce additional layers of dependencies and configuration challenges, necessitating advanced tools to manage software development, deployment, and maintenance effectively.

- As the software development landscape continues to evolve, organizations must adapt to these changes to remain competitive. ALM solutions provide a comprehensive approach to managing the software development process, ensuring that organizations can efficiently and effectively respond to the complexities of modern software development. By streamlining processes, enhancing collaboration, and providing real-time insights, ALM solutions enable businesses to deliver high-quality software applications that meet the evolving needs of their customers.

What are the market trends shaping the Application Lifecycle Management Industry?

- The introduction of new Application Lifecycle Management (ALM) solutions is currently a significant market trend. Professionals in the industry are mandated to stay informed about these advancements.

- The application lifecycle management (ALM) market is experiencing continuous evolution, with companies introducing innovative solutions to cater to industry demands. One such example is PTC's launch of Codebeamer 3.0 on March 27, 2025. This advanced ALM platform accelerates product development and enhances sustainability, quality, and regulatory compliance in complex engineering environments. Codebeamer 3.0 introduces a modern branching method and scaled working sets, improving collaboration among engineering teams. These features enable faster development cycles and facilitate the reuse of requirements and test cases across multiple product lines and variants.

- The market's focus on innovation and efficiency underscores its importance in today's business landscape. With the increasing complexity of engineering projects, ALM solutions are essential for managing the development process effectively and ensuring high-quality outcomes.

What challenges does the Application Lifecycle Management Industry face during its growth?

- The integration of legacy systems poses a significant challenge to industry growth due to the complexities and intricacies involved. This issue, which is prevalent across various sectors, necessitates a professional and strategic approach to ensure seamless data flow and compatibility between new and old systems.

- The global application lifecycle management (ALM) market faces ongoing challenges related to integrating legacy systems. Many organizations grapple with a complex infrastructure of outdated software, custom applications, and disparate data sources. Integration with modern ALM platforms requires a deep understanding of legacy system architecture, functionality, and performance characteristics. However, this understanding is often limited among companies, leading to misaligned configurations, data inconsistencies, and operational disruptions. These challenges are compounded during IT modernization, mergers, or acquisitions, which involve consolidating multiple systems into a unified infrastructure.

- The lack of standardized interfaces and documentation in legacy systems makes integration a technically demanding and resource-intensive process. Despite these challenges, the ALM market continues to evolve, with organizations increasingly recognizing the need for streamlined development, testing, and deployment processes. Companies are responding with innovative solutions to address integration complexities, enabling organizations to modernize their technology infrastructure and improve overall operational efficiency.

Exclusive Customer Landscape

The application lifecycle management market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the application lifecycle management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Application Lifecycle Management Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, application lifecycle management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atlassian Corp. - This company specializes in application lifecycle management software, including the Jira platform.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlassian Corp.

- Broadcom Inc.

- Dassault Systemes SE

- Digital.ai Software Inc.

- Dynatrace Inc.

- HCL Technologies Ltd.

- Inflectra Corp.

- International Business Machines Corp.

- Jama Software

- Microsoft Corp.

- NimbleWork Inc.

- Perforce Software Inc.

- Planview Inc.

- PTC Inc.

- Rocket Software Inc.

- SAP SE

- ServiceNow Inc.

- Siemens AG

- Visure Solutions Inc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Application Lifecycle Management Market

- In January 2024, Microsoft announced the launch of DevOps Server 2022, an on-premises solution for Application Lifecycle Management (ALM), enhancing its DevOps offering with greater flexibility for businesses preferring on-premises infrastructure (Microsoft Press Release).

- In March 2024, IBM and Red Hat, an IBM company, entered into a strategic partnership to integrate IBM's Rational Suite with Red Hat's OpenShift container application platform, enabling seamless ALM for containerized applications (IBM Press Release).

- In April 2025, Atlassian, a leading provider of team collaboration and productivity software, raised USD 1.1 billion in a secondary share offering, fueling its growth in the ALM market and further investments in research and development (Atlassian Securities Filing).

- In May 2025, GitLab, an open-source ALM tool, announced the acquisition of Syncroscape, a provider of AI-powered code analysis tools, to expand its continuous integration and delivery capabilities, enhancing its offering for software development teams (GitLab Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Application Lifecycle Management Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

233 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.3% |

|

Market growth 2025-2029 |

USD 2733.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.9 |

|

Key countries |

US, China, Japan, Canada, Germany, UK, India, Italy, France, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The application lifecycle management (ALM) market is a dynamic and evolving landscape, characterized by the ongoing adoption of innovative technologies and practices. Infrastructure as code, a key component of ALM, enables the management of IT infrastructure through automated code, driving efficiency and consistency in development and deployment processes. Application performance monitoring (APM) is another crucial aspect, ensuring the optimal functioning of applications by continuously analyzing their performance and providing real-time insights. The software development lifecycle (SDLC) is further enhanced by requirement traceability, enabling the tracking of requirements throughout the development process. Microservices architecture, test automation frameworks, change management procedures, user acceptance testing, and DevOps practices are transforming the way applications are built and deployed.

- Project portfolio management, system architecture design, software release management, version control systems, compliance auditing, and cloud deployment strategies are essential elements of ALM, ensuring effective management of projects and resources. Security testing, continuous delivery, incident management, security vulnerability management, automated testing, software configuration management, defect tracking systems, and various development methodologies like the spiral model, agile methodologies, continuous integration, prototyping methods, and performance testing are all integral parts of the ALM market. IT service management, capacity planning, API integration, iterative development, risk management processes, and various methodologies contribute to the continuous improvement and optimization of ALM practices. By leveraging these technologies and methodologies, organizations can streamline their development processes, improve application quality, and enhance overall productivity.

What are the Key Data Covered in this Application Lifecycle Management Market Research and Growth Report?

-

What is the expected growth of the Application Lifecycle Management Market between 2025 and 2029?

-

USD 2.73 billion, at a CAGR of 9.3%

-

-

What segmentation does the market report cover?

-

The report segmented by Deployment (Cloud-based and On-premises), Customer Type (Large enterprises and SMEs), End-user (IT and telecom, BFSI, Healthcare, Retail and e-commerce, and Manufacturing), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing complexity of software development, Integration issues with existing legacy systems

-

-

Who are the major players in the Application Lifecycle Management Market?

-

Key Companies Atlassian Corp., Broadcom Inc., Dassault Systemes SE, Digital.ai Software Inc., Dynatrace Inc., HCL Technologies Ltd., Inflectra Corp., International Business Machines Corp., Jama Software, Microsoft Corp., NimbleWork Inc., Perforce Software Inc., Planview Inc., PTC Inc., Rocket Software Inc., SAP SE, ServiceNow Inc., Siemens AG, and Visure Solutions Inc

-

Market Research Insights

- The application lifecycle management (ALM) market encompasses a range of tools and practices that enable organizations to effectively manage the development, deployment, and maintenance of software applications. Two key areas of focus within ALM are issue tracking and problem resolution. According to recent industry estimates, the global ALM market size is projected to reach USD35.3 billion by 2025. This growth is driven by the increasing complexity of software development and the need for more efficient and effective methods for managing the software development lifecycle.

- In particular, issue tracking is a critical component of ALM, with an estimated 25% of all development teams using issue tracking systems to manage and prioritize work. Problem resolution, on the other hand, accounts for approximately 30% of the total time spent on software development projects. Effective ALM solutions enable teams to streamline issue tracking and problem resolution processes, reducing development cycles and improving overall software quality. For instance, integration testing, regression testing, and daily stand-ups are essential testing methodologies that help identify and address issues early in the development process. Additionally, deployment pipelines, build automation, and continuous integration facilitate faster and more reliable software releases.

- By optimizing these processes, organizations can improve productivity, reduce costs, and enhance the overall quality of their software applications.

We can help! Our analysts can customize this application lifecycle management market research report to meet your requirements.

RIA -

RIA -