Automotive Laser Headlight System Market Size 2024-2028

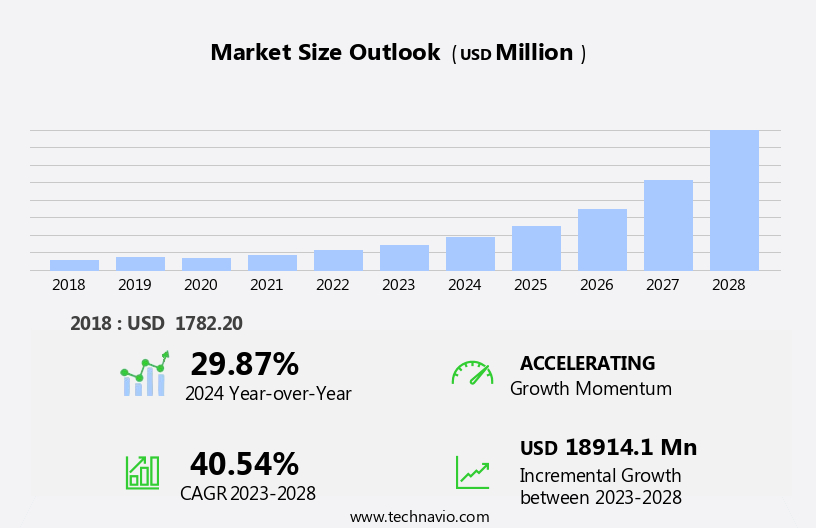

The automotive laser headlight system market size is forecast to increase by USD 18.91 billion at a CAGR of 40.54% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing adoption of energy-efficient solutions in automobiles and the rise in research and development (R&D) spending on headlight technology. The shift towards advanced lighting systems, such as laser headlights, is a key trend in the market, with automakers prioritizing improved visibility, energy savings, and design aesthetics. The adoption of light-emitting diode (LED) lighting in automobiles is another significant trend, as it offers numerous advantages, including longer lifespan, reduced energy consumption, and enhanced lighting performance.

- However, challenges such as high production costs and regulatory compliance remain, necessitating strategic planning and innovation from market participants to capitalize on the market's potential and navigate these challenges effectively. Companies seeking to capitalize on the opportunities in the market must focus on developing cost-effective solutions, collaborating with technology partners, and staying abreast of regulatory requirements to maintain a competitive edge.

What will be the Size of the Automotive Laser Headlight System Market during the forecast period?

- The market is experiencing significant growth due to advancements in photonics technology and the increasing demand for enhanced road safety and improved illumination range in various vehicle segments. Laser diodes, a key component of laser headlights, are driving this trend, as they offer superior brightness and longer lifespan compared to traditional LED-powered lights. The semiconductor sector is playing a crucial role in the development and production of these advanced headlight systems. The passenger vehicle and light commercial vehicle segments are major contributors to the market's growth, with logistics vehicles and luxury automobiles also showing strong demand. Passenger car sensors and night vision cameras are complementary technologies that further boost the market's potential.

- Additionally, the integration of LiFi communication and autonomous driving technologies is expected to create new opportunities for photonics executives in the automotive industry. Global vehicle production continues to increase, leading to a larger addressable market for headlamp manufacturers. The use of phosphorous lenses and other photonics-related technologies is further expanding the capabilities of laser headlights, providing high-resolution sensing and contributing to overall road safety. The integration of laser headlights in recreational vans and other applications is also gaining traction, broadening the market's scope.

How is this Automotive Laser Headlight System Industry segmented?

The automotive laser headlight system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

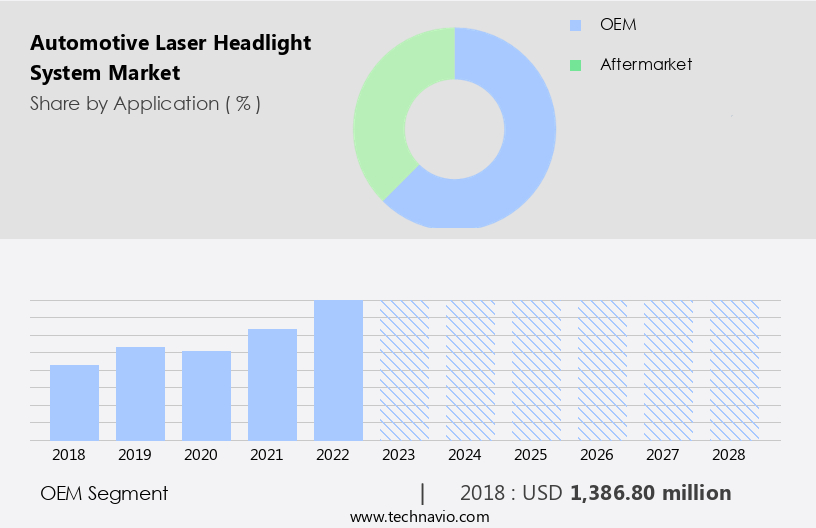

- Application

- OEM

- Aftermarket

- End-user

- Passenger cars

- Motorcycle

- Geography

- Europe

- Germany

- Italy

- UK

- APAC

- China

- North America

- US

- Middle East and Africa

- South America

- Europe

By Application Insights

The oem segment is estimated to witness significant growth during the forecast period.

Laser headlight technology is revolutionizing the automotive industry, offering brighter and energy-efficient illumination for both light commercial vehicles and passenger cars. OEMs are increasingly adopting this advanced technology to enhance safety and visibility for drivers. With a focus on innovation and customer experience, OEMs are incorporating laser headlights into their vehicles to differentiate themselves from competitors. Initially, laser headlights were primarily found in high-end or luxury models due to their higher cost. However, as technology advances and becomes more cost-effective, it is becoming increasingly attractive for integration into a wider range of vehicle models. Moreover, the integration of laser headlights is not limited to passenger cars alone.

They are also being adopted in logistics vehicles and recreational vans to improve road safety. The technology's long lighting distance and high-resolution sensing capabilities make it an ideal solution for autonomous vehicles and pedestrian protection systems. The photonics-related businesses, including headlamp manufacturers, are at the forefront of this technological shift. The automotive industry's digitalization trend is driving the adoption of laser headlights. The Internet of Things (IoT) and smart automotive electronics are enabling software control and computing capabilities, making laser headlights an integral part of the overall vehicle system. Energy efficiency and intelligent technology are also significant factors in the growing popularity of laser headlights.

Electric vehicles and hybrid vehicles are increasingly incorporating laser headlights to enhance their lighting systems. Laser diodes are the key components of laser headlights. Automakers closely monitor advancements in laser diode technology to ensure they can offer the latest and most advanced features to their customers. The integration of night vision cameras and LiFi communication systems further enhances the capabilities of laser headlights, providing drivers with a comprehensive view of their surroundings and improving road safety. In , laser headlights represent a significant advancement in automotive lighting technology. Their adoption is driven by a combination of factors, including improved safety, energy efficiency, and the desire for differentiation.

As technology continues to evolve, we can expect to see laser headlights becoming increasingly common in a wide range of vehicle models.

Get a glance at the market report of share of various segments Request Free Sample

The OEM segment was valued at USD 1.39 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

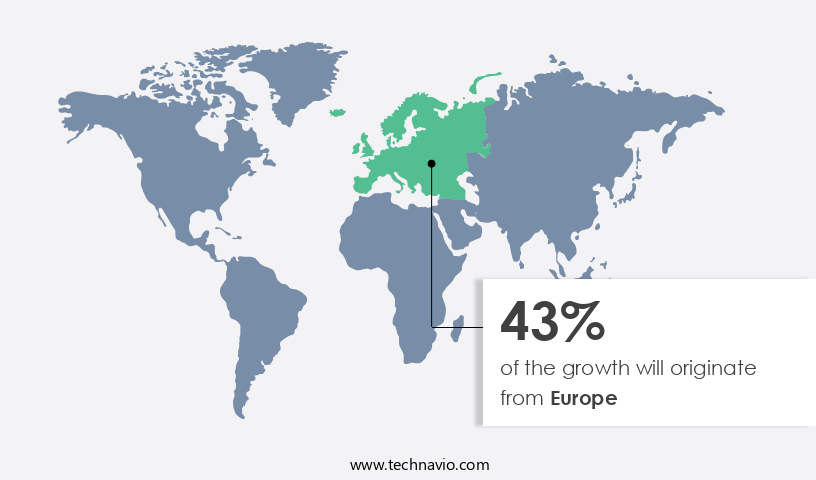

Europe is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The European automotive market is characterized by the presence of numerous luxury car Original Equipment Manufacturers (OEMs), including AUDI AG, BMW, and Daimler, who incorporate advanced lighting solutions to boost safety and aesthetics in their vehicles. The European market's positive response to laser headlight system technology has resulted in high adoption rates in recent years. This market's dynamism can be attributed to continuous technological advancements in automotive lighting systems. The European automotive industry's competitiveness is due to the presence of leading automotive OEMs, and the demand for vehicles equipped with sophisticated technologies and features remains high. The market for automotive laser headlight systems is witnessing significant growth, driven by the integration of intelligent technology, digitalization, and energy efficiency in headlamp systems.

In the passenger cars segment, laser headlights offer long lighting distances and high-resolution sensing capabilities, enhancing road safety. The integration of night vision cameras, IoT, and software control in these systems further improves safety by providing real-time pedestrian protection. Additionally, the growing popularity of electric and hybrid vehicles is fueling the demand for laser headlights due to their energy efficiency. Photonics-related businesses, including headlamp manufacturers, are investing in research and development to create advanced lighting systems using laser diodes and photonics technology. The semiconductor sector also plays a crucial role in the production of laser diodes, enabling the miniaturization and cost reduction of laser headlight systems.

The increasing adoption of autonomous vehicles and smart automotive electronics is expected to further drive the growth of the market. The integration of intelligent technology, such as computing and sensing, in these systems allows for real-time data processing and analysis, enhancing the overall driving experience. In , the European automotive market's continuous technological advancements and high demand for luxury vehicles equipped with advanced features are driving the growth of the market. The integration of laser diodes, IoT, and software control in these systems is enhancing road safety, energy efficiency, and the overall driving experience.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Automotive Laser Headlight System Industry?

- Incorporation of energy-efficient solutions in automobiles is the key driver of the market.

- The global automotive industry is witnessing a shift towards energy efficiency, with governments and automotive original equipment manufacturers (OEMs) prioritizing the adoption of energy-saving technologies. One such technology gaining significant attention is the use of advanced laser headlight systems. These systems offer numerous benefits, including lower power consumption and longer service intervals, making them an attractive option for consumers. Emerging economies, such as India, are implementing stringent emission regulations, leading to an increase in the production of energy-efficient vehicles. This trend is expected to continue, as consumers become more conscious of their carbon footprint and governments promote the use of eco-friendly vehicles.

- Moreover, the development of electric vehicles (EVs) is a critical area of focus for OEMs. With growing awareness about green energy and the need to comply with stringent emission standards, many prominent OEMs are investing heavily in EV technology. The implementation of laser headlight systems in EVs can further enhance their energy efficiency, making them an attractive option for consumers. In , the adoption of energy-efficient technologies, including advanced laser headlight systems, is a key trend in the automotive industry. This shift towards sustainability is being driven by both consumer demand and regulatory requirements, making it a significant growth area for OEMs.

What are the market trends shaping the Automotive Laser Headlight System Industry?

- Increase in R and D spending on headlight technology is the upcoming market trend.

- The automotive lighting market has seen significant advancements since the introduction of incandescent lights. One such innovation is Organic Light Emitting Diodes (OLED) technology, which was first implemented in the 2016 Audi TT RS. This optional feature offered homogeneous and precise taillights without harsh shadows or reflectors, making it efficient, lightweight, and visually appealing. However, the high cost of OLED technology has limited its adoption to luxury vehicle models.

- Despite the similarities between OLED and Light Emitting Diodes (LED), OEMs like Audi and BMW utilize OLEDs to differentiate their premium offerings. The technology's benefits include energy efficiency, lightweight design, and improved visual appeal, making it an attractive option for the automotive industry's high-end segment.

What challenges does the Automotive Laser Headlight System Industry face during its growth?

- Adoption of LED lighting in automobiles is a key challenge affecting the industry growth.

- The automotive headlamp market is witnessing significant advancements, primarily driven by the pursuit of energy efficiency. LED headlights, for instance, have gained popularity due to their low power consumption and long lifespan. Audi executives have expressed optimism towards LED headlights, indicating a potential delay in the adoption of newer technologies like lasers. Despite the versatility of LEDs and recent discoveries of their applications by competitors such as Mercedes Benz, the rate of laser technology adoption remains uncertain.

- The luxury car segment is expected to witness a rise in LED headlight adoption during the forecast period, posing a challenge to the market as headlights represent a substantial revenue contributor to the global automotive headlight system market.

Exclusive Customer Landscape

The automotive laser headlight system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive laser headlight system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive laser headlight system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ams OSRAM AG - The company introduces advanced automotive laser headlight systems, including NIGHT BREAKER LASER halogen headlights. These lamps deliver exceptional illumination, outperforming minimum legal standards by up to 150 percent. By utilizing laser technology, these headlights ensure superior visibility, enhancing safety and driving experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ams OSRAM AG

- Baja Designs Inc.

- Bayerische Motoren Werke AG

- Continental AG

- HELLA GmbH and Co. KGaA

- Infineon Technologies AG

- Koito Manufacturing Co. Ltd.

- KYOCERA Corp.

- Lazer Lamps Ltd.

- Marelli Holdings Co. Ltd.

- Mercedes Benz Group AG

- Robert Bosch GmbH

- Stanley Electric Co. Ltd.

- Universe Kogaku Inc.

- Valeo SA

- Varroc Engineering Ltd.

- Volkswagen AG

- ZKW Group GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth as the global automotive industry embraces advanced lighting technologies. This market is driven by the increasing demand for improved road safety, energy efficiency, and digitalization in the automotive sector. Laser headlights offer several advantages over traditional lighting systems. They provide longer lighting distance, enabling better visibility for drivers, especially during nighttime conditions. The use of laser diodes in laser headlights results in a high-resolution sensing capability, enhancing the overall driving experience. Moreover, the integration of laser headlights with other advanced technologies, such as night vision cameras and pedestrian protection systems, is gaining popularity.

These systems use photonics-related technologies to enhance road safety and provide better situational awareness for drivers. The automotive industry's shift towards autonomous vehicles is also driving the demand for laser headlight systems. These systems are essential for enabling vehicles to detect and respond to their surroundings in real-time, enhancing the safety and performance of autonomous driving systems. The increasing adoption of intelligent technology in vehicles is another factor fueling the growth of the laser headlight system market. The use of software control, computing, and semiconductor sector technologies in headlight systems is enabling manufacturers to offer advanced lighting solutions that cater to the varying needs of different vehicle segments.

The market for laser headlight systems is not limited to passenger cars alone. The logistics and recreational vehicle segments are also adopting these systems to enhance the safety and efficiency of their operations. The use of laser headlights in light commercial vehicles and buses is gaining popularity due to their long lighting distance and energy efficiency. The global vehicle production is on the rise, and headlamp manufacturers are investing heavily in research and development to offer innovative and energy-efficient lighting solutions. The use of LED-powered lights and phosphorous lenses is becoming increasingly common in the automotive industry, as they offer better energy efficiency and longer lifespan compared to traditional lighting systems.

The retail sectors, including e-commerce, are also playing a role in the growth of the laser headlight system market. The increasing popularity of online sales channels is driving the demand for smart automotive electronics, including advanced lighting systems, as consumers look for innovative features to enhance their driving experience. In , the market is experiencing significant growth due to the increasing demand for improved road safety, energy efficiency, and digitalization in the automotive sector. The use of laser diodes, night vision cameras, and other advanced technologies is enabling manufacturers to offer innovative and energy-efficient lighting solutions that cater to the varying needs of different vehicle segments.

The market is expected to continue growing as the automotive industry embraces advanced technologies and the shift towards autonomous vehicles gains momentum.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 40.54% |

|

Market growth 2024-2028 |

USD 18914.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

29.87 |

|

Key countries |

Germany, China, US, UK, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Laser Headlight System Market Research and Growth Report?

- CAGR of the Automotive Laser Headlight System industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, APAC, North America, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive laser headlight system market growth of industry companies

We can help! Our analysts can customize this automotive laser headlight system market research report to meet your requirements.

RIA -

RIA -