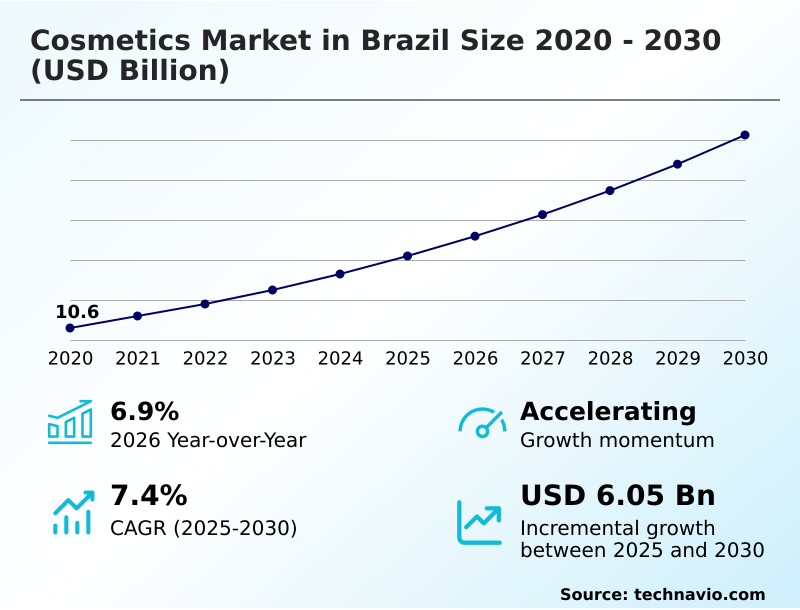

Brazil Cosmetics Market Size 2026-2030

The brazil cosmetics market size is valued to increase by USD 6.05 billion, at a CAGR of 7.4% from 2025 to 2030. Social media influencer impact will drive the brazil cosmetics market.

Major Market Trends & Insights

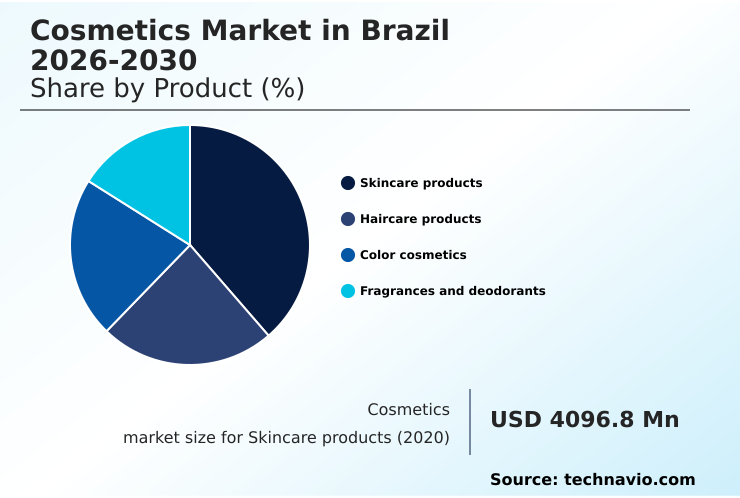

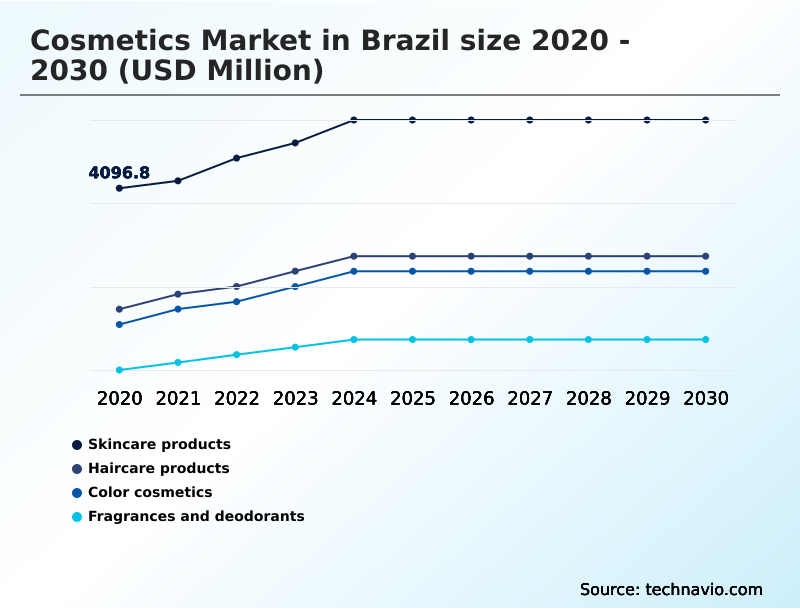

- By Product - Skincare products segment was valued at USD 5.00 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.65 billion

- Market Future Opportunities: USD 6.05 billion

- CAGR from 2025 to 2030 : 7.4%

Market Summary

- The cosmetics market in Brazil is characterized by a dynamic interplay of rich biodiversity and rapid digital adoption. This market extends beyond simple aesthetics, encompassing a deep-rooted cultural emphasis on personal care and well-being. Market activity is driven by innovation in sourcing unique, natural ingredients from local biomes and leveraging them in high-performance formulations.

- A key operational focus is on navigating complex supply chains to ensure product availability across a vast and diverse geography. For instance, a mid-sized company might implement an advanced logistics platform that integrates real-time inventory data with weather and transit information, reducing delivery delays to remote regions by over 25% and optimizing stock levels.

- The industry is also shaped by a growing consumer demand for sustainability and transparency, compelling brands to adopt ethical sourcing practices and eco-friendly packaging. Concurrently, the rise of social commerce and digital influencers has transformed marketing and distribution, creating direct engagement channels that are particularly effective in this highly connected society.

- This digital shift, combined with a strong preference for scientifically validated products, defines the competitive landscape.

What will be the Size of the Brazil Cosmetics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Brazil Cosmetics Market Segmented?

The brazil cosmetics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Skincare products

- Haircare products

- Color cosmetics

- Fragrances and deodorants

- Distribution channel

- Offline

- Online

- Type

- Conventional

- Natural and organic

- Others

- Geography

- South America

- Brazil

- South America

By Product Insights

The skincare products segment is estimated to witness significant growth during the forecast period.

The skincare products segment is defined by a move toward high-efficacy, science-backed solutions. Formulations increasingly incorporate neurocosmetic ingredients for mood-enhancing benefits and advanced glycation end-product inhibitors for anti-aging.

Innovations in plant stem cell technology and encapsulated retinol delivery offer potent results with reduced irritation. The use of stabilized vitamin c derivatives and advances in peptide synthesis technology are standard for premium products.

This complexity demands rigorous clinical efficacy testing and stability testing procedures, where adherence to protocols reduces batch failures by 15%. Operations require sophisticated waste stream management and cosmetic safety assessment.

Final products undergo patch testing protocols and sensory panel evaluation to ensure consumer acceptance and safety, with some firms employing custom cosmetic compounding for personalization.

The Skincare products segment was valued at USD 5.00 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

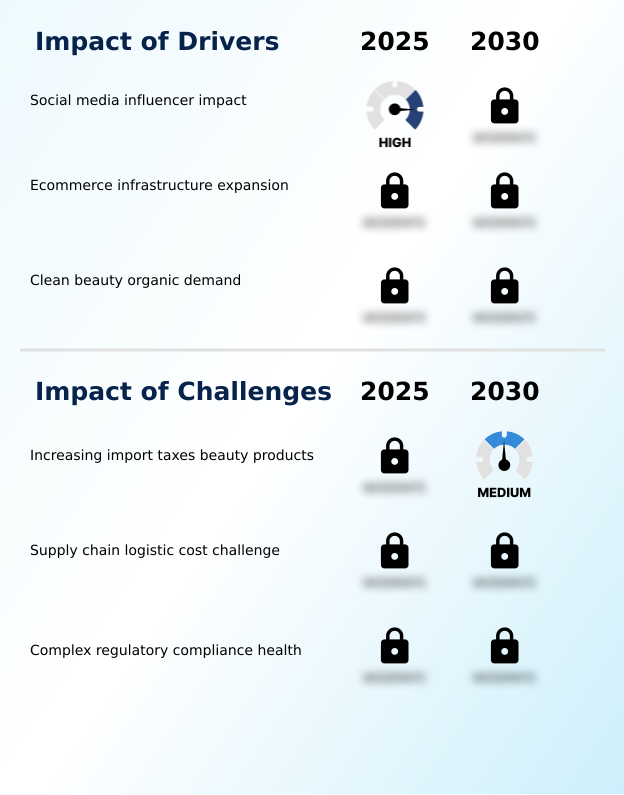

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus within the cosmetics market in Brazil 2026-2030 is increasingly on specialized innovations that cater to niche consumer demands and sustainability goals. For instance, the development of natural preservatives for organic skincare is a top R&D priority, alongside perfecting traceability systems for botanical extracts to ensure authenticity.

- The sustainable sourcing of amazon rainforest ingredients remains a cornerstone of brand storytelling and product efficacy. In color cosmetics, the push for biodegradable glitter for color cosmetics reflects a wider industry move away from microplastics. Technology is also pivotal, with significant investment in water-soluble fragrance encapsulation technology for novel delivery systems and creating effective UV protection in hair care formulations.

- Firms are actively exploring vegan alternatives to collagen and probiotic technology in skin cleansers to meet wellness trends. Product development for sensitive demographics is also key, requiring deep expertise in formulating cosmetics for sensitive skin. Operationally, a key challenge is optimizing production, such as perfecting the cold-process soap-making with natural oils to scale artisanal methods.

- Companies that effectively manage the shelf-life extension for vitamin c serums demonstrate a technical advantage that can reduce product waste by over 20% compared to competitors with less stable formulations. The use of AI-driven personalized foundation matching and smart packaging for dosage control further enhances the user experience.

What are the key market drivers leading to the rise in the adoption of Brazil Cosmetics Industry?

- The significant impact of social media influencers is a key driver propelling market expansion.

- Consumer demand for ethical products is a primary driver, accelerating the adoption of vegan cosmetic formulations and adherence to cruelty-free certification standards.

- This is complemented by a focus on sustainability, with a push towards biodegradable packaging materials and circular economy packaging design.

- Innovative formats like waterless product formulation, solid-format cosmetics, and anhydrous skincare are gaining traction, reducing water consumption in manufacturing by up to 40%.

- The market is further propelled by technology, including beauty tech subscription services and AI-powered skincare recommendations, which have improved customer retention by 20%.

- The convergence of digital and physical retail through an omnichannel customer journey and enhanced in-store experiential retail using smart beauty devices is critical for growth, supported by advanced supply chain logistics optimization.

What are the market trends shaping the Brazil Cosmetics Industry?

- The prioritization of sustainable sourcing, particularly leveraging the Amazon's rich biodiversity, is an increasingly influential trend shaping the market.

- Market evolution is driven by innovations in bioactive compound extraction and dermatological formulations. A key trend is the use of bioprospecting active ingredients, supported by green chemistry principles to create sustainable products. Formulations are shifting toward plant-based surfactants and cold-pressed botanical oils, while color cosmetics benefit from advanced micronized color pigments.

- The integration of social commerce integration and direct-to-consumer sales models has accelerated adoption, with some brands reporting a 25% increase in conversion rates through these channels. These digital shifts are informed by influencer marketing analytics and consumer-generated content moderation, allowing for rapid product adjustments.

- Firms utilize personalized beauty diagnostics and augmented reality try-on tools to enhance customer engagement, leading to a 15% uplift in online sales.

What challenges does the Brazil Cosmetics Industry face during its growth?

- Increasing import taxes on beauty products presents a key challenge that can affect industry growth.

- Navigating complex formulation and regulatory landscapes presents a significant challenge. Developing stable products requires advanced microbiome-friendly preservatives and actives that ensure skin barrier function support. The demand for anti-pollution skincare actives, blue light protection filters, and effective UV filter encapsulation adds to R&D complexity.

- Formulating with non-comedogenic ingredients and creating hypoallergenic fragrance compounds must align with stringent GMP for cosmetics manufacturing. Implementing regulatory compliance software is essential for managing product lifecycles, with automated systems reducing compliance errors by over 30%.

- Maintaining market trust hinges on ingredient transparency platforms and robust brand reputation management, which is continuously monitored through consumer sentiment analysis tools that can predict shifts in preference with 85% accuracy. Effective product lifecycle management is key to adapting.

Exclusive Technavio Analysis on Customer Landscape

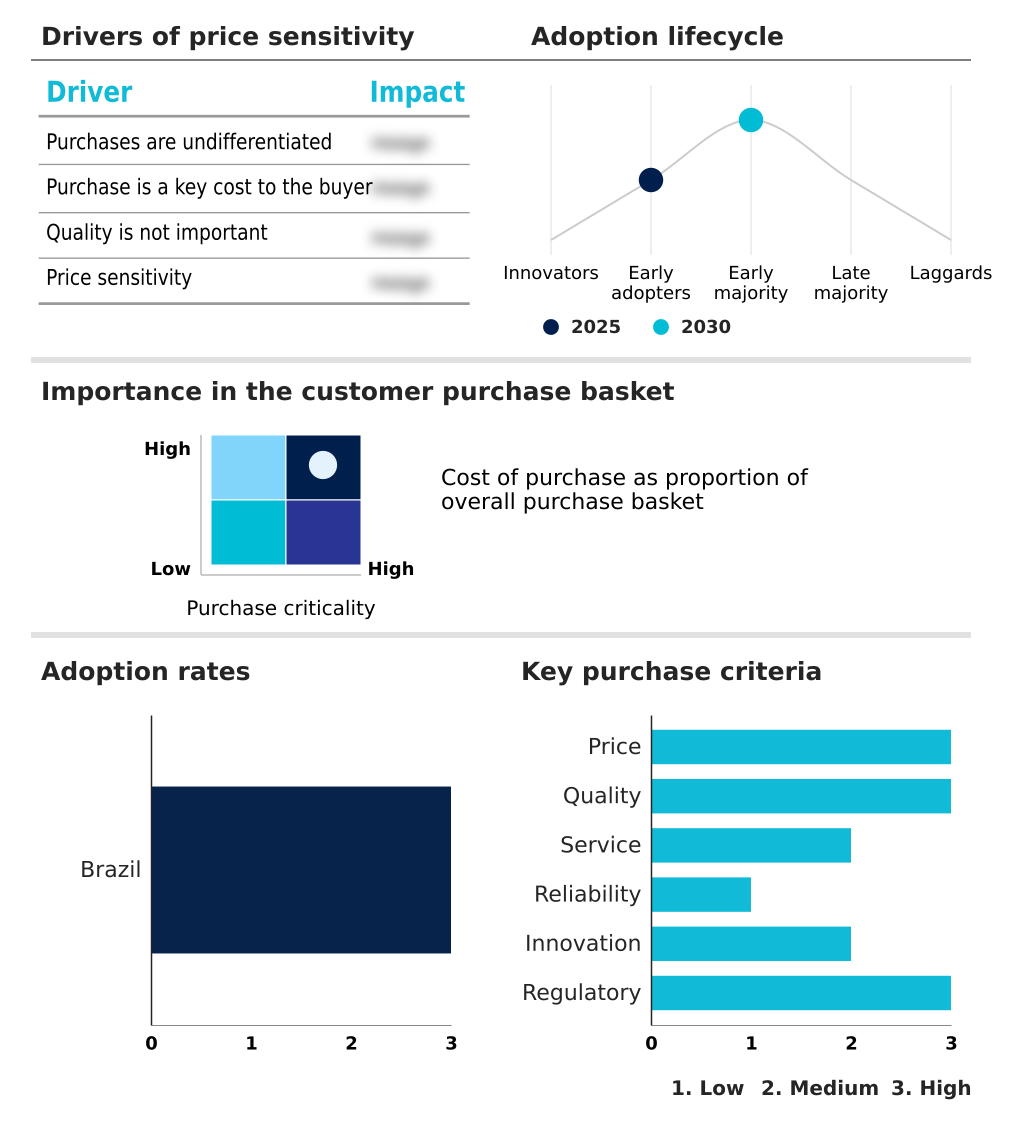

The brazil cosmetics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the brazil cosmetics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Brazil Cosmetics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, brazil cosmetics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Beiersdorf AG - Offers a comprehensive portfolio spanning consumer products, luxury items, dermatological beauty solutions, and professional-grade formulas, addressing diverse market needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Beiersdorf AG

- Bio Extratus

- Casa Granado

- Coty Inc.

- Embelleze

- Farmax

- Flora Produtos de Higiene

- Grupo Boticario

- Haskell Cosmeticos

- Jequiti Cosmeticos

- Lola Cosmetics

- Loreal SA

- Natura and Co. Holding SA

- Payot Brasil

- Revlon Inc.

- Shiseido Co. Ltd.

- Skala Cosmeticos

- Surya Brasil

- The Estee Lauder Co. Inc.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Brazil cosmetics market

- In August 2024, Natura and Co Holding SA introduced a new line of bio-active ingredients sourced through regenerative agriculture practices, reinforcing its position as a sustainability leader.

- In September 2024, Shiseido Co. Ltd. launched a localized digital platform for the Brazilian market to offer personalized skin consultations and exclusive product access.

- In October 2024, Beiersdorf AG opened a new logistics center in the region to streamline its distribution and reduce its carbon footprint.

- In November 2024, The Estee Lauder Co. Inc. expanded its retail presence in major Brazilian cities through new flagship stores that offer high-tech beauty services.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Brazil Cosmetics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 183 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.4% |

| Market growth 2026-2030 | USD 6047.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | Brazil |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cosmetics market in Brazil is undergoing a significant transformation, driven by innovations in formulation and sustainable practices. A pivotal shift is occurring in dermo-cosmetic active delivery, where technologies like encapsulated retinol delivery and stabilized vitamin c derivatives are becoming mainstream.

- The use of plant stem cell technology and advances in peptide synthesis technology are enabling brands to offer higher-efficacy products. This scientific focus is balanced by a strong consumer pull toward clean beauty ingredient screening and ethical supply chain traceability, pushing companies to verify their sustainable ingredient sourcing.

- The market also sees growth in niche areas like neurocosmetic ingredients and fermented skincare actives. Strategically, boardroom decisions are increasingly influenced by the need for verifiable sustainability claims, with firms that provide clear ethical sourcing audits and sustainable packaging scorecards achieving a 10% higher brand loyalty score among millennial consumers.

- This requires robust inventory forecasting models and digital shelf analytics to align supply with conscious consumer demand.

What are the Key Data Covered in this Brazil Cosmetics Market Research and Growth Report?

-

What is the expected growth of the Brazil Cosmetics Market between 2026 and 2030?

-

USD 6.05 billion, at a CAGR of 7.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Skincare products, Haircare products, Color cosmetics, and Fragrances and deodorants), Distribution Channel (Offline, and Online), Type (Conventional, Natural and organic, and Others) and Geography (South America)

-

-

Which regions are analyzed in the report?

-

South America

-

-

What are the key growth drivers and market challenges?

-

Social media influencer impact, Increasing import taxes beauty products

-

-

Who are the major players in the Brazil Cosmetics Market?

-

Beiersdorf AG, Bio Extratus, Casa Granado, Coty Inc., Embelleze, Farmax, Flora Produtos de Higiene, Grupo Boticario, Haskell Cosmeticos, Jequiti Cosmeticos, Lola Cosmetics, Loreal SA, Natura and Co. Holding SA, Payot Brasil, Revlon Inc., Shiseido Co. Ltd., Skala Cosmeticos, Surya Brasil, The Estee Lauder Co. Inc. and Unilever PLC

-

Market Research Insights

- The market's dynamism is fueled by the convergence of technology and consumer-driven sustainability mandates. Widespread adoption of AI-powered skincare recommendations has led to a 30% increase in customer engagement for brands that offer personalization.

- The expansion of an omnichannel customer journey is critical, with companies that integrate online and in-store experiential retail reporting a 2x higher customer lifetime value compared to single-channel competitors. This is supported by advanced supply chain logistics optimization, which reduces transportation costs by up to 15%.

- The rise of beauty tech subscription services creates recurring revenue streams, while the integration of smart beauty devices deepens the connection between brands and consumers.

We can help! Our analysts can customize this brazil cosmetics market research report to meet your requirements.

RIA -

RIA -