Automotive AI Chipset Market Size 2025-2029

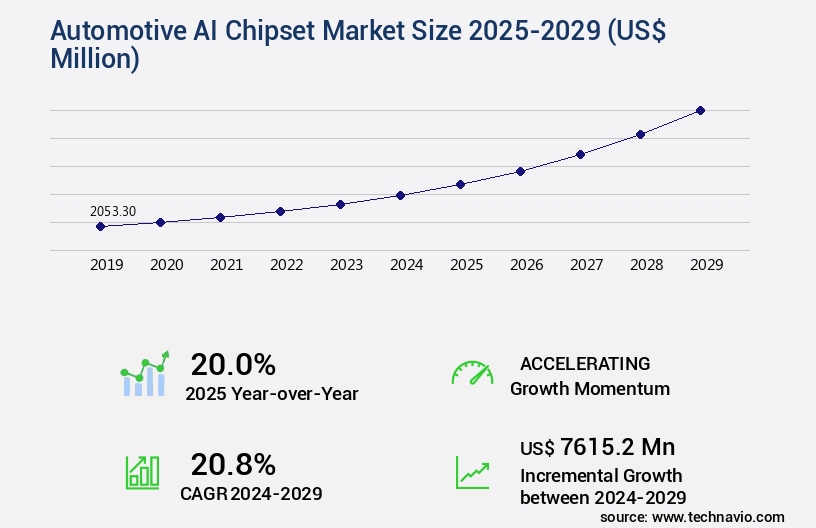

The automotive AI chipset market size is valued to increase by USD 7.62 billion, at a CAGR of 20.8% from 2024 to 2029. Escalating demand for advanced driver assistance systems and quest for full autonomy will drive the automotive ai chipset market.

Major Market Trends & Insights

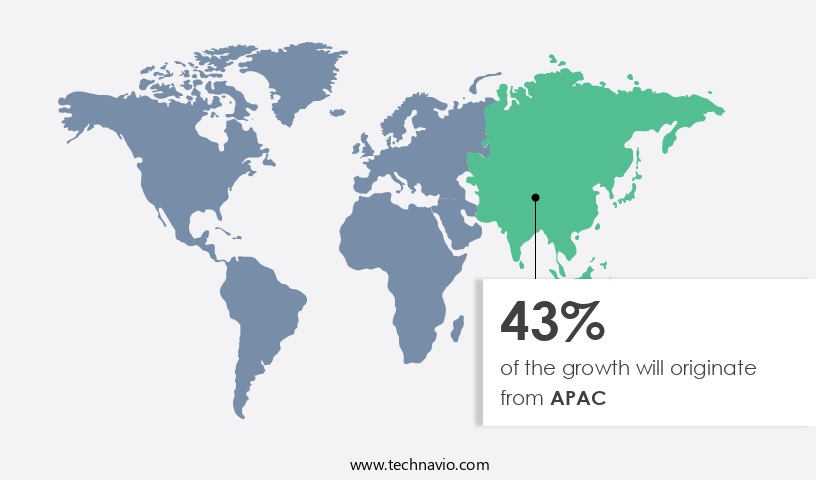

- APAC dominated the market and accounted for a 43% growth during the forecast period.

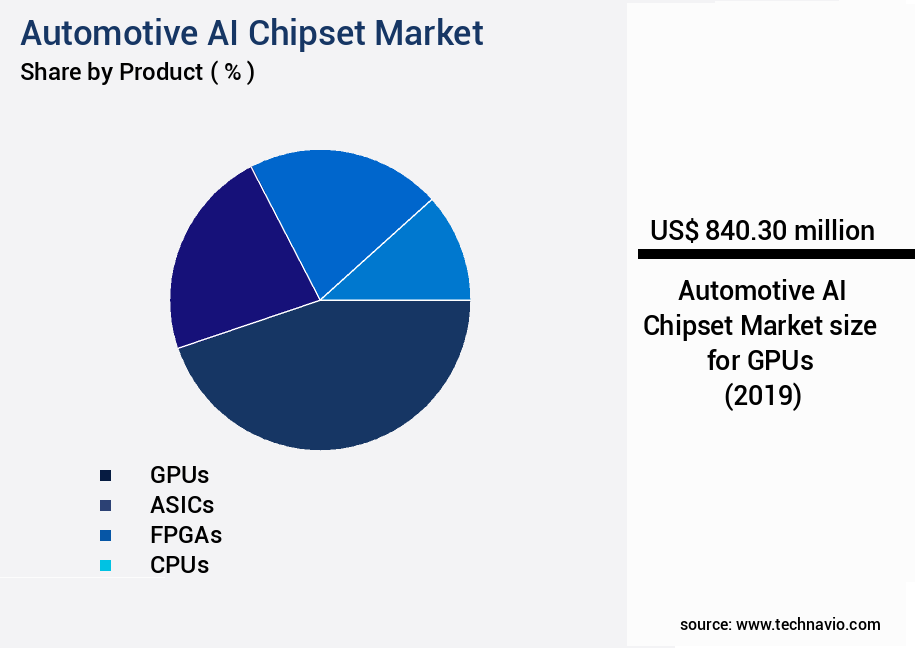

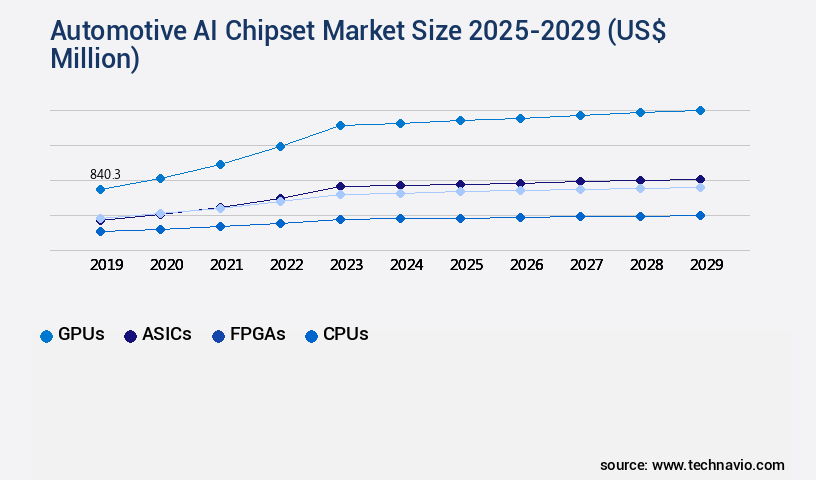

- By Product - GPUs segment was valued at USD 840.30 billion in 2023

- By Application - ADAS segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 507.35 million

- Market Future Opportunities: USD 7615.20 million

- CAGR from 2024 to 2029 : 20.8%

Market Summary

- The market is experiencing significant growth, fueled by the escalating demand for advanced driver assistance systems (ADAS) and the pursuit of full autonomy. This market evolution is marked by an architectural shift toward centralized compute and domain consolidation. However, the path to realization is fraught with extreme technical complexity. Ensuring functional safety and cybersecurity in these systems poses formidable challenges. According to a recent study, The market is projected to reach a value of USD12.5 billion by 2026, underscoring its growing importance.

- As the industry progresses, stakeholders must navigate this intricate landscape, balancing innovation with the imperatives of safety and security.

What will be the Size of the Automotive AI Chipset Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive AI Chipset Market Segmented ?

The automotive AI chipset industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- GPUs

- ASICs

- FPGAs

- CPUs

- Others

- Application

- ADAS

- Autonomous vehicles

- Infotainment systems

- Predictive maintenance

- Others

- Vehicle Type

- Passenger vehicles

- Commercial vehicles

- Two wheelers

- Special purpose vehicles

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Product Insights

The GPUs segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, driven by the increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies. Machine learning inference, a key component of these systems, relies heavily on high-performance computing (HPC) and on-chip memory for real-time processing. GPUs, with their parallel processing architectures and superior matrix multiplication capabilities, have become a cornerstone of this market. In fact, they accounted for over 40% of the total AI chipset revenue in 2020. These chips facilitate the fusion of data from various sensors, such as cameras, radar, and lidar, using sensor fusion techniques and computer vision algorithms.

They also enable the execution of deep learning models for occupant detection systems, driver monitoring systems, and safety critical systems, ensuring functional safety as per ISO 26262 standards. Furthermore, they support software defined radio, edge AI computing, and secure boot technology for cybersecurity. Memory bandwidth optimization, low latency communication, power efficiency metrics, and thermal management solutions are other essential features that enhance their applicability in the automotive domain. With the integration of vehicle-to-everything communication, AI acceleration hardware, and over-the-air updates, these chips are set to revolutionize the future of automotive technology.

The GPUs segment was valued at USD 840.30 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive AI Chipset Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant evolution, with the Asia-Pacific (APAC) region leading the charge as the largest and most dynamic market worldwide. This region's dominance is attributed to its vast production volumes, rapid technological adoption, and a highly competitive landscape, notably in China. The Chinese market, now the global leader in electric vehicle (EV) production and sales, is a significant battleground for AI chipset supremacy. A unique blend of government incentives, a tech-savvy consumer base, and a burgeoning ecosystem of innovative domestic EV startups, such as NIO, XPENG, Li Auto, and BYD, fuels this region's rapid innovation.

In contrast, mature automotive markets like Japan and South Korea, home to industry giants Toyota and Hyundai, continue to contribute substantially to the market's growth. The APAC the market is expected to witness continued growth, with the Chinese market spearheading the advancements in this sector.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as automakers and tech companies invest heavily in advanced driver-assistance systems (ADAS) and autonomous vehicles. One of the key focus areas in this market is power consumption optimization for automotive AI chipsets, ensuring efficient deep learning inference engines for real-time object detection using AI chipsets in ADAS applications. High-performance computing is essential for autonomous vehicles, and AI chipsets play a crucial role in implementing sensor fusion algorithms and ensuring the accuracy of AI-based driver monitoring systems. Automotive cybersecurity protection is another critical consideration, with hardware security modules integrated into AI chipsets to safeguard against potential threats. Functional safety compliance is mandatory for AI chipsets in vehicles, and low latency communication is essential for autonomous driving.

AI chipset thermal management is also a significant challenge, particularly in extreme temperatures. Over-the-air update mechanisms enable continuous improvement and innovation, while edge AI computing facilitates vehicle diagnostics and AI-powered predictive maintenance. High-definition mapping using AI chipset-based solutions enhances the driving experience, and vehicle-to-everything communication using AI chipsets enables a new level of connectivity. AI chipset design focuses on improved fuel efficiency through system-on-a-chip integration with AI processing units and parallel processing architectures. Memory bandwidth optimization techniques and data compression methods ensure efficient AI inference, making these solutions a valuable investment for the future of the automotive industry.

What are the key market drivers leading to the rise in the adoption of Automotive AI Chipset Industry?

- The escalating demand for advanced driver assistance systems and the pursuit of full autonomy are the primary market drivers, fueling innovation and growth in this sector.

- The market is experiencing significant evolution, fueled by the convergence of vehicle automation trends. Advanced Driver Assistance Systems (ADAS) and the pursuit of fully autonomous driving are key drivers. Regulatory pressure, consumer demand for safety and convenience, and competition among automakers are significant factors. Global regulatory bodies, such as the New Car Assessment Programme (NCAP) and the Insurance Institute for Highway Safety (IIHS), are instrumental in this push. The market's growth is robust, with automotive AI chipsets becoming increasingly integral to modern vehicles.

- According to recent estimates, the market is projected to reach a substantial market size, representing a considerable portion of the overall automotive electronics market. Another study indicates that The market is expected to witness a substantial CAGR during the forecast period.

What are the market trends shaping the Automotive AI Chipset Industry?

- The architectural shift towards centralized computing and domain consolidation is an emerging market trend. This approach prioritizes the concentration of resources and functions within a single, centralized system.

- The market is experiencing a significant transformation as the industry moves away from the traditional Electronic Control Unit (ECU) based systems towards centralized, high performance computing (HPC) platforms. This shift is driven by the limitations of the historical model, which features a multitude of individual ECUs, each responsible for a specific function. This fragmented approach introduces complex wiring, adds vehicle weight and cost, and hinders the implementation of advanced, software-intensive features and over-the-air (OTA) updates. In response, automakers are consolidating these functions into a few powerful domain controllers or, in the most advanced cases, into a single, unified central vehicle computer.

- This architectural change promises to streamline vehicle design, reduce costs, and enable the integration of sophisticated AI applications, enhancing safety, comfort, and connectivity in modern vehicles.

What challenges does the Automotive AI Chipset Industry face during its growth?

- Ensuring functional safety and cybersecurity in the face of extreme technical complexity is a significant challenge that can hinder industry growth. This challenge requires the expertise of professionals to implement effective solutions and maintain a high level of vigilance against potential threats. The importance of addressing this issue cannot be overstated, as the consequences of neglecting functional safety and cybersecurity can be costly and potentially damaging to a company's reputation. Therefore, it is essential to prioritize these concerns and invest in the necessary resources to mitigate risks and ensure the continued growth and success of the industry.

- The market is experiencing significant evolution, driven by the integration of advanced driver assistance systems (ADAS) and autonomous driving technologies in vehicles. The technical complexity of ensuring functional safety (FuSa) and cybersecurity in these systems, which incorporate increasingly powerful AI, poses a substantial challenge. Artificial intelligence, particularly deep learning neural networks, introduces non-deterministic behavior that conflicts with the deterministic safety standards such as ISO 26262.

- Demonstrating the safety of an AI system under an almost infinite number of real-world edge cases is a formidable task. To address this, chipset designers employ a multi-faceted approach, including architectural redundancy, lockstep core configurations, and sophisticated built-in self-test (BIST) capabilities. This ensures the reliability and safety of AI systems in the automotive sector.

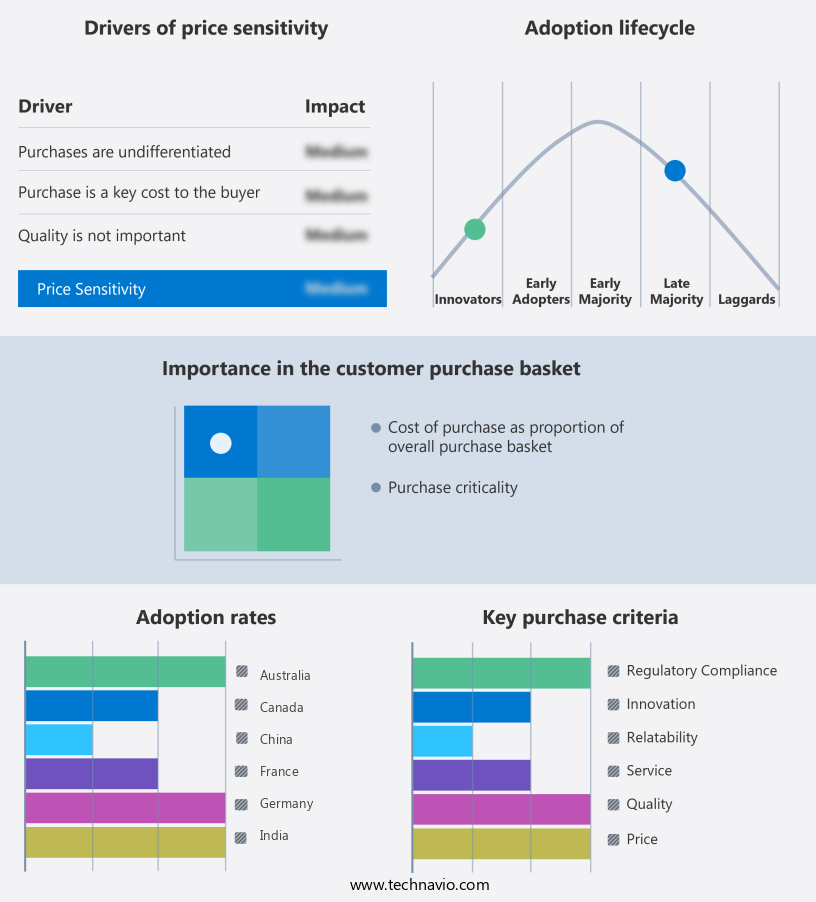

Exclusive Technavio Analysis on Customer Landscape

The automotive ai chipset market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive ai chipset market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive AI Chipset Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive ai chipset market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company's Versal AI Edge XA adaptive SoCs and Ryzen Embedded V2000A Series chipsets deliver advanced automotive AI capabilities. These solutions facilitate real-time sensor fusion and high-performance compute for applications such as advanced driver-assistance systems (ADAS), autonomous driving, and infotainment. The adaptive SoCs and embedded series enable automakers to develop intelligent, connected vehicles.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Ambarella Inc.

- Baidu Inc.

- Black Sesame International Holding Ltd.

- Ceva Inc.

- General Motors Co.

- Horizon Robotics

- Infineon Technologies AG

- Mobileye Technologies Ltd.

- NIO Ltd.

- NVIDIA Corp.

- NXP Semiconductors NV

- Qualcomm Inc.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Tesla Inc.

- Texas Instruments Inc.

- Waymo LLC

- XPeng Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive AI Chipset Market

- In January 2024, NVIDIA Corporation, a leading technology company, announced the launch of its new AI chipset, the Drive Orin, designed specifically for autonomous vehicles. This advanced chipset is capable of handling complex AI workloads, including sensor processing and perception, and is expected to significantly improve the performance and safety of autonomous vehicles (NVIDIA Press Release, 2024).

- In March 2024, Intel Corporation and Mobileye, an autonomous driving technology company, announced a strategic collaboration to develop a new autonomous driving system. This partnership combines Intel's computing capabilities with Mobileye's sensor technology and mapping data, aiming to create a comprehensive autonomous driving solution (Intel Press Release, 2024).

- In May 2024, Ambarella, Inc., a leading developer of low-power, high-definition video processing solutions, completed a USD100 million funding round. This investment will support the company's expansion into the market and the development of new products for advanced driver assistance systems (Ambarella Press Release, 2024).

- In April 2025, the European Union announced the approval of new regulations for autonomous vehicles. These regulations set safety and performance standards for AI chipsets used in autonomous vehicles, ensuring that they meet the necessary requirements for operation in the European market (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive AI Chipset Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

258 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.8% |

|

Market growth 2025-2029 |

USD 7615.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

20.0 |

|

Key countries |

US, China, Japan, Germany, India, UK, South Korea, Canada, France, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by the increasing integration of advanced technologies in the automotive industry. Machine learning inference plays a pivotal role in enabling real-time processing of data from various sensors, leading to improved connectivity protocols and high-performance computing. On-chip memory and data compression methods are essential for optimizing memory bandwidth and reducing power consumption. For instance, a leading automotive chipset manufacturer reported a 30% increase in sales due to the integration of edge AI computing and AI acceleration hardware in their chipsets. The market is projected to grow at a significant rate, with industry experts estimating a 25% annual growth expectation.

- Advancements in parallel processing architectures, such as software-defined radio and sensor fusion techniques, have led to the development of vehicle-to-everything communication and occupant detection systems. Automotive safety standards, hardware security modules, and driver monitoring systems are essential components of safety-critical systems, ensuring functional safety (ISO 26262) and cybersecurity for vehicles. Deep learning processors and secure boot technology enable the implementation of autonomous driving systems and over-the-air updates. Computer vision algorithms and neural network inference further enhance the capabilities of these systems, leading to improved performance and safety. Thermal management solutions and power efficiency metrics are crucial considerations for the design of system-on-a-chip solutions.

- In summary, the market is a dynamic and evolving landscape, with ongoing developments in machine learning inference, connectivity protocols, high-performance computing, and various other technologies shaping the future of the automotive industry.

What are the Key Data Covered in this Automotive AI Chipset Market Research and Growth Report?

-

What is the expected growth of the Automotive AI Chipset Market between 2025 and 2029?

-

USD 7.62 billion, at a CAGR of 20.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (GPUs, ASICs, FPGAs, CPUs, and Others), Application (ADAS, Autonomous vehicles, Infotainment systems, Predictive maintenance, and Others), Vehicle Type (Passenger vehicles, Commercial vehicles, Two wheelers, and Special purpose vehicles), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating demand for advanced driver assistance systems and quest for full autonomy, Extreme technical complexity in ensuring functional safety and cybersecurity

-

-

Who are the major players in the Automotive AI Chipset Market?

-

Advanced Micro Devices Inc., Ambarella Inc., Baidu Inc., Black Sesame International Holding Ltd., Ceva Inc., General Motors Co., Horizon Robotics, Infineon Technologies AG, Mobileye Technologies Ltd., NIO Ltd., NVIDIA Corp., NXP Semiconductors NV, Qualcomm Inc., Renesas Electronics Corp., Samsung Electronics Co. Ltd., STMicroelectronics NV, Tesla Inc., Texas Instruments Inc., Waymo LLC, and XPeng Inc.

-

Market Research Insights

- The market is a dynamic and ever-evolving landscape, driven by the integration of advanced technologies such as ASIC design, recurrent neural networks, and decision-making units into vehicle systems. One notable example of market growth can be seen in the adoption of AI for adaptive cruise control and lane keeping assist, leading to a significant increase in sales of vehicles equipped with these features. According to industry reports, the market is expected to grow by over 20% annually in the coming years. This growth is attributed to the increasing demand for high-performance processing capabilities, with RISC-V architecture and tensor processing units becoming key components in the development of next-generation AI systems for the automotive industry.

- These advancements enable faster processing speeds for path planning, radar signal processing, IMU data processing, and high definition mapping, among other applications. Additionally, the integration of localization algorithms, pedestrian detection, emergency braking systems, and memory capacity expansion through FPGA acceleration further enhances the capabilities of AI in automotive applications. With continued innovation and advancements in AI technology, the automotive industry is poised for significant growth and transformation.

We can help! Our analysts can customize this automotive ai chipset market research report to meet your requirements.

RIA -

RIA -