Automotive Die-stamping Equipment Market Size 2026-2030

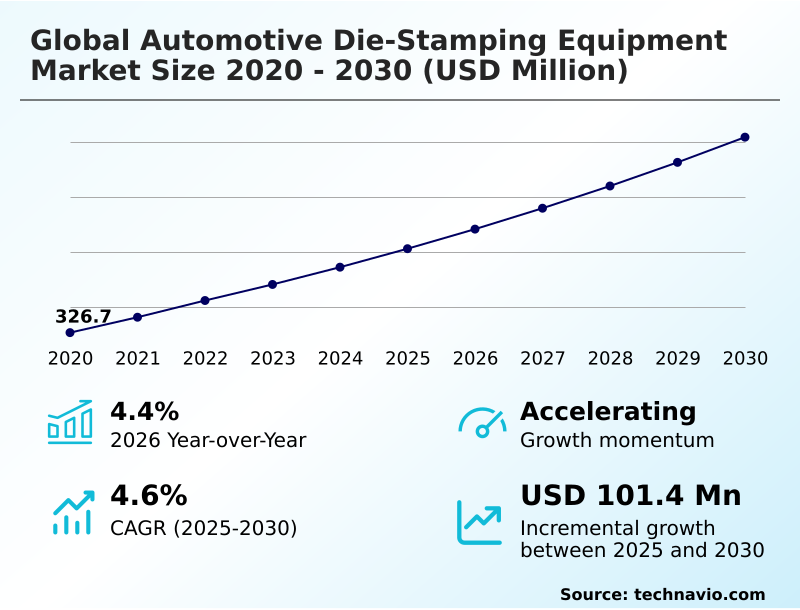

The automotive die-stamping equipment market size is valued to increase by USD 101.4 million, at a CAGR of 4.6% from 2025 to 2030. Accelerating demand for vehicle lightweighting solutions will drive the automotive die-stamping equipment market.

Major Market Trends & Insights

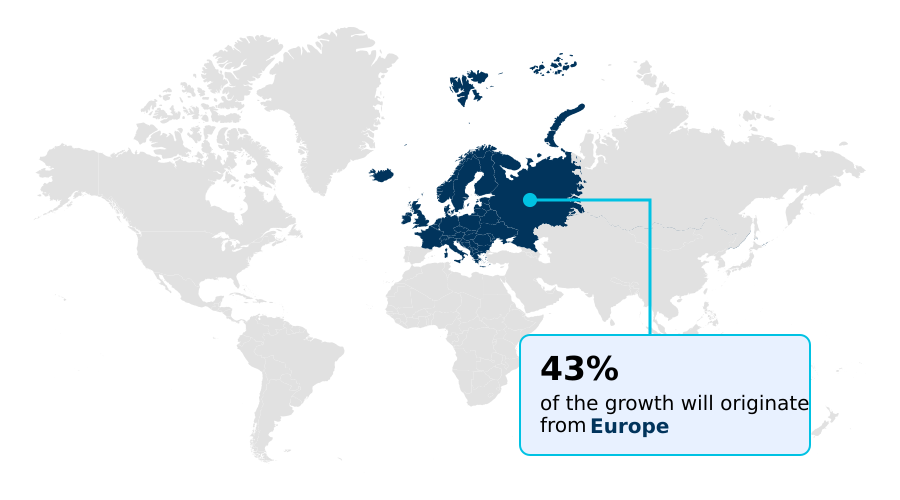

- Europe dominated the market and accounted for a 42.6% growth during the forecast period.

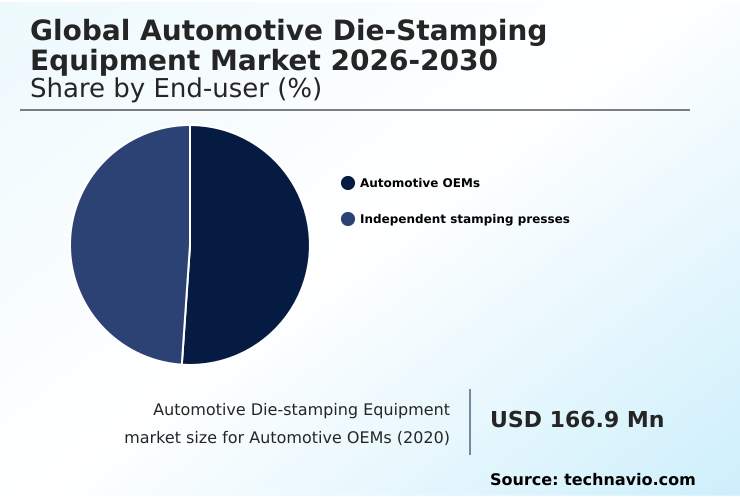

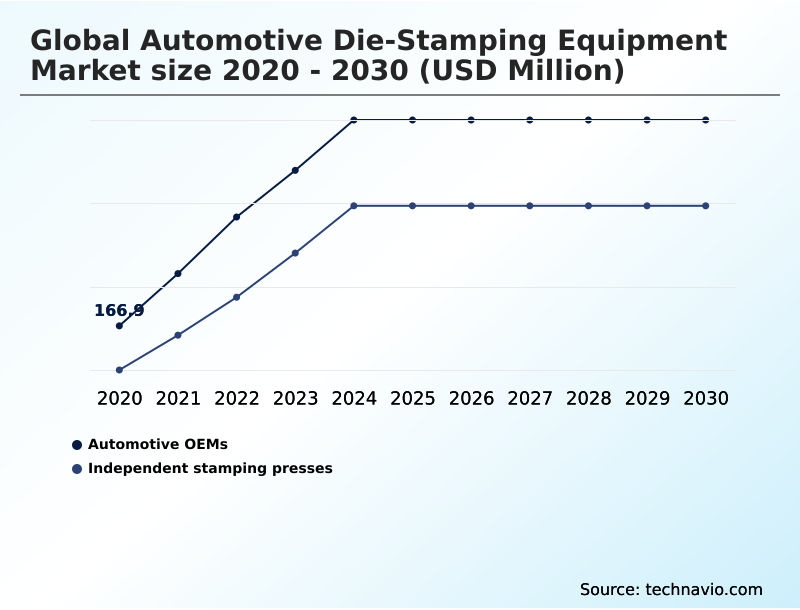

- By End-user - Automotive OEMs segment was valued at USD 200 million in 2024

- By Product Type - Cold stamping segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 177.7 million

- Market Future Opportunities: USD 101.4 million

- CAGR from 2025 to 2030 : 4.6%

Market Summary

- The automotive die-stamping equipment market is undergoing a significant transformation, driven by the automotive industry's pivot toward electrification and enhanced safety standards. This shift necessitates the use of advanced high-strength steels (AHSS) and aluminum alloys, which require sophisticated tooling systems and forming processes.

- Consequently, there is a rising demand for high-tonnage presses, particularly servo-driven press systems and hot stamping technology, to create complex body-in-white (BIW) components and chassis structures with high dimensional accuracy. For instance, a Tier 1 supplier aiming to secure a contract for an electric vehicle's battery enclosure must evaluate investing in a new press hardening line.

- This decision involves balancing the high capital expenditure against the long-term benefits of meeting stringent crashworthiness standards and achieving vehicle lightweighting solutions. The integration of a digital ecosystem, including predictive maintenance protocols and digital twin technologies, is becoming crucial for optimizing overall equipment effectiveness (OEE) and minimizing unplanned downtime.

- However, the industry faces challenges related to the skilled technical workforce required to operate and maintain this advanced mechatronics-based machinery, alongside the technical difficulties of forming advanced materials without issues like the spring-back phenomenon.

What will be the Size of the Automotive Die-stamping Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Die-stamping Equipment Market Segmented?

The automotive die-stamping equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Automotive OEMs

- Independent stamping presses

- Product type

- Cold stamping

- Hot stamping

- Material

- Steel

- Aluminum

- Geography

- Europe

- Germany

- Italy

- UK

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- Europe

By End-user Insights

The automotive oems segment is estimated to witness significant growth during the forecast period.

The automotive OEM segment is redefining its manufacturing infrastructure, driven by the imperative for vehicle lightweighting solutions in electric vehicles. This shift compels investment in advanced die-stamping equipment capable of handling new materials for chassis structures and body-in-white (BIW) components.

OEMs are prioritizing servo-mechanical press lines and hot stamping technology to achieve structural integrity and precise dimensional accuracy. The forming process for these parts is optimized through digital twin technologies to ensure zero-defect production.

This strategic localization of production enhances supply chain resilience, with some OEMs reporting a 15% reduction in cross-continental logistics dependencies. This focus on cost-efficiency and advanced heavy machinery underscores the segment's commitment to high-performance manufacturing without compromising on quality.

The Automotive OEMs segment was valued at USD 200 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 42.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Die-stamping Equipment Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the market is characterized by distinct regional priorities and investment patterns, influencing the demand for specific types of die-stamping equipment.

Europe, a hub for carbon-neutral production, leads in the adoption of energy-efficient servo-driven press systems and press hardening lines for ultra-high-strength steels (UHSS). This region's growth is projected to be approximately 1.7 percentage points higher than North America's.

In contrast, APAC is defined by high-volume production, with an emphasis on high-speed presses and stamping automation systems to meet mass-market demand.

North America is experiencing a wave of reshoring, driving new investments in manufacturing infrastructure and high-tonnage presses for electric vehicle platforms.

This supply chain reconfiguration reflects a global trend toward nearshoring to mitigate logistical risks, requiring advanced tooling systems to maintain competitiveness.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the automotive die-stamping equipment market requires a nuanced understanding of evolving manufacturing demands and technologies. A critical decision for suppliers is the choice between cold stamping vs hot stamping equipment, a determination driven by the specific requirements for forming advanced high strength steels.

- For components like aluminum body panels, investing in a servo press for aluminum body panels is essential for managing the spring-back phenomenon and ensuring surface quality. The return on investment of servo press technology is significant, as these systems offer unparalleled control and efficiency compared to older machinery.

- Addressing the challenges in stamping aluminum alloys and other difficult materials necessitates sophisticated die design for high strength steel and optimized automation in automotive stamping lines.

- Furthermore, the implementation of predictive maintenance for stamping presses, a key aspect of Industry 4.0 in press shop operations, can reduce defect rates by a factor of two compared to reactive maintenance schedules, directly improving supply chain reliability. A thorough cost analysis of die-stamping equipment, including automotive stamping press tonnage calculation, is fundamental for strategic investment.

- As lightweighting strategies in automotive manufacturing intensify, the demand for both high tonnage servo press systems and specialized hot stamping press hardening lines will continue to define the market. This landscape highlights the differences between servo press technology vs hydraulic press capabilities and underscores the growing skill requirements for modern press shops.

- The automotive body-in-white production process is now intrinsically linked to advanced technologies like laser blanking for automotive parts, reshaping how components are made.

What are the key market drivers leading to the rise in the adoption of Automotive Die-stamping Equipment Industry?

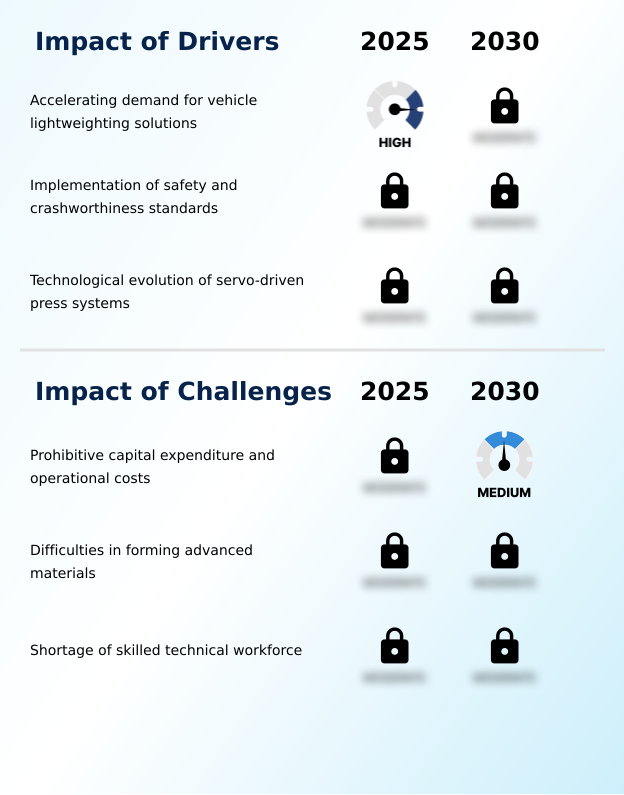

- The accelerating demand for vehicle lightweighting solutions is a key driver for the market.

- Market growth is driven by fundamental shifts in automotive design and manufacturing. The primary catalyst is the push for vehicle lightweighting solutions, which necessitates the use of advanced high-strength steels (AHSS) and aluminum in body-in-white (BIW) components.

- The adoption of servo-driven press systems is critical, as they offer energy efficiency gains of over 30% compared to legacy hydraulic systems.

- A second major driver is the enforcement of stringent crashworthiness standards, which propels the demand for hot stamping technology and press hardening to produce ultra-high-strength steels (UHSS) for crash safety zones.

- The use of these press-hardened steels enhances component strength by more than 1,000 MPa.

- The technological superiority of servo-mechanical press lines, offering superior control over the forming process and increased production flexibility, provides a compelling economic justification for upgrading manufacturing infrastructure.

What are the market trends shaping the Automotive Die-stamping Equipment Industry?

- The integration of Industry 4.0 principles and predictive maintenance protocols is an influential trend shaping the market.

- Key trends are reshaping the market, centered on digitalization and supply chain optimization. The integration of a digital ecosystem through Industry 4.0 is paramount, with digital twin technologies enabling manufacturers to reduce tooling setup times by up to 20%. This is complemented by predictive maintenance protocols, which have demonstrated a capacity to cut unplanned downtime by over 15%.

- Another significant trend is the adoption of laser blanking technology, which provides unparalleled operational flexibility for high-mix, low-volume production scenarios. This shift supports the strategic localization of manufacturing, with reshoring and nearshoring initiatives driving a supply chain reconfiguration.

- These trends collectively push the industry toward greater energy efficiency and zero-defect production, demanding advanced tooling systems and mechatronics-based machinery capable of handling complex automotive components.

What challenges does the Automotive Die-stamping Equipment Industry face during its growth?

- Prohibitive capital expenditure and high operational costs represent a key challenge affecting industry growth.

- The market is constrained by significant financial, technical, and operational challenges. The prohibitive capital expenditure required for modern high-tonnage presses and tandem press lines creates a high barrier to entry, particularly for smaller suppliers.

- On a technical level, forming advanced materials like AHSS introduces complexities such as the spring-back phenomenon, which can increase part rejection rates by up to 10% if not managed with advanced forming processes. This also leads to accelerated die wear.

- A critical operational challenge is the shortage of a skilled technical workforce proficient in the mechatronics and programmable logic controllers (PLCs) that underpin modern die-stamping equipment. This skills gap can extend equipment downtime by an average of 20% during complex repairs, hindering the achievement of optimal overall equipment effectiveness (OEE) and highlighting the difficulties in maintaining advanced heavy machinery.

Exclusive Technavio Analysis on Customer Landscape

The automotive die-stamping equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive die-stamping equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Die-stamping Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive die-stamping equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AIDA Engineering Ltd. - Analysis indicates a focus on delivering advanced servo press and mechanical stamping press solutions engineered for automotive manufacturing applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AIDA Engineering Ltd.

- Amada Co. Ltd.

- Andritz AG

- AP and T

- Beckwood Press

- Chin Fong Machine Industrial Co. Ltd.

- FAGOR ARRASATE

- Galdabini SPA

- Hyundai Wia Corp.

- Isgec Heavy Engineering Ltd.

- JIER Machine Tool Group Co. Ltd.

- Komatsu Ltd.

- Lauffer GmbH and Co. KG

- Macrodyne Technologies Inc.

- Nidec Press and Automation

- OMERA Srl

- Shieh Yih Machinery Industry Co. Ltd.

- G.Siempelkamp GmbH and Co. KG

- SIMPAC America Co. Ltd.

- Yangli Group Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive die-stamping equipment market

- In January, 2025, Honda Development and Manufacturing of America advanced the installation of new manufacturing systems, including high-tonnage die-stamping equipment, at its Marysville Auto Plant as part of its EV Hub initiative in the United States.

- In January, 2025, Schuler, part of the Andritz Group, announced the successful commissioning of a fully digitized ServoTech press line at a major European OEM facility, specifically engineered to produce lightweight aluminum side panels for an upcoming electric SUV fleet.

- In February, 2025, Nidec Press and Automation confirmed the delivery of a 2,500-ton servo transfer press to a leading Tier 1 supplier in Mexico to bolster capacity for manufacturing complex high-strength steel structural components for North American electric vehicles.

- In February, 2025, AP&T confirmed the delivery of a fully automated press hardening line to a European Tier 1 supplier, configured to manufacture complex, high-strength structural components for a new electric vehicle platform.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Die-stamping Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2026-2030 | USD 101.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | Germany, Italy, UK, France, Spain, The Netherlands, China, Japan, South Korea, India, Thailand, Indonesia, US, Canada, Mexico, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Egypt and Morocco |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive die-stamping equipment market is being fundamentally reshaped by the automotive sector's transition to electric mobility and stricter safety mandates. This evolution is fueling demand for advanced heavy machinery, particularly servo-driven press systems and specialized hot stamping technology.

- Manufacturers are investing in servo-mechanical press lines and tandem press lines to achieve the precise forming process required for advanced high-strength steels (AHSS) and other complex materials used in body-in-white (BIW) components and chassis structures. The adoption of mechatronics and programmable logic controllers (PLCs) in stamping automation systems is crucial for managing these sophisticated operations.

- For executive leadership, this translates into critical capital allocation decisions; for example, a CFO must approve a multi-million-dollar investment in a new servo tandem line, weighing the high upfront cost against the long-term ROI from forming ultra-high-strength steels (UHSS) and securing contracts for next-generation automotive components.

- Such an investment can reduce processing time by up to 20% compared to legacy equipment. This landscape also sees innovation in press hardening, deep draw forming, and the use of hydraulic forming presses, transfer presses, and high-speed progressive die presses.

- Technologies like gigacasting and hydroforming are emerging, while demand for electrical steel laminations, blanking lines, and specialized trimming and beading machines grows. This positions press shop operations as a central focus for technological advancement.

What are the Key Data Covered in this Automotive Die-stamping Equipment Market Research and Growth Report?

-

What is the expected growth of the Automotive Die-stamping Equipment Market between 2026 and 2030?

-

USD 101.4 million, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Automotive OEMs, and Independent stamping presses), Product Type (Cold stamping, and Hot stamping), Material (Steel, and Aluminum) and Geography (Europe, APAC, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerating demand for vehicle lightweighting solutions, Prohibitive capital expenditure and operational costs

-

-

Who are the major players in the Automotive Die-stamping Equipment Market?

-

AIDA Engineering Ltd., Amada Co. Ltd., Andritz AG, AP and T, Beckwood Press, Chin Fong Machine Industrial Co. Ltd., FAGOR ARRASATE, Galdabini SPA, Hyundai Wia Corp., Isgec Heavy Engineering Ltd., JIER Machine Tool Group Co. Ltd., Komatsu Ltd., Lauffer GmbH and Co. KG, Macrodyne Technologies Inc., Nidec Press and Automation, OMERA Srl, Shieh Yih Machinery Industry Co. Ltd., G.Siempelkamp GmbH and Co. KG, SIMPAC America Co. Ltd. and Yangli Group Corp.

-

Market Research Insights

- The market's momentum is shaped by the strategic adoption of technologies that deliver measurable business outcomes. The shift to servo-driven press systems, for instance, has demonstrated energy efficiency improvements of up to 40% over legacy hydraulic units, directly impacting operational costs.

- Concurrently, the implementation of predictive maintenance protocols within a connected digital ecosystem has enabled manufacturers to reduce unplanned downtime by over 25%, enhancing production versatility. This focus on cost-efficiency and structural integrity is critical as the industry embraces vehicle lightweighting solutions and more complex automotive components.

- The strategic localization of manufacturing infrastructure is further altering the competitive landscape, compelling suppliers to invest in equipment that ensures both operational flexibility and high-mix, low-volume production capabilities. This push toward industrial digitization is essential for maintaining a competitive edge.

We can help! Our analysts can customize this automotive die-stamping equipment market research report to meet your requirements.

RIA -

RIA -