Automotive Touch Screen Control Systems Market Size 2026-2030

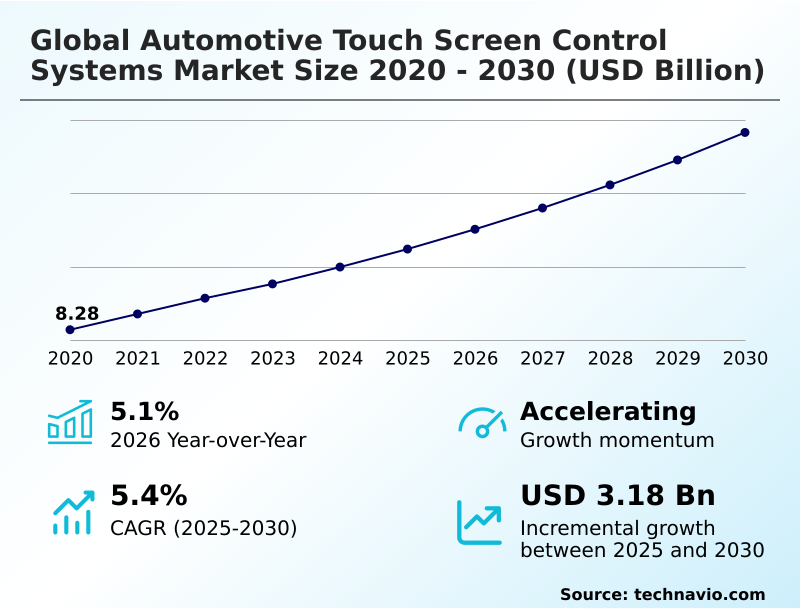

The automotive touch screen control systems market size is valued to increase by USD 3.18 billion, at a CAGR of 5.4% from 2025 to 2030. Integration of advanced visual technologies and high resolution displays will drive the automotive touch screen control systems market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 51.2% growth during the forecast period.

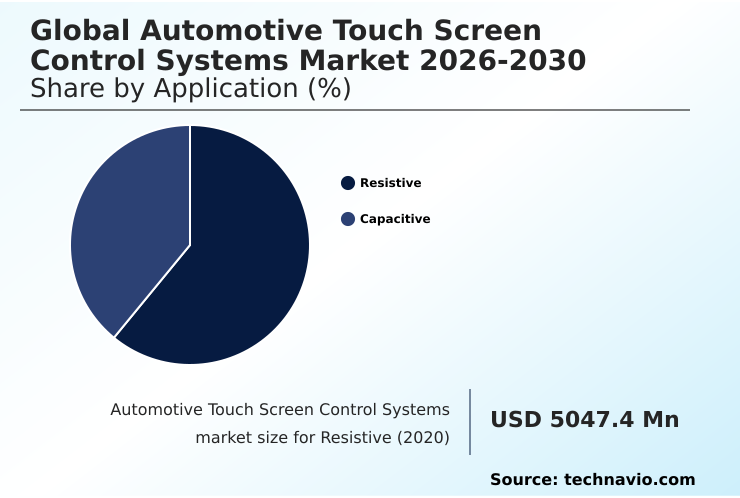

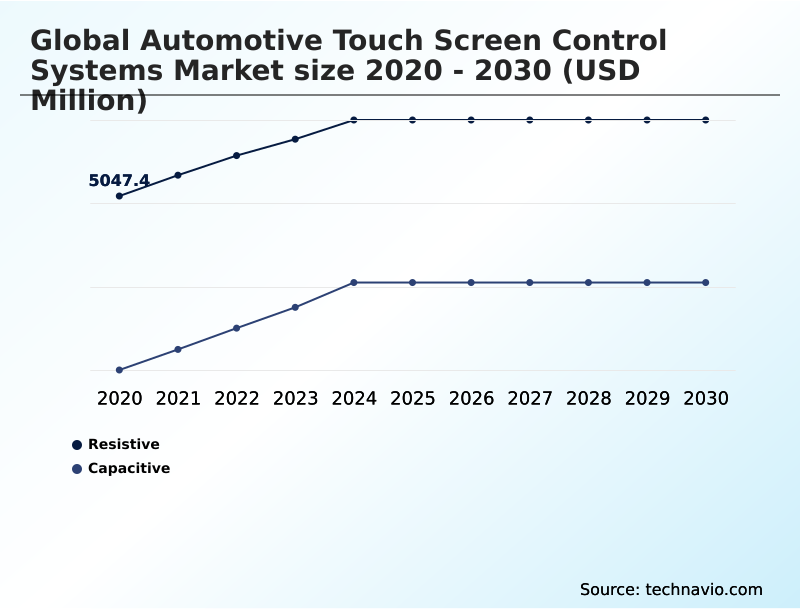

- By Application - Resistive segment was valued at USD 5.84 billion in 2024

- By Vehicle Type - Passenger cars segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.38 billion

- Market Future Opportunities: USD 3.18 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The automotive touch screen control systems market is undergoing a significant transformation, driven by the industry-wide shift to software-defined vehicles and connected digital ecosystems. This evolution replaces traditional physical controls with intuitive, high-resolution surfaces that serve as the central hub for the human-machine interface (HMI).

- Key drivers include the rising adoption of electric vehicles, which favor minimalist interior designs, and consumer demand for sophisticated infotainment that mirrors smartphone functionality. Trends are moving toward expansive, pillar-to-pillar display configurations and the integration of generative AI assistants that offer a proactive user interface.

- For instance, an OEM must now balance the appeal of a large capacitive touch panel with new safety mandates requiring physical controls for critical functions, a decision impacting both cockpit electronics integration and compliance costs.

- This dynamic is compounded by challenges such as ensuring in-vehicle cybersecurity and managing supply chain volatility for key components like the touch screen controller IC, pushing innovation in both hardware and software.

What will be the Size of the Automotive Touch Screen Control Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Touch Screen Control Systems Market Segmented?

The automotive touch screen control systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Resistive

- Capacitive

- Vehicle type

- Passenger cars

- Commercial vehicles

- Distribution channel

- OEM

- Aftermarket

- Geography

- APAC

- Japan

- India

- China

- Europe

- Germany

- France

- UK

- North America

- US

- Mexico

- Canada

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The resistive segment is estimated to witness significant growth during the forecast period.

Resistive screens remain relevant in specific automotive applications due to their operational durability and cost-effectiveness.

This resistive touch screen technology, which operates via mechanical pressure, is ideal for commercial vehicle control system interface designs and entry-level passenger cars where glove-based operation is common. Unlike a capacitive touch panel, it offers high resistance to environmental contaminants.

The integration of advanced touch screen controller ICs now enables multi-touch gesture recognition, bridging the functionality gap with more modern systems.

This evolution, part of a broader push for better automotive display solutions, allows for a single-chip touch solution that improves input accuracy by over 15% in high-vibration environments, ensuring the technology's place within the connected car HMI and smart cockpit architecture landscape.

The Resistive segment was valued at USD 5.84 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 51.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Touch Screen Control Systems Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for over 51% of incremental growth, driven by its robust electronics manufacturing ecosystem and rapid vehicle electrification. This region is a hub for high-performance computing (HPC) and low latency interface development.

Europe focuses on premium cabin aesthetics and ergonomic cockpit design, integrating features like real-time visual control. North America leverages major technology hubs for advancements in creating an empathetic cabin environment and enabling third-party application integration.

The market in MEA is gaining momentum, fueled by smart city initiatives. These regional dynamics highlight a global push towards a proactive user interface and advanced driver monitoring system (DMS), with regional growth rates varying by as much as 2%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of automotive HMI design is a central theme, with a clear trajectory away from simple screens toward complex, integrated systems. The debate over resistive vs capacitive automotive screens is largely settled in passenger cars, but the nuances of functional safety in touch controllers remain critical.

- Integrating AI in vehicle cockpits is no longer a futuristic concept; generative AI in-cabin virtual assistants are becoming key differentiators. This trend is enabled by powerful automotive SoC for digital cockpits and is a core component of software-defined vehicle architecture benefits.

- However, this advancement introduces new challenges, including the need for robust cybersecurity for automotive touch controls and managing driver distraction from complex touchscreens. The impact of pillar-to-pillar displays and large format displays in electric vehicles is reshaping interior design, while automotive touch panel material science advances to improve durability.

- As the market bifurcates between OEM vs aftermarket infotainment systems, the ability to deliver OTA updates for infotainment systems becomes a competitive necessity. This is particularly true for centralized computing in automotive design, which streamlines updates and can reduce production costs, even though the initial cost of automotive touch screen production for these systems is higher.

- The future will likely involve a multi-modal interface for driver safety, combining touch with haptics and voice to address the challenges of touchless gesture control and augmented reality head-up display integration.

What are the key market drivers leading to the rise in the adoption of Automotive Touch Screen Control Systems Industry?

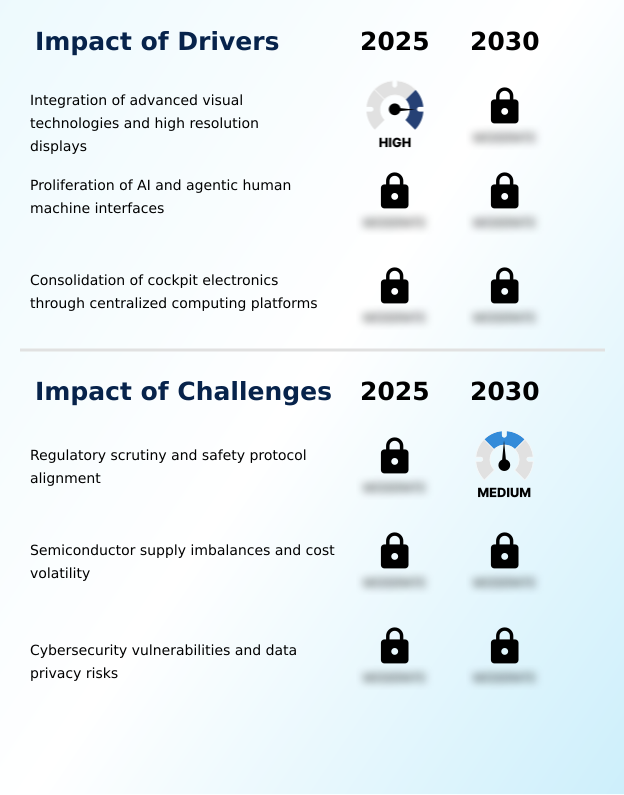

- The integration of advanced visual technologies and high-resolution displays serves as a primary driver, enhancing user experience and differentiating vehicle cabins in a competitive market.

- A key driver is the move toward a centralized computing platform, consolidating infotainment, instrument clusters, and ADAS into a single high-performance unit.

- This approach, integral to the software-defined vehicle (SDV) concept, leverages a powerful automotive system-on-a-chip (SoC) to manage diverse functions. The integration of AI, including large language model integration, enables proactive user interface features that anticipate driver needs.

- This deep integration reduces system latency by 40% and simplifies the automotive software stack.

- The proliferation of AI transforms the display into an active partner, managed by a sophisticated infotainment domain controller and supported by automotive-grade semiconductors and multi-modal user interface designs.

What are the market trends shaping the Automotive Touch Screen Control Systems Industry?

- The integration of large-scale, curved, and pillar-to-pillar displays is a prominent trend. This shift redefines vehicle interior aesthetics and centralizes controls into a single, fluid digital interface.

- The market is shifting towards ultra-wide, curved display architecture and pillar-to-pillar display configurations that redefine the automotive digital cockpit. This trend is driven by the desire for an immersive human-machine interface (HMI) and the centralization of vehicle controls. Advancements in haptic feedback technology and OLED automotive display panels create a more intuitive and premium in-vehicle infotainment (IVI) experience.

- Such advanced HMI development improves user engagement by over 30%. The rise of personalized generative AI assistants and touchless interaction systems is also transforming the automotive user experience (UX), with infotainment hardware modules now supporting complex digital instrument panel technology, reducing menu navigation time by 25%.

What challenges does the Automotive Touch Screen Control Systems Industry face during its growth?

- A key challenge is aligning with increasing regulatory scrutiny and evolving safety protocols, which are designed to address driver distraction caused by complex touch interfaces.

- A significant challenge involves aligning with stringent functional safety (ISO 26262) standards and addressing in-vehicle cybersecurity threats. As vehicles become more connected, the risk of breaches targeting the in-vehicle commerce platform or telematics control unit (TCU) grows, with secure-by-design principles becoming mandatory. The complexity of the automotive software stack, often based on automotive grade linux (AGL), requires robust protection.

- Supply chain volatility for mini-LED backlight components and display driver ICs creates further pressure. Failure to meet new safety protocols can reduce market access by over 15%, while the cost to remedy a cybersecurity flaw is 50% higher than for a mechanical defect. This environment necessitates a focus on flexible cockpit display designs and reliable embedded processing solutions.

Exclusive Technavio Analysis on Customer Landscape

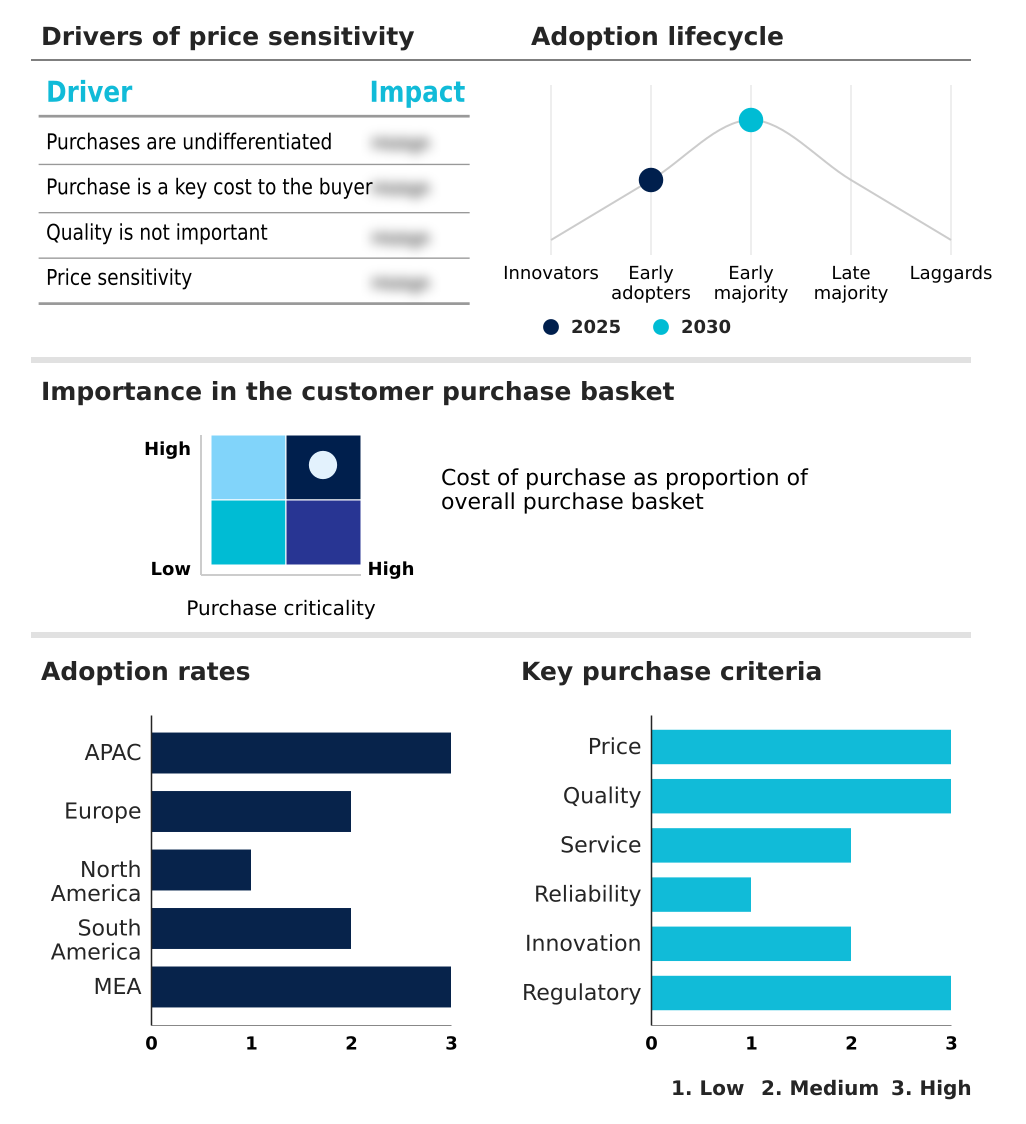

The automotive touch screen control systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive touch screen control systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Touch Screen Control Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive touch screen control systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Analog Devices Inc. - Specializes in single-chip solutions and advanced sensing technologies, delivering intuitive and reliable touch interfaces for diverse in-vehicle applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Analog Devices Inc.

- Continental AG

- Dawar Technologies

- Fujitsu Ltd.

- Infineon Technologies AG

- Kyocera Corp.

- Lascar electronics Ltd.

- LEONHARD KURZ Stiftung and Co.

- Methode Electronics Inc.

- Microchip Technology Inc.

- Orient Display

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Semtech Corp.

- STAFL Systems LLC

- STMicroelectronics NV

- Synaptics Inc.

- Texas Instruments Inc.

- TouchNetix Ltd.

- US Micro Products Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive touch screen control systems market

- In August 2025, LG Electronics announced a strategic initiative to transform the in-cabin environment by forming new content partnerships, aiming to turn vehicles into connected, content-centric spaces with advanced display solutions.

- In October 2025, HARMAN was recognized as a leading connected car solution provider, highlighting its advancements in integrating telematics, satellite communication, and high-performance computing for in-cabin entertainment.

- In February 2025, Microchip Technology expanded its maXTouch family by launching new single-chip touch screen controllers engineered to support large, free-form displays up to 34 inches for advanced smart cockpits.

- In December 2025, Sony Honda Mobility revealed that its AFEELA production model will feature the first in-car integration of PlayStation Remote Play, transforming the vehicle cabin into an interactive digital entertainment ecosystem.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Touch Screen Control Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 3179.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | Japan, India, China, South Korea, Thailand, Indonesia, Germany, France, UK, Italy, Spain, Czech Republic, US, Mexico, Canada, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by the deep integration of advanced hardware and software, creating a highly competitive landscape. The shift towards an automotive digital cockpit is driving demand for pillar-to-pillar display configurations featuring OLED automotive display and mini-LED backlight technology.

- This requires a sophisticated human-machine interface (HMI) with low latency interface capabilities, managed by a powerful touch screen controller IC and graphics processing unit (GPU). A key boardroom decision centers on investing in a centralized computing platform, essential for the software-defined vehicle (SDV) and enabling features like over-the-air (OTA) updates.

- This approach, which reduces development cycles by over 25%, integrates the digital instrument cluster, in-vehicle infotainment (IVI), and advanced driver-assistance systems (ADAS) on a single automotive system-on-a-chip (SoC). Innovations in haptic feedback technology, touchless gesture control, and automotive voice recognition are creating a multi-modal interaction environment.

- Furthermore, the inclusion of a generative AI assistant, leveraging large language model integration, is setting new standards for a proactive user interface.

What are the Key Data Covered in this Automotive Touch Screen Control Systems Market Research and Growth Report?

-

What is the expected growth of the Automotive Touch Screen Control Systems Market between 2026 and 2030?

-

USD 3.18 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Resistive, and Capacitive), Vehicle Type (Passenger cars, and Commercial vehicles), Distribution Channel (OEM, and Aftermarket) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of advanced visual technologies and high resolution displays, Regulatory scrutiny and safety protocol alignment

-

-

Who are the major players in the Automotive Touch Screen Control Systems Market?

-

Analog Devices Inc., Continental AG, Dawar Technologies, Fujitsu Ltd., Infineon Technologies AG, Kyocera Corp., Lascar electronics Ltd., LEONHARD KURZ Stiftung and Co., Methode Electronics Inc., Microchip Technology Inc., Orient Display, Robert Bosch GmbH, Samsung Electronics Co. Ltd., Semtech Corp., STAFL Systems LLC, STMicroelectronics NV, Synaptics Inc., Texas Instruments Inc., TouchNetix Ltd. and US Micro Products Inc.

-

Market Research Insights

- The market is shaped by a confluence of technological advancements and evolving consumer expectations for a sophisticated automotive user experience (UX). The consolidation of cockpit electronics into unified platforms improves functional safety (ISO 26262) compliance by 30%. Innovations in vehicle user interface design are critical, as advanced HMI development now incorporates multi-modal user interfaces and touchless interaction systems.

- The shift towards a smart cockpit architecture, supported by a complex automotive software stack and automotive-grade semiconductors, is paramount. This integration of infotainment hardware modules and automotive display solutions enables features like in-vehicle commerce platforms.

- Such connected car HMI systems, often running on automotive grade linux (AGL), are protected by robust in-vehicle cybersecurity measures and secure-by-design principles, with graphical user interface (GUI) responsiveness improving by 25%.

We can help! Our analysts can customize this automotive touch screen control systems market research report to meet your requirements.

RIA -

RIA -