Automotive Exhaust Manifold Market Size 2026-2030

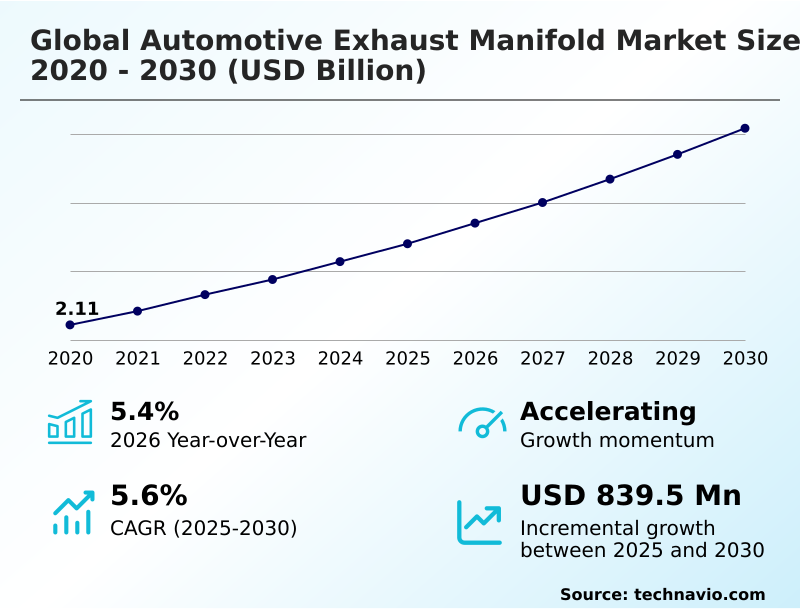

The automotive exhaust manifold market size is valued to increase by USD 839.5 million, at a CAGR of 5.6% from 2025 to 2030. Stringent emissions regulations and mandatory thermal efficiency standards will drive the automotive exhaust manifold market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41.5% growth during the forecast period.

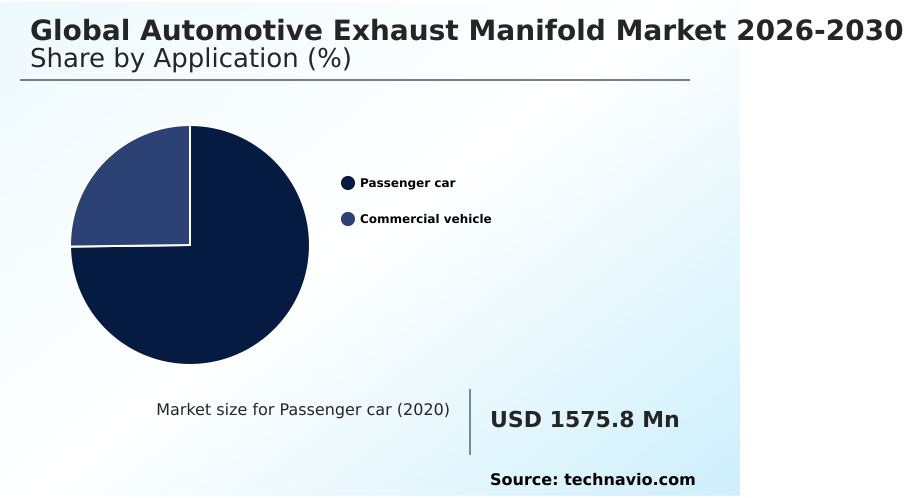

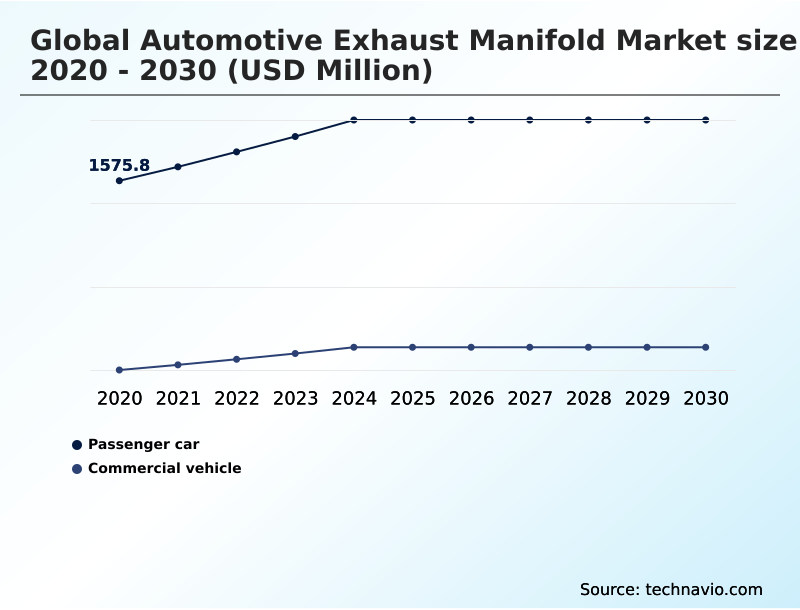

- By Application - Passenger car segment was valued at USD 1.91 billion in 2024

- By Fuel Type - Gasoline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.44 billion

- Market Future Opportunities: USD 839.5 million

- CAGR from 2025 to 2030 : 5.6%

Market Summary

- The Automotive Exhaust Manifold Market is undergoing a rapid architectural evolution driven by the absolute necessity to minimize tailpipe emissions while maximizing engine performance. Stringent international emissions regulations compel automakers to replace heavy conventional castings with advanced thin-walled tubular designs that accelerate catalytic converter activation.

- This regulatory pressure acts as the primary market driver, fueling massive procurement shifts toward high-grade alloys that resist extreme oxidation. In a real-world supply chain scenario, tier-one component manufacturers have upgraded their fabrication lines with automated robotic welding, reducing geometric defect rates by 18% during high-volume production runs.

- This operational efficiency ensures that complex modular assemblies remain gas-tight under immense thermal stress. Conversely, the aggressive industry transition toward pure battery electric vehicles presents a critical structural challenge, as electric powertrains completely eliminate the need for traditional exhaust infrastructure, thereby shrinking the long-term addressable market.

- Consequently, component suppliers are optimizing internal combustion architectures to sustain profitability while adapting to shifting macroeconomic vehicle production volumes.

What will be the Size of the Automotive Exhaust Manifold Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Exhaust Manifold Market Segmented?

The automotive exhaust manifold industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Passenger car

- Commercial vehicle

- Fuel type

- Gasoline

- Diesel

- Material

- Cast iron

- Stainless steel

- Others

- Distribution channel

- OEM

- Aftermarket

- Geography

- APAC

- China

- Japan

- India

- South Korea

- Thailand

- Indonesia

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Poland

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Turkey

- Saudi Arabia

- UAE

- Egypt

- APAC

By Application Insights

The passenger car segment is estimated to witness significant growth during the forecast period.

The passenger car application segment demands highly engineered configurations designed to operate as a precise thermal management component within modern engine bays.

Driven by ultra-strict environmental regulations and clean air standards, automakers are aggressively transitioning toward fabricated multi-layer stainless steel designs. This shift addresses corporate average fleet emissions by accelerating heat transfer to downstream emissions control systems.

The lower thermal mass of these advanced assemblies facilitates rapid catalyst light-off, which drastically curtails the release of toxic nitrogen oxides during the critical cold-start phase combustion cycle.

Implementing these lightweight structures has improved overall vehicle fuel efficiency by 12% in specific passenger models. By integrating a close-coupled catalytic converter directly into the manifold, OEM engineers minimize exhaust heat loss, maximizing conversion efficiency and supporting continuous legislative compliance.

The Passenger car segment was valued at USD 1.91 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Exhaust Manifold Market Demand is Rising in APAC Get Free Sample

The geographic distribution of the Automotive Exhaust Manifold Market reveals stark contrasts in manufacturing adoption and regulatory pressures. While emerging regions favor cast iron, North America and Europe rapidly pivot toward lightweight assemblies to accommodate downsized turbocharged internal combustion engines.

This regional divergence is highlighted by European manufacturers improving catalytic efficiency by 25% through the deployment of complex hybrid-electric vehicle architectures.

To safely manage severe thermal expansion, European suppliers prioritize high-temperature oxidation resistance and structural warping prevention, reducing component warranty claims by 14% compared to traditional markets.

Furthermore, North American engineering facilities are prioritizing fluid dynamics optimization for high-pressure turbochargers to effectively neutralize particulate matter. These strategic material adaptations ensure strict compliance with regional greenhouse gas thresholds while satisfying diverse continental consumer performance expectations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As automotive engineering shifts toward maximizing thermal efficiency, manufacturers must continuously address complex hybrid vehicle thermal retention challenges. Hybrid powertrains experience frequent engine start-stop cycles, requiring advanced exhaust infrastructure that prevents critical heat from dissipating during electric-only operational phases. To mitigate these extreme temperature fluctuations, the industry is accelerating the deployment of dual wall fabricated stainless steel manifolds.

- These highly sophisticated components feature an insulating air gap that effectively traps exhaust heat, ensuring immediate operational readiness. This thermal management directly supports close coupled catalyst rapid heating, which is absolutely vital for reducing hazardous tailpipe emissions during the initial seconds of combustion.

- Compared to legacy single-wall cast iron components, these modern dual-wall architectures improve heat retention by nearly 30%, vastly enhancing the performance of downstream emissions control hardware. Furthermore, the rising integration of multi-stage turbocharging exhaust systems in both commercial and premium passenger segments demands absolute structural precision to handle intense backpressure and extreme gas velocities.

- To achieve these rigorous aerodynamic and structural requirements, tier-one suppliers are heavily investing in automated robotic welding in component fabrication. This advanced manufacturing approach eliminates manual inconsistencies, reducing microscopic weld-seam defects and significantly lowering long-term component failure rates.

- Through these targeted engineering strategies and advanced material applications, the supply chain continues to optimize internal combustion platforms against escalating international environmental mandates.

What are the key market drivers leading to the rise in the adoption of Automotive Exhaust Manifold Industry?

- Stringent emissions regulations and mandatory thermal efficiency standards propel the industry by forcing automakers to adopt advanced materials that accelerate catalytic converter activation.

- The aggressive expansion of localized emissions mandates acts as a paramount driver reshaping the Automotive Exhaust Manifold supply chain.

- Automakers are increasingly securing multi-year procurement contracts for integrated hot-end modules that drastically compress the physical distance between the engine block and primary catalytic converters.

- To manufacture these complex assemblies, tier-one suppliers leverage predictive machine learning design tools and advanced hydroforming manufacturing technologies. This technological synergy allows engineers to mitigate severe mechanical stresses effectively, improving downstream emissions neutralization by nearly 20%.

- While traditional cast iron retains its position in sectors demanding extreme structural density, mass-market passenger vehicle production aggressively adopts advanced ferritic stainless steel solutions.

- Fused seamlessly using robotic gas tungsten arc welding, these premium material structures ensure maximum durability and strict statutory compliance without inflating manufacturing overhead.

What are the market trends shaping the Automotive Exhaust Manifold Industry?

- The rising integration of close-coupled catalytic converters and modular manifold designs represents a pivotal shift in automotive thermal management. This architectural evolution ensures rapid catalyst activation to strictly comply with escalating international clean air standards.

- The rapid integration of advanced virtual simulation software is radically reshaping the engineering landscape of the Automotive Exhaust Manifold. Utilizing comprehensive digital twin simulations allows suppliers to evaluate fluid dynamics seamlessly, decreasing physical prototyping overhead by 25%. This digital transition supports the widespread adoption of double-walled manifold fabrications and insulated manifold fabrications designed specifically for modern compact high-efficiency powerplants.

- By replacing outdated automated sand casting methods with highly precise thin-walled stainless steel architectures, manufacturers achieve critical internal geometries optimization that drastically improves engine backpressure reduction. Consequently, component assembly weight has decreased by up to 18%, significantly enhancing vehicle power-to-weight ratios.

- Meanwhile, even the heavy-duty long-haul commercial trucks sector is selectively adopting these advanced lightweight configurations, ensuring that continuous thermal innovation aligns flawlessly with rigorous international sustainability targets.

What challenges does the Automotive Exhaust Manifold Industry face during its growth?

- Rapid electrification trajectories and regulatory adjustments that reduce internal combustion engine volume significantly constrain long-term production forecasts for traditional exhaust infrastructure.

- The immense manufacturing complexity required to produce modern exhaust infrastructure presents a severe operational challenge for the Automotive Exhaust Manifold industry. Designing aerodynamically optimized manifold geometries to eliminate engine lag demands intricate sheet metal assemblies that endure extreme thermodynamic loads.

- To combat elevated geometric defect rates, manufacturers must invest heavily in advanced quality control protocols focused strictly on critical weld-seam thinning prevention and reliable micro-porosity reduction. Despite these costly technological upgrades, the integration of hybrid powertrains subjects expensive austenitic stainless steel alloys to high-intensity engine start-stop cycles, accelerating structural thermal fatigue.

- Furthermore, replacing robust cast iron forces engineers to sacrifice natural vibration dampening qualities to achieve aggressive vehicular lightweighting targets. Implementing these rigorous geometric tolerances has increased localized manufacturing costs by 15%, heavily squeezing operational profit margins for tier-two supply chain participants.

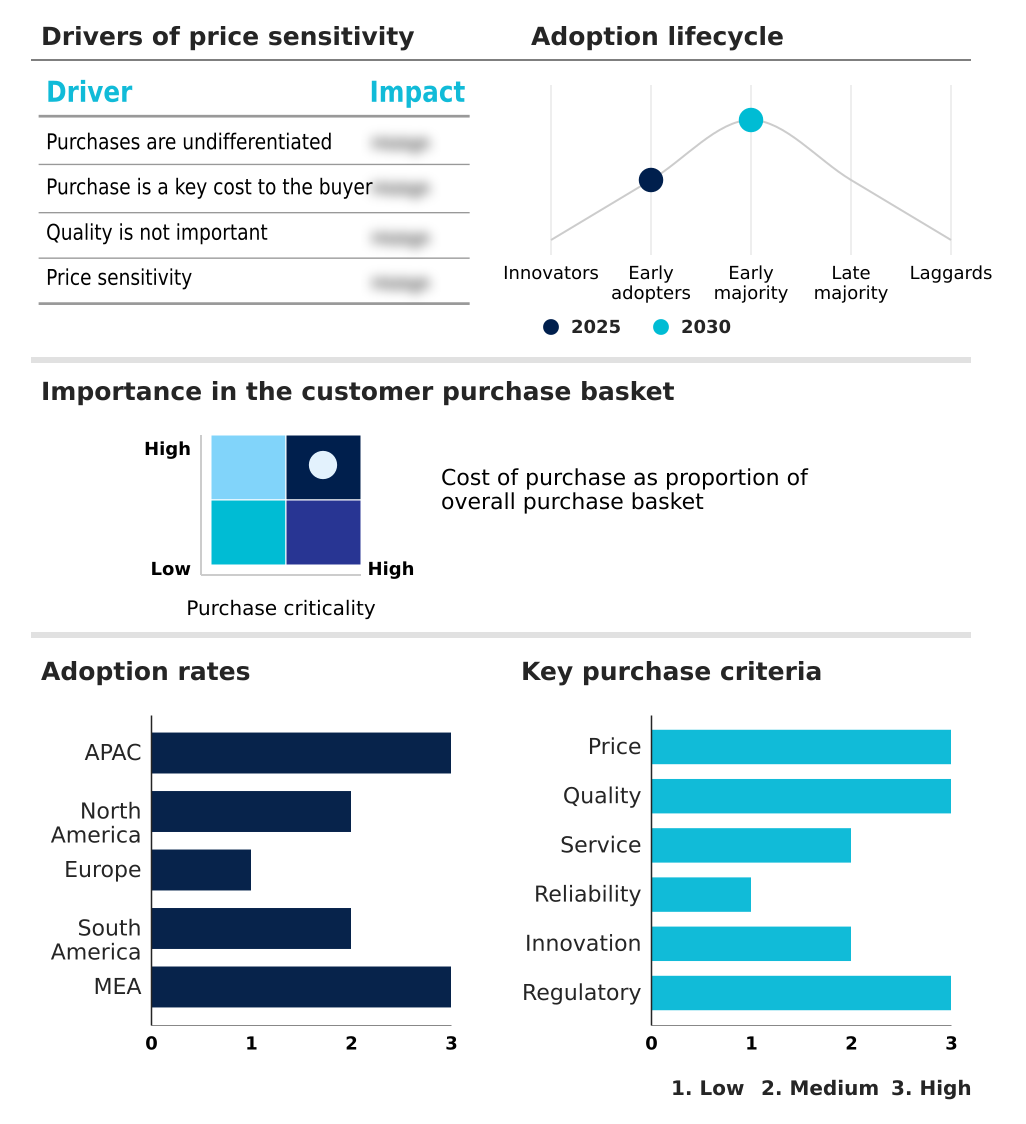

Exclusive Technavio Analysis on Customer Landscape

The automotive exhaust manifold market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive exhaust manifold market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Exhaust Manifold Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive exhaust manifold market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

advanced FLOW engineering Inc. - The prominent vendor supplies highly engineered automotive exhaust manifold assemblies including lightweight tubular stainless steel headers and cast iron configurations designed to optimize exhaust flow and structural durability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- advanced FLOW engineering Inc.

- AP Emissions Technologies

- Bellows Systems Inc.

- Benteler International AG

- Borla Performance Industries

- Bosal Nederland BV

- Dorman Products Inc.

- Eberspacher Gruppe GmbH

- Forvia SE

- Friedrich Boysen GmbH and Co.

- Futaba Industrial Co. Ltd.

- GP Headers Inc.

- Ilmor Engineering Inc.

- Marelli Holdings Co. Ltd.

- MetalTek International

- SHARDA MOTOR INDUSTRIES LTD.

- Stainless Works

- Tenneco Inc.

- Vibrant Power Inc.

- Yutaka Giken Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive exhaust manifold market

- In the Automotive Parts and Equipment industry, the aggressive implementation of Euro VII regulations mandated the integration of advanced thermal management systems, directly impacting Automotive Exhaust Manifold demand by forcing a structural shift toward rapid-heating stainless steel components.

- The widespread adoption of predictive machine learning design tools optimized aerodynamic fluid routing across engine components, reducing internal airflow resistance by 15% and increasing the engineering complexity required for next-generation Automotive Exhaust Manifold geometries.

- The continuous transition toward downsized turbocharged internal combustion engines increased average operating temperatures above 950 degrees Celsius, accelerating the Automotive Exhaust Manifold market shift from basic cast iron to highly durable austenitic stainless steel alloys.

- The integration of multi-piece flexible hot-end modules reduced vehicle assembly line packaging footprints by 10%, heavily influencing Automotive Exhaust Manifold procurement strategies toward modular, pre-assembled catalytic converter configurations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Exhaust Manifold Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.6% |

| Market growth 2026-2030 | USD 839.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.4% |

| Key countries | China, Japan, India, South Korea, Thailand, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, Poland, Brazil, Argentina, Colombia, South Africa, Turkey, Saudi Arabia, UAE and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The continuous evolution of the Automotive Exhaust Manifold relies heavily on addressing the intense thermal expansion and severe mechanical stresses generated by modern high-output powerplants. To withstand extreme thermodynamic loads frequently exceeding nine hundred degrees Celsius, component suppliers are systematically abandoning traditional heavy cast iron in favor of advanced ferritic stainless steel and premium austenitic stainless steel alloys.

- This material substitution directly aligns with boardroom-level product strategies focused on aggressive vehicular weight reduction and long-term regulatory compliance. Incorporating these resilient materials allows engineers to develop aerodynamically optimized manifold geometries that smoothly channel exiting exhaust pulses, which effectively minimizes engine lag and maximizes turbocharger efficiency.

- By adopting these complex fabricated architectures, automotive manufacturers have achieved a 20% reduction in total exhaust system mass, drastically improving fuel economy metrics. This technological transition ensures that internal combustion platforms remain viable amid tightening legislative frameworks, forcing tier-one suppliers to continuously refine automated manufacturing techniques and material procurement strategies to maintain their competitive industrial positioning.

What are the Key Data Covered in this Automotive Exhaust Manifold Market Research and Growth Report?

-

What is the expected growth of the Automotive Exhaust Manifold Market between 2026 and 2030?

-

USD 839.5 million, at a CAGR of 5.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger car, and Commercial vehicle), Fuel Type (Gasoline, and Diesel), Material (Cast iron, Stainless steel, and Others), Distribution Channel (OEM, and Aftermarket) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent emissions regulations and mandatory thermal efficiency standards, Rapid electrification trajectories and regulatory adjustments reducing internal combustion volume

-

-

Who are the major players in the Automotive Exhaust Manifold Market?

-

advanced FLOW engineering Inc., AP Emissions Technologies, Bellows Systems Inc., Benteler International AG, Borla Performance Industries, Bosal Nederland BV, Dorman Products Inc., Eberspacher Gruppe GmbH, Forvia SE, Friedrich Boysen GmbH and Co., Futaba Industrial Co. Ltd., GP Headers Inc., Ilmor Engineering Inc., Marelli Holdings Co. Ltd., MetalTek International, SHARDA MOTOR INDUSTRIES LTD., Stainless Works, Tenneco Inc., Vibrant Power Inc. and Yutaka Giken Co. Ltd.

-

Market Research Insights

- The Automotive Exhaust Manifold Market is rapidly evolving to support compact high-efficiency powerplants that demand exceptional thermal stability. Automakers are prioritizing the critical cold-start phase combustion cycle by deploying components that rapidly transfer heat to downstream emissions control systems.

- By utilizing advanced virtual simulation software, engineering teams have reduced prototype development times by 22%, allowing for faster compliance with stringent greenhouse gas thresholds. Furthermore, these optimized geometric designs have lowered exhaust backpressure, improving total engine operational efficiency by up to 14% across modern vehicle fleets.

- This continuous digital transformation ensures that material innovations align perfectly with regulatory demands and advanced powertrain requirements without inflating manufacturing overhead.

We can help! Our analysts can customize this automotive exhaust manifold market research report to meet your requirements.

RIA -

RIA -