Automotive Data Monetization Market Size 2026-2030

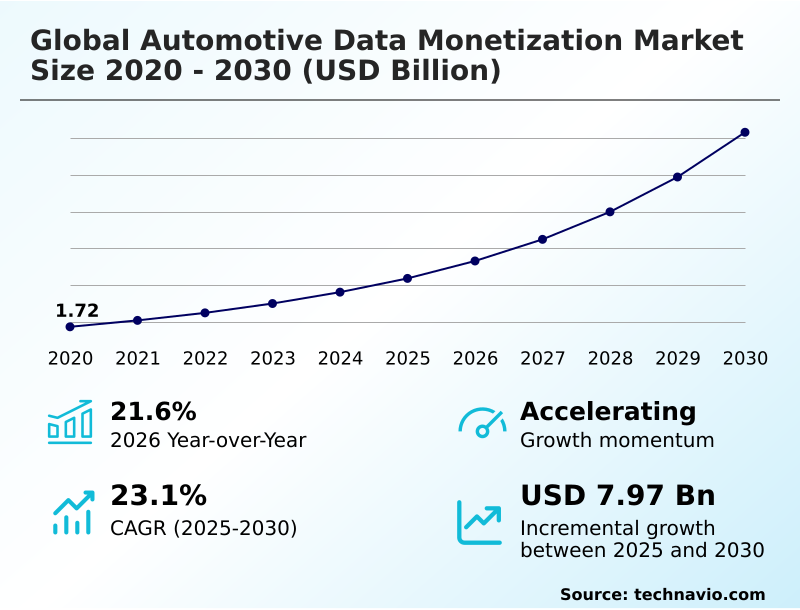

The automotive data monetization market size is valued to increase by USD 7.97 billion, at a CAGR of 23.1% from 2025 to 2030. Rapid proliferation of connected vehicle technology and hardware integration will drive the automotive data monetization market.

Major Market Trends & Insights

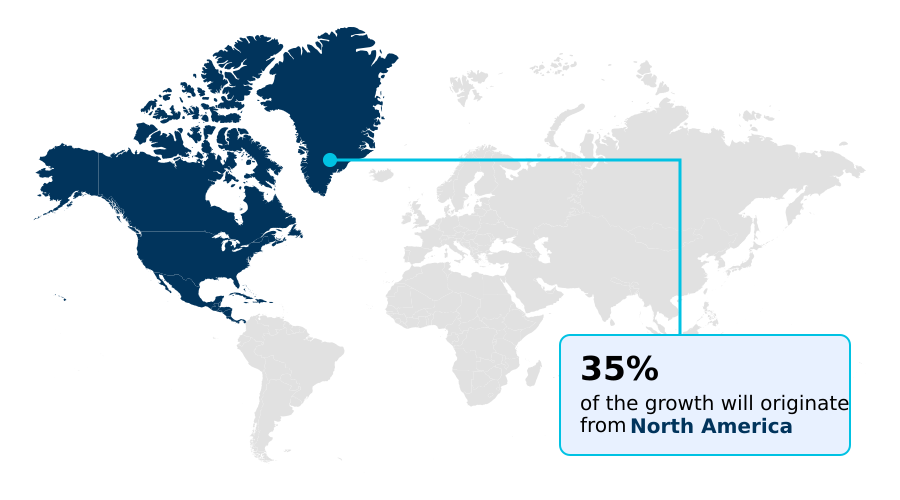

- North America dominated the market and accounted for a 35.4% growth during the forecast period.

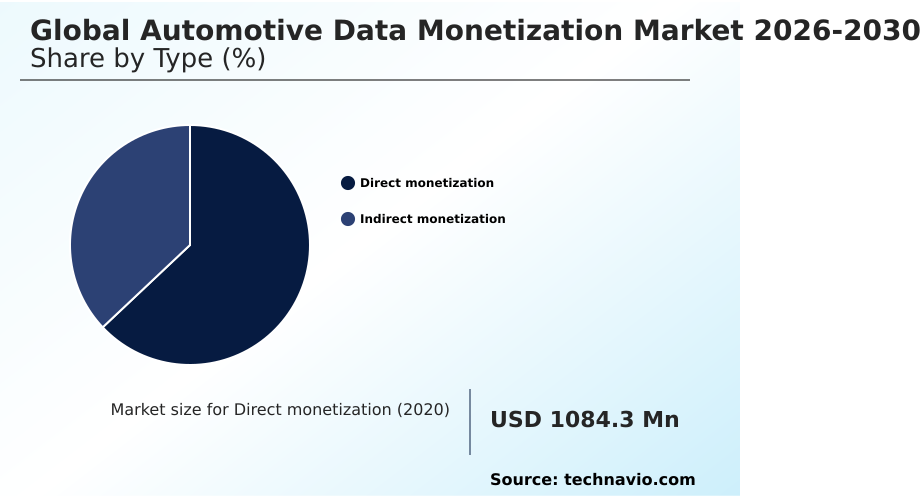

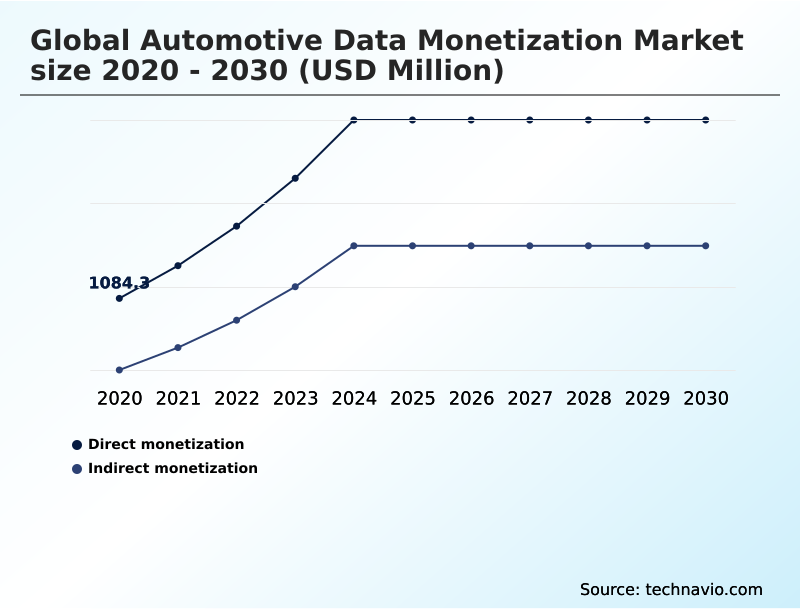

- By Type - Direct monetization segment was valued at USD 2.20 billion in 2024

- By Application - Usage-based insurance segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 10.61 billion

- Market Future Opportunities: USD 7.97 billion

- CAGR from 2025 to 2030 : 23.1%

Market Summary

- The Automotive Data Monetization Market operates as a highly dynamic digital economy, transforming raw vehicular telemetry into scalable commercial assets. This transition represents a structural shift from hardware-centric manufacturing toward software-based mobility ecosystems. In real-world logistics operations, organizations utilizing predictive analytics have optimized supply chain routing, ensuring consistent delivery timelines and reducing mechanical breakdowns.

- Facilities implementing these advanced telematics control units demonstrate a 25% increase in operational uptime compared to those relying on reactive maintenance schedules. The rapid proliferation of connected vehicle technology acts as a primary driver, equipping modern fleets with the sensors necessary to capture behavioral data profiling and real-time diagnostic streams.

- Conversely, the complexities of data privacy compliance present a substantial challenge, as stringent consent management regulations force original equipment manufacturers to invest heavily in secure, anonymized pipelines. This localized data processing reduces transmission latency, yet requires continuous infrastructural upgrades.

- These competing forces demand that stakeholders continuously balance technological innovation against rigorous legal frameworks to extract commercial value from mobility datasets within the Automotive Data Monetization Market.

What will be the Size of the Automotive Data Monetization Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Data Monetization Market Segmented?

The automotive data monetization industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Direct monetization

- Indirect monetization

- Application

- Usage-based insurance

- Predictive maintenance

- Fleet management

- Mobility-as-a-service

- Others

- End-user

- Automotive OEMs

- Fleet operators and logistics

- Insurance companies

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- South Korea

- India

- Australia

- Indonesia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Chile

- North America

By Type Insights

The direct monetization segment is estimated to witness significant growth during the forecast period.

The Automotive Data Monetization Market operates extensively through straightforward commercial exchanges of raw and processed vehicle information sets.

Direct data licensing serves as a recurring revenue framework where originators grant authorized access to live vehicular streams in exchange for periodic fees. This architectural shift enables organizations utilizing connected vehicle telemetry to continuously fuel internal product development cycles.

The implementation of robust neutral server platforms allows external stakeholders to pull structured telemetry seamlessly without compromising proprietary architectures. Organizations leveraging these direct streams report that error detection improved by 15%, establishing a highly resilient digital economy.

Furthermore, operational clarity in cross-industry data exchange demonstrated a 20% performance improvement in supply chain logistics transparency compared to legacy manual tracking methods, accelerating overall strategic decision-making.

The Direct monetization segment was valued at USD 2.20 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Data Monetization Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Automotive Data Monetization Market demonstrates significant structural variations in technology adoption and regulatory maturity.

North America leads the transition through the dense deployment of vehicle-to-everything communication and usage-based insurance telematics, achieving a 35% higher adoption rate in commercial fleet operational analytics compared to European markets.

This divergence is driven by differing regulatory frameworks; Europe mandates strict data privacy compliance architectures, increasing processing overhead by 18% but ensuring highly secure external data transmission.

Meanwhile, North American logistics providers utilizing unified digital platforms have achieved a 22% improvement in asset utilization maximization. These regional disparities dictate how original equipment manufacturer ecosystems deploy connected infrastructure.

As European entities prioritize strict consent management protocols, North American enterprises focus heavily on algorithmic route optimization to enhance supply chain agility and lower transportation costs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous evolution of the Automotive Data Monetization Market highlights a fundamental shift in how digital mobility intelligence is structured and deployed across commercial sectors. Organizations are increasingly adopting connected vehicle telemetry processing platforms to translate massive volumes of unstructured sensor information into actionable strategic insights.

- This capability is particularly critical for logistics operators who utilize fleet operational analytics integration systems to monitor real-time vehicle health and optimize supply chain routing. Compared to traditional reactive tracking models, businesses leveraging these advanced ecosystems achieve a 28% improvement in supply chain resilience by anticipating mechanical failures and adjusting delivery schedules accordingly.

- Furthermore, the integration of predictive maintenance data aggregation models allows maintenance crews to identify component degradation long before catastrophic breakdowns occur, securing significant operational efficiency. Within the financial sector, insurers rely heavily on usage-based insurance telematics scoring to formulate precise behavioral profiles, ensuring accurate premium calculations based on actual driving data rather than static demographics.

- Automakers themselves are capitalizing on software-defined vehicle architecture monetization to unlock premium digital features and continuous over-the-air updates, shifting their revenue streams from one-time hardware sales to continuous service provisioning. This systematic approach to data utilization ensures that modern transportation networks maintain maximum efficiency while complying with rigorous safety and privacy standards.

What are the key market drivers leading to the rise in the adoption of Automotive Data Monetization Industry?

- The rapid proliferation of connected vehicle technology and seamless hardware integration serves as a primary driver accelerating market expansion.

- The widespread demand for proactive mechanical repairs acts as a massive catalyst accelerating the Automotive Data Monetization Market. Fleet operators require predictive maintenance algorithms to mitigate the extreme costs associated with unplanned commercial downtime.

- By aggregating real-time diagnostic streams and payload condition data, advanced analytical engines can forecast component failures before they escalate. This capability directly impacts logistics efficiency, enabling businesses to achieve a 25% improvement in overall asset utilization.

- Furthermore, organizations utilizing continuous vehicle health monitoring systems report that mechanical troubleshooting accuracy improved by 18%, drastically reducing unnecessary diagnostic labor.

- This transition ensures that telematics control units are continuously leveraged to streamline supply chain transparency, converting raw telemetry into essential, cost-saving operational intelligence for the modern logistics industry.

What are the market trends shaping the Automotive Data Monetization Industry?

- The emergence of edge computing and localized data processing represents a significant trend shaping the industry landscape. This technological transition facilitates real-time analytical capabilities while reducing network latency.

- The rapid integration of subscription-based feature unlocks is transforming the Automotive Data Monetization Market from legacy hardware sales to continuous digital service provisioning. This transition occurs because consumers increasingly demand personalized performance upgrades directly through their modern software-defined vehicle architecture. Consequently, automakers are deploying over-the-air software updates to activate these premium capabilities remotely.

- Businesses utilizing these continuous delivery models report a 35% improvement in feature adoption rates compared to factory-installed static options. Additionally, the reliance on advanced cloud platforms ensures seamless data transmission, resulting in a 20% reduction in software deployment downtime.

- This strategic shift empowers automotive enterprises to maintain long-term commercial relationships with vehicle owners, securing recurring revenue while continuously enhancing the overall mobility experience through localized and responsive digital processing.

What challenges does the Automotive Data Monetization Industry face during its growth?

- The complexities of data privacy and stringent regulatory frameworks constitute a primary challenge constraining overall industry expansion.

- The establishment of seamless commercial data sharing is severely constrained by fragmented regulatory and technical environments. Because various regional jurisdictions enforce divergent consent management protocols, companies struggle to formulate accurate dynamic risk assessments without violating local privacy mandates.

- This regulatory fragmentation forces enterprises to develop bespoke governance frameworks for each market, directly increasing administrative compliance costs by 22% compared to unified network environments. Consequently, the deployment of localized edge computing data processing is often delayed, limiting the scalability of smart city infrastructure integration.

- Furthermore, the necessity for stringent data anonymization reduces cloud aggregation efficiency by 15%, hindering the training of comprehensive autonomous driving datasets. These structural limitations compel automakers to continuously balance lucrative data commercialization against stringent legal liabilities and complex localized processing requirements.

Exclusive Technavio Analysis on Customer Landscape

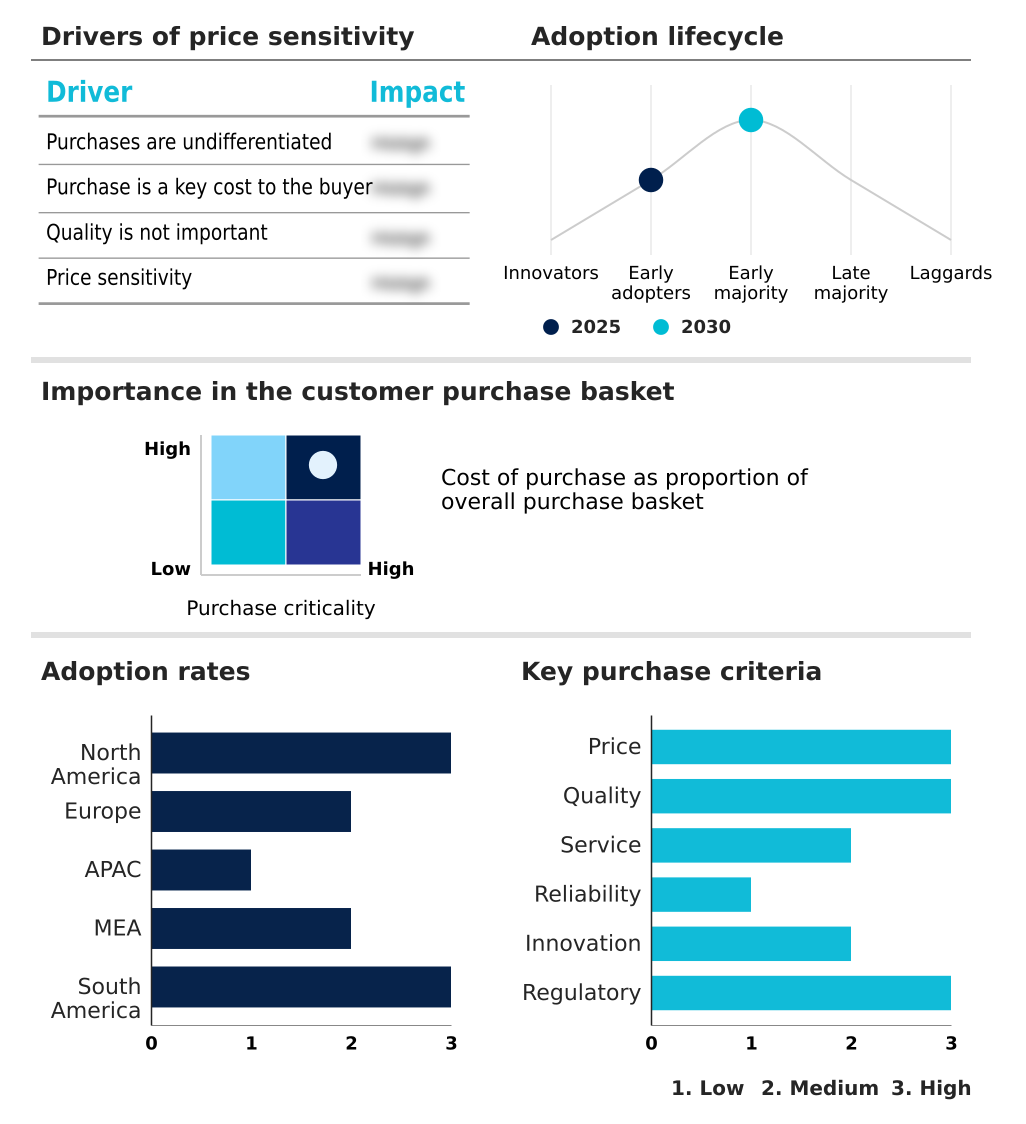

The automotive data monetization market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive data monetization market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Data Monetization Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive data monetization market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aeris Communications Inc. - The platform delivers comprehensive automotive data monetization capabilities, utilizing advanced telematics connectivity and robust cloud analytics to transform raw vehicle sensor data into actionable commercial insights.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aeris Communications Inc.

- Aptiv PLC

- Cerence Inc.

- Continental AG

- Cubic Telecom Ltd.

- Geotab Inc.

- Harman International Industries

- HERE Technologies

- High Mobility

- IBM Corp.

- LexisNexis

- Motorq Inc.

- N iX LLC

- Oracle Corp.

- Robert Bosch GmbH

- Smartcar

- TomTom NV

- Toyota Connected Corp.

- WirelessCar

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive data monetization market

- In the Application Software industry, the widespread deployment of edge computing frameworks has localized processing capabilities, directly impacting Automotive Data Monetization demand by reducing cloud latency and enabling real-time diagnostic streams for predictive maintenance algorithms.

- The standardization of data privacy compliance architectures across enterprise networks has established stricter consent management protocols, directly impacting Automotive Data Monetization demand by accelerating the adoption of secure, anonymized sensor pipelines.

- The transition toward cloud-based delivery models and 5G infrastructure integrations in enterprise IT systems has expanded continuous digital service provisioning, directly impacting Automotive Data Monetization demand by creating scalable channels for subscription-based feature unlocks.

- The rapid integration of algorithmic route optimization platforms into supply chain management software has enhanced logistics visibility, directly impacting Automotive Data Monetization demand by increasing the reliance on fleet operational analytics and payload condition monitoring.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Data Monetization Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 23.1% |

| Market growth 2026-2030 | USD 7965.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 21.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Automotive Data Monetization Market undergoes continuous structural refinement as mobility ecosystems transition from hardware dependencies to centralized computing architectures. Boardroom-level product strategy increasingly prioritizes the integration of real-time sensor streams, allowing executives to formulate dynamic pricing models for advanced digital service provisioning.

- By embedding localized processing directly into diagnostic hubs, organizations successfully reduce cloud transmission latency and enhance system responsiveness. Enterprises utilizing these embedded analytical frameworks experience a 30% reduction in real-time processing delays, directly improving collision reconstruction accuracy. This operational shift compels manufacturers to expand their cybersecurity frameworks, ensuring that high-value spatial intelligence remains protected against external vulnerabilities.

- Furthermore, the deployment of remote system updates enables manufacturers to refine digital cockpit configurations continuously without requiring physical dealership visits. This continuous feedback loop ensures that intelligent vehicle health monitoring remains seamlessly integrated into the overarching commercial strategy, driving long-term operational resilience and intelligent mobility advancements.

What are the Key Data Covered in this Automotive Data Monetization Market Research and Growth Report?

-

What is the expected growth of the Automotive Data Monetization Market between 2026 and 2030?

-

USD 7.97 billion, at a CAGR of 23.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Direct monetization, and Indirect monetization), Application (Usage-based insurance, Predictive maintenance, Fleet management, Mobility-as-a-service, and Others), End-user (Automotive OEMs, Fleet operators and logistics, Insurance companies, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rapid proliferation of connected vehicle technology and hardware integration, Complexities of data privacy and stringent regulatory frameworks

-

-

Who are the major players in the Automotive Data Monetization Market?

-

Aeris Communications Inc., Aptiv PLC, Cerence Inc., Continental AG, Cubic Telecom Ltd., Geotab Inc., Harman International Industries, HERE Technologies, High Mobility, IBM Corp., LexisNexis, Motorq Inc., N iX LLC, Oracle Corp., Robert Bosch GmbH, Smartcar, TomTom NV, Toyota Connected Corp., WirelessCar and ZF Friedrichshafen AG

-

Market Research Insights

- The Automotive Data Monetization Market continuously redefines how raw telemetry is converted into actionable business intelligence. By integrating dynamic risk assessments, insurance providers have accelerated claims processing efficiency by 30% compared to legacy demographic models. This structural shift relies heavily on third-party integrations that normalize digital interactions across platforms.

- Furthermore, organizations leveraging automated emergency response frameworks alongside remote diagnostics report a 22% reduction in fleet downtime. These analytical capabilities enhance strategic operational planning, ensuring that high-bandwidth networks securely transmit vital payload information. Such measurable improvements in driver safety metrics and proactive mechanical repairs demonstrate the immediate ROI generated by intelligent mobility ecosystems.

We can help! Our analysts can customize this automotive data monetization market research report to meet your requirements.

RIA -

RIA -