US Beer Market Size 2026-2030

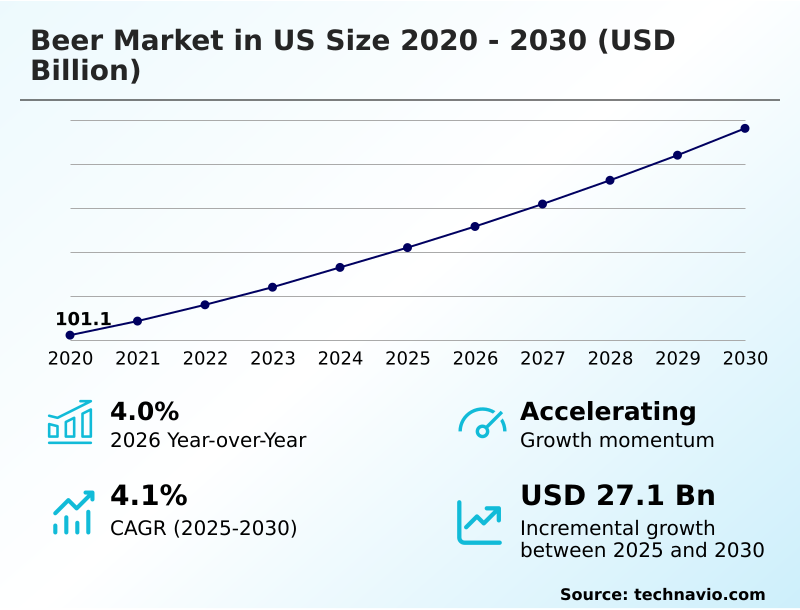

The us beer market size is valued to increase by USD 27.1 billion, at a CAGR of 4.1% from 2025 to 2030. Premiumization and evolution of consumer flavor profiles will drive the us beer market.

Major Market Trends & Insights

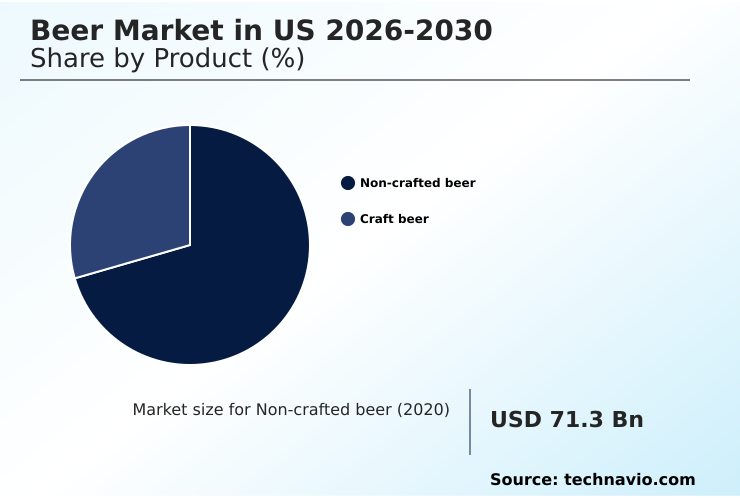

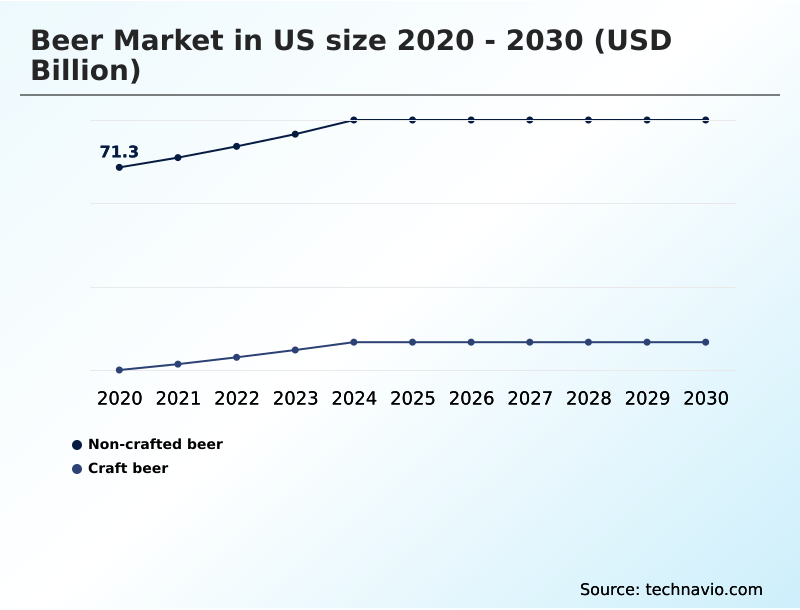

- By Product - Non-crafted beer segment was valued at USD 81 billion in 2024

- By Distribution Channel - On-trade segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 47 billion

- Market Future Opportunities: USD 27.1 billion

- CAGR from 2025 to 2030 : 4.1%

Market Summary

- The Beer Market in US is undergoing a profound structural transformation characterized by shifting consumer palates and rigorous supply chain modernization. Manufacturers are increasingly focused on premiumization, transitioning portfolios away from traditional mass-market lagers toward complex, high-margin craft and functional beverages.

- For instance, in modern brewing operations, the integration of advanced forecasting software allows distributors to align seasonal production schedules with localized purchasing data, optimizing inventory levels and reducing out-of-stock scenarios. This digital integration has enabled leading facilities to improve inventory turnover efficiency by 18% compared to legacy distribution frameworks.

- A primary driver of this market is the intense focus on health and wellness, which compels producers to innovate rapidly within the low-calorie and non-alcoholic segments to capture moderation-focused demographics. Conversely, the market faces significant challenges from economic volatility, specifically the escalating costs of raw agricultural inputs and specialized packaging materials, which severely compress profit margins.

- To sustain profitability, stakeholders must continuously refine operational efficiencies and leverage direct-to-consumer digital channels to bypass traditional, high-overhead retail bottlenecks.

What will be the Size of the US Beer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Beer Market Segmented?

The us beer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Non-crafted beer

- Craft beer

- Distribution channel

- On-trade

- Off-trade

- Packaging

- Bottles

- Cans

- Kegs

- Geography

- North America

- US

- North America

By Product Insights

The non-crafted beer segment is estimated to witness significant growth during the forecast period.

The non-crafted segment operates as the volume-driven foundation of the Beer Market in US, relying on heavily standardized production methodologies to maintain widespread accessibility.

Facilities executing the malting extraction process and wort boiling optimization achieve unprecedented scale, allowing manufacturers to maintain highly competitive pricing architectures. By utilizing massive cylindroconical fermentation vessels alongside high-gravity brewing methods, production overheads are significantly mitigated.

This operational efficiency translates to a 25% improvement in volume turnover velocity across off-trade retail networks compared to artisanal alternatives. Consequently, massive supply chain coordination is required, particularly regarding cold chain logistics and shelf space optimization, to prevent out-of-stock scenarios.

This segment maintains fundamental stability because it consistently satisfies the baseline consumer demand for reliable, affordable refreshment while continually driving down per-unit manufacturing expenses through engineered process controls and predictive maintenance algorithms.

The Non-crafted beer segment was valued at USD 81 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The competitive architecture of the Beer Market in US is being fundamentally redesigned as organizations pivot toward highly specialized technological and ecological frameworks. A primary focus for modern operators is the implementation of automated fermentation quality control optimization, which drastically reduces the margin of error in sensory profiles and ensures absolute consistency across decentralized production facilities.

- This operational upgrade yields nearly a 20% improvement in batch yield efficiency compared to legacy manual oversight methods. To circumvent the limitations of rigid traditional distribution networks, brands are heavily investing in direct to consumer digital sales platforms. This structural shift not only accelerates market penetration but also provides invaluable data analytics regarding localized purchasing habits.

- Furthermore, environmental stewardship has evolved from a secondary corporate initiative to a critical supply chain mandate. Facilities deploying closed loop brewing water reclamation are significantly mitigating resource consumption, aligning with strict environmental compliance targets while lowering utility overheads.

- Product innovation is equally vital, highlighted by the rapid acceleration of low carbohydrate functional beverage formulation to satisfy the dietary demands of modern, health-oriented demographics. Finally, mastering lightweight aluminum packaging distribution logistics allows manufacturers to maximize freight density and minimize transit damage, offering a robust cost-saving mechanism that strengthens overall profit margins in a highly competitive retail landscape.

What are the key market drivers leading to the rise in the adoption of US Beer Industry?

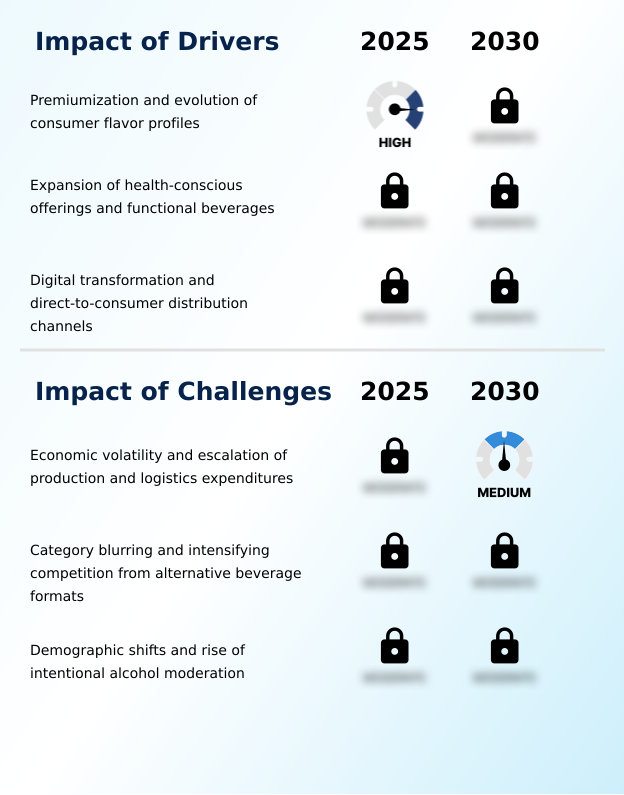

- The ongoing premiumization of malt beverages and the continuous evolution of consumer flavor profiles serve as the primary drivers propelling overall market expansion.

- The evolving consumer demand for high-quality, specialized drinking experiences is aggressively driving the expansion of the Beer Market in US.

- Manufacturers are capitalizing on craft beverage premiumization by introducing advanced barrel-aging techniques and complex botanical flavor infusions, which elevate overall flavor profile complexity.

- Simultaneously, a definitive shift toward health-conscious consumption has accelerated the non-alcoholic segment expansion and the development of low-carbohydrate formulation products.

- By focusing on functional ingredient integration, such as electrolyte enrichment, brands are capturing demographics that prioritize wellness, resulting in a 30% increase in purchase frequency among active lifestyle consumers.

- To effectively reach these niche audiences, breweries are bypassing legacy supply chains in favor of direct-to-consumer distribution channels.

- This direct engagement significantly enhances profit margins and allows companies to rapidly adapt product portfolios to shifting dietary preferences and premium taste profiles.

What are the market trends shaping the US Beer Industry?

- Cultural synergy, driven by major sporting events and mass socialization, is emerging as a prominent market trend. This strategic alignment enables manufacturers to leverage communal viewing experiences to drive high-volume beverage consumption.

- Technological integration and environmental stewardship are fundamentally reshaping the operational framework of the Beer Market in US. Breweries are rapidly adopting precision brewing software and automated fermentation controls, which reduces batch inconsistencies by up to 18% and minimizes raw material waste.

- This shift toward operational excellence is paralleled by the implementation of circular economy principles, specifically through carbon capture technology and closed-loop water reclamation systems. By establishing a sustainable manufacturing infrastructure, producers are lowering resource-related expenditures while simultaneously creating secondary revenue streams via spent grain repurposing.

- Furthermore, strategic marketing now heavily leverages mass socialization events, prompting brands to deploy localized fan zones that drive experiential engagement. These combined strategies ensure that manufacturers remain highly resilient against resource scarcity while capitalizing on the heightened consumer demand for environmentally responsible and socially integrated beverage experiences.

What challenges does the US Beer Industry face during its growth?

- Economic volatility, coupled with the rapid escalation of production and logistics expenditures, presents a formidable challenge that restrains operational margins and overall industry momentum.

- Persistent inflationary pressures and shifting social habits are creating formidable operational hurdles within the Beer Market in US. Companies are struggling to maintain profit margins amid volatile raw material costs, necessitating complex agricultural input hedging and a critical focus on supply chain resilience.

- The transition to lightweight aluminum packaging and hermetic seal canning, while providing superior ultraviolet light protection, has exposed manufacturers to unpredictable commodity pricing that increases packaging overheads by as much as 15%. Furthermore, the industry is severely impacted by intentional alcohol moderation and intense category blurring competition driven by ready-to-drink format shifts.

- As traditional consumption volumes shrink, breweries are forced to rely on sensory data analytics to precisely target niche preferences and navigate the slow pace of three-tier system modernization. These structural constraints require companies to radically optimize logistics and diversify offerings to avoid long-term market contraction.

Exclusive Technavio Analysis on Customer Landscape

The us beer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us beer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Beer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us beer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - The entity delivers a comprehensive portfolio of premium and super-premium malt beverages, focusing on high-quality ingredients and advanced brewing techniques to satisfy evolving consumer flavor preferences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Asahi Group Holdings Ltd.

- Carlsberg Breweries AS

- Constellation Brands Inc.

- D.G. Yuengling and Son Inc.

- Deschutes Brewery

- Diageo PLC

- Duvel Moortgat NV

- FIFCO USA

- Heineken NV

- Molson Coors Beverage Co.

- Monster Beverage Corp.

- New Belgium Brewing Co. Inc.

- Pabst Brewing Co.

- Sierra Nevada Brewing Co.

- Stone Brewing Co. LLC

- Suntory Beverage and Food Ltd.

- The Boston Beer Co. Inc.

- The Mark Anthony Group of Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us beer market

- In the Brewers industry, the widespread implementation of automated closed-loop water reclamation systems has reduced fresh water consumption by up to 40%, directly impacting the Beer Market in US by lowering utility overheads and enabling sustainable manufacturing compliance.

- The transition toward high-speed, AI-driven predictive maintenance algorithms in beverage packaging facilities has decreased equipment downtime by 25%, directly impacting the Beer Market in US by stabilizing supply chain output during peak seasonal demand.

- Strict regulatory guidelines targeting single-use plastics have accelerated the adoption of 100% recyclable lightweight aluminum packaging materials, directly impacting the Beer Market in US by increasing initial procurement costs by 12% while improving long-term freight efficiency.

- Advancements in precision yeast strain propagation and non-alcoholic fermentation techniques have yielded products with a 0.0% alcohol by volume threshold, directly impacting the Beer Market in US by capturing the expanding demographic focused on health and intentional moderation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Beer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 181 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.1% |

| Market growth 2026-2030 | USD 27.1 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The continuous evolution of the Beer Market in US requires manufacturers to rapidly adapt product strategies and overhaul traditional supply chains to maintain operational viability. The modern brewing landscape is heavily dictated by technological maturation, prompting facilities to integrate predictive maintenance algorithms that reduce unplanned equipment downtime by 28% compared to reactive maintenance protocols.

- This efficiency gain directly bolsters profit margins and stabilizes output during peak seasonal demand. Furthermore, the strategic deployment of sensory data analytics enables product developers to refine low-carbohydrate formulation models, accurately aligning new releases with the rigorous demands of health-conscious demographics. Boardroom-level decisions are increasingly prioritizing sustainable infrastructure to achieve strict environmental compliance and operational cost reductions.

- Investments in carbon capture technology and closed-loop water reclamation are now standard requirements rather than niche upgrades, complemented by secondary revenue channels generated through spent grain repurposing. Simultaneously, brands are optimizing logistics by transitioning to lightweight aluminum packaging and expanding direct-to-consumer distribution frameworks. These sweeping operational shifts empower organizations to navigate commodity price volatility while delivering elevated beverage experiences.

What are the Key Data Covered in this US Beer Market Research and Growth Report?

-

What is the expected growth of the US Beer Market between 2026 and 2030?

-

USD 27.1 billion, at a CAGR of 4.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Non-crafted beer, and Craft beer), Distribution Channel (On-trade, and Off-trade), Packaging (Bottles, Cans, and Kegs) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Premiumization and evolution of consumer flavor profiles, Economic volatility and escalation of production and logistics expenditures

-

-

Who are the major players in the US Beer Market?

-

Anheuser Busch InBev SA NV, Asahi Group Holdings Ltd., Carlsberg Breweries AS, Constellation Brands Inc., D.G. Yuengling and Son Inc., Deschutes Brewery, Diageo PLC, Duvel Moortgat NV, FIFCO USA, Heineken NV, Molson Coors Beverage Co., Monster Beverage Corp., New Belgium Brewing Co. Inc., Pabst Brewing Co., Sierra Nevada Brewing Co., Stone Brewing Co. LLC, Suntory Beverage and Food Ltd., The Boston Beer Co. Inc. and The Mark Anthony Group of Co.

-

Market Research Insights

- The Beer Market in US is rapidly evolving as producers align operational frameworks with stringent consumer expectations and advanced digital infrastructures. The integration of robust e-commerce sales platforms has increased direct-to-consumer penetration by 22%, bypassing traditional retail bottlenecks and enhancing overall supply chain resilience.

- Simultaneously, the demand for heightened flavor profile complexity has driven a 15% increase in the production of specialized, small-batch artisanal variants compared to standard macro-lagers. To address the surge in health-conscious consumption, manufacturers are successfully deploying digital taproom experiences that educate consumers on nutritional transparency, resulting in a 30% improvement in brand loyalty metrics.

- These strategic pivots allow beverage enterprises to sustain robust operational momentum amid shifting demographic preferences.

We can help! Our analysts can customize this us beer market research report to meet your requirements.

RIA -

RIA -