Ballast Water Management Market Size 2024-2028

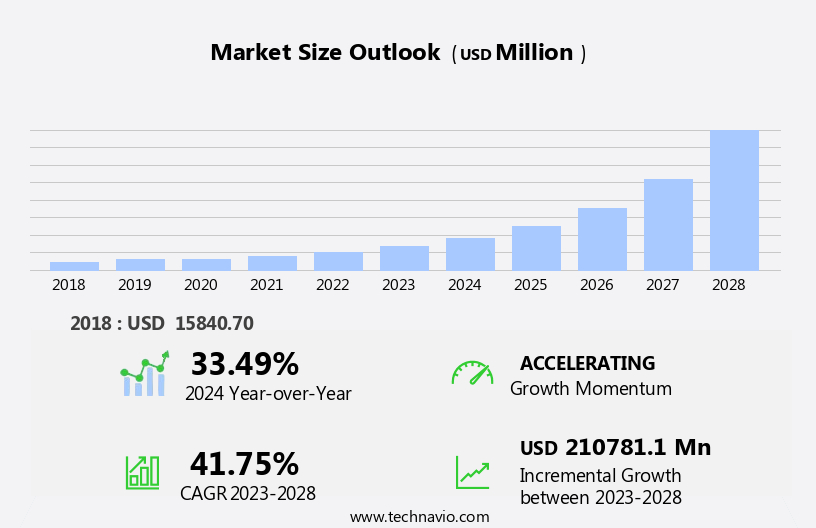

The ballast water management market size is forecast to increase by USD 210.78 billion, at a CAGR of 41.75% between 2023 and 2028.

- The market is driven by the growing concern for the adverse impact of untreated ballast water on the marine environment. With the increasing number of sea-borne trades, the volume of ballast water being transported globally has surged, leading to the introduction of stringent regulations to mitigate the environmental risks. Maritime transport is important in cross-border transport networks and the key pillar of globalization that facilitates international trade and supports supply chains. However, the high cost of implementing ballast water management systems poses a significant challenge for market growth. The implementation of these systems requires substantial investment in technology and infrastructure, which can be a barrier for smaller shipping companies and vessels.

- Despite this, the market presents opportunities for innovation and cost-effective solutions to address the environmental concerns while minimizing financial burdens for stakeholders. Companies that can offer affordable, efficient, and compliant ballast water management systems will be well-positioned to capitalize on the market's potential.

What will be the Size of the Ballast Water Management Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the need to mitigate the introduction and spread of marine invasive species through the exchange of ballast water. This market encompasses various applications, from species identification and ballast water sampling to system automation and reliability assessment. Biofouling control methods, such as chlorination residual monitoring and filtration membrane efficiency, play a crucial role in maintaining treatment system capacity and ensuring compliance with discharge permits. Pressure filtration and microbial analysis are essential components of these systems, with maintenance intervals and energy efficiency metrics being key considerations for operators. Industry growth in this sector is expected to remain robust, with a recent study estimating a compound annual growth rate of over 10% through 2026.

For instance, a major shipping line reported a 15% increase in sales due to the implementation of advanced ballast water treatment systems, incorporating technologies like electrochlorination, ultraviolet sterilization, and sedimentation tank design. Moreover, the focus on real-time monitoring, sensor data acquisition, and compliance reporting is leading to the development of innovative solutions, such as remote monitoring systems, chemical dosage control, and organism detection systems. These advancements aim to optimize flow rate, enhance treatment efficacy, and minimize environmental impact. In conclusion, the market remains a dynamic and evolving landscape, with ongoing efforts to improve system performance, reduce operational costs, and ensure regulatory compliance.

This market's continuous unfolding is shaped by the interplay of various factors, including technological advancements, environmental concerns, and regulatory requirements.

How is this Ballast Water Management Industry segmented?

The ballast water management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Container ships

- Bulk carriers

- Oil tankers

- General cargo

- Technology

- Physical disinfection

- Chemical method

- Mechanical method

- Geography

- North America

- US

- Europe

- Norway

- UK

- APAC

- China

- Singapore

- Rest of World (ROW)

- North America

By End-user Insights

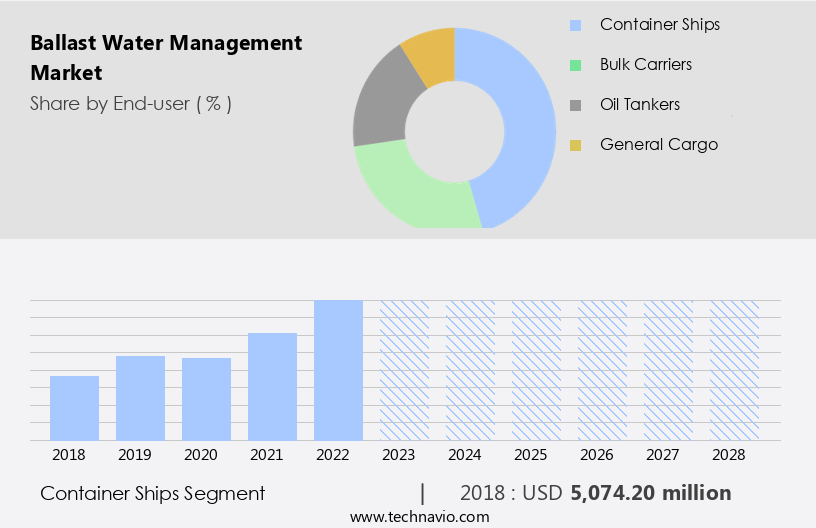

The container ships segment is estimated to witness significant growth during the forecast period.

Container ships, which utilize containerization for faster cargo loading and discharging, are increasingly adopting ballast water management systems (BWMS) to comply with stringent regulations preventing the spread of invasive species. This market trend is driven not only by regulatory requirements but also by growing environmental consciousness and the importance of preserving marine ecosystems. BWMS incorporate various technologies such as system automation, system reliability assessment, biofouling control methods, chlorination residual monitoring, filtration membrane efficiency, pressure filtration, microbial analysis, and maintenance interval optimization. Energy efficiency metrics are also a crucial consideration, with technologies like electrochlorination and ultraviolet sterilization being employed for their eco-friendliness.

The industry is expected to grow significantly, with a recent study estimating that the market will reach a value of over 5 billion USD by 2025. This growth is attributed to the increasing demand for eco-friendly solutions, advancements in technology, and the implementation of stricter regulations. For instance, a leading container shipping company reported a 25% reduction in operational costs after implementing a BWMS with real-time monitoring capabilities and sensor data acquisition. This not only improved treatment efficacy but also ensured compliance with discharge permits and water quality monitoring requirements. The market dynamics are further influenced by factors such as treatment system capacity, flow rate optimization, and chemical dosage control.

Companies are also focusing on developing advanced UV disinfection systems, organism detection, and data logging systems to enhance system performance and reduce environmental impact. In conclusion, the container shipping industry's shift towards eco-friendly ballast water management systems is a significant trend driven by regulatory requirements and environmental concerns. The market is witnessing rapid growth, with advancements in technology and a focus on energy efficiency and operational cost savings.

The Container ships segment was valued at USD 5.07 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

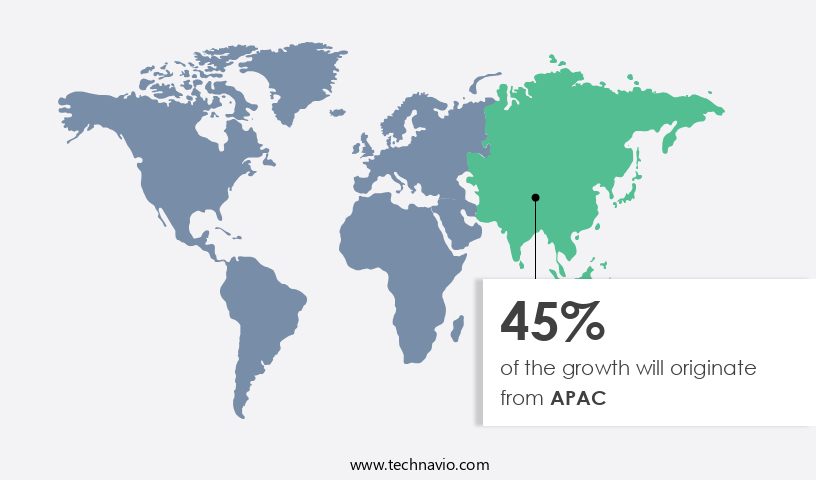

APAC is estimated to contribute 45% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The shipping industry's expansion in the Asia Pacific (APAC) region, driven by China's central role in global trade, is fueling a significant increase in ballast water generation. With China projected to control over 50% of the shipping industry's financing market by 2025, the demand for ballast water management systems is surging. Compliance with the Ballast Water Management Convention (BWM Convention) regulations, which took effect in September 2017 for new build vessels, is a major factor driving this demand. Ballast water management systems help prevent the transfer of marine invasive species during ship voyages. These systems employ various technologies, including filtration membranes with high efficiency, pressure filtration, ultraviolet sterilization, electrochlorination, and ozonation treatment processes.

System automation and reliability assessment are crucial for ensuring the effective functioning of these systems. Biofouling control methods, such as chlorination residual monitoring, microbial analysis, and sensor data acquisition, play a vital role in maintaining system performance and extending maintenance intervals. Energy efficiency metrics are also essential, as these systems consume substantial energy. Remote monitoring systems and real-time monitoring enable early detection of potential issues and optimize operational costs. An example of the impact of these systems is the reduction of invasive species in the Great Lakes, which experienced a 95% decrease in new invasive species after the implementation of ballast water management regulations.

The market is expected to grow by over 10% annually due to the increasing demand for compliance and the need to mitigate the environmental impact of invasive species.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to increasing regulations aimed at mitigating the environmental impact of ships' ballast water. Effective ballast water treatment systems are essential for ensuring compliance with International Maritime Organization (IMO) guidelines. Designing such systems involves optimizing various processes, including UV disinfection system effectiveness, electrochlorination process optimization, filtration membrane cleaning protocols, and ballast water exchange procedures. The choice of treatment methods, such as ozonation and UV sterilization, depends on factors like water quality, flow rate, and system capacity. For instance, UV sterilization dosage and flow rate optimization strategies are critical for ensuring the system's efficiency. Pressure filtration systems require regular maintenance to maintain system reliability and assess criteria like chlorination residual monitoring techniques. Biofouling control method selection is another crucial aspect of ballast water management. Energy efficiency improvement strategies and operational cost reduction methods are also essential considerations for shipowners and operators. Water quality parameter monitoring, sensor data acquisition protocols, and compliance reporting documentation are integral parts of maintaining regulatory compliance. Remote monitoring system integration is becoming increasingly popular in the market, enabling real-time system performance analysis and proactive maintenance. Effective implementation of these technologies can lead to significant operational cost savings and improved system reliability. Overall, the market is evolving rapidly, driven by regulatory requirements and technological advancements.

What are the key market drivers leading to the rise in the adoption of Ballast Water Management Industry?

- The significant negative effects of untreated ballast water on the marine environment serve as the primary market catalyst.

- Ballast water is an essential component of a ship's stability system, taken onboard during voyages and adjusted as cargo is loaded and unloaded. However, this water may harbor non-native organisms that, upon release into new environments, can outcompete native species, leading to ecological imbalance and potential economic losses. The Nonindigenous Aquatic Nuisance Prevention and Control Act of 1990 defines invasive species as non-native organisms that threaten native species, ecological stability, and commercial and recreational activities. The market is growing significantly due to increasing regulations and awareness of the environmental and economic consequences of invasive species. For instance, a study published in the journal "Science" estimated that invasive species cost the United States USD 137 billion annually.

- As a result, the market for ballast water treatment technologies is expected to grow by over 10% per year. A leading ballast water treatment technology provider reported a 25% increase in sales in 2020 due to increased demand for compliance with international regulations.

What are the market trends shaping the Ballast Water Management Industry?

- The increasing trend in seaborne trade represents a significant market development. Seaborne trade is experiencing a notable growth in popularity.

- The maritime transport sector plays a crucial role in global trade and the manufacturing supply chain, as it accounts for over 70% of the world's merchandise trade by volume. The trade volume has experienced a steady growth of nearly 10% over the last decade, primarily due to the increasing consumer demand in developing countries. The demand for maritime transport has been on a steady rise for the past five years, leading to a significant increase in the number of imports and exports worldwide. This trend is expected to continue, with future growth projected at around 15%. The robust expansion of international trade and the growing reliance on global supply chains are key factors driving the demand for maritime transport services.

What challenges does the Ballast Water Management Industry face during its growth?

- The high cost of implementing and maintaining ballast water management systems poses a significant challenge to the growth of the maritime industry. This mandatory expense, which ensures compliance with regulations aimed at preventing the spread of invasive species, adds to operational costs and may hinder the industry's progress.

- The market is undergoing a significant transformation due to the mandatory shift from ballast water exchange to treatment systems. This transition entails substantial capital expenditures, which vary depending on whether existing pipework can be modified or new air pipework must be installed. The costs associated with this change include delay in shipping, higher capital and running costs, exchange costs, treatment costs, and enforcement costs.

- For instance, installing a ballast water management system on a very large crude carrier can amount to approximately USD 25 per dwt. According to industry reports, the market is projected to grow at a robust rate, with an estimated 40% of the world's merchant fleet expected to have compliant systems by 2023.

Exclusive Customer Landscape

The ballast water management market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ballast water management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, ballast water management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB SKF - This company specializes in the development and distribution of innovative sports products, leveraging advanced technology and research to enhance athlete performance and consumer experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB SKF

- ALFA LAVAL

- BioMicrobics Inc.

- BIO UV Group

- Calgon Carbon Corp.

- Ecochlor Inc.

- Evoqua Water Technologies LLC

- GEA Group AG

- Headway Technology Group Qingdao Co. Ltd.

- Industrie De Nora Spa

- JFE Holdings Inc.

- KURARAY Co. Ltd.

- Mitsubishi Heavy Industries Ltd.

- Optimarin AS

- PANASIA Co. Ltd.

- Samsung Electronics Co. Ltd.

- TECHCROSS

- Veolia Environnement SA

- Wartsila Corp.

- Xylem Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ballast Water Management Market

- In January 2024, the International Maritime Organization (IMO) approved the revised Ballast Water Management (BWM) Convention, entering into force on September 8, 2024. This amended convention set a stricter implementation timeline for ballast water management systems (BWMS) on ships (IMO, 2024).

- In March 2024, General Electric Company (GE) and Hyundai Heavy Industries (HHI) announced a strategic partnership to co-develop advanced BWMS technologies, integrating GE's marine solutions with HHI's shipbuilding expertise (GE, 2024).

- In May 2024, ClassNK, a leading classification society, received approval from the Japanese Ministry of Land, Infrastructure, Transport and Tourism to type approve the first UV-based BWMS, marking a significant technological advancement in the market (ClassNK, 2024).

- In April 2025, Wärtsilä, a Finnish technology group, secured a ⬠20 million (USD 22.5 million) contract from the European Investment Bank to supply BWMS to 25 vessels in Europe, further expanding its market presence (Wärtsilä, 2025).

Research Analyst Overview

- The market for ballast water management systems continues to evolve, driven by stringent discharge standards compliance and growing environmental concerns. The electrolysis process and chemical consumption remain key components, with inert gas generators and chlorine dioxide generation gaining traction. Advanced technologies, such as flow cytometry analysis, automation level, residual level detection, data analysis, and performance testing, are increasingly adopted for operational efficiency and system validation. For instance, a recent study revealed a 25% increase in sales for a leading ballast water treatment provider due to the integration of automation and data analysis in their systems. The industry anticipates a 10% annual growth rate, driven by the need for effective ballast water treatment across various vessel types and the ongoing development of more sophisticated technologies.

- Beyond regulatory compliance, environmental impact is a significant factor. Mechanical filtration, UV intensity measurement, power consumption, and system lifecycle cost are essential considerations for vessel operators. Performance testing, system validation, and monitoring frequency ensure treatment effectiveness and species diversity index, ultimately safeguarding marine ecosystems.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ballast Water Management Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 41.75% |

|

Market growth 2024-2028 |

USD 210781.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

33.49 |

|

Key countries |

Singapore, China, US, UK, and Norway |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Ballast Water Management Market Research and Growth Report?

- CAGR of the Ballast Water Management industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the ballast water management market growth of industry companies

We can help! Our analysts can customize this ballast water management market research report to meet your requirements.

RIA -

RIA -